Apart from equity, there is another interesting option for people with faith in PEL.

Secured NCD (675PCHFL31 on BSE) available around 11.7% yield to maturity.

This was originally issued to DHFL debt-holders. Pays out interest and part capital repayment bi-annually. Final maturity is on 26.9.2031.

Other Piramal NCDs trade closer to 9%, as far as I know.

Disc: invested in the NCD.

Good points on Q4 which surprised the street -

In accordance with the provisions of Regulation 30 of the Listing Regulations, we wish to now

inform you that the Reserve Bank of India under Section 45 IA of the Reserve Bank of India Act,

1934, has granted Certificate of Registration to the Company to commence the business of nonbanking financial institution without accepting public deposits. The said license was received by

the Company today i.e. 26th July, 2022

It already had an NBFC licence right what’s this new licence ?

just a formality after merger of DHFL with piramal. Point to be noted though is that -

" Non-banking financial institution not accepting public deposits"

DHFL was deposit taking NBFC.

Could someone throw some light on this news, what book is this that they have sold. Is this part of POCI.

Most of the portfolio consisted of loans from DHFL, the housing finance firm it acquired last year under an insolvency process.

This could be the marked down to 1 rupee loans.

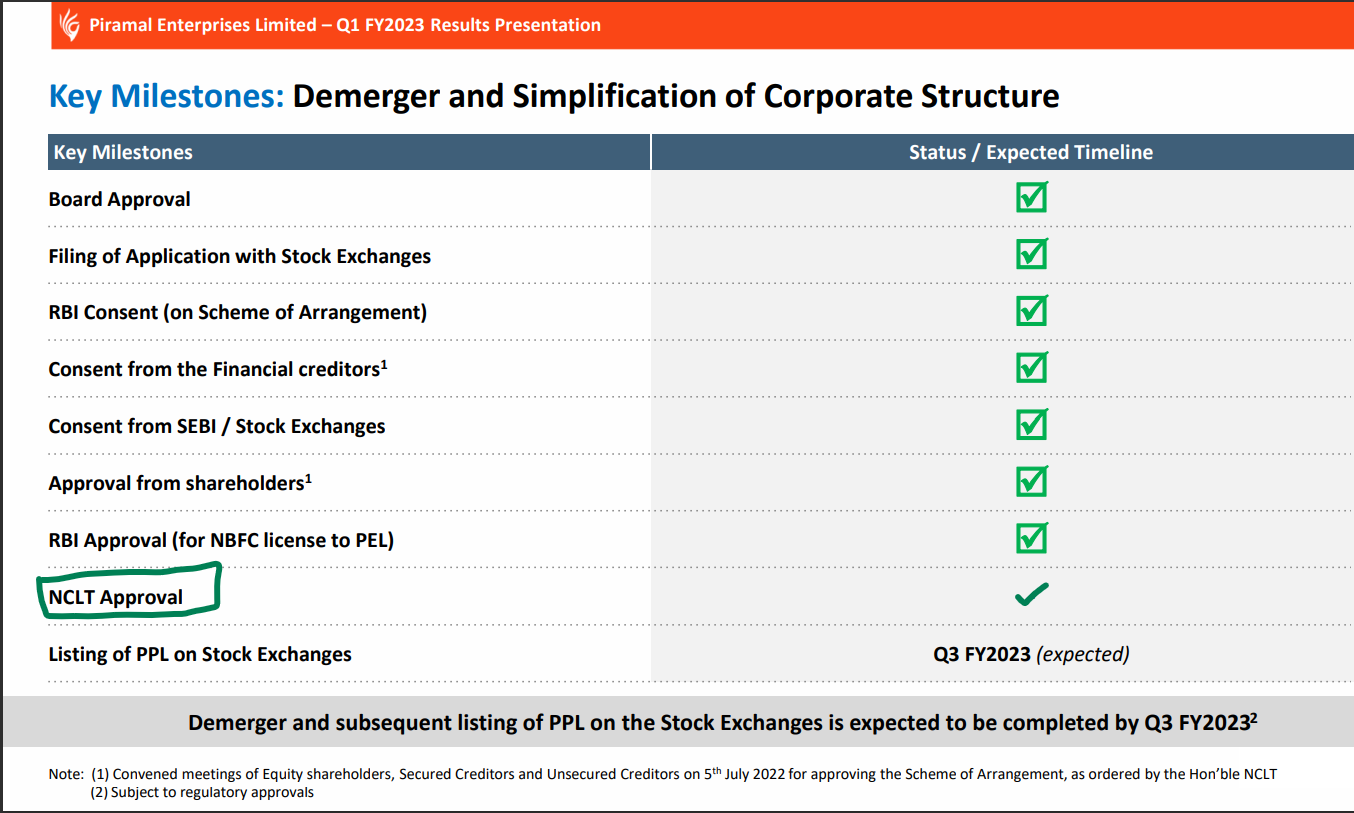

The last step of NCLT approval is done for the demerger. So we should look at this closing in the next few weeks.

Sanction of Scheme by Hon’ble National Company Law Tribunal, Mumbai Bench (‘NCLT’)

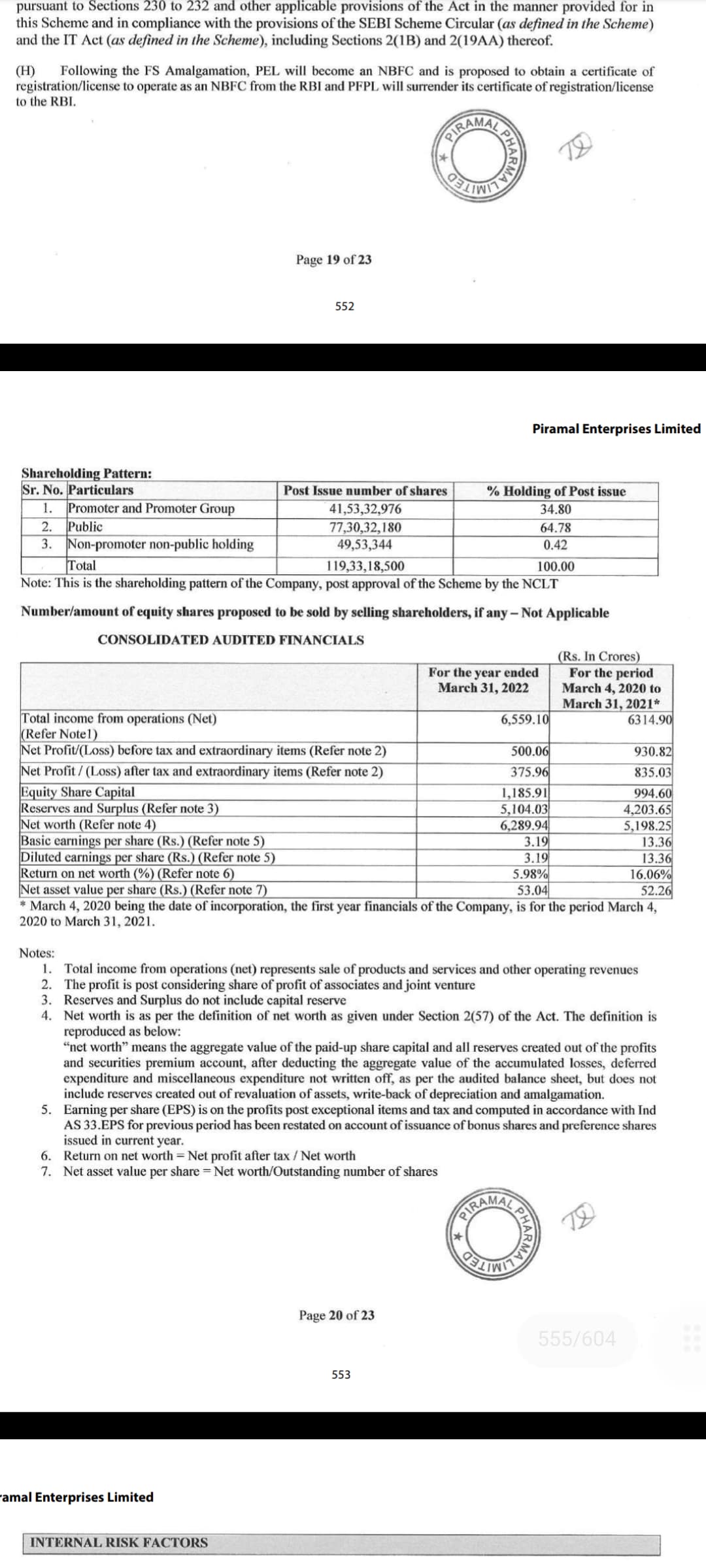

Incase someone is trying to figure out piramal Pharma accounting numbers.

Revenue looks stagnant probably because of DRG business sale at the end of FY21. else, there its a 16% topline growth.

ROE numbers look horrible, partly because of one time acquisition expenses, some new equity raise from Carlyle. Adjusting for this ROE would have been some 10% types.

PPL folks have guided that their EBITDA margins should move back to 22% levels from current 18% in the medium term… factoring that, normalised ROE will be close to 15%.

Also, their depreciation growth in the last 5 years is about 50% and EBITDA margin growth is also close to that- seems like incremental reinvestment is very high to maintain growth in CDMO & Indian OTC brands. PPL folks always talk about EBITDA in their presentations and never about PAT numbers.

Maybe with more phase 3 molecules commercialisation & incremental brownfield expansion utilisations operating and profit margins will shoot up and take the ROE numbers above 20%- I think this should take some time to reflect.

Atleast today as the facts stand, it’s a mid teen topline growth company -growing at the expense of PAT margin and aggresive acquisitions.

Source of PPL financials :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/78c6c53e-466c-4b6f-8ec4-858cef943750.pdf

Sept 1 is the record date for demerger.

discl: holding

shiv kumar

Ref: Composite Scheme of Arrangement

September 1, 2022 has been fixed as the Demerger Record Date for the purpose of ascertaining

the Shareholders of the Company who would be entitled to receive equity shares of PPL in accordance with the Scheme.

4 (Four) fully paid up equity shares of face value of Rs. 10/- each of PPL are proposed to

be issued and allotted to the eligible shareholders of the Company whose names appear in the register of members as on the Demerger Record Date, for every 1 (One) equity share of face value of Rs. 2/- each held in the Company.

The equity shares, proposed to be allotted by PPL, are proposed to be listed with the BSE Limited and National Stock Exchange of India Limited, subject to necessary regulatory approvals, in terms of the relevant provisions of the circular no. CFD/DIL3/CIR/2017/21 dated March 10, 2017 issued by SEBI, as amended, from time to time.

PEL has released a updated presentation on the listed FS services business, possibly to support the sell off that Pharma Only investors might engage in, after the Record Date.

PEL - Financial Services Roadshow Presentation

The off balance sheet item of around 16000 cr will be added to the book right. This should increase the book size and shud be done in upcoming Q2 results for FS Business

Is my understanding right ? Experts please advice ![]()

Just Curious regarding calculations (as this is my first demerger experience)

Q1. Does todays fall will impact the market cap of the pharma business when it lists? (i know that it will recover, just want to know)

Q2. How can one calculate the maket cap of the listing pharma business? ( a detailed calculation will be even more appriciated)

Note : Not asking the question for any buy/sell reccommendation. Just want to learn for future demergers…

dis : invested.

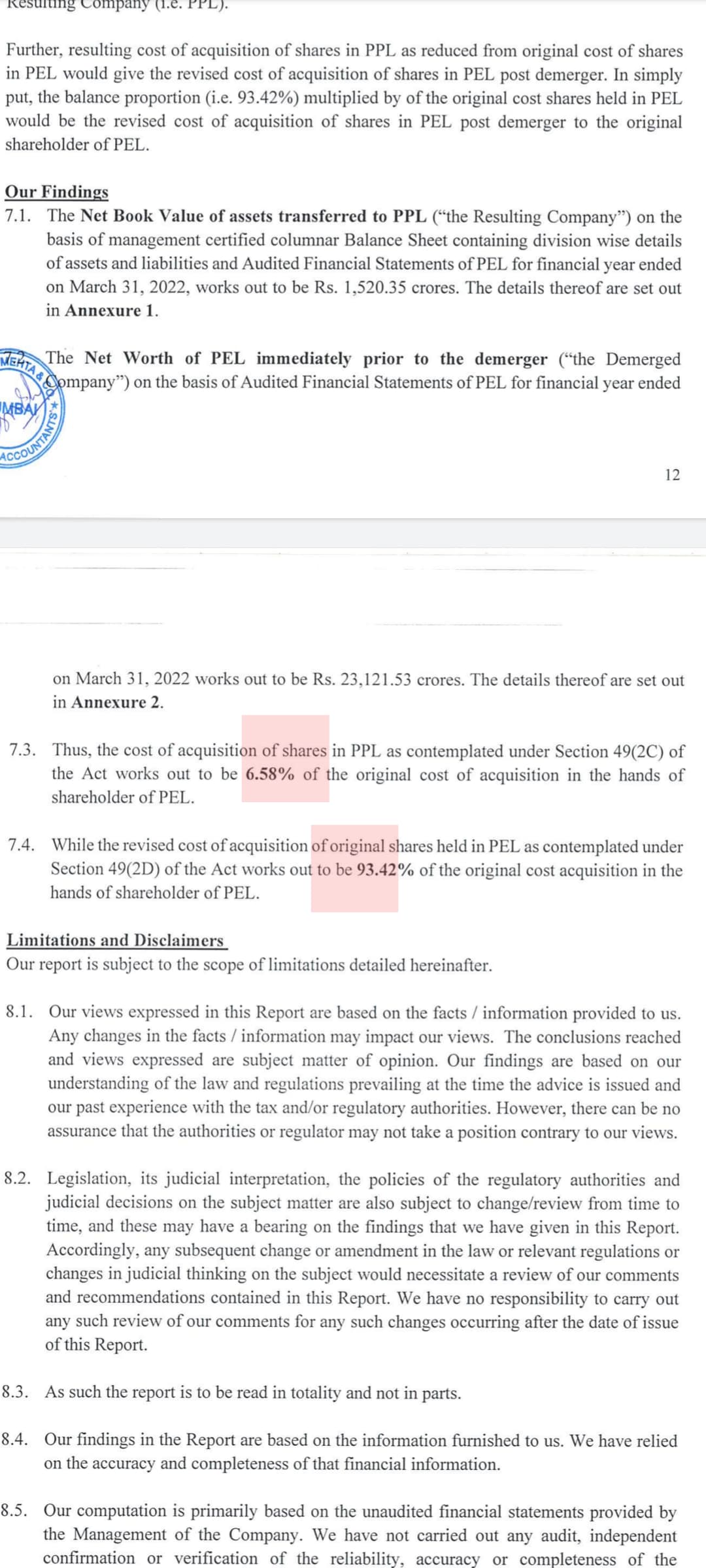

PEL Enterprises should publish a guidance (not sure when but pretty soon) on what % of acquisition cost of earlier PEL can be attributed to PEL finance and remaining to Pharma.

Determine Acquisition Cost of Piramal Pharma and Piramal Finance after demerger

e.g. PEL might say 93.42% value is spun into finance business and remaining 6.58% in PPharma.

In this case If,

- PEL is acquired before demerger at Rs. X (i.e. say Rs. 2000)

Then, based on guidance, - PEL Finance acquisition cost for calculating Capital Gain after demerger is Rs. 0.9342 multipled X (i.e. 0.9342x2000 = Rs. 1868.4)

- PPharma acquisition cost for calculating Capital Gain will be Rs. 0.0658 multipled X (i.e. 0.0658x2000 = Rs. 131.6), since we get 4 shares per demerger ratio, 1 share acquisition cost for calculating Capital Gain of PPharma will be 0.0658/4 multipled by X (i.e. Rs. 32.9).

Hope this helps. Seems people can book quite a bit of loss if holding PEL Finance (for adjustments with gains somewhere), but Pharma shareholders can end up holding some good profits.

Update: Refer https://www.piramal.com/wp-content/uploads/2022/08/PEL-PPL-Demerger_Report-to-determine-Cost-of-Acqusition-S.-492C_Signed.pdf

Page 13 says 6.58% for Piramal Pharma and balance 93.42% for PEL Financial Services.

So when the news report “business lists at Rs 1050” (example below), does it mean that this listing price is being determined by market forces and is not what is formally guided by PEL?

For folks who are trying to figure out your acquisition costs.

Multiple your average buy price with the finance division acquisition cost %.

As per the article, 93.42% of the acquisition cost will get attributed to Finance entity and only 6.58% would go towards PPL. If this is true, my understanding is as below

If you purchased shares of PEL before 29th August, let’s say at Rs 2000 each, then the revised acquisition cost for capital gain calculations would be as below

PEL - Finance entity - Rs 2000x .9342 = Rs 1868.4 per share

PPL - Pharma entity - Rs. 2000 x .0658/4 = Rs 32.9 per share

If true, one would be booking large capital loss on financial entity share sale (1063-1868=805 per share loss) and large capital gains on sale of PPL shares , when they get listed. (as per current market estimate of listing at Rs 200 per share, CG profit per share would be Rs 200-32.9= Rs 167 )

Assuming all of the above assumptions are true, then long time PEL shareholders would be worse off post demerger (167X4)-805 = -137 per share loss. As everyone is talking about value unlocking post demerger, I think there is scope of both PEL and PPL share prices to rise beyond current assumptions.

Disclosure - invested for last 5+ years and running our of patience ![]()

I think you might have got it right. Another aspect is time of acquisition for calculation of capital gain/loss. As you mention you holding it since 5 years, will acquisition time for Pharma shares be when u acquired the original shares of whole business or when this subsidiary was incubated within Piramal (say if it was incubated 3 years back only just for sake of example & learning) or the date of credit of Pharma shares to your dmat account?

Prior to its listing or credit to dmat account date, the scrip ID would not even exist and so to have it’s acquisition date prior to that can be technically incorrect in case someone has to report details for tax purposes…thought welcome