Link to one of the article covering the points highlighted

4 Likes

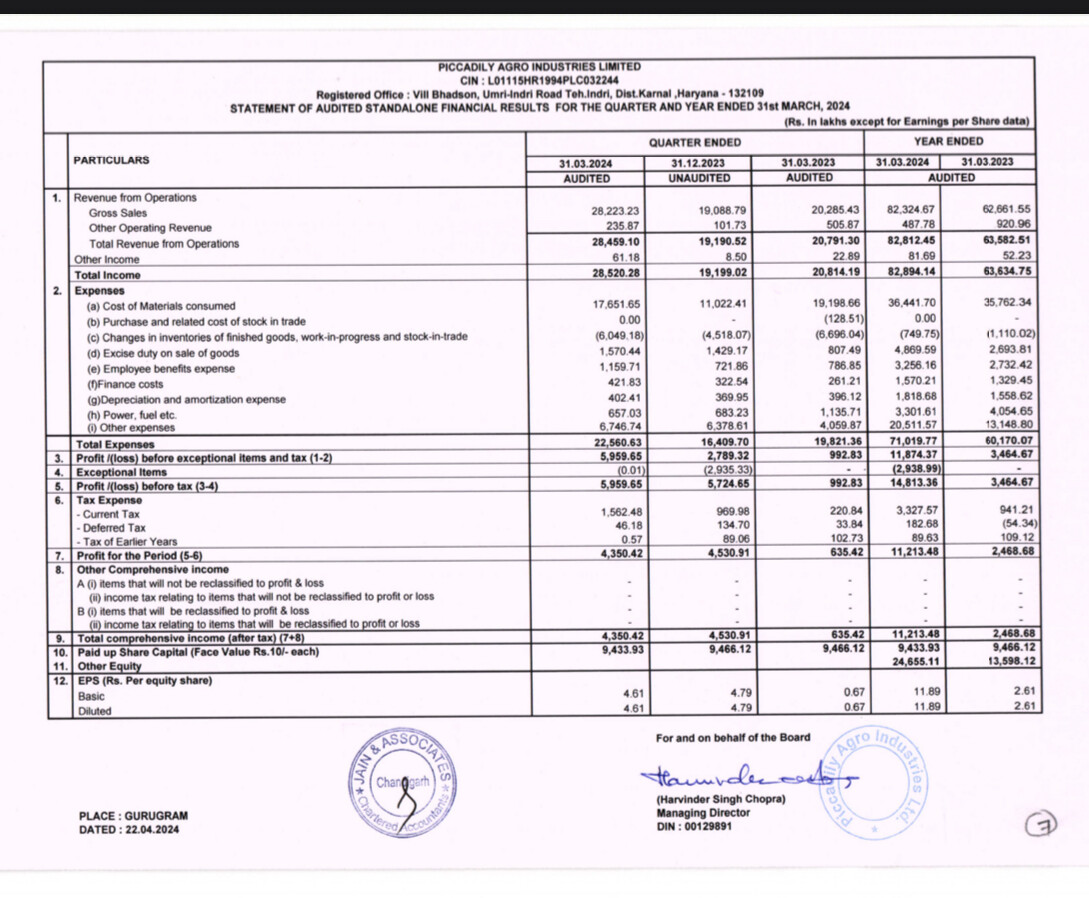

Great year on year growth.

Company is also planning to do QIP of 1000 crores.

Disc- invested and biased

3 Likes

What are your estimates for the next year? If you can please suggest.

Salient points of interview on NDTV -

- Present capacity 12,000 litre malt/day.

- Single malt need 5-7 years to mature.

- Capacity expansion at existing Indri plant.

- New plant coming up in Chattisgarh for malt.

- Capacity in indri will start in CY24 & will be 2.5x that of FY24.

- 30K litre/day malt capacity in Sep-Oct CY24.

- New capacity will take capacity to 60k/day in FY26.

- 13-15% Net Profit Margin for FY25.

- Operating Profit Margin may drop 1-2% from 23% in FY25 with growth

of 30%. - Very bullish about Kamikara rum.

5 Likes

Does this imply that products manufactured with expanded capacity will be ready to be sold after 5~7 Yrs.?

Another question to all who have conviction in this business?

None of the results filing has a business update from the management to the minority shareholders. Even AR has limited insight. How do you make a decision to become and continue to be a shareowner?

1 Like

All your questions are answered in this video.

As far as l know, single malt must be 3 years old to get that tag in UK.i also know that in warm weather of the tropics, aging is faster

And it takes 1 year instead of 3 to get the same effect. So this talk of 5-7 years is somewhat confusing. But in the interview, he also said that the capacity expansion for indri comes online in October. So probably it’s better to wait till the presentation comes out.

Regarding the question of conviction. I am pretty convinced that even at this price it’s cheap considering its plans and growth potential. Even if the eps stays flat for next 3 quarters the Eps per year would be 16Rs and that means the company is trading at 35 PE. Just read this thread from the start and see how the management has executed a long term plan since 2016.

In my case, i bought it around 40 Rs and invested 2% of portfolio. I have already sold some before Q3. So effectively I have invested X, taken out 2X and still have 11X left in portfolio. When I bought it ,'it was selling only about 100 casks of indri and winning awards. Picture is much clearer now and I do not intend to sell anymore anytime soon.

For some considering investing it now, I think it’s better to wait for the presentations ,media coverage etc that is surely going to come before the QIP , in case there is doubt about managements execution capacity or future potential.

9 Likes

BTW, Indri is a NAS (No Age Statement) single malt. The UK law of 3 year aging only applies to whisky produced in UK.

1 Like

very nice article -very relevant for Indri

2 Likes

Extrapolating 4q profit of 40crs to full year FY25 company should deliver minimum 160crs PAT in FY25. So trading at 35x FY25 vs Radico Khaitan at 60x PE multiple.

Most probably PAT should be higher given capacity is going up 2.5x mid FY25 (it also going up 5x to 60000 litres in FY26) from current capacity of 12000 litres.

Disclosure: Invested

6 Likes

You have to put a market order pre market through your broker at 9 am to be ahead of the queue if stock is hitting upper circuit.

2 Likes

Right now it is difficult to obtain the shares. You may have to wait for things to cool down a bit.

1 Like

With the latest developments which have taken place over the last few months viz. - the success of Indri; capital raise which will bring-in institutional investors; step change in the level of ambition which is reflected by the huge amount of capital raise; growth projections and new product pipeline - Piccadily Agro is going through a paradigm shift.

Given its best-in-class performance metrics of highest growth rate & highest margins amongst all alcobev cos. in India, along with its sizeable market share, Piccadily is poised to move from being a little-known nanocap to being the market leader in the Indian premium alcohol market - which is the highest ROCE segment of the market and which all the other majors are trying to push into as the mass market slows down.

Given this background, I feel Piccadily will give United Spirits a run for their money in times to come.

After all, USL wasn’t built by Diageo, current majority-owner of USL, but by a smart & influential Indian (Mallya senior), and I feel, in Piccadily we have the same kind of management / promoters - people who are smart, who understand the pulse of Indians and the industry and people who are extremely influential.

Piccadily overtaking Radico in marketcap seems like a foregone conclusion. Rather, I would not be surprised to see Piccadily overtake USL in marketcap in the next 7-8 yrs.

13 Likes

2 Likes

9 Likes

A stock can’t keep rising indefinitely. It will eventually face selling pressure and hit lower circuit for a few days. In October-2023 Piccadily was at Rs 312, then it hit lower circuit for many days and went down to about Rs214. It stayed in that range for a few months before shooting up again in Feb-2024. This is a normal pattern for stock price growth.

7 Likes

Sir, please clarify why did Mr Batra says single malt takes 6-7 years to be made while you are mentioning there is no aging required for single malt ,which Indri is making.

Bcos all these capacity expansion will kickin post 6-7 years or immediately? Pretty confusing but key statements.

2 Likes