A stock can’t keep rising indefinitely. It will eventually face selling pressure and hit lower circuit for a few days. In October-2023 Piccadily was at Rs 312, then it hit lower circuit for many days and went down to about Rs214. It stayed in that range for a few months before shooting up again in Feb-2024. This is a normal pattern for stock price growth.

7 Likes

Sir, please clarify why did Mr Batra says single malt takes 6-7 years to be made while you are mentioning there is no aging required for single malt ,which Indri is making.

Bcos all these capacity expansion will kickin post 6-7 years or immediately? Pretty confusing but key statements.

2 Likes

Apologies for my out of turn attempt to answer …but here goes …

You should probably listen to the Spotify link in post no . 121. The thing is more complex than simple capacity of malt. Listen from 12 minutes onwards .Piccadily does not make only INDRI …they have other blended whiskies and they also sell a significant quantity of 2-3 years old malt to other whisky sellers as well. Currently they are reducing these external sales but that also means they are not so much constrained in capacity because of malts availabilty but they are constrained by number of casks in which they age the stuff . Currently they have 47000 casks and are going to add 55000 more by end of 2024 . While this indeed means the extra casks won’t get sold just now but the maturing period is also varying depending on the desired finish by the blender and that in turn that depends on their target market . So a bottle of indri bought in Belgium will taste different than one bought in Germany .So while currently they are selling 6 year old casks , since they do not provide any age statement , they can sell younger mix as well if the master blender deems it fit by mixing different casks .

So while it’s true that the expanded capacity will not get sold immediately, it’s also true that they are nowhere near the end of the ready stock since they have not even stopped selling malts to outsiders .That indicates that they do not foresee going out of stock for Indri in next 3 years at least since they are still selling some quantity of 3 year old malts to other breweries. .They are raising the money to buy the barrels for keeping inventory that will get sold in future just like they have kept inventory for past 11 years .

Disc… Invested .

15 Likes

@Metalhead44 - Piccadily currently has 40,000 plus casks maturing in their warehouses. They have enough stock to meet demand for the next 4 or 5 years. This capacity expansion is required to maintain the current rate of supply at current rate of demand. If they do not start capacity expansion right now, they will have to cut down the rate of bottling 3 or 4 years down the line. Cutting down supply is not a good marketing strategy for a brand that is aiming for a dominant position in the market. Once competitors start taking the supply gap you left, it’s very hard to regain the lost market share.

Discl : Invested.

14 Likes

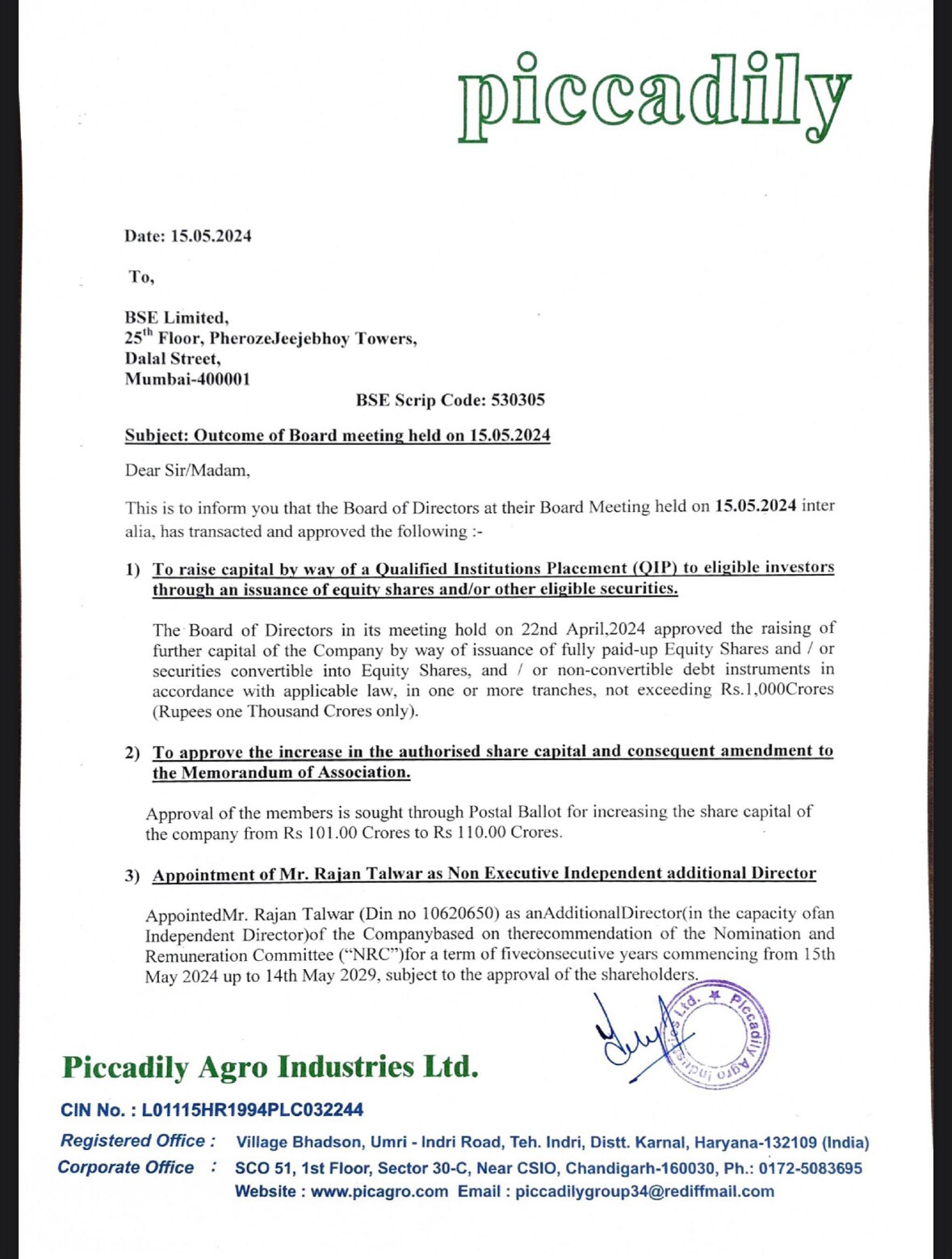

Can anyone guide me how much equity dilution we can expect from upcoming QIP of 1000 crores?

Disc- Invested

Piccadily will gain entry into CSD and CPC canteens in this financial year and this will add significant volumes as defence market is quite big for Indian single malts and Amrut,Paul John ( 3 Variants ) and Radico with Rampur Select and Royal Ranthambore has huge shares in defence markets . Also as imported brands not being there due govts vocal for local brands Indian Single Malts enjoy huge traction in CSD and CPC markets. Amrut and Radico are facing lots of issues in supplying as they are out of matured spirits so this expansion should serve Indri well.

7 Likes

If i remember correctly, Indri had said somewhere that due to the warm weather in North, maturing is relatively faster here as compared to the established benchmarks of Scotland where the climate is completely different.

Would it be fair to say that we can look at expanded capacity selling out in FY26? If that is there, then, I think profits are likely to 2-3x by end of FY26? given capacity itself is going up by 2.5x… some element of operating leverage and conservatively, we can look at 3x profit growth?

4 Likes

In the interview , it was clearly said that malts are sold when it’s 2 to 3 years old to other breweries who produce blended whiskies . So the malt produced in the new capacity will not be fit for sell for at least 2 years . The problem here is we do not have a few important pieces of information…

- How much Indri is ready for sell if someone wants to buy it all today ?

- What percentage of their malt output is being used for their single malts ?

- How many casks of maturing single malt do they have ? All 40000 barrels ?

- How much is profit per case ? How much of the barrel content is lost during bottling ?

There is no end to these questions and while one can get rough estimates , how accurate they would be is anyone’s guess.

As I see it, they did not seem to be worried about satisfying market demand for next few years . One thing is clear…even if they continue selling at present rate …they would earn around 17 rs eps. Even if we give it 60 PE, the stock should be somewhere near 1k . Then with QIP, dilution, expansion and all those present unknowns, I am not getting into complex maths . In my case, I have monetized enough to let it give a long leash and ride it till I envision stagnation (nowhere in sight at the moment) .

@DrHarshilRohit It depends on the price at which they do it . Assuming 750 … they would need to issue 1.2 crore shares. So 1.2/9.4 = 12.7% approx. They have changed the authorised capital to 110 crores… or 11 crore shares . So that is the outer limit assuming lower floor price .

Disclosure : invested since sept 22 and still largest allocation in portfolio by present value.

7 Likes

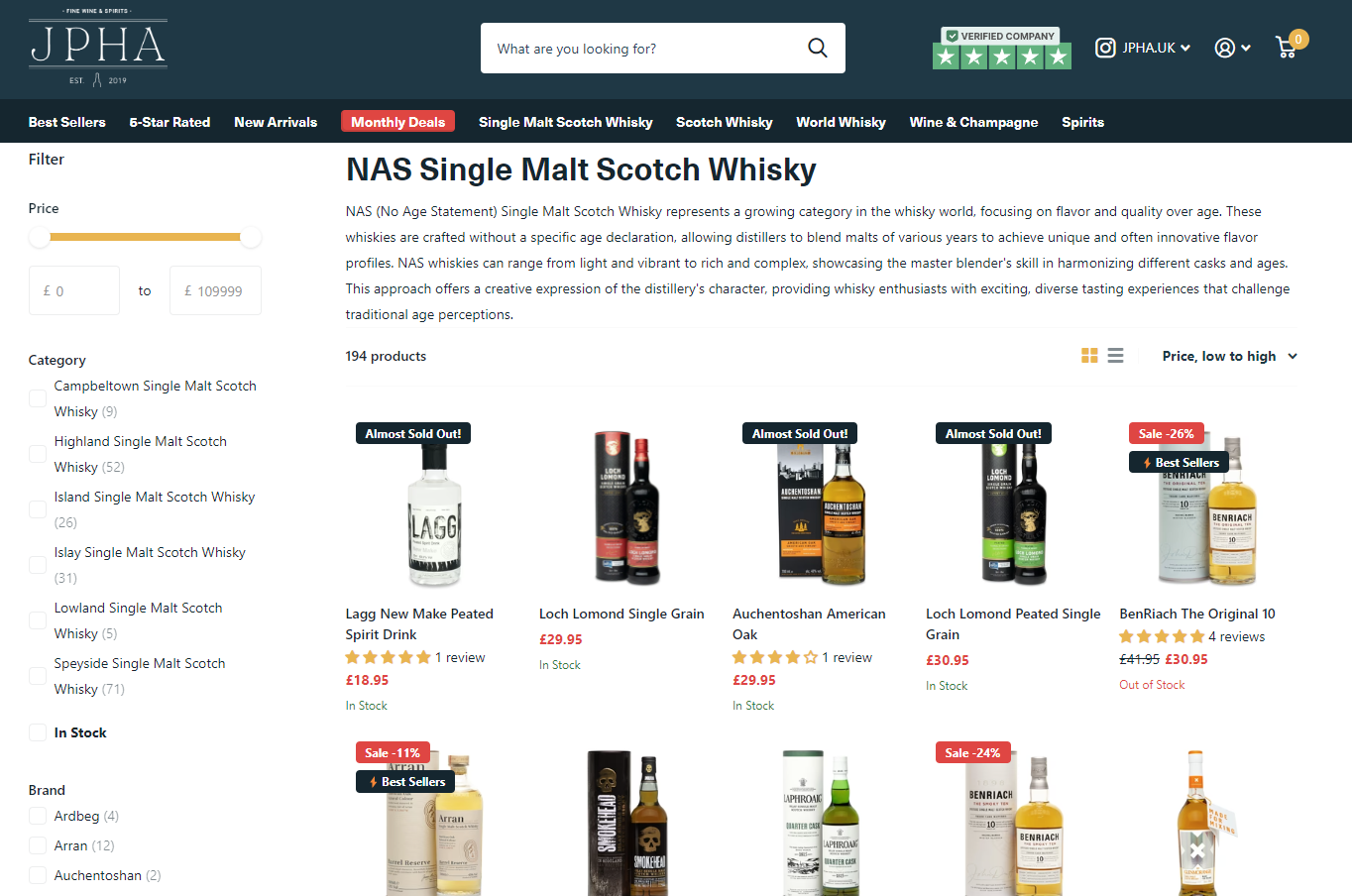

Here are some currently selling brands of No Age Statement Whiskies currently selling in the UK, with the cheapest one costing £30 / north of 3K INR.

To quote what the site says “NAS (No Age Statement) Single Malt Scotch Whisky represents a growing category in the whisky world, focusing on flavor and quality over age. These whiskies are crafted without a specific age declaration, allowing distillers to blend malts of various years to achieve unique and often innovative flavor profiles. NAS whiskies can range from light and vibrant to rich and complex, showcasing the master blender’s skill in harmonizing different casks and ages. This approach offers a creative expression of the distillery’s character, providing whisky enthusiasts with exciting, diverse tasting experiences that challenge traditional age perceptions.”

That being said, we need to figure out what is the minimum time required to make an Indri?

6 Likes

Rough maths based on YT videos

| Total Casks | 40,000 |

|---|---|

| Allocation for Indri | 50% |

| Total Casks for Indri | 20,000 |

| Litres / Cask | 200 |

| Total Volume (litres) | 40,00,000 |

| Typical Bottle Size (litre) | 0.75 |

| # of Bottles | 53,33,333 |

| Per Bottle Realisation (INR) | 4,000 |

| Total Potential Revenue (INR crores) | 2,133 |

| EBITDA % on Indri | 28% |

| EBITDA (INR Crores) | 597 |

So annual EBITDA can be easily 250 crores assuming all of this capacity will get sold out in 2 years - same time when a lot of existing casks would be reused for fresh batches and… and 6-10 months prior to when the new capacity can get on steam.

You can easily alter numbers here depending on your thoughts and arrive at the revenue / ebitda numbers… all in all, Indri seems to be headed for a bumper run over next 4-5 years

7 Likes

How the per bottle realisation is 4000 when in market it is selling around 3000?(

1 Like

True. If you change it to 3500, you get 523 crs of EBITDA… this is a plug and play very crude model - so you can alter the numbers.

What is clear to me is that with 2.5x capex coming on steam later this year… FY27 numbers can be bumper

2 Likes

Yesterday, while passing by a liquor shop near my home in a tier 3 city in Haryana, I was taken aback to see bottles of Indri displayed prominently on the counter. Curiosity piqued, I asked store owner about sales, who mentioned that they sell around 2 bottles of Indri daily. This came as a surprise, considering the modest size of our town; I had expected sales figures to hover around 1 or 2 bottles per week at best.

It seems that Piccadilly Management is strategically extending its distribution reach to smaller cities like ours. Not only is the product available here, but locals are also evidently aware of its presence and are showing interest in purchasing it.

9 Likes

Liquor MRP also includes excise levies being charged by various state governments . MRP varies as per state excise duties slabs . All states different excise duty structures and that is the reason of variation of MRP in different states

2 Likes

How much have the prices of Indri increased after it won the award? Per bottle?

If not much. Can one believe there will be a scope for that to happen?

4 Likes

How is Camikara rum doing? Based on the reviews it looks good although I am unable find that anywhere in the market. Has the management given a split of Indri, Camikara and Whistler sales?

What I like most about Piccadily Agro is “Focus”.

Compared to others such as Radico & USL, who seem to be doing random stuff such as launching products with weird names - victory of xxxx year, launching a few dozen bottles of super expensive whisky at (Rs. 5 lacs per bottle) and struggling with their mass market biz which constitutes majority of their revenue, Piccadily has abondoned the mass market end of the market, gone all out with just one product - Indri, made it super successful with amazing brand recall and consequently brand value. And now, Piccadily is getting ready to repeat the success of Indri with its new award winning product - Camikara rum which aims to create a new category of premium rum altogether. It seems they are on a mission to reach the pinnacle of alco-bev market in India.

9 Likes

A bottle is costing 4360 in Bangalore on 28May24.

Packing date is April 24. Also, the supply seems to be better now. 3 months back, the same shop keeper was telling that there is demand but no supply as the factory is in North India.

2 Likes