thanks for your analysis. can you pls help me understand how 500K barrels with 10 cases per barrel, translates to 5 Lakh cases. Isn’t it 50 Lakh, OR their capacity is 50K barrels (and not 500K ).

let’s assume it is 5 lakh cases, for them to be ready rolling into market around 40-50% of this should be ready after maturing for past 5 years… no?

Also, how’s competition catching up? how’s tis pricing strategy vis-a-vis Amrut and other renowned/foreign brands. I get a sense that there is no pricing attraction of their product vis-a-vis others. I guess this one will be a prime differentiation when other factors are almost similiar…

and Happy Holi to all!

Lots of expensive brands come in 6 bottle pack . e.g grey goose , lots of imported single malts too so as to make brand affordable for trade and make replenishment easier .

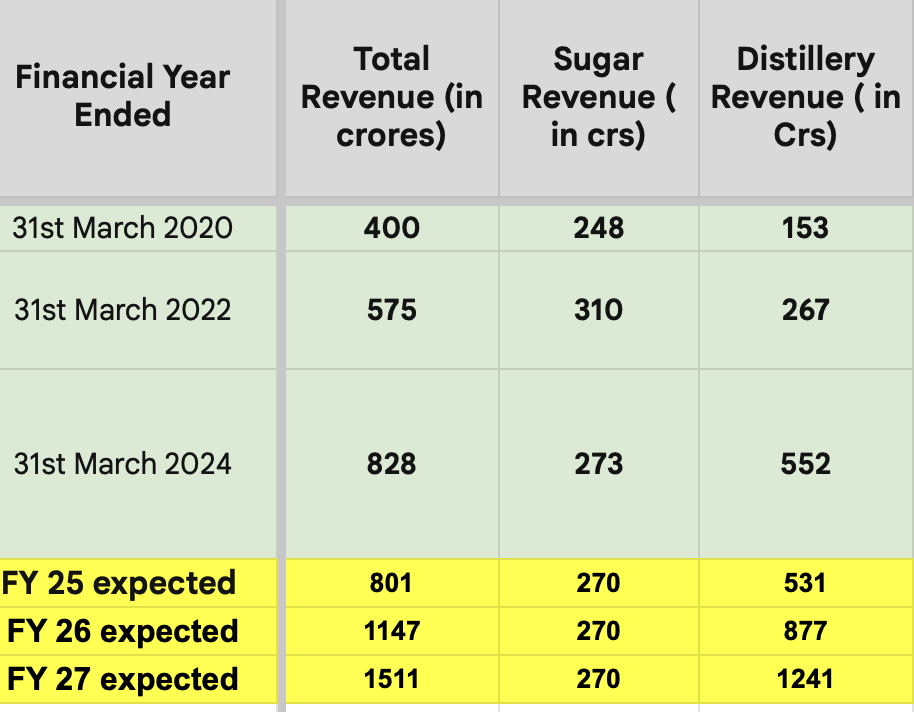

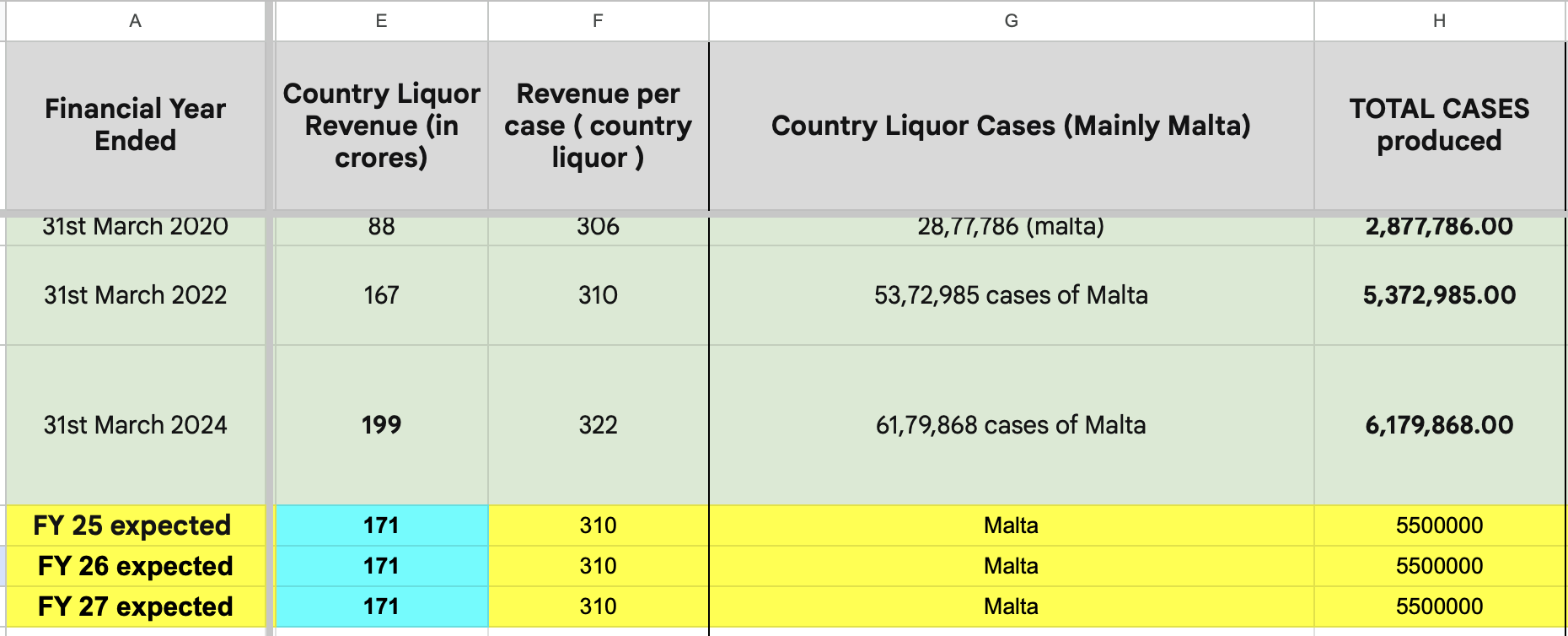

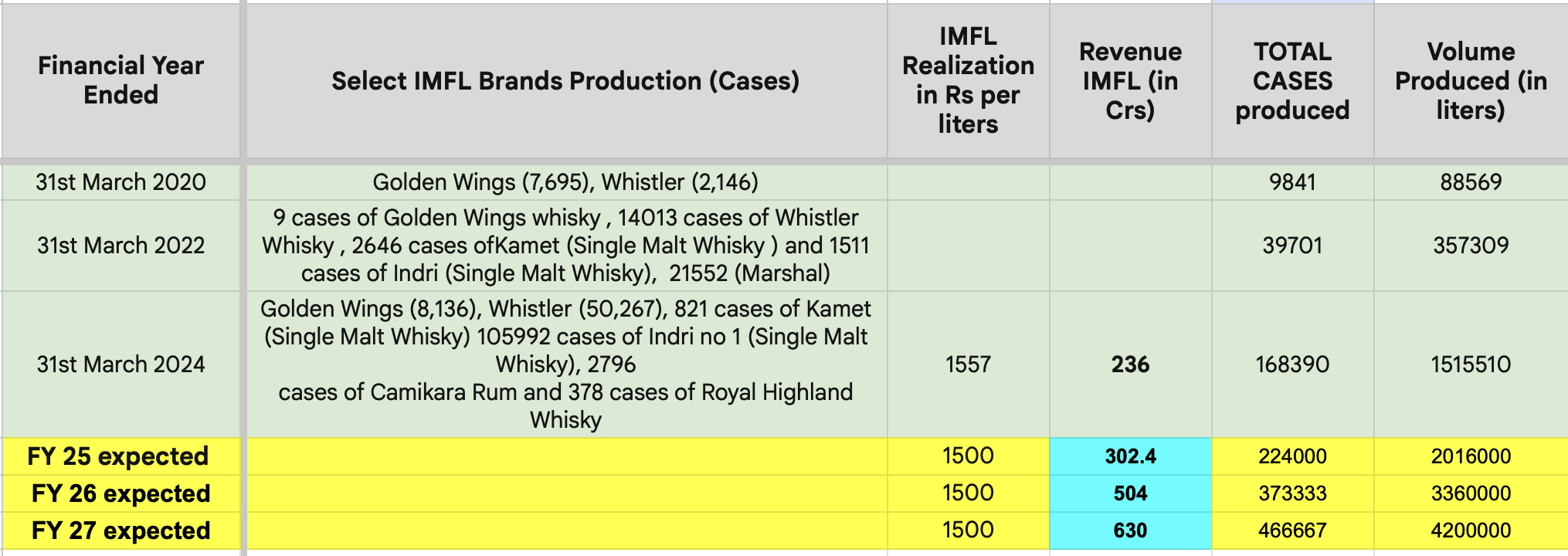

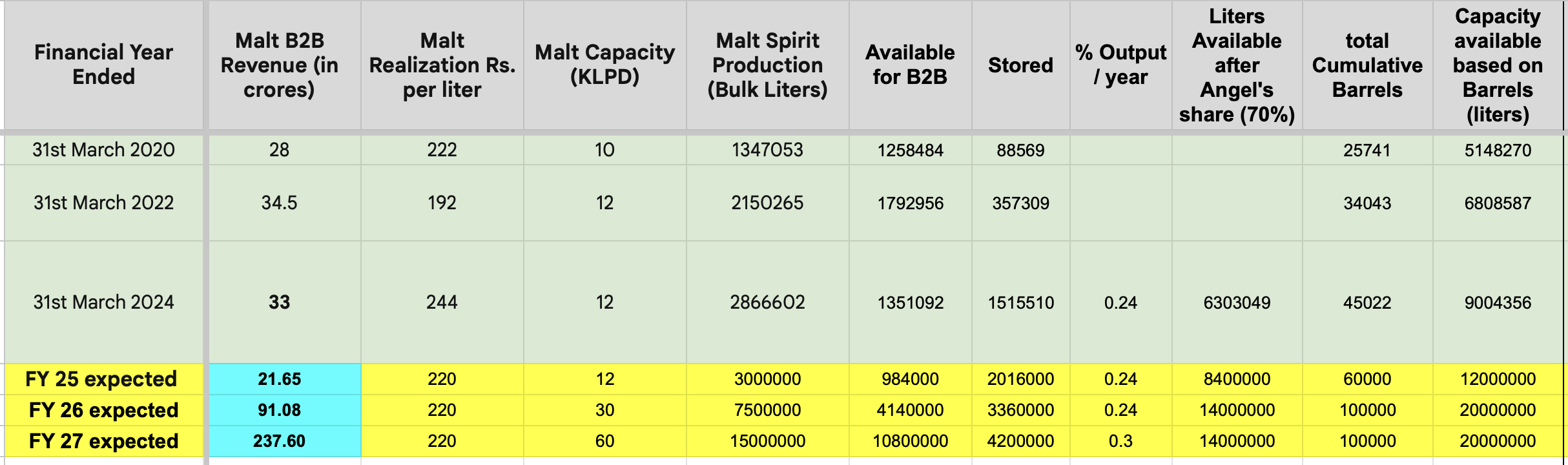

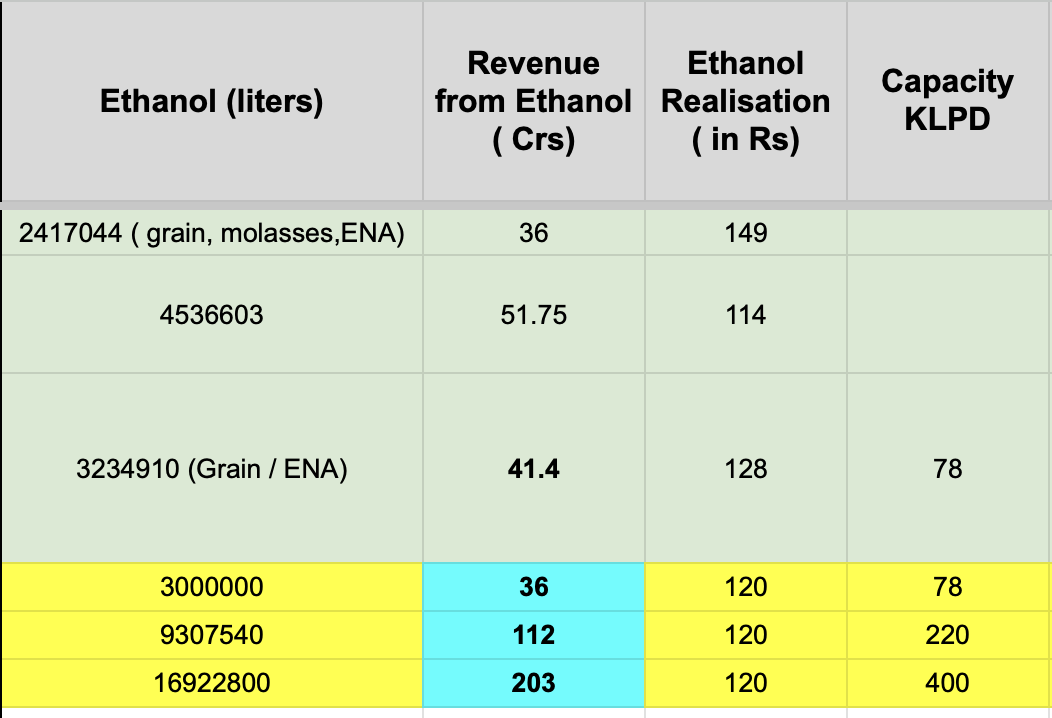

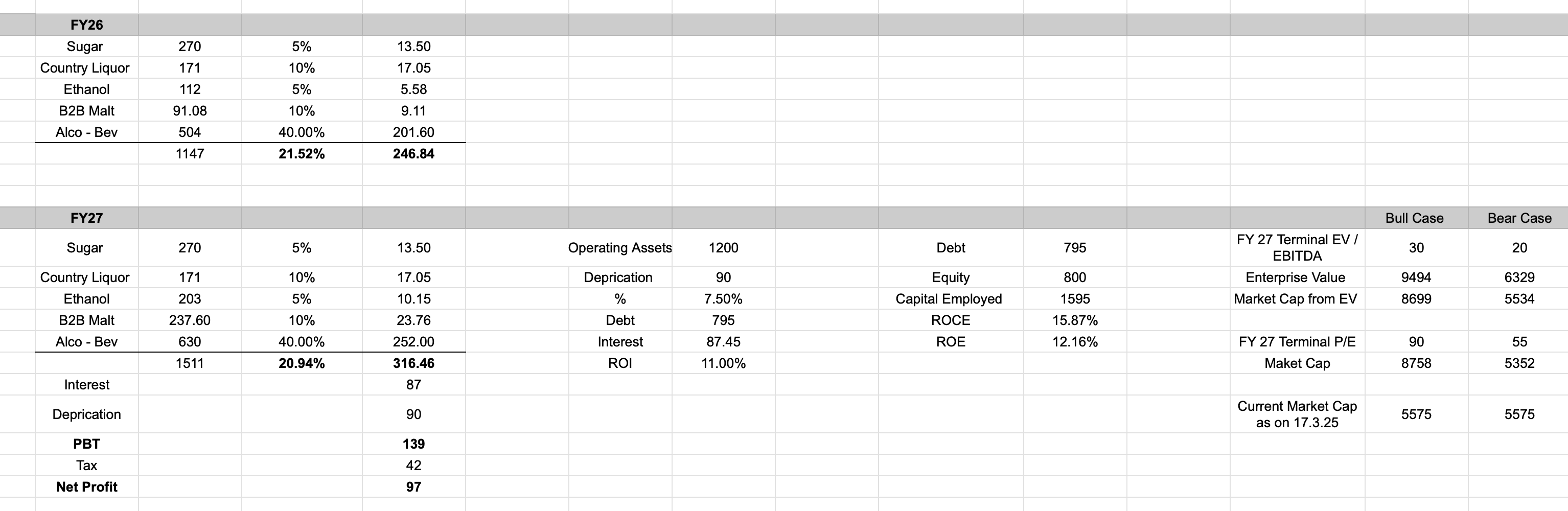

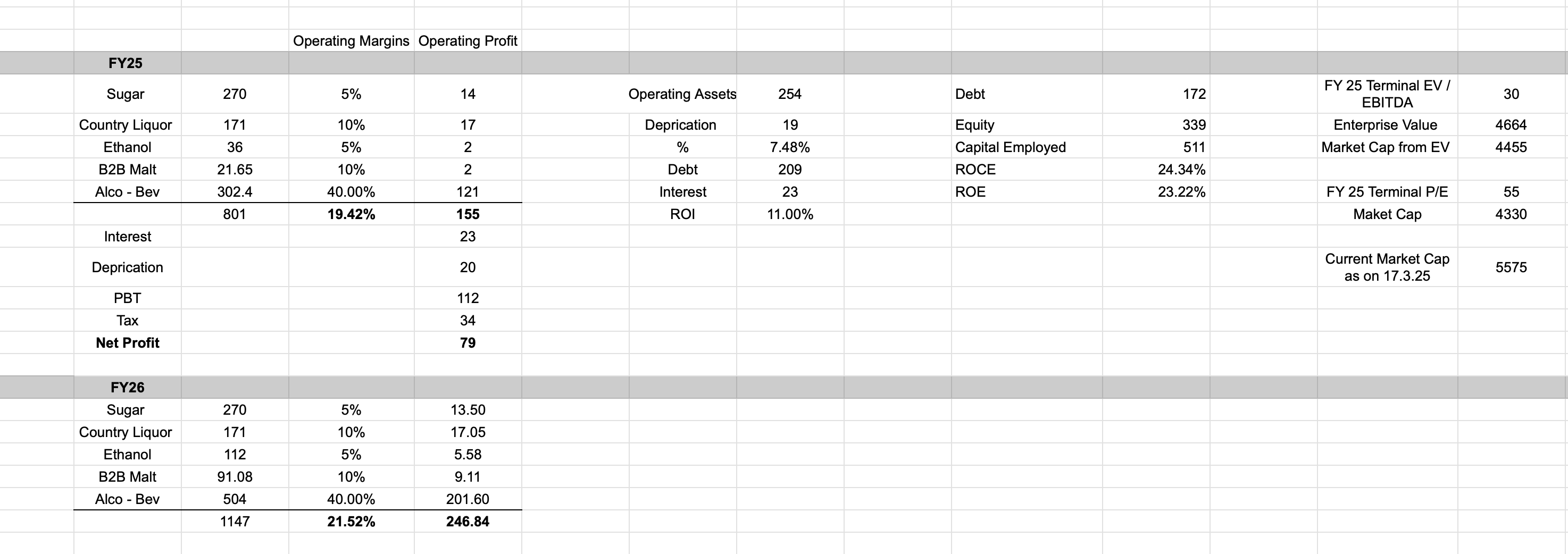

Thanks for your replies. Not an expert in this field , but did some number crunching over the last couple of days. Based on data available from Investor Presentations and production volumes reported from previous years annual reports, company seems fairly valued to me.

I feel like they have good demand for their new IMFL brands but the very nature of producing single malts especially ageing, creates a bottleneck to produce it in quantities. Hence scaling up can be problem where aging is involved.

On the contrary, if they can leverage their increasing brand recognition and make more blended products where production can be easily scaled which they seem to be focusing with greater increase in ENA/Ethanol capacity, they can aim for higher realisation and increased scalability.

I have attached my calculations. Any suggestions on the same are welcomed.

I was just thinking…how many companies do we know internationally/domestically that have made it big with a major focus on premium spirits? Has anybody dug deeper into this ? will help understand if Piccadily is walking the right path. I mean they do have country liquor/under 1000 products but they are never seen promoting them or innovating in that space, Unlike Radico Khaitan.

I deal exclusively in that segment, in 3 of my business, obviously not in spirit.

Hence, What I know is this,

anyone who has cracked the premium segment, should go all in, in that segment, and should ignore everything below that.

We and I personally know many premium brands in saree, clothing, jewellery, cars, electronics, super markets, restaurants, hotels, etc. that deals only in premium segment.

Once you can please the HNIS/Wealthy/Upper middle class. You have to be stupid to be concerned about other segments. Yes, you can create a parallel brand any day in future and do this all over again, and one should too.

But, this segment has higher margin, better loyalty, lesser competition, Stronger moats, also do note that this segment has lesser business volatility, than any other segment/demographic.

So answering your question,

I don’t know why it couldn’t be done by an Haryanvi guy, who is a ministers son, has best of worlds money, intention, and connections, and is running this business from more than last 20 something years.

Well, good to hear from you but you missed my point. The premium liquor industry is different from other industries that you mentioned where Time is not a limiting factor whereas here time is a limiting factor irrespective of how huge the demand is we need supply to fulfill and I can’t completely agree with the less competition part of yours clearly that’s not the case. I haven’t been able to find a company that has turned into mammoths like United Spirits, United Breweries, Radico Khaitan etc… with just premium liquor, they started with smaller ticket sizes, mass production and gradually scaled up to premium liquors (Well awarded and in demand) which even today contributes very little to their Top-Line. India is a different market, global rules don’t apply here Less than 1% of the population can afford Indri like the others afford Beer. We need scale to become big. But still to consider your example Zara is struggling to expand in India where Zudio is killing it and both managed by the same Company.

Definitely an unpopular opinion, specially for this thread.

Hey hi, your POV is utmost valid, and I agree to it, let me add onto it what I mean.

So, on ZARA in india, you see zudio is the better brand suited to India, than ZARA itself, zara was never a premium brand globally.

Zara actually is a brand that got “high-end-ramp” fashion at dirt-cheap rate to the middle class of the world, and it did it best.

This is exactly what eventually Zudio did and succeeded in India. Not ramp fashion, well because Indians MASSES dont look at fashion as the west MASSES does.

Hence zara ended up catering to the fashion-savvy premium strata in India. Also, zara is doing well, but it is already catering to the 1% and is doing it decently well, it cant expand anymore due to saturation of India in that segment, maybe it can grow 200-500% more in future, but thats about it.

However, this company is different as it is not a retail store which is restricted by its location/country and hence, will expand beyond our national boundaries.

Indri is in demand all over the world. Everything produced above india’s needs will be exported.

So to give you a perspective, It will compete with the glen’s-*****(put any name here of your linking) of the world. Think of single malts, bourbons, irish, and scotch brands which are succesful and you shall see the full potential of it.

Regarding size - this company is neither samll/ nor massive, it has atleast 10 times growth potential before it saturates the premium segment in India.

I have not done the number crunching but as far as i remember khaitan premium segment is 500cr. and indri is already doing around 200cr. if i remember right. this is how it went something inline of in terms of cases,

Johnie walker some 28 laks cases

Indri - 1 lakhs case

so yeah, massive leg room of growth is there, also indian preimium demographic is expanding at fastest pace compared to any other strata.

Hope I have been helpful in sharing my POV

(p.s- ill check the numbers and edit the post as I can accumulate better data, this is to just share my POV with you)

I think it is unfair to compare Radico Khaitan and piccadily agro, the only reason is premiumization of the whiskey, as per the annual report of Radico khaitan , there are 2 catagories and their respective sales as follows:

Radico Khaitan

volume (in millions)

fy2024

fy2023

change

prestige and above

11.26

9.35

20.30%

regular and others

13.42

15.62

-14.10%

prestige and above represents premium segment.

whereas premium segment has begun 3-4 years back in piccadily and majority of the portion of revenue comes from country liquor, if you see the production of malta i.e country liquor AKA deshi , fy 2024 states it produced almost 6.1 million cases.

the point is to tell you that if you refer my earlier threads volume growth of piccadily is phenomenol and is likely to continue, the next 2 years is very much important from execution point of view.

just for instance i would like to draw comparision between piccadily and radico , though its unfair but likely to sum-up the discussion.

PARTICULARS

PICCADILY AGRO

RADICO KHAITAN

M.CAP

5991

30851

SALES RUN RATE

832

4626

NET PROFIT RUNRATE

106

307

MCAP/SALE

7

7

PE

56.5

100.5

ROCE

30%

13%

ROE

31%

11%

EBITDA RUNRATE

184

614

CASHFLOW FROM OPERATION

51

183

CASHFLOW AS A% EBITDA

27.72%

29.80%

Due to significant positive change in the product mix, which creates a BAZOOKA for piccadily agro.

whether it will grow 2x ,4x or 10x it will be seen in next 2-3 quarters, the point is how much is they will be able to convert NET i.e profitability.

1 test is already passed i.e profitability, the next test is scale in their premium products.

(Note: most of the revenue still comes from Haryana only, meaning thereby there are other states also for Growth)

Management track record is good, Hope it continues the same.

Disclosure: invested and biased.

Not necessarily when you’re producing for the luxury segment? The margins take care of scale & incremental benefits are far and fewer. Indri already at ~40% EBITDA margin (reasonable guess since it only contributes 25% of total revenues & consol margins are around 22-25%)

Marketing spend will always be high in this segment and maybe you’ll have another 5-10% EBTIDA margin improvement in next 2-3 years.. but that’s about it.

If you mean scale in terms of - product breadth (no premium gin or vodka in their portfolio) or distribution (still not present in some southern states). I would agree.

At this point of time, I want Piccadily to come up with newer products and also tap into global sales. Open marketing subsidiaries in key markets if you want, but go press the pedal. They have enough money in the bank.

This is why I love VP, so many ideas and so many perspectives, and all right in their own way, thanks for all the responses but we are still missing out on my concern maybe I didn’t put it up in the right way, “Time is a limiting factor” by this I meant Piccadily is working only towards aged liquor…check the above article where they have launched a beer which needs 15 months to brew…no doubt there is massive potential and great demand for their products but what to do with it if we have no products to sell because they are still being manufactured? No product to sell = No growth in sales/scale. I am still not convinced as to how they are going to speed up 15 months of brewing or 3 years of aging. Margins are going to be high but it’s of no value if the top line isn’t growing…there is a reason why Indri is sold out in most places it’s primarily because of the demand but also equally due to the shortage of supply. Until and unless they aren’t available 365 days and in most premium stores they can’t multiply their numbers they do this either by purchasing more casks every month or stepping into mass manufactured liquor.

This, I agree, Mohit. But if you see this video which is 11 months old https://www.youtube.com/watch?v=ESC6KU1NaXA. You see barrels in the new warehouse which are ageing since 2022 / 2023.. I think it’s a reasonable assumption that a lot of this liquid will be coming onto the market in next 1 year or so?

If you add another 1 year to the mix, I do feel supply side challenges should be ironed out. But it’s all a guess at this point (specifically in the absence of con-calls).

Agree Even top liquor companies like Diageo , Pernod also needs to be in mass and volume space . Infact Diageo acquired Unites Spirits to get share of volumes and they are still continuing selling McDowell’s range in India and its the biggest brand for them in India and Diageo also hold largest luxury brand portfolio including JW Blue , whole range of malts, Ciroc , Don Julio so and so forth .PAIL is growing well but for it grow beyond a certain point will become tough and challenging .

Thats why they are going all in on capacity front, I mean they are setting up warehouses , changing product mix, they are able to maintain margins, all this shows that a circle has started filling up, will they be able to complete is a matter of time, well on valuation front, it cannot be said said that stock is cheap, ofcourse it is expensive but on a relative valuation basis it is trading almost half.

one important point while comparing piccadiliy with the likes of united spirits, Radico Khaitan and others…

just give the importance on volume growth , i will not say it is the only parameter but as we are talking about consumption, volume growth will be a great indicator. if you see united spirits you will hardly see a volume growth of 1-2% and in some segments there is clearly degrowth, Radico is showing good volume growth on premium segments around 20%… and now there is piccadily where there is Mammoth growth in volumes… so things are turning well.

surprisingly, united spirits trades at 70PE and radico khaitan is trading at 100PE…

Piccadily is trading at 60PE, but wait give time to adjust their figures in the coming time and maybe it will be a point of trigger for PE ReRating.

Disclosure- Invested and Biased

Founders Reserve.pdf (382.3 KB)

New Limited edition whiskey launched. Slowly and steadily making portfolio bigger and better. Total of 1100 Bottles - Half in India and half will be sold in International markets.

Market price is not indicating a blockbuster qtr. Even at this price PE is around 50. Only a better than expected qtr can lift the share price on immediate future. More, traction and upward movements will come from post announcement of expansion which is suppose to be completed by August. I am hanging tight even in this downturn. Yesterday indexes were doing good but this scrip keeps falling. Staying patience. Any other take?