Since I invested in Pidilite, did some fundamental analysis before I add more at lower levels. Sharing here:

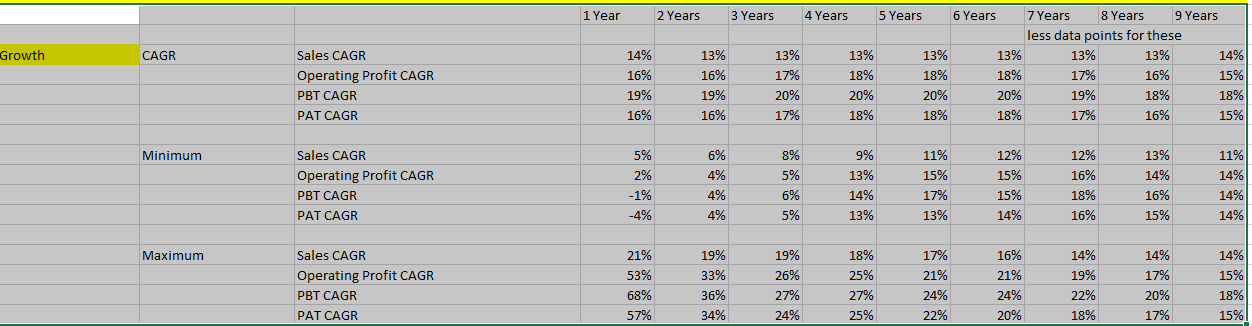

We see that this is Mr Consistent with Sales, PBT, PAT, Operating Profit CAGR in any period more than 13%. There is variation with Sales, EBITDA, PAT, Operating Profit sometimes in single digits or negative but it always bounces back over longer periods

ROCE > 20% in every year over 10 years. With above and ROCE, this is clearly a Coffee Can stock.

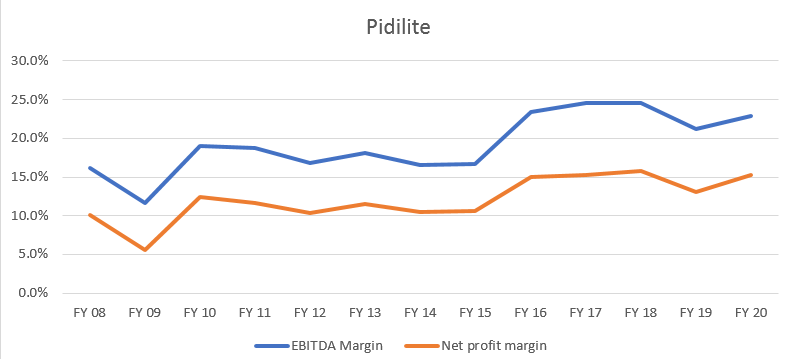

The source of high ROCE is both high NPM and a high capital turnover ratio closer to 2. So even if NPM falls in the future, the capital turnover ratio will make up for it.

Company is investing for the future as we see that the fixed assets have become 2.5 times over 10 years. Company does not need to take on any debt to grow because of its strong NFAT, high NPM, low dividend payout ratio and low consistent depreciation. Company generates strong cash with cash flow RoC more than 40%. Clearly this is a jewel.

Company generates strong Free cash flow.

EXPENSIVE stock

P/E is at 64 which is above 3 year and 5 year averages of 52 and 60 respectively.

All valuation methods like Dhandho and Ben Graham show that this is over-valued stock. Dhandho method shows Pidilite as 14X overvalued (meaning it can fall 94%) and Ben Graham method shows that this is 3X over-valued (meaning it can fall 65%). Clearly, traditional valuation methods are not working for Pidilite

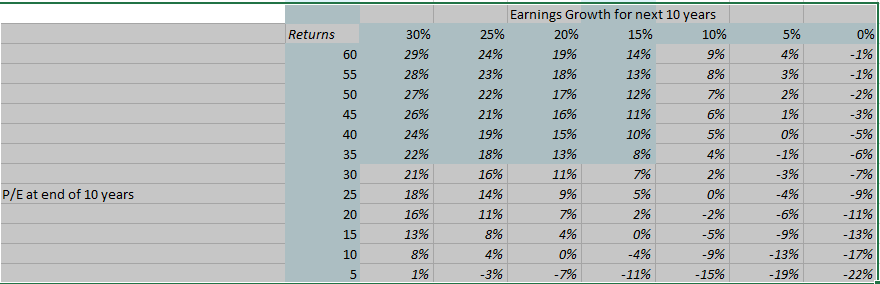

Did some sensitivity analysis to see what would be the returns for different earning growth rates and different P/E values.

We are likely to get double digit CAGR from Pidilite as long as the P/E after 10 years is more than 35 and the earnings growth > 15% CAGR

Given that Pidilite has consistently delivered 15% CAGR in the past and this is likely to continue on the back of strong ROCEs, and the market will attach a high P/E for companies like Pidilite, we can say this is a reasonably ‘buy and forget’ stock.

In case earnings growth falls below 15% consistently for a couple of years, Pidilite could become unviable as there is no safety in buying such a high P/E stock

Disclosure: Invested, Will add more on falls