I think two things may be happening with the stock. Earlier, PEL consisted of Financial Services + Pharma. Some of the investors may be interested only in Pharma. They may be exiting their position as PEL is separated, causing the price to correct sharply in the last few weeks.

At the same time, there are NOT many positives in the stock(other than the valuation mentioned above).

If investors ask " What is the PEL stock now to buy?", there are not many positive answers, other than valuation point which is highlighted above by @Ravi_Hingarajiya

Cons:

- Wholesale exposure is still 65%. Real estate wholesale exposure is a bad word for NBFC. NBFCs that have wholesale exposure have/are suffering. Edelweiss is one of them. IIFL Finance is reducing its wholesale exposure, though it is 3-5% of its overall loan book.

- PEL is aiming to make Retail one-third in the next five years, but that is a long shot from today, so not sure how this plays out. Five years back, PEL was going full steam on wholesale lending and aiming to start a high-value mortgage business. Incidentally, they are curtailing both of them now. Five years is a long shot

- DHFL book market has apprehension as it is not tested (not long enough) for PEL yet.

- PEL does not provide much info on AIF/Insurance business, so we cannot say much about it.

NBFC’s competitive nature is also changing. RBI is imposing more and more regulations on NBFC, making their life a little hard. As a result, competition is also reducing. At the same time, Banks and Fintech players are also eating their lunch. So it is becoming competitive by the say.

In Wholesale, PEL seems to be ok with the Real estate business, but their non-real estate business has suffered badly in the last couple of years. However, looks like the economy is back on track, so non-RE should fare ok going forward (hope).

It looks to me that they do not have many downsides. How much down can it go? It can certainly go down a further 10/20%, but sooner or later, the market will realize the value (if they do not do another swing quarter).

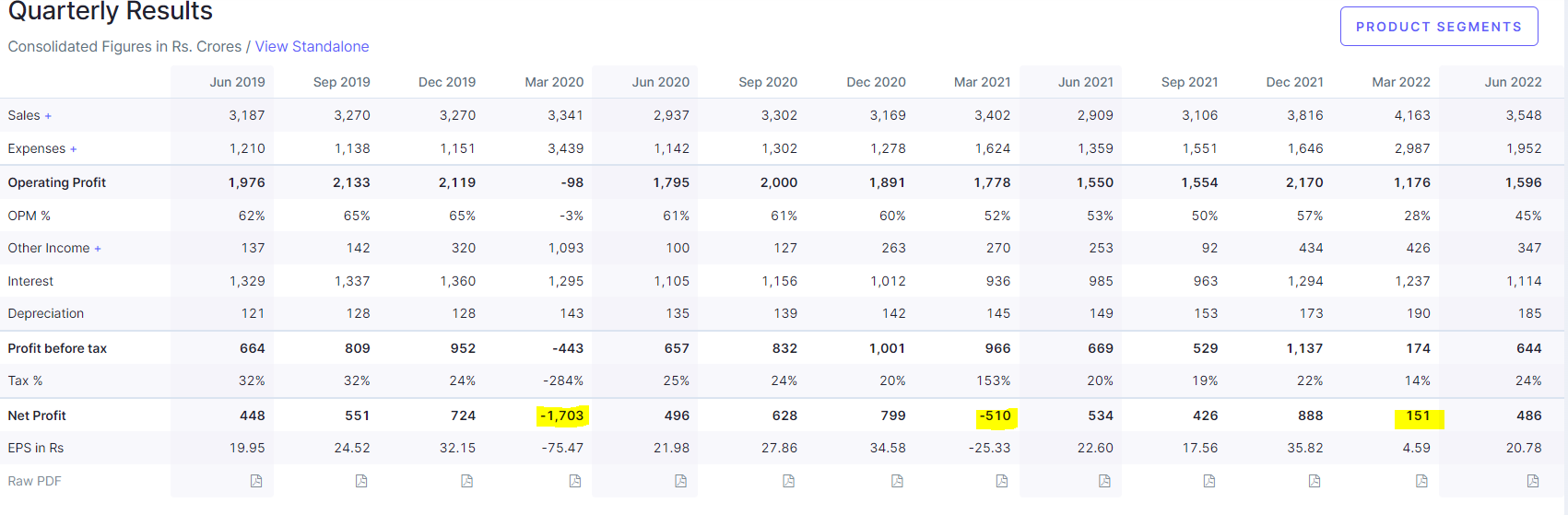

Historically, Q4 has been very volatile and brought in wild fluctuations in profitability.

As PEL is separated, I hope that they have sorted the book reasonably well and starting the new inning on a relatively clean slate. Of course, there could be some write-offs, but I think they have reached the bottom.

For COVID, they provided 2000 cr+, but around 1900 cr + was still unutilized (I heard that number a couple of quarters back, but I’m not sure if that is still the same number now). So even if I presume some might be utilized, I think still 1500 cr+ may be unutilized (I am guessing here).

PEL is aiming for a Banking license, so they are making it bank ready. Time will tell if and when its materializes. However, they must demonstrate a robust risk profile and monitoring framework if they want RBI to grant their wishes. Otherwise, RBI will not grant their licenses. Based on their current actions (preventive provisioning in Covid/Mytrah) may be giving good indications for RBI.

Shriram. I guess their reorganization is about to complete in Oct/Nov. Assuming they get 2/3 quarters to settle their new business, PEL shall be in a position to exit their position in the next 4-6 quarters. So even if Armageddon happens next year (due to various issues in the world), they have a resource to withstand the stock.

In short, I think there could be some pain in the short term, but a medium to a long time shall ok IMO.

Note- Invested and views are biased