Usually tarriffs are applied based on country of origin rather than port of origin .Otherwise anybody would circumvent them . So if the product is made in India , the tarriff would be at the rate of Indian whiskies. But what defines country of origin is another question…does bottling it in scotland make it a scottish product !

Frankly, I am not getting too deep into it since , as I see it, reciprocal tariffs are not going to make it any worse for Indri sales in USA and thats enough for me .

Disc: Still invested and now there is no point in selling until it goes to 1200 atleast ![]() .

.

1 Like

Tariff on alcohol trade between India/US is inconsequential for most Indian alcohol companies.

India can drop the tariff on US alcohol to zero, US will do the same as per reciprocity. There is no great demand for US liquor such as Bourbon/JimBeam/JackDaniels in India- its not that popular. So, I see zero impact on Indian alcohol companies.

As for UK’s scotch whisky, it can take some share away from premium Indian whisky if it was priced cheaper. But India has refused to drop the tariff on scotch whisky as UK doesn’t really carry any leverage in trade talks with India.

2 Likes

India slashed import duties on Bourbon Whiskies from 150% to 100% ( Basic 50% and an Additional levy of 50%).

The import value of Bourbon whiskey in 2024 till date is around USD 8.8mn which is very insignificant.

Moreover, a Gamechanger product “DRU” Malt whiskey which is exclusively designed for export market as the content of Alcohol is more than 50% which is not permissible in India, is Ranked as the best whiskey of the year 2024 attaching a screenshot of the same.

On the contrary, Madhu Kanna of Piccadily Agro Industries projects a 40% increase for Indri, targeting markets in China and Africa.

Fundamental is strong, price correction is witnessed in recent times.

Remember we are just not even the Tip of iceberg, well all goes well with the management, this will be the story to remember, considering the Demand and genuine reviews of the customers of piccadily agro.

3 Likes

WWhiskiesA25-WinnerList-A4-v3.pdf (1.5 MB)

Search by Indri.

1 Like

Bourbon as a category is not that big in India .Probably Bourbon producers need to invest big time in india to have significant presence . Jack Daniels is categorises as Tennessee whisky and duty reduction benefit will come only if they categorise it as bourbon whisky .even Irish whisky like Jameson is more visible than leading Bourbon brands .Jim Beam since being produced in india might have good price advantage and more Bourbon producers will start producing in india

2 Likes

I have just gone through the thread. I have two questions,

- Since management never does concalls has anyone ever attended their AGM? What was the experience? Were they open to sharing the information and clearing the doubts? It looks like from the thread, no one has shared their AGM experience after 2011.

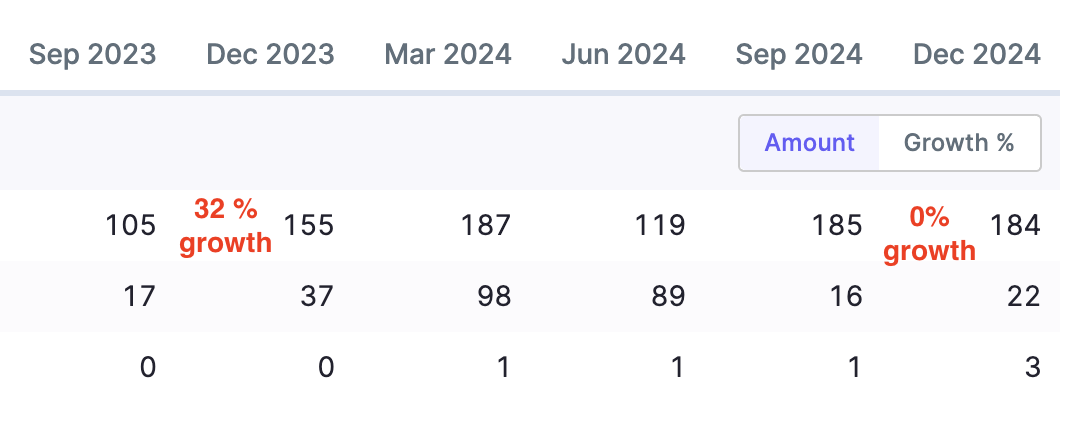

- The thread is filled with posts that Indri is out of stock everywhere. But somehow there is negative growth in the Distillery segment from SEP 2024 to DEC 2024. I am assuming December is usually a good quarter for alcohol companies. Whereas last year it had 32% growth from 105 to 155 cr (SEPT to DEC). If the brand has such a pull then they should have at least made a new high in the Distillery segment. Do we have any understanding of this?

Disclosure: Not invested. As of now trying to understand the business.

1 Like

| Distillery Segment | Q2FY25 | Q3FY25 | QoQ % |

|---|---|---|---|

| Revenue | 184.88 | 183.91 | -0.52% |

| EBIT | 44.21 | 51.58 | 16.67% |

| EBIT Margin | 23.9% | 28.0% |

Rise in EBIT margin indicates higher share of premium alco-bev sales (majorly Indri). It’s entirely possible that counry liquor segment might have degrown in Q3 and hence the decline in revenue.

Premium alco-bev brands were ~200cr in FY24. Assuming 50% rev growth, this is 300 crs in FY25, bulk of which will be Q3 and Q4. And this is the segment where Piccadily has 35-40% EBIT margins (or maybe more)

4 Likes

Any idea on the current capacity utilisation? As per latest presentation they are expanding capacity significantly in FY25 and 26… were they constrained by capacity and therefore no expansion in revenue?

Just came around the query, will try to address the same to the best of my knowledge,

well divide the results of PICCADILY AGRO IND into Two segments,

1.Sugar

2.Distilliery

well if you consider the sugar segment of the same there has been a clear degrowth YOY, and there has been a clear Double digit uptick of more than 15% in Distillery segment, clearly embarking a journey towards high EBITDA margin business.

Moreover, one needs to understand the business model of the company,

- company is in the phase that it’s products like single malt whisky is gathering international attention.

- secondly, other products like Rum, spirits and other whisky which are specially meant for foreign countries ( refer my previous reply) are also picking up.

- Third and last, if all odds are in favour then what’s left, its the management and the team around the same, they are confident to grow more than 30% after the expansion which is scheduled in FY 2026, which is chattisgarh plant and scotland buyout.

Attaching a screenshot of the results for your comparison.

Hope it helps.

Disclosure - Invested and Biased.

2 Likes

Couple updates from the recent notification posted by exchange

Infomerics Ratings has upgraded its rating assigned to the bank facilities for the long-term facilities to IVR A- with stable outlook and short-term facilities to IVR A2+.

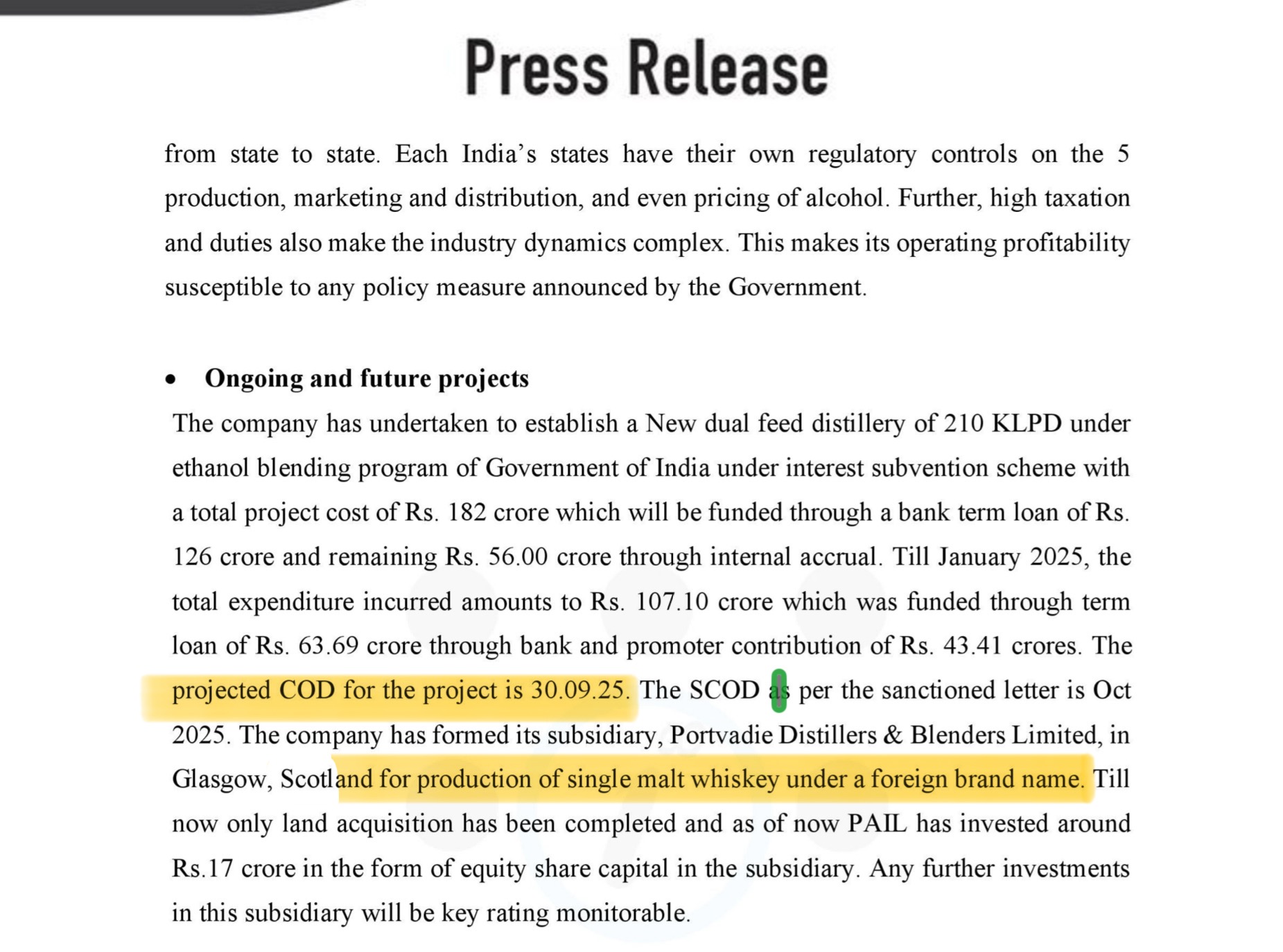

The recent notification states that ongoing expansion will get completed by 30 Sept.

This is the first hint that subsidiary bought in Scotland is for a new single malt.

It has been said that differentiating factor of a great management from an average one is that great management finds ways to develop new products/verticals to add to topline every couple years while scaling up already well established products and Piccadily is doing that very well.

Disc- have been invested from lower levels

3 Likes

Frankly, do not get too excited about the Scottish distillery and its outputs . It has been mentioned in the Annual report of FY21 and nothing has happened since .Scottish outlets say it’s supposed to be a 15 million GBP (nearly 170 crores) project but company and the rating agency says 17 crores…matter of a missing zero somewhere over the ocean perhaps ![]() . The site they bought was an old defunct oil drilling village which was bought by Loch Lomond owners to refurbish as a whiskey distillery cum visitor centre .But then Piccadily bought it but even now there is nothing done yet . Considering in cold weathers it takes a lot longer to age whiskies, just think about the long years before they can start selling single malt whiskey produced there .It probably was just a family milestone to have a distillery in Scotland and they bought it when not too many people were looking at the company and nobody asked why .

. The site they bought was an old defunct oil drilling village which was bought by Loch Lomond owners to refurbish as a whiskey distillery cum visitor centre .But then Piccadily bought it but even now there is nothing done yet . Considering in cold weathers it takes a lot longer to age whiskies, just think about the long years before they can start selling single malt whiskey produced there .It probably was just a family milestone to have a distillery in Scotland and they bought it when not too many people were looking at the company and nobody asked why .

Even the visitor centre in Indri is also taking years to reach completion.Let’s hope they finish the Chhattisgarh expansion this year .

The management is nonchalant about shareholders mostly as they do not do concalls and neither do they reply to mails (own experience) .How ever, they do know their business very well and one can expect them to do well in future too but it’s better not to expect things to happen fast .

Disc. Still holding and it’s still the largest allocation at current price .

5 Likes

Well it seems a Good Rating Upgrade means a sustainable cashflow with an increased profitability along with smoothening of cash conversion cycles.

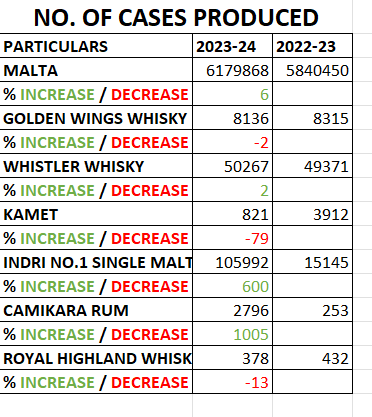

I would like to make a point regarding production of products and trying to communicate that management is serious about changing product mix… attaching a screenshot of product mix.(source: Annual report)

.

.

Folks,

as you can clearly see the Product mix play can lead to dramatic improvement in financials. moreover, the management is guiding for increase of production in malt segment and other distillery segment (Source: Annual Report)

This clears doubt regarding how EBITDA will increase, how cashflow will be sustained, how operating leverage will get into play and ultimately leading to margin expansion.

Hope it helps.

Disclosure: Invested and Biased

2 Likes

Visitor center is already open. Around 1 week back. Someone senior from Piccadily had mentioned about it on linkedin.

5 Likes

I think promoter also mentioned in one of his interview that it was their grandfather’s vision/desire to have a distillery in scotland. I think it’s more of a vanity project instead of some venture they expect great monetary outcome.

New to this industry. Each case has 6 bottles of 750 ml each. So one case is 4.5 liters? Is my assumption correct?

1 Like

For whiskey each case has 12 bottles (750 ml) and for champagne it’s 6.

1 Like

Is this one case? Why just 6 bottles?

1 Like

where to get this data?

Read Annual reports of previous years.

3 Likes

Had prepared the same basis inputs from annual report