AUM is constant at around 60K Cr. There is an increase in retail assets by approx 11K cr YoY and a similar amount of decrease in Wholesale book and hence no growth in assets is seen. Few points to be noted

Wholesale book yield is around 10.3% while Retail book yield is around 14.5%. With mix changing their yields should increase but seems like its very near to peak now

Retail asset growth is approx 50% YOY with sequential growth in Q4 at 25% which is quite encouraging

Opex Cost is approx 3.7% of AUM because of manpower and branch expansion. Last year it was 2% which has removed approx 1KCr from PBT

Interest cost is approx 8.6% with 59% liabilities at fixed interest rates

GNPA in retail portfolio need to be watched out for. Currently, they have provisions of just 600Cr on the retail book of 31Kcr. These need to be assessed in the coming quarters in terms of tenure and quality of assets.

At approx 15% YOY asset growth, opex cost of 3.5% of AUM and GNPA in line with Q4FY23, stock is trading at forward PE of 13 for FY24.

While stock appears a very good bargain in book value terms things that need to be watched out for are

a) Asset growth & quality

b) Deployment of surplus liquidity

Was thinking about PEL’s profitability metrics as % AUM for FY23 and trying to see where they could go from here in FY24

FY24

Net total income as % AUM for FY23 = 6.75% (NTI = Total income - total interest & fee related costs; Ignored 700Cr one time income from Shriram). In FY24 with yields expanding via retail and assuming borrowing costs, can come down by another 60-75bps from 8.6%, the overall NTI should be able to expand by 1.5-2% IMO. So NTI as % AUM would be say 8.5%

Guidance for opex costs = 3.5%-4% (Retail share increasing)

Most generous assumption on credit costs = 2%

PBT as % AUM = 2.75%

PBT as % B/S Assets = 2.4% (Assuming same ratio of total assets to AUM in FY24 as in FY23)

PAT as % B/S Assets = ROA = 1.8%

Assuming leverage increases from current 1.6x to 2x, ROE = 5.5%

What valuation should be commanded by a lender doing 5.5% ROE at the peak of the credit cycle with 1/3rd book still being in mid to big ticket RE? PEL seems cheap for a reason. Happy to hear and learn from contra views.

I’ve been struggling with the same dilemma for some time. I couldn’t come to a Story where their ROE beats their COC.

The pulldown on their ROE is from low Leverage and High Opex. Increasing leverage is a two edged sword, your NII falls and this is a company which is keen to hold onto the excess cash from increase in leverage rather than do buybacks even when P/B was ~0.6.

But Jairam sounds like a guy who knows stuff at least in the concalls it looks like that. Would love to hear feedback about him if anyone has any.

Bet should be on Jairam/Management to turnaround, their 50% Stage 1 wholesale book is due in the next 2 years. I was surprised to see this Qtr that even with all the risk that the earlier Piramal Management was taking with RE Lending the Yields on that book were just 10.3%.

You should factor the increase in Yields with Credit mix shifting with time, that should make a case where the current Valuations can give an okayish IRR over years if they’re able to wind up their Wholesale book well and not replace it with similar risky assets.

Some thoughts and queries on the Piramal-DHFL deal:

Piramal had issued ten-year bonds to the tune of Rs 19,500 crore with a coupon of 6.75 per cent to the lenders of DHFL in 2021.

These bonds are being redeemed at the rate of 2.5 per cent every six months and the face value of the bond is now Rs 925 each (Rs 75 having been paid out over the last 18 months.) If I am not mistaken PEL should have paid around Rs 1316 crores by way of bi-annual interest on the bonds in the first year, tapering down to around Rs 1100 cr in Sept-2023. The company would also be shelling out Rs 1950 cr at the end of the first two years by way of redemption of principal.

Won’t such huge payouts stretch PEL’s P&L account? Also has the DHFL acquisition begun paying for itself.

The bonds themselves are available in the market at a yield of 10.83 per cent.

dis: holding PEL. took a small SIP of the bonds today.

Why would the bond repayments stretch the P&L? Or do you mean the Balance Sheet?

Also, have they disclosed how many of the bonds they were able to buy back? They had booked some profit on account of buyback of bonds.

by default 2.5 per cent of the bonds would be redeemed every six months. The bonds with face value of Rs 1000 at the time of issue now has an FV worth Rs 925 only. however each bond is being traded at Rs 790.02 plus accumulated interest of Rs 10.95 = 800.87.

I am guessing the six-monthly interest and the redemption amount is being paid by PEL from its P&L account. I may be wrong also. I am not well-versed in accounting.

Because the yield is so high buying back such bonds is actually beneficial for the borrower(PEL). You get 1000 from a loan and you buy it from someone at 750(hypothetically) so net net you saved 250.

Its actually P&L accretive in the short term, in the medium term if they have to raise capital from the markets then the markets would price their new Bonds at much higher yields than the DHFL bonds because of ongoing higher Interest rates and Risk pricing PEL’s past history.

When buying DHFL from lenders they had the upper hand since the lenders were happy to get anything for their capital lent to DHFL asap.

The value of property investment in the BS has increased to 2310 Cr from 1335 Cr last year. This property is the andheri land I believe. The value has been increasing every year. However, there is no discussion (rather no questions, and hence no answers) on the quarterly calls regarding the status of the project and its monetization. I tried to reach the IR to seek clarifications, but found that they dont want to share much details, they were not even ready to share precise project name and location. I found the IR/company is not minority shareholder friendly.

If someone knows someone working in any institution, would be great to put this query across. The company keeps claiming that there are pockets of value unlocking in the balance sheet, this Andheri land is one of them.

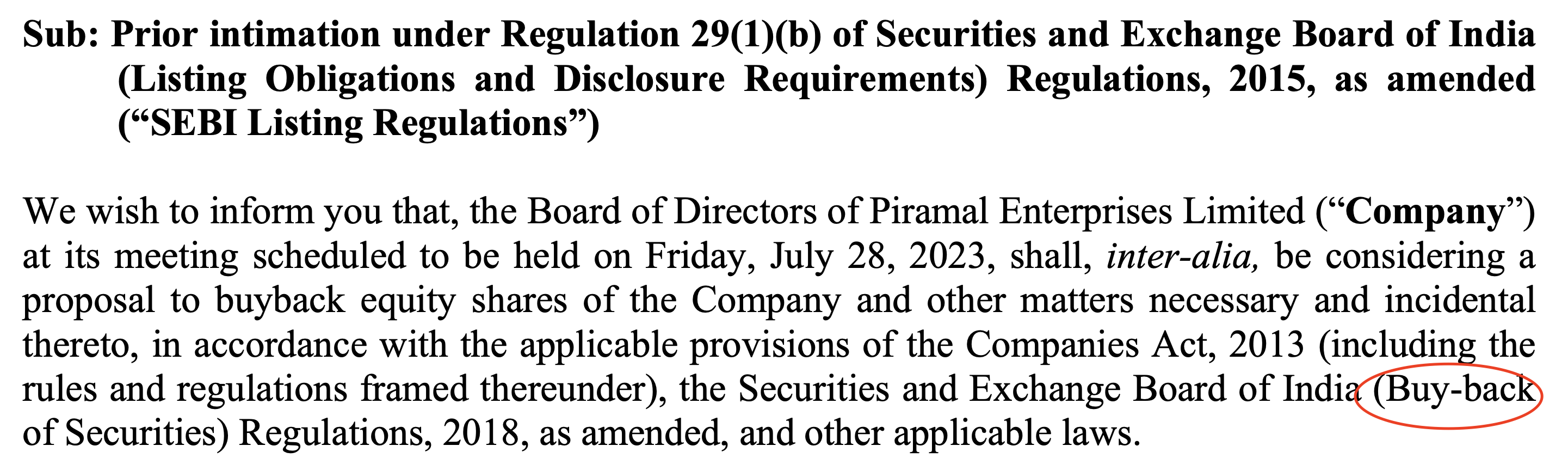

This is encouraging. However PPL Pharma has announced a rights issue and may announce the offer price by end of this week. So for promoters is it more about using the buyback money to participate in Pharma rights issue?

In any case I think this shud help PEL, hope they have good results as then buyback is really a smart move

Good news is that promoters are not participating in the buyback, thereby showing their confidence in the company. Mr. Piramal clarified on the concall today