Q3 F22 results out

1 Like

Result seems decent, but best is yet to come IMO as they work on DHFL integration.

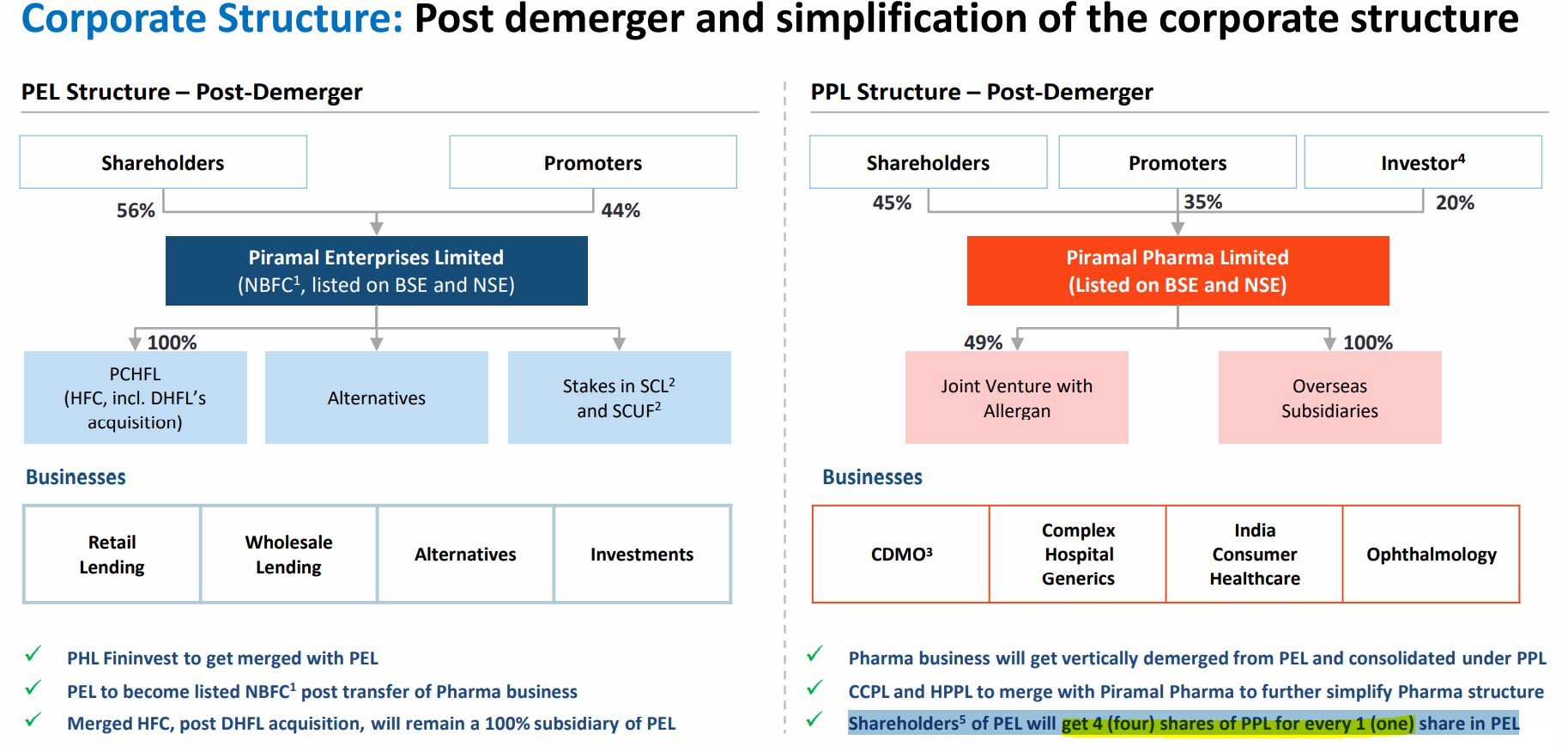

Demerger ratio is announced (although it is almost 8/10 months away)

Pharma division announced number of Capex plan.

CDMO Piramal earmarks $74M for upgrades to UK antibody, API manufacturing sites | FiercePharma

3 Likes

Concall notes -

• Demerger of pharma and financial business to be completed by Q3 of FY 23

• Implemented RBI circular for NPA – stage 3 – 25 Cr – not 90 days past due

• 147 Cr – stage 2 to stage 3 – packaging company – moved to stage 3 for restructuring of the loan, will recover completely

• 10% retail, 90% wholesale provision

• Pharma – CDMO – off take by innovator – no impact on demand. Challenge is in execution, finding people, finding logistics so additional cost

• Complex hospital generics side – seen improvement in US markets. ROW demand volatile, situation fluid. Order book is 30% increase. New customers additions continued

• Nearly 20% overall growth for the year for Pharma– so Q4 will be big quarter. Mainly in CDMO.

• Small recoveries from DHFL book

• Collection efficiency 97-99%

• Retail is already break-even so retail will be profitable in Q4 FY22

• 100+ branches, 2000 employees to be hired

• Q4 will have much higher margin – seasonality due to higher margin projects in H2 as compared to H1

• Historically H1 is low margin period and H2 is better margin period. Trying to reduce seasonality but depends on customer

• Order book visibility is good. Challenge is to execute. Jan has lot of absenteeism due to covid so trying to catch up in Feb and March

• Largest manufacturing facility at Digwal. Always trying to get more business for Digwal

• DHFL yield 11% (on gross book), cost of borrowing is 7%. What flows into financial would-be higher yield

• Loan disbursals pre DHFL – 500 Cr per quarter. With DHFL, it will grow 5x to 7x by Q3 of FY 23

• CDMO deferrals – due to RM unavailability, carrier issues, people unavailable. Customers sensitized. Some place customers also deferred. Now plants are running fine.

• Sold lot of securities books (20000 Cr) when DHFL was having liquidity issues. That book is with banks (off balance sheet) but is managed by DHFL (now PEL) so PEL earns fees on that.

• Not very large cost base of DHFL - 90Cr in Q1 FY 22. (last published financials of DHFL) so it got absorbed by PEL without much bigger impact. (manpower moved to third party so cost classification changed)

• Difference of 65,792 Cr (AUM) – 60,640 Cr (Total loan book) on slide 32 - Major amount is in AIF except investment in Omkar land of around 1300 Cr

• Incremental cost of funding – 8.5%

• Slide 38 – Oncology 3 products – very high potential - $5B sales potential of innovator.

• Effective tax rate – 24-25%

• 29% increase in price of Shriram City Union – between Apr to Dec 21

• Share of net profits of associates and joint ventures – profit portion in Shriram and Allergan JV

• Allergan – growing business with 30% profit margin

12 Likes

anything they mentioned about the nclat order on ncd holders? what’s the way forward? are they going to appeal in apex court?

1 Like

2 Likes

Is there anything negative news about PEL recently. The stock price is reducing gradually.I am able to check Q3 results,they are also looking good to me. Kindly educate me if i am missing any news about the company

4 Likes

The stock has fallen like anything. Found these 2 good videos by @valueeducator and SOIC while looking for points I could have missed during my research. Didn’t find any such negatives. In fact, the financial business is doing very well.

Pharma business:

4 Likes

These are old video. I do not think there is anything significant happened in the company. May be it has broken the 50 DMA and 200 DMA and hence facing some selling.

2 Likes

It’s a Bottoms down U pattern. Next weak support is at 1900  and it’s in strong downtrend. Selling seems likely to continue

and it’s in strong downtrend. Selling seems likely to continue

Disc: Sizably invested.

Seems like someone knows something we don’t. Is there any risk in the pharma hive off plan? Or any adverse possibilities out of the DHFL acquisition?

Since it’s a speculative post, i’ll delete it in a while if there’s no discussion value add.

It is a human nature to under-analyze when stocks go up and overanalyze when stock goes down. You let the stock price validate or invalidate the business instead of doing the work on the business. Investing is a game of seperation. Seperate the business from the stock. Do the work- Ian Cassel

10 Likes

I dont thinks so demerge always takes time, currently, its with NCLT approvals would suggest wait for some time.

1 Like

Now hearing for this will be tomorrow Mar 11

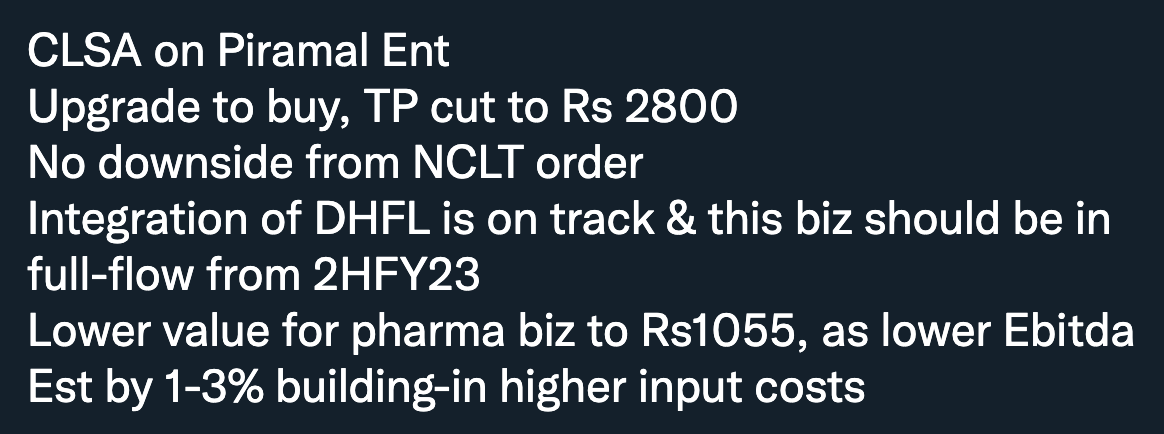

I’ve a query regarding the last line, if they are mentioning here that lowering the value of pharma business to Rs1,055 then does that mean that the listing of Piramal pharma will be somewhere close to this price? Any explanation will be grateful. Thanks!

5 Likes

Note you are getting 4 shares of Piramal Pharma for each PEL share. Rs.1055 is attributed to PEL Pharma biz (80% of Piramal Pharma as 20% is owned by Carlyle), so you need to divide by 4.

So this gives an approx value of Rs.260-265/ share of demerged Piramal Pharma. Balance of PEL at Rs.1000 (based on current CMP of 2000 odd, looks like a good buy at this level)

6 Likes

Can someone help find the full Kotak securities research report? Really curious. Can’t seem to find the PDF on this link or anywhere else.

1 Like

Mentioned in the video below 48k crore mcap. Things become very interesting here, given the guide is to improve pharma margins to 25-28%.

Disc: bought recently

12 Likes

It seems like a Intraday call - can be ignored IMO.

1 Like

Hi, just wanted to know - if majority of player know about this demerger - what if the Piramal NBFC goes into lower circuits once the Pharma is listed separately.

The gains made in ( Piramal Pharma ) on buying pre-merger will be wiped out by loss in the selling of Piramal NBFC. Means nearly ALL MARKET knows about this demerger. So where is the kind of Margin of Safety?

So why shouldn’t we wait till actual demerger happens?

In fact, this is the main query in all such special situations where the Good business is getting demerged from bad business. Another stock is like GMR Airport demerging from GMR Infra.

Means no sane person will keep on holding GMR infra and when all come for selling , it may very well go into lower circuits.

Means why this can’t happen with Piramal NBFC post demerger?

Please do share your views on it.

13 Likes