In my personal opinion, everyone knows Piramal pharma would attract lot of new investors so it is discovered story. Finance business with huge boost from DHFL acquisition is still unknown and can be a real winner post demerger. Real estate is doing well so all legacy issues are being taken care of. So if Piramal positions its financial business smartly, it may lead to rerating. I know it is contra view but its possible

4 Likes

My two cents:

- Its difficult to gauge what all market is pricing in the short term in PEL, since there are a lot of near term factors like the Ukraine-RUS war. Does this impact PEL revenues directly? Mostly no, but with potential loan takers being impacted, this might affect loan uptake.

- GMR versus PEL might a bit tricky. In GMR, the listed entity was going to have the better visibility business of Airports, and power/infra was in new unlisted entity. In PEL, its kind of reverse with the better visibility business of Pharma being in the new unlisted entity, and PEL continue having the finance business.

- Margin of safety is getting better (view >2+ years, ideally 5 years) with every fall in short term.

I have being invested since 2014, seen it go 7x from ~400 to 3000+, fall 80% to 700, and then go up 3.5x to 2600, and now down 25% to 1950 odd. I saw this as a 10+ year journey, am in the money, but think this can be a big compounder based on the growth engines they have created.

Question is when will the growth engines really start firing and fire for the long term. +ve on the management on their long term vision, nuanced understanding of finer aspects of business. Post 2018 it has been a tough time with several headwinds, but they will survive is my thought, and can make merry if the headwinds temper down, and growth accelerates.

5 Likes

How much lower will the NBFC trade? Such questions often come up in bear markets. It’s already at 0.8 times Price to book and they are expecting write backs.

My thinking between post or pre demerger:-

Buying this pre demerger as this is a widely followed and tracked business. Opportunity might not be there post demerger. Will look at something like Aarti Pharmalabs post demerger as the implied mcap will be likely sub 4000 crores. Which is when a lot of institutions won’t be able to own it given the mandates. This isn’t the case with Piramal as implied mcap for both the divisions will be likely to be more than 15k+ Crores.

Disc:- invested. Buying in chunks given the weak market Strucuture.

28 Likes

Not necessarily… Even Piramal Finance business is not a gruesome business at 0.8 P/BV. So, it may not fall much, infact any fall here is an opportunity. On GMR, it is already demerged - the current listed GMR Infra is pure airport business. The other business will get listed after few weeks

5 Likes

There is a difference between a good business & good investment. The opportunities to create alpha are created whn the supposedly sane minds oversell. GMR demerged biz oversold upon listing might present an investment opportunity with MOS greater than the airports biz.

Similarly, if there’s value in the demerged Piramal nbfc biz, the selling there post demerger will be a buying opportunity for the investor who has done his\her calculations. The question to be asked always is - Is the stock price presenting enough MOS vis-a-vis the intrinsic value of the business.

For the investors who are investing/invested now, the answer to above question was probly YES - even in its current form both Pharma & nbfc biz present great value.

Disclosure :- Invested

11 Likes

another case filed in Supreme court…no wonder our courts are overloaded with huge backlogs… since they allow such frivolous cases (from fraudulent promoters) to come up for hearing. Needless to say, market is nervous due to the uncertainty, hammering the stock price making it extremely attractive to any long term investors…

Disclosure - Long term investor, transactions in last 30 days.

1 Like

I have just a small query.

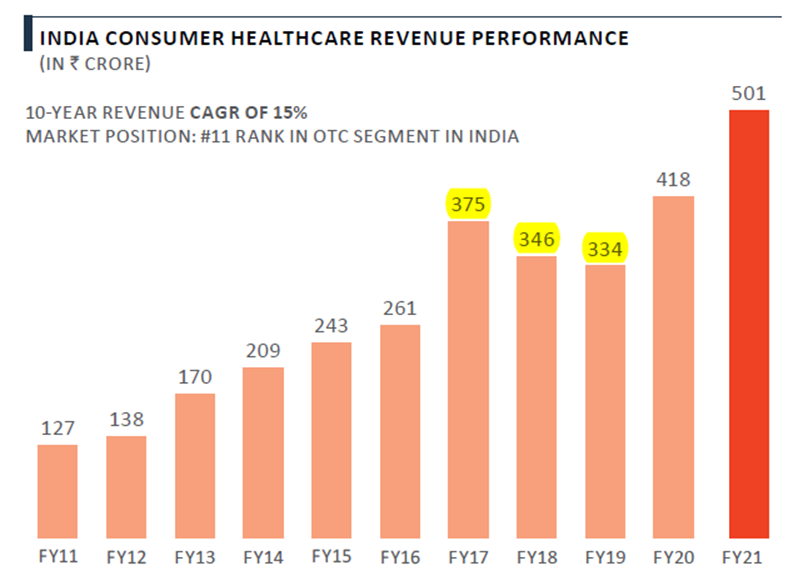

For someone who has read the company, can you please tell was there any specific reason for de-growth in the Indian healthcare business from FY17-FY19 or something to note about?

Nandini Piramal, Executive Director, Piramal Group, shares the company’s vision and ambition for the global pharma business and its Consumer Product Division with Storyboard 18.

Transcript

3 Likes

Courtroom drama continues…making share price YoYo

My take on the valuations. Moderator, please feel free to delete if you think it is incorrect.

TTM sales for pharma business: 6484 crores

62% of pharma sales are from CDMO, which makes it 4000 crores.

If you give the CDMO business, a price to sales of 10 times, similar to what Suven and Syngene get, just the market cap from CDMO business will be 40000 crores.

For balance 2500 crores, comprising complex hospital generics and India OTC business, giving it price to sales of 4 times, the market cap will be 10000 crores

Total market cap : 50000 crores just from pharma division.

As per SOIC’s latest video on special situations covering Piramal Enterprises, the price ascribed to the pharma business is Rs. 762, implying market cap of 18000 crores.

Potential upside could be about 3 times, once pharma business gets listed.

Disclosure: Studying, no positions yet.

14 Likes

Interesting take on valuations.

Didn’t it occurred to you that maybe the comparable cos. you mentioned might be overvalued.

A valuation perspective on pharma biz was given when Carlyle invested in the co. for 20% stake - So, if you wanna take a shot at valuations I suggest go thr that transaction, understand which multiple they paid and why and then adjust for how mch a retail investor( who is a proxy voice, not a say like Carlyle)

Disclosure :- Invested

1 Like

“If you have to create extraordinary value, there are two things (to do). You have to buy something, which is imperfect and you have to sell something that is perfect. If you are willing to take the risk, and if you can identify the value there, then the value can be created," Piramal said.

‘Do the process right, and results will follow’ (livemint.com)

5 Likes

Looks like Piramal is fully intent of recovering whatever they can from DHFL NPAs … Surely they will not do that to hand it over on platter to CoC as per current NCLAT order… which means they are confident of getting favorable verdict from Supreme Court

Bit dated but I liked the balanced reporting , seeing through the eyes of bad loans acquirer. This not only explains the problems but also offers interesting win-win solution. Must read for anyone interested in PEL stock

5 Likes

you have posted Jan’22 Article.

4 Likes

Tareekh pey Tareekh…

our supreme court is left leaning, they will never accept capitalists solution to the problem.

Re 1 should be written off to 0 by PEL & PEL will never work towards resolution of those loans for the creditors (why should they).

Socialists solution no one wins.

6 Likes

New regulation from RBI for lending to real estate sector.