Piramal Pharma Con call notes.

-

Margin improvements to come from higher sales and operating leverage

-

Aspire to move towards 25-26% range across all businesses over the medium term (3 to 5-year target). Q0Q margin improvement.

-

Delayed decision-making for RFP.

-

CDMO-

- Combination of capacity investment with client late-stage commercial work. molecule progression

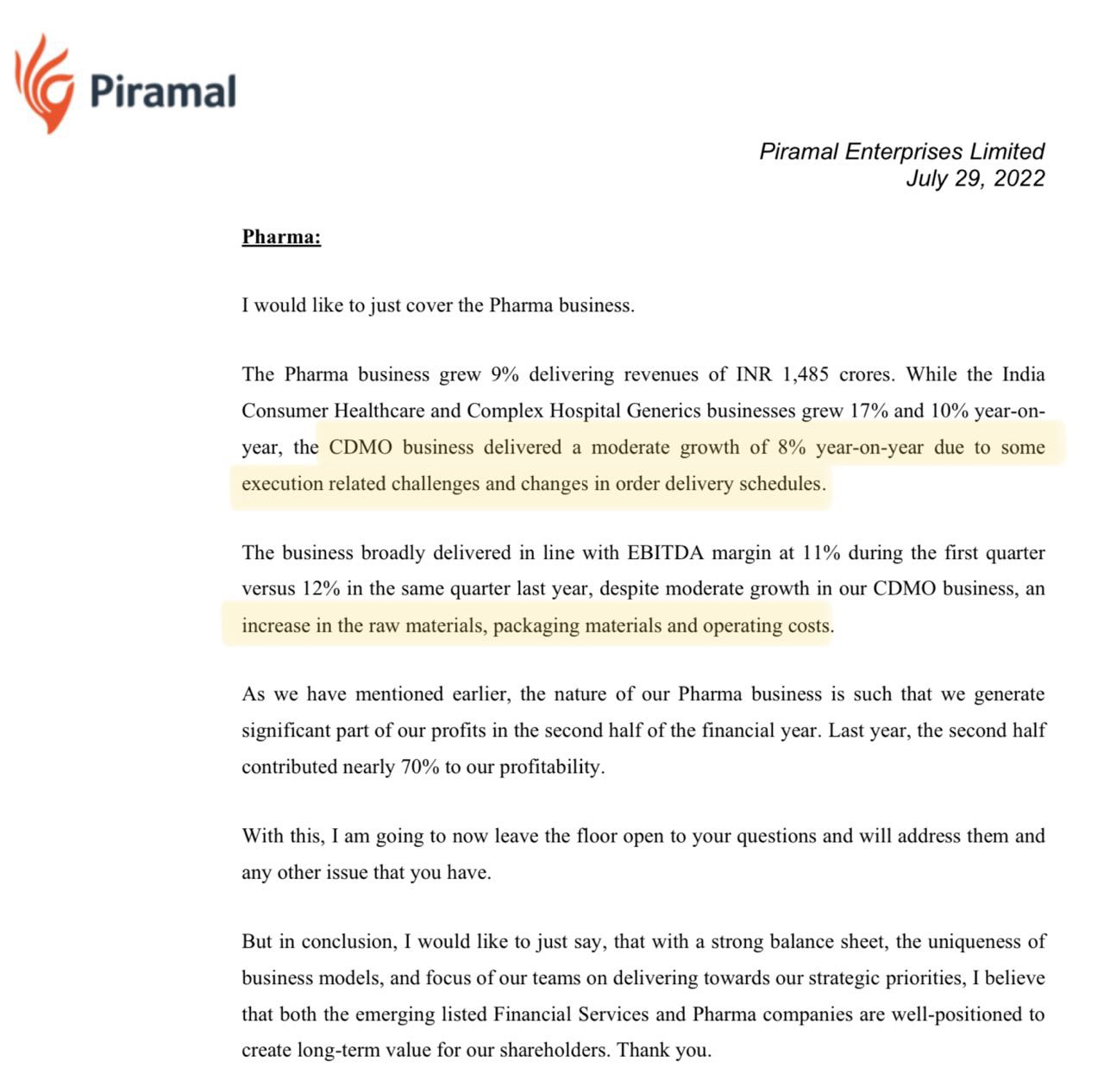

- Overall growth should be higher than in the past.

-

Hospital

- Still far from fully utilising potential

- Increasing market share

- Increasing further backend capacity/capabilities

- Gaining more

- Continue to progress same products to be sold to the same channel.

-

ICH

- Investing 15% of the top line in investing for growth

- With scale increase profitability

-

Margin Drop recently

-

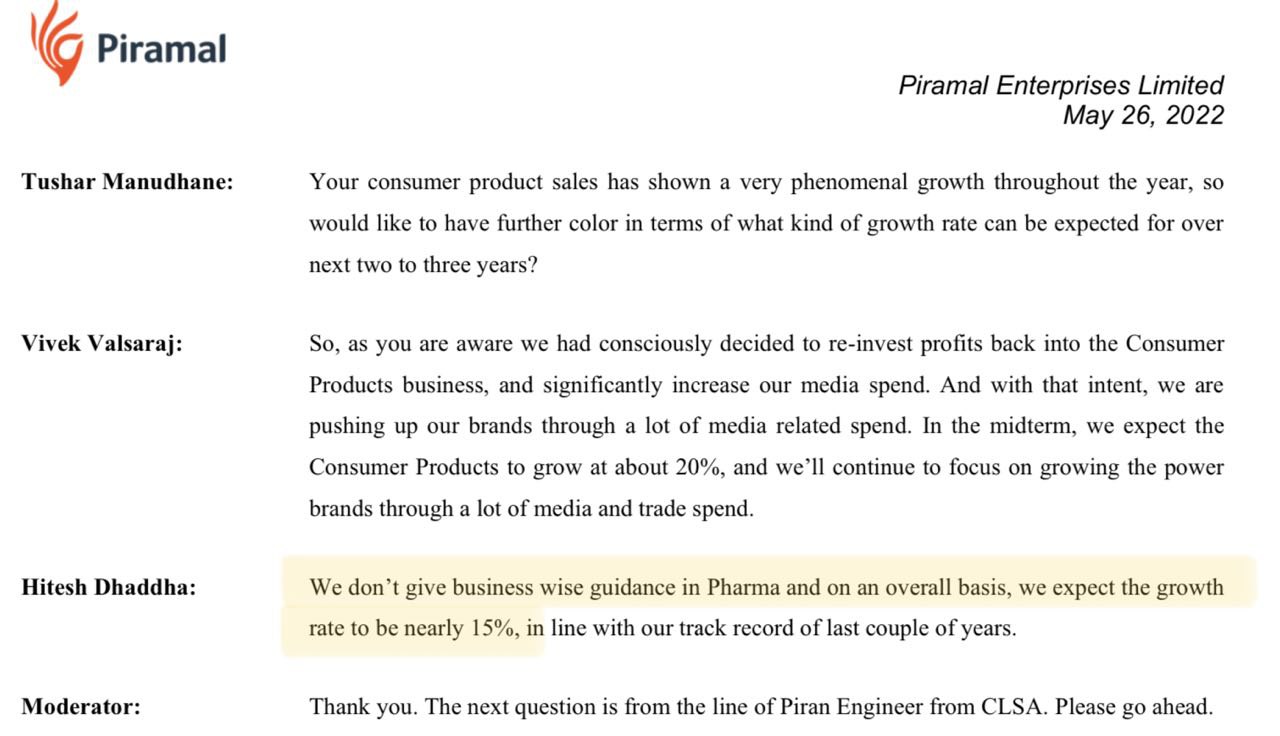

ICH profit reinvestment. Investing in sale promotion

-

Inflation and Input cost lead to margin compression.

-

CDMO- Fix cost leverage business.

-

Some sales are won on PEL name.

-

Max debt 4-4.5 EBITDA. 4300 cr net debt.

-

No plan to raise capital as of now. Existing profits are enough to pay off debt.

-

We will go with what the customer want. If they want from the US, we will serve them from the US. No intentional plan to compel clients to purchase from India.

CDMO

- 60% API and 40% formulations

- More proposals are coming for the phase 3 molecule. Earlier phase 1/2 projects were more, but now more requests are for phase 3 molecules. Generally, phase 3 decision takes a long time.

- 19 patents products.- This should grow at a faster rate than other segments.

- Margin expansion will happen due to the top line as it is operating

- leverage business.

- Following the trend playing out in CDMO

- An increasing number of queries are related to China +1 strategy

- Due to cost, companies are looking at east to reduce cost

- Innovator molecule- looking for onshore/western market.

Hospital

- Inhalation market share- low to mid-teen globally. A lot of scope for improvement.

- Difficult for new competitors to enter into the Inhalation segment and sustain.

ICH

- Breakeven margin

- Once we get to 1000cr, we should see show increment in profit.

My Take:

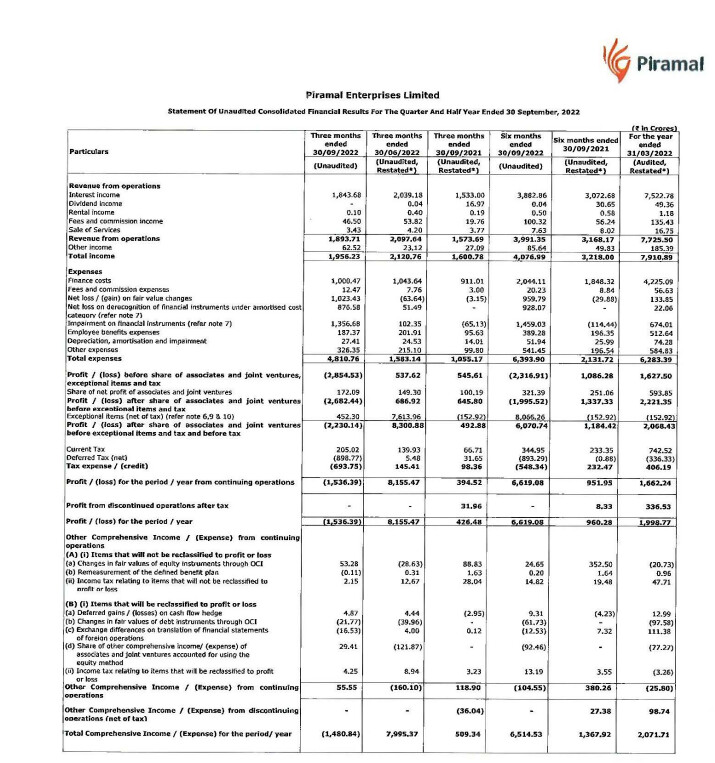

CDMO is a scale business where operating leverage is significant. PPL has chosen to expand manufacturing capacities across the world as compared to other CDMO players in India, having mainly Indian manufacturing. As a result, PPL has considerably less margin generally. It looks like they suffered badly in Q1/Q2, but their profitability was not visible due to merging with PEL. Many( myself included) did not know that PPL had a Q1 loss of 139 cr.

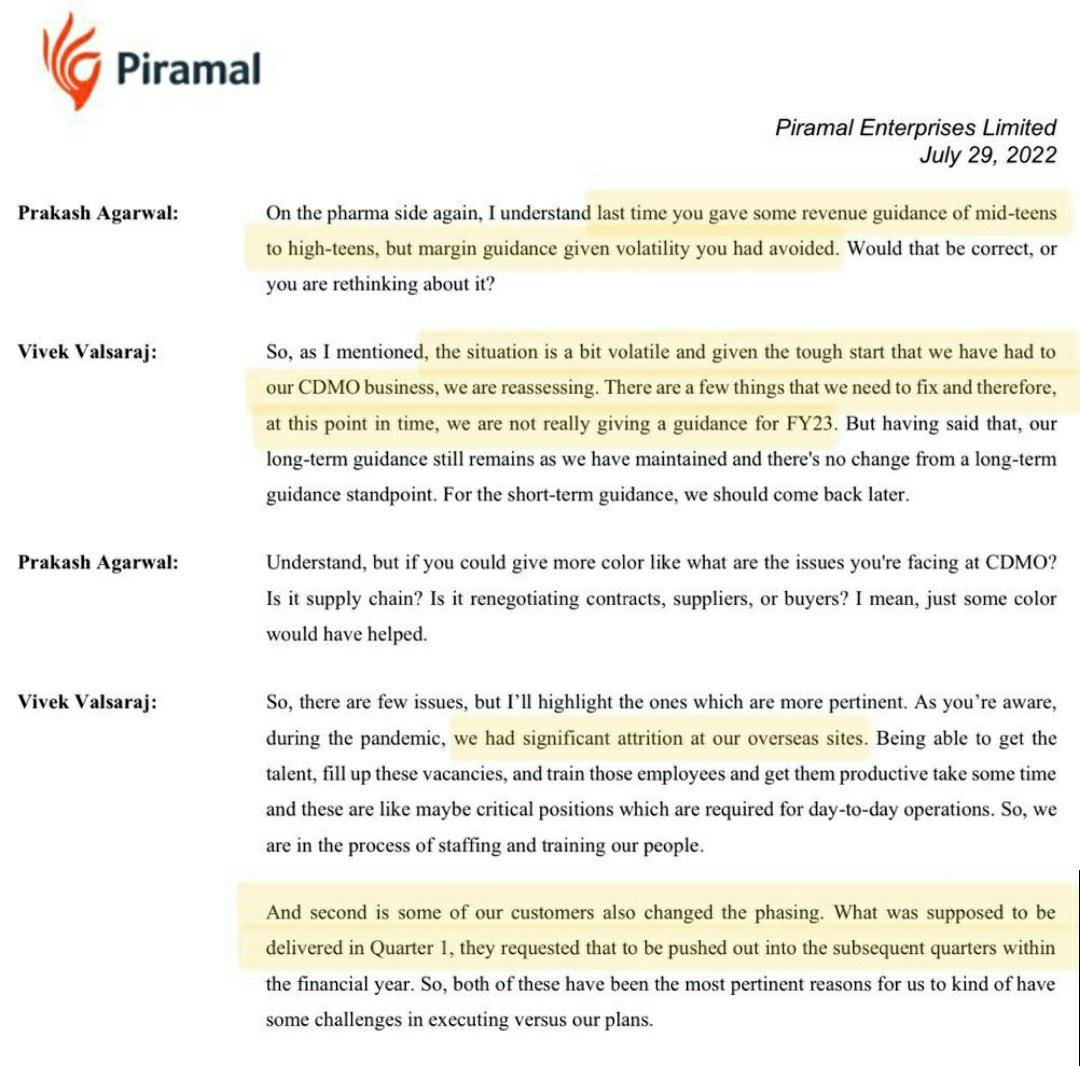

The more they sell, the better is profitability. Additionally, they are doing Capex considerably for CDMO, which will get completed in the next 18/24 months- assuming by March 24. Then it will slowly start getting validated/used, so profitability will take some time to reach a better level. They have been loss-making for a few quarters, and so hopefully, they will turn the corner. They indicated higher sales in H2, so hopefully, CDMO will turn around and shows a profit on a much more consistent basis.

They have around 19 molecules in phase commercial, and as more molecules move into commercial, it will drive their revenue/profit. They have indicated that they are seeing most of the RFP in phase 3 molecule, which augers well for the future.

Due to funding issues with starts up, I am sure it would have impacted emerging biopharma companies- which contribute decently to their revenue. So I feel this could have impacted them, but management has not highlighted that already. But if one sees it on Google, this trend is visible.

So, CDMO is going through a tough phase as they are working on rectifying the situation.

The hospital business seems to be a better place. They launched one product and are ready to launch 8 more in H2. These new products are unlikely to make a significant dent in H2, but it will augur well for the coming years. Management gave a hint about competitive intensity. There was only one major player who entered this space after their entry a few years back. They remained sidelined despite trying various things. As they(the new competitor) could not make headway in the Inhalation Anastasia segment, they eventually gave up. So it seems that it is comparatively difficult to enter in that segment.

ICH- Looking at the current rate, this segment could hit 900 cr this year and 1000 + cr next year. Currently, it is operating at a break-even level as it is reinvesting the profit into a growing power brand, which is reflected in its increased spending on Sales and marketing for this section.

PPL indicated that they would gradually turn toward profitability once they reach 1000 cr sales. So FY23 will break even, and Fy24 could be a lot similar to FY23. However, from FY25, they shall be reporting some decent profitability. It means ICH profitability is away at least 7/8 quarters based on current understanding. As PPL report consolidating EBITDA, this will hamper their overall profitability.

Con Call audio

PDF Transcript of Con Call

Note- Invested. Posted it here as there is no separate thread