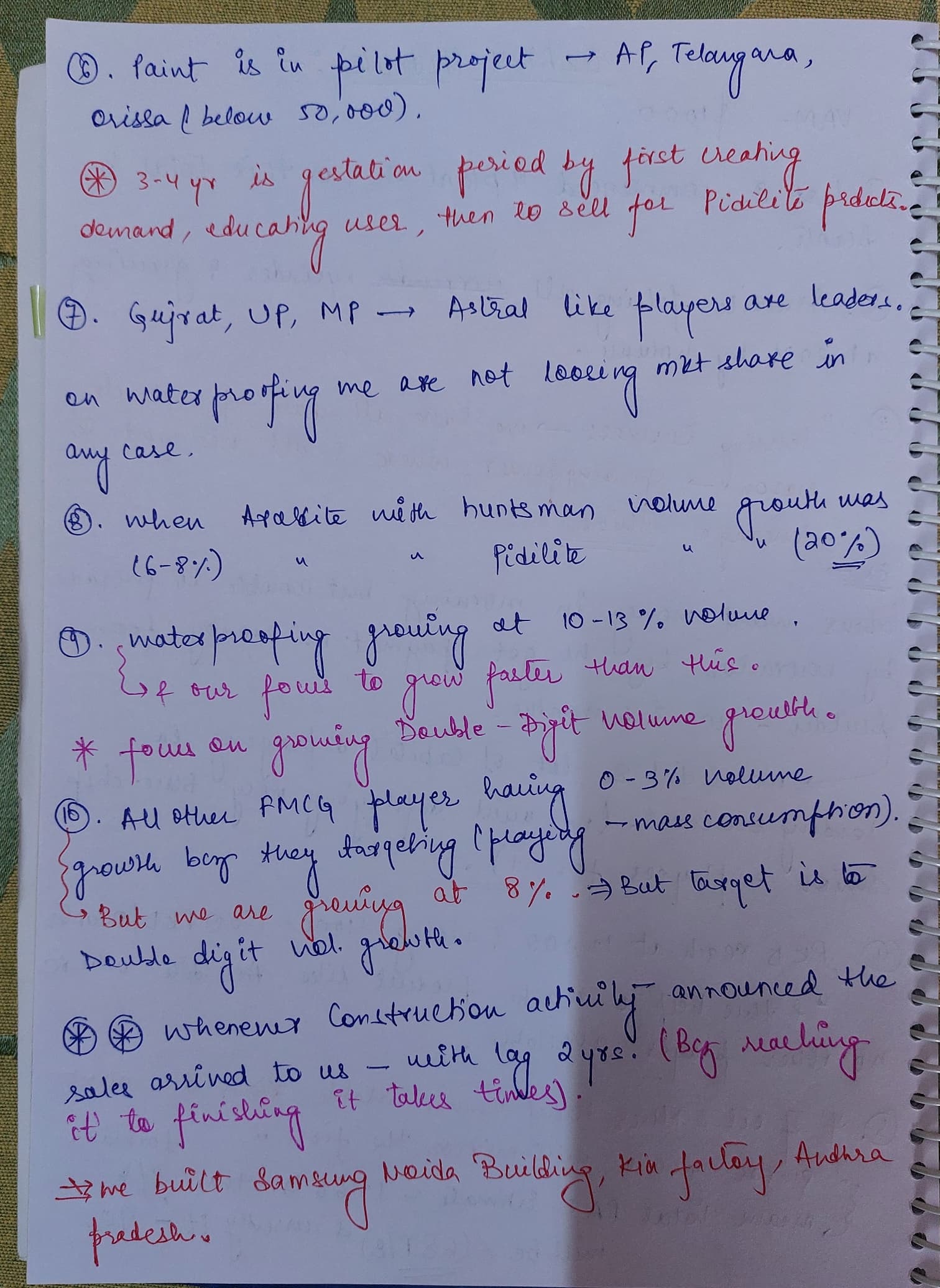

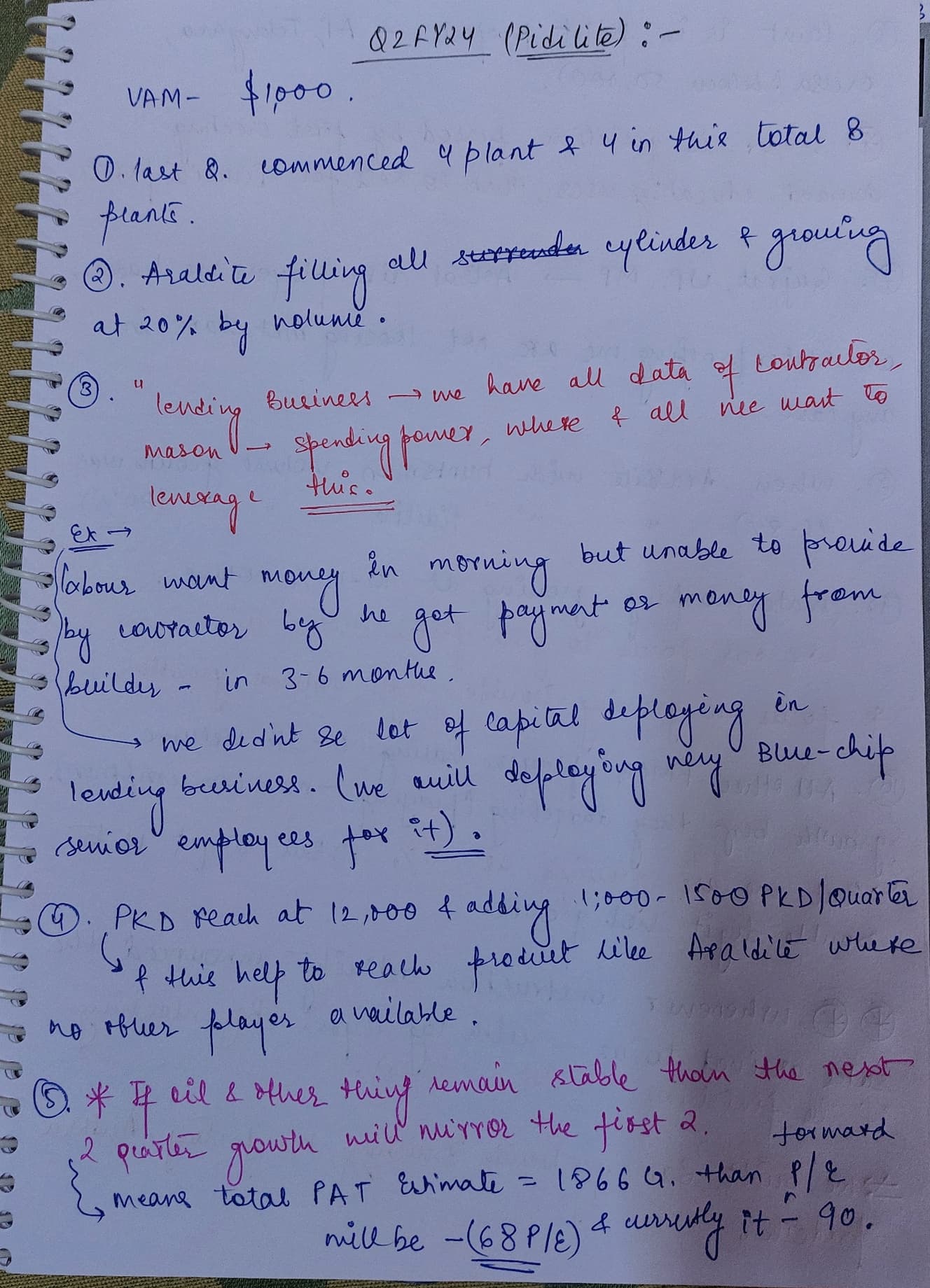

Pidilite to manufacture Litokol and Tenax products from Italy in India

~The state-of- the art manufacturing facilities are located in Amod, Gujarat~

~Development to strengthen Pidilite’s presence in the tile and stone care range ~

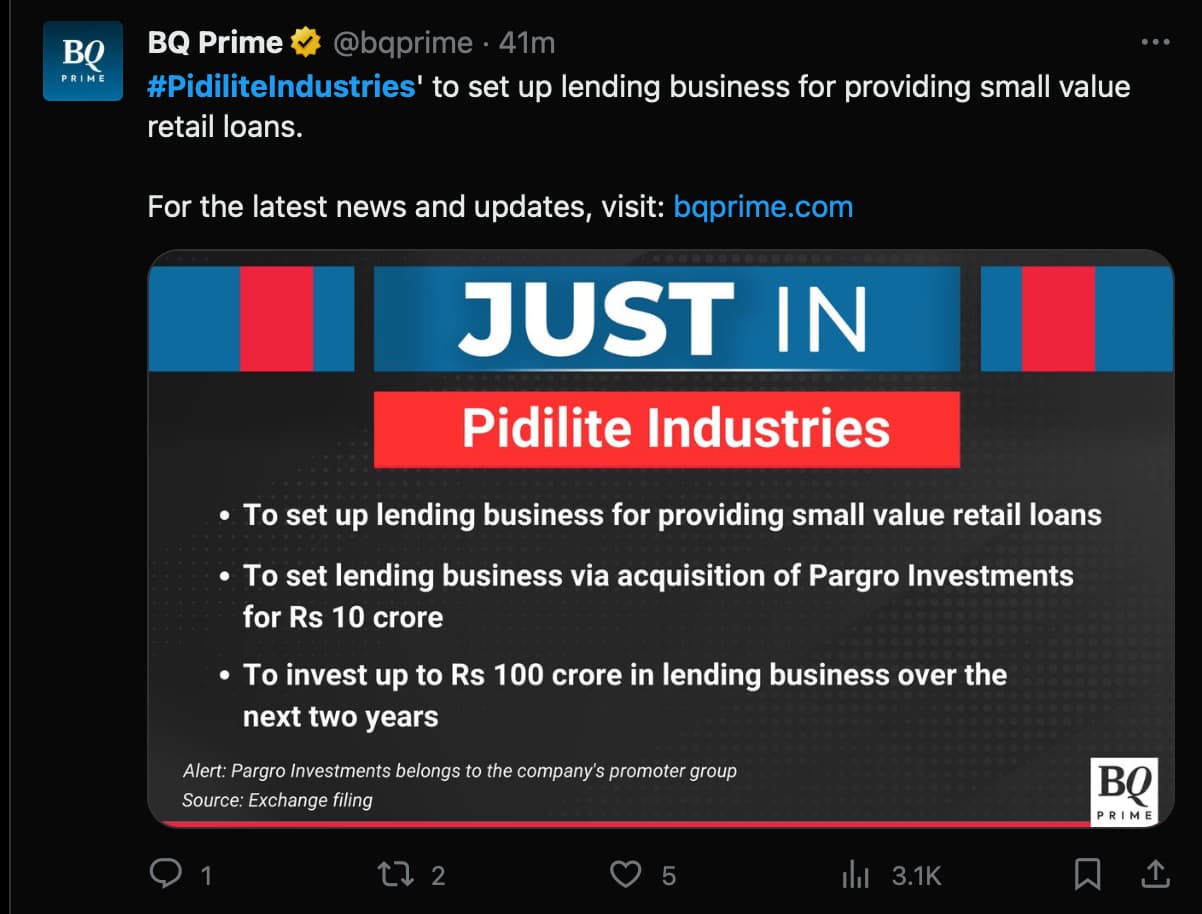

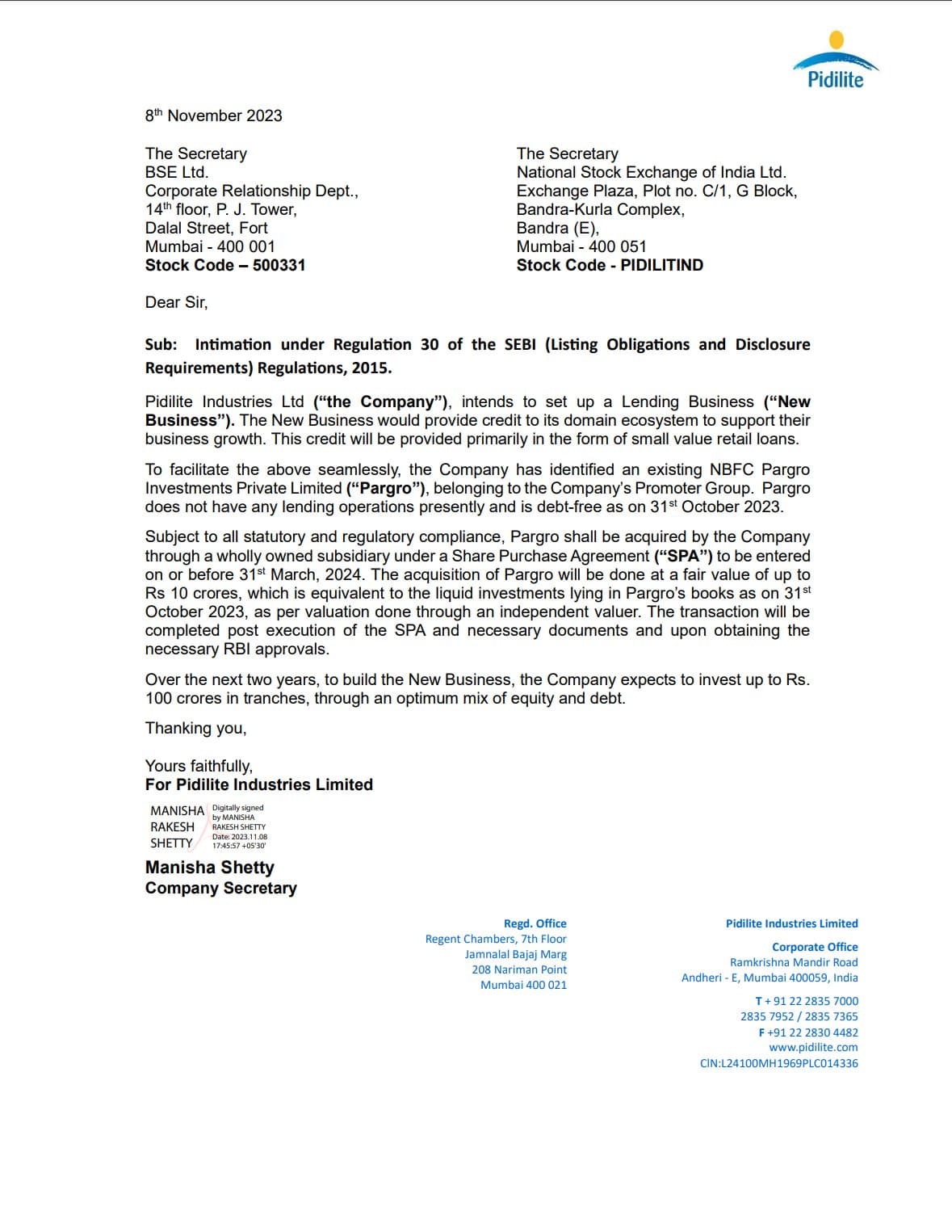

Pidilite Industries Ltd, has plans to start a new business which involves lending money. This new business will provide small loans to people or companies within its network to help them grow.

To make this new business happen, the company has found another company called Pargro Investments Private Limited, which is part of the same group as Pidilite Industries. Currently, Pargro doesn’t lend money to anyone, and it doesn’t owe any debts as of October 31, 2023.

Pidilite Industries plans to acquire Pargro by creating a new company, fully owned by itself, through a Share Purchase Agreement (SPA). This agreement should be in place by March 31, 2024. They will buy Pargro at a price of up to 10 crores Rupees, which is the same as the value of the investments Pargro holds on its books as of October 31, 2023. This value has been determined by an independent expert. The acquisition will be finalized after the SPA is signed and they get the necessary approvals from the Reserve Bank of India (RBI).

Over the next two years, to make this new lending business work, Pidilite Industries plans to invest up to 100 crores Rupees, using a combination of their own money (equity) and borrowed money (debt).

seems like a John Deere model. I came to know that they also have internal lending business and it helps them keep PAT at good levels by keep good margins.

my understanding so this should bode well for pidilite as well.

When I first saw this nbfc diversification news I was surprised and little disappointed. when i read more about it, the reason and purpose behind it to make their own ecosystem better and self sufficient. The real moat of pidilite is the trust their partners and consumer have over their products and this nbfc seems to cater to the benefit of their partners which seem to strengthen that moat further…provided this channel is used judiciously and sensibly…now that seems to be a big if for me as and when this nbfc grows…considering i had decided long back not to invest single penny in any lending nbfc…

For now, i am just evaluating the situation and it seems they will go very slow and conservatively with this nbfc which is a positive factor for me…also giving benefit of doubt to a good management so far…

I would not call it a typical diversification because they have not entered this business as they want to derisk from main business and neither they intend to increase revenue and profits out of this…instead they eneterd thos for their main business.

others views welcome on this new business

Disc: Invested & biased with pidilite among top 3 holdings. Not a buy/sell recommendation. Post only for academic purposes and i can be wrong in all my assessments. Not eligible for any advice.

As you said, you have not invested a single penny in NBFC, i was wondering what must be the reason and also, you must have lost on the great journey of Bajaj Finance and Chola Finance and to some degree muthoot finance. Do you feel that this decision is more emotional than fact based, performance based?

i think its experienced based and knowing myself as investor. we should not look at what we lost in say nbfc as success stories will be everywhere and we cannot be everywhere…its more personal decision and i am perfectly fine in not having ridden a bajaj finance…not so fine in having lost the page industry story though…

Grasim is trying to be a “big threat” for every industry and their cement industry leader is itself facing a big threat. Would it not be a better decision to focus on cement and then try hands here and there? The old saying of not to invest in conglomerates seems to be true here!

Looked this up … seems epoxy resin and epoxy adhesive have slightly different applications, but are complementary. and about Birla Babu… the old adage goes … traditional approach was to target raw material sensitive sectors get scale and cost advantage and then keep expanding… this is now extended to consumer areas also with debatable results … Birla has this knack of raising both equity and debt capital in advantageous way so long term they keep one step ahead of competitors. Kumar Babu thinks your margin my opportunity <> . this is some inside stuff I have been privy to …

Their main cash cow business is facing stiff competition from a player who probably has the deepest pockets currently. While they are more interested in trying to compete with market leader in another industry. This should logically mean that they commit very high capex in Paints business, while they feel competition in their cements business.

For me, it could be a potential case of mis-allocation of capital, because for them to gain market share in Paints, under-cutting the existing price points or giving higher margins to distributors would be the go-to way which would ensure they are not making much money for sometime, maybe like the Jio entry in telecom. But the difference here is, we do not have a 2-3 player market in Paints or Cements industry.

Paint industry is attracting players like never before- Astral and JSW too have joined the bandwagon and they also possess the same advantage (at least on paper) of having an established brand name in Infra material segment. But these many players, with reasonable willingness and ability to spend money is only going to cause pain in terms of margins and lower return ratios (because of high capex!)

Disclosure: Invested in Asian Paints, Pidilite and Astral. In the decision making process of selling Asian Paints, depending on how Grasim and JSW Paints perform in the next 6 months

Cement is a mature sector comparatively. There is muted growth in it volume wise and a very local business where their is no moat and very less brand loyalty. Many of the cement companies in South india are in losses!

Grasim is putting money in paints business not ultratech. Grasim is the one who is diversifying to create a whole empire. They might be seeing muted opportunity with ultratech and thus expanding into paints. They bought ultratech in 2000s from l and t. What if they didn’t do that and thought let’s just expand in the textiles or dyes segment?

I do take your point, but Paints industry is also a multi player industry, which in my limited understanding would not go the Telecom way. It is not a small sized or huge runway industry either, hence “the multi players can easily fit and increase their respective sales at a good rate by winning market share without anyone sacrificing theirs” should not work.

What I understand is paint industry does not have brand loyalty either. One of my relatives is into construction business and through scuttlebutt with him, what I could gather is- be it pipes or paints, the construction guys only prefer the ones which are costing lesser and their customer is usually bouyed by “how good it looks” and not by which brand it is. If Asian Paints sells a premium product and JSW/ Grasim offer similar product at a 2-3% lower price point, they are going to win customers, which should ideally prompt Asian Paints to cut price. Similar to Jubilant Foodworks needing to offer 40% cut on their pizza prices due to stiff competition, despite the consensus view that QSR segment is a fast growing one.

Coming to Grasim putting into Paints business- they always end up putting their legs in the businesses which are highly capex intensive and end up generating sub-optimal returns. They generally enter industries with higher number of players and in the quest of gaining market share, take longer time to generate returns which obscure the CAGR.

Creating empires should be based on 1-2 businesses throwing out enough free cash flows to support the other new ventures so that the returns are not diminished for the shareholders. Empires should not be built on “let us do A because B is now a low growth venture”. They have burnt their hands in Idea, as you rightly said- not going anywhere in Cements industry, AB Capital’s market cap is also increasing because of the long lull it had seen between 2017 to 2022 while other players in Loan/MF/Insurance saw much better returns.

My personal views are based on my limited understanding and some scuttlebutt + the history of returns generated by AB Group in all the businesses they have operated.

What I learned after reading the Pidilite Industries Q1FY25 Earnings Call.

Industry-wise

Investors should keep an eye on this. If it’s a widespread trend, it could impact other consumer goods companies too.

Could be a good sign for Pidilite’s bottom line. Let’s see how this plays out.

Company-wise

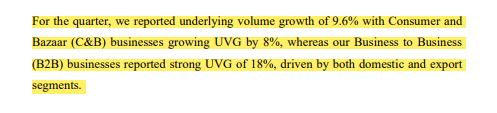

C&B at 8% is steady, but B2B shining with 18% is impressive. Exports & domestic demand driving the B2B engine. This is a positive sign for the company’s overall performance. Let’s see if this momentum can be sustained.

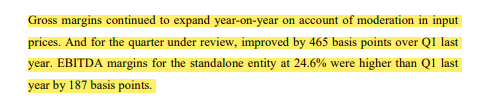

If this trend continues, Pidilite’s profitability could reach new heights.

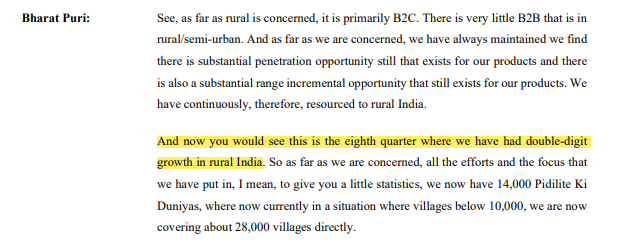

Eight quarters of double-digit growth is no small feat. This shows the increasing purchasing power in rural India and Pidilite’s strong distribution network.

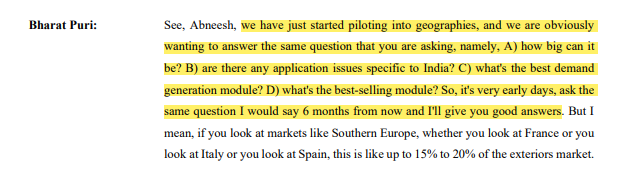

Pidilite’s new product launch is still in pilot mode. They’re playing it cautious, testing the waters.This is where the real work begins.

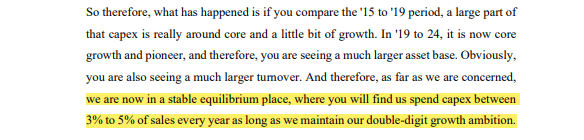

Pidilite’s capex plans are steady as she goes. 3-5% of sales for growth seems reasonable. This indicates a balance between expansion and financial prudence.

Let’s see how deep they can penetrate these markets.

VAP prices stable and oil coming down. Raw material prices are low. Can look at some stability.

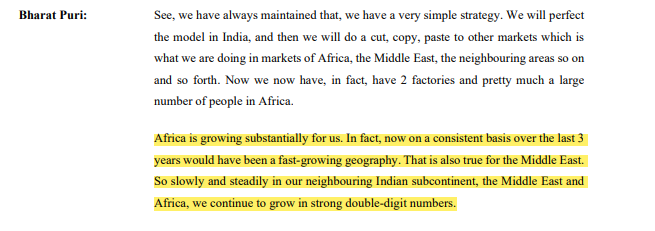

Volumes should increase in core B2B business with deep inroads in Tier-2 and -3 and increased penetration of roofing and tiling adhesive products beyond Tier-1.

Studying it as looks attractive at current prices.

Birla group has been disrupting major construction related categories. Paints, Cables, Wires etc as new entry. So far Pidilite’s core areas seem to escape this added competetion. Any plans of Birla group to enter Pidilite areas? Do they have any edge that Birla would not consider their main categories in future? Or are those categories for any reason not attractive enough (for maybe their inherent difficult nature) for Birlas?