I expect this to also get fixed in due course as promoter stake comes down and institutional holdings go up.

EDIT - I’m not fully understanding what do they need 1k cr for? Also if annual EBITDA is going to be 250 crs, why can’t they fund the capex via internal accruals? If anyone can help on this

Result is disappointing. Distillery revenue is down and material cost is significantly high. Can anyone throw light why that could have happened? Seasonality or something else?

The distillery segment is down QoQ due to seasonality factors and also the settling of the great Indri rush, as per my conversations with a couple of dealers in a few states there has been a slight dip in the popularity growth rate of Indri as earlier it went viral after the best whisky award, so going forward it will be a normalized and a more stable growth rate, distillery business did decently well YoY despite the heat wave, elections and dip in the euphoria where every alcohol consumer wanted to try Indri. The best part is people are still putting themselves on the waiting list for their expensive bottles. The major hit to the topline came from the sugar division which fell both QoQ and YoY, only the management can answer why this happened either in an interview or a con-call (which has now become the need of the hour). The only satisfying figure is the margin improvement from 11% to 14% which is due to higher contribution from the distillery business. I am still confident about the company’s growth prospects and won’t let a rough quarter change my mind.

imo, one should only look at the distillery division, since that is what is driving the value:-

Q1FY25

Q1FY24

YoY

Q4FY24

QoQ

Revenue

119.23

105.61

12.9%

186.51

-36.1%

EBIT

29.66

17.46

69.9%

58.23

-49.1%

%

24.9%

16.5%

31.22%

It’s not as bad but looks optically bad due to seasonality and current valuations.

Valuations

For FY24, distillery division did EBIT of 131crs. It has done 30crs in Q1FY25, which is ideally the weakest. Most likely, on a full year basis, distillery division should touch 180crs of EBIT (assuming 0 extra capacity gets sold in FY25). Assuming 15 crs of fin cost, we get a PBT of 165 crs or a PAT of 123 crs for the distillery. 55x (reasonable given the capacity add for next year) multiple gives you 6765crs of mcap or 717 closing price.

I do expect the stock to correct by ~20% in the near term. Long-term, the growth is intact.

Not sure if the stocks would flow in market in October. The capex (which is the warehouse primarily & copper still pots etc that they’ve bought) is commissioned in October, which means the barrels are kept in the warehouse.

They then take around 1 year (not sure on this? but not 3 years for sure since Indri is NAS and takes less time to mature) to mature.

You add the time to shipment etc… so on and so forth.

Btw - in the leanest quarter, distillery segment is delivering an EBIT of 25% or an EBITDA of around (26/27%). Make your own conclusions. The EBIT in Q4 was 30%+. As revenue for distillery segment goes up, overall blended margins would also inch closer to that of distillery segment.

Piccadily outperformed both of them by a good margin when only the alcohol businesses are compared -

YoY Sales

United Spirits +8% (Sports business excluded)

Radico +9%

Piccadily +13% (Sugar business excluded)

YoY Profit before tax

United Spirits +19%

Radico +20%

Piccadily +70%

The results are very deceptive, the company should de-merge the sugar business as there is already a listed sugar business that posted the worst-ever numbers recently.

I think the point @DrHarshilRohit (please correct me if I’m wrong) is trying to make is that Radico, for instance, has seen a huge QoQ jump in net profit of about 40% and hasn’t seen the seasonality we’re talking about over here.

Piccadily’s real growth started coming in only in Q3 last year and hence a YoY comparison isn’t a fair comparison.

But then the whole point that he made about whisky makes sense as Radico is a vodka player, United Spirits who does everything from whisky to vodka showed a similar de-growth QoQ. Yes, much less than Piccadilly predominately due to the revenue mix consisting of multiple offerings.

I am not saying the performance was great but that it isn’t as bad as it seems at first glance.

That’s an equally valid point. What we’ll have to see is how are next quarter’s results and whether the corresponding quarter last year was an aberration due to the hype/virality or whether we’ll see growth on top of that.

History is irrelevant in this stock given the changing business model. Key question to answer is does USL show a QoQ jump between June & September. Here’s the data:-

June

September

QoQ

FY24

2,667

2,867

7.50%

FY23

2,419

2,911

20.34%

FY22

1,722

2,508

45.64%

One can ignore FY22 as being marred by Covid wave 2, but FY23 and FY24 numbers are pretty evident.

Also another point on capacity - if one has seen the 40-50 minute video of the tour of piccadily, towards the end you can see that in the new warehouse, whiskey is maturing in new barrels since 2022. So its likely they’ll take some of it out for sale in Q3.

Madhu in this video says, younger barrles have been purchased “over the last few years”. So whiskey etc / liquid is already maturing in some of these barrels. This is confirmed as you move forward in the video & Madhu shows you barrels that have been stocked since 2022. So its likely some of this extra capacity would be released in the market towards Diwali

If I take a 10% QoQ revenue jump for Piccadily, and around 15% QoQ jump in EBIT, we get 132 crs & 34crs of EBIT for Q2. Q3 and Q4 should be bumper given season + extra capacity + new launches (maybe?)

It is very difficult to find out what is happening in the company.

Investors have no idea how many casks company have? How many of them are maturing this year? How long is the maturation period - Is it 3 years or 5 years or 7 years?

Also, how much malt is for captive use and how much is company selling? Is company selling matured malt or fresh malt? If it is matured malt, how is it matured?

I have realised the 30k litre/day capacity management was talking about in the interview was malt capacity and similarly 60k litre/day capacity in fy26 is also malt capacity.

No one has an idea about the Indri whiskey or other whiskey capacity. The company is a total back box, no one can see inside.

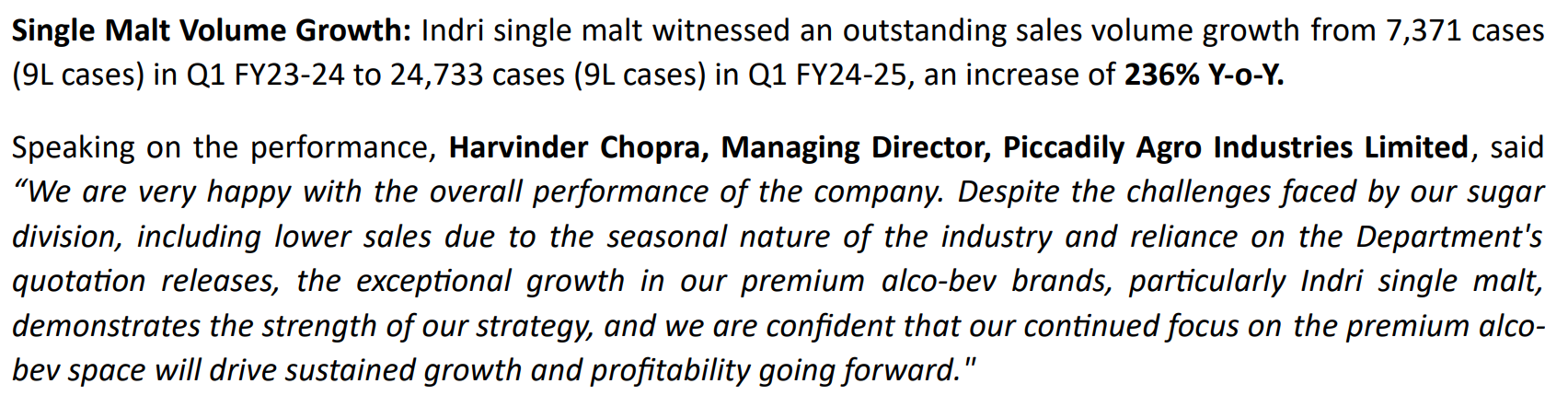

Now the distillery revenue has increased from 106cr to 119cr an increase of 12% but Indri whiskey sale has gone from 7,371 cases to 24,733 cases. Assuming Rs. 3000/bottle price revenue from Indri last year was 27cr whereas this year it is 89cr.

so, what happened to the sale of other brands - Golden wings, Whistler Whiskey, Kamet Single malt, Camikara rum & Royal highland.

I have dropped a mail to the MD, let’s see if we get a response. Will try getting in touch with the company and let you all know if things move further so that we can have a few questions answered.

The number of cases sold for each brand is mentioned in the annual report. Next annual report will contain the updated figures.

Some things like maturation period are things distillers prefer not to advertise. There is no legal or moral requirement to state maturation period for No Age Statement whisky. My guess is that the final product is a blend from casks of various maturation periods.