Nice coverage of Piramals by BT

2 Likes

This is not an approval but the direction to conduct the shareholders meeting. Post the approval of the scheme by the shareholders, the NCLT will consider the scheme for approval.

3 Likes

Piramal Pharma Solutions Upgrades Oral Solid Dose Capabilities with New Production Block at Pithampur Site

5 Likes

Looks okay result, Things falling in place for NBFC business, Expected better from PPL CDMO. Consumer & Hospitals growth made up for it which was expected.

2 Likes

These additional provisions are dampener… How much its there more.

1 Like

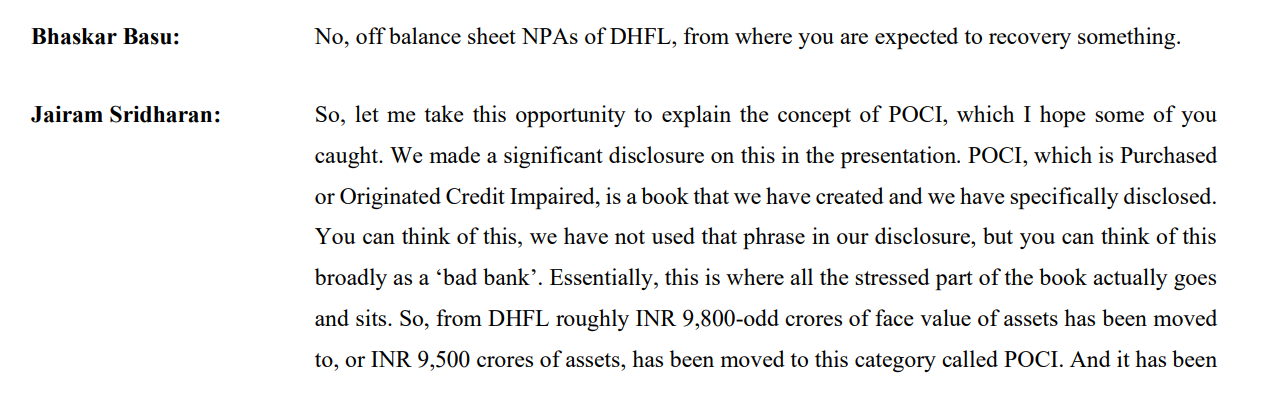

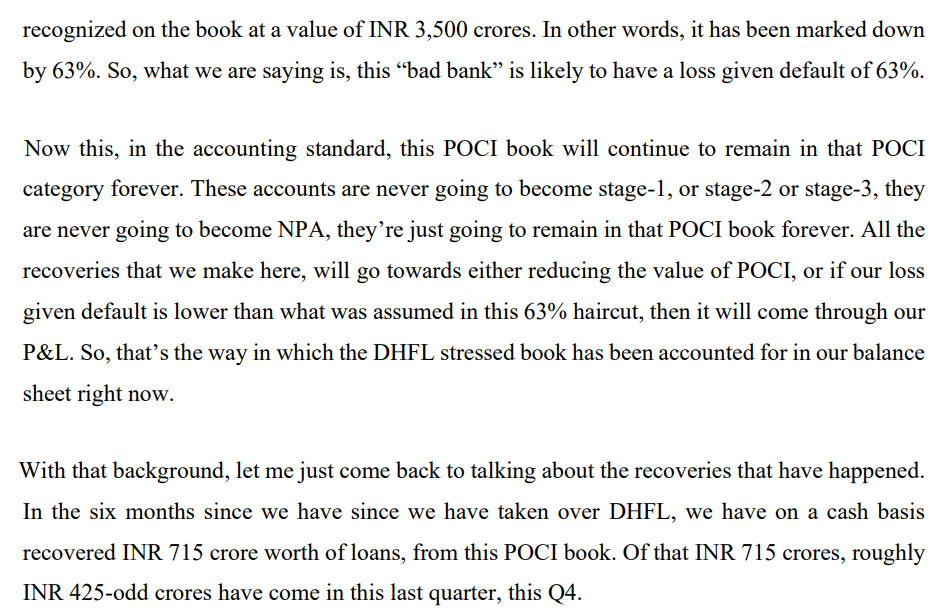

To be honest, I am disappointed with the results. On one hand, management (Mr. Khushroo Jijina) has spoken very highly of their processes like due diligence and stress testing, assuring investors that their book is pristine and their provisioning is conservative. But then when actual results come out, they have to eat their words as wholesale book continues to throw surprises (howlers… ![]() ). I hope company stops this once for all.

). I hope company stops this once for all.

It seems company is in house cleaning mode prior to demerger… but does that mean pain for 2 more quarters in financial business? No one knows…I hope not…:- ![]()

2 Likes

Some imprecise (calculations) and high level thoughts…

Pharma sales is 6700Cr and net profit is 1180 Cr (Consol NP 1923 less FS NP 743). Assuming an approx. Mc/Sale of 6, or MC/NP (P/E) of 20, the Pharma business MC could be in the range of 23,600Cr to 40,000Cr. The Pharma business was valued at $2.77bn (21,000Cr) in Jun 2020, so expecting that the value would have improved in 2 years.

Coming to the financial services business, they acquired DHFL for 34,250Cr, the value of which they would obviously improve overtime. In addition, they have their own retail lending business, wholesale lending business, a real estate development project in Andheri (Mumbai) which they will be monetizing over the next few years, 2 AIFs, some investments (Shriram). I don’t know how much value to consider for these, but feel its safe to assume not less than 40,000Cr.

Putting the 2 together, I feel the downside risk is negligible, this presents an interesting opportunity.

Please feel free to share your thoughts where I could be wrong (I guess there could be many mistakes in my rational).

Disc: invested

9 Likes

I have been invested from last 6 yrs and staring at huge loss of capital…Investing is not easy as many say…hindsight investing in index would have be much better…may sell out some qty to reduce the risk of over concentration…it doesn’t make any sense to hold long term when they cant deliver

7 Likes

Interesting issue here, PSB’s NPAs have started coming down as they’ve aggressively been asked to provision for it and their lending improved. So much so, rating agencies are saying they’re on the path to growth.

PEL however seems to be slow in recognizing bad asset quality and that might be a problem aggravated by the DHFL assets

With all due respect, you didn’t mentiined the fact that you paid 4X BV multiple. And when one pays such multiples, the time horizon and business performance over that time period matters.

Keeping the stock price and this qtr performance aside, the co. has doubled its BV over the holding period you mentioned. Yes, the contraction in BV multiple happened. Now the questions come back to what was your initial thesis and expectations when you bought at that point of time at that valuation. And wat has changed - BUSINESS-WISE, to that thesis now. Consider on those lines.

Disclosure :- Invested. But primarily as demerger arb bet.

This post isn’t an analysis or comment on company’s business or its recent performance. But it was to highlight an important consideration from the data points you mentioned.

5 Likes

I don’t know how you came to 40,000 cr its an absurd amount… If they would have had this much money they would have sold 20℅ of their gem to Carlyle for 3000 odd crore.

Including everything it comes down to 18000 - 20000cr in financial services business.

I am taking the DHFL value at its acquisition price which is 34,250Cr.

The land in Andheri, is 67 lac sq.ft. I assume it will be valued at more than 6,000Cr. PEL gave a loan to the to tune of 1300Cr. if I am not wrong.

See below snippet from May 2021 call regarding the land in Andheri.

Piran Engineer: So, the land has not been developed yet?

Khushru Jijina: No, now we will actually give it off to other developers. We will cut the land and give it. There is 67 lakh sq. ft. on the highway. It is not small. It is a very valuable piece of land.

Piran Engineer: How much would the land be worth, by a rough estimate?

Khushru Jijina: We actually did this exercise, but I would not give you the exact number, but it is far more than the value of the loan. I can only comment on that, that it is far more.

In addition to these, there is retail (ex. DHFL) + wholesale lending business, 2 AIFs and investments in Shriram group companies. And I forgot the Life Insurance JV business.

So I am trying to ascertain the “market value” of all these, which will obviously not be precise, and I not being any expert on valuation. Its just my hunch that the downside risk is negligible at the current price.

2 Likes

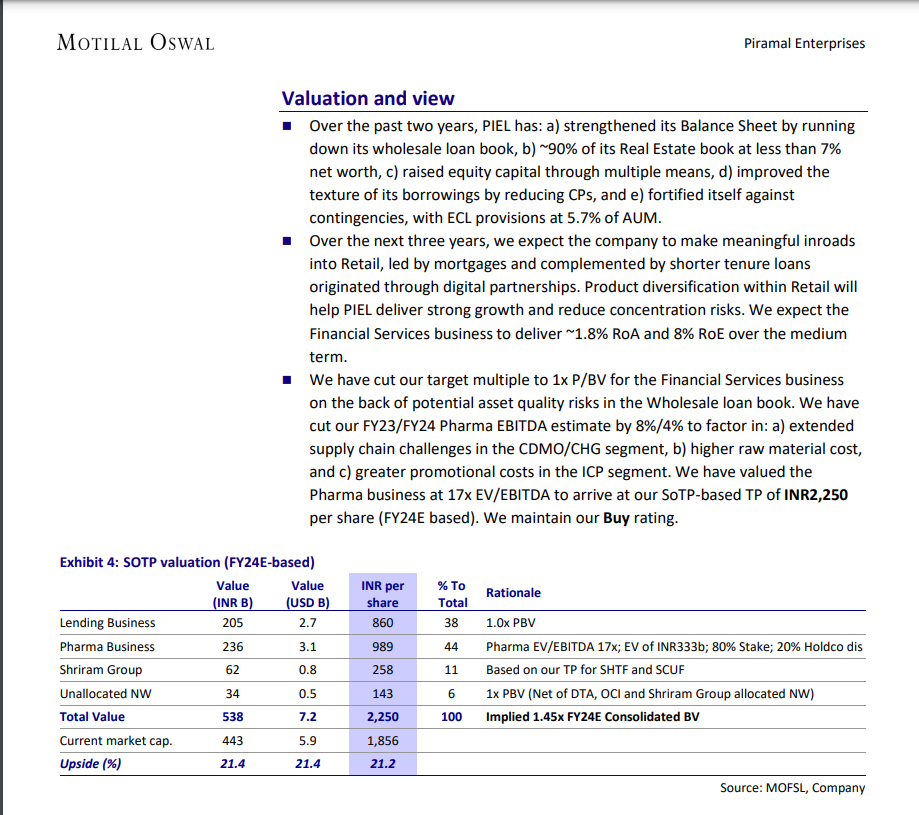

PEL valuation as per Motilal Oswal’s latest report - they value the entity at ~54000 Cr. This is down from ~76000 Cr in Feb.

Their Feb report had a 1.7x P/B financial business valuation and 19x EV/EBITDA for pharma business. Financial business valuations have been reduced significantly after Q4 results.

PS: Haven’t studied the company yet. Interested in the Pharma business and evaluating taking a position before demerger.

7 Likes

and the story continues…:- ![]()

1 Like

Could this lead to domino effect of filing cases by others who also lended to dhfl ?

1 Like

1 Like

Good news item from BQ.

However, if one has followed PEL closely, there is nothing new in the article which is not mentioned on the current thread. Still, it covers different points in one article for example related to General Insurance (PEL seems to be interested in Reliance General insurance arm in particular as per the article)

2 Likes