Investor presentation is not giving much information. They should have at least put some dates for these expansion plans. Earlier it was supposed to be by end of the previous year but now those are ‘in progress’ items. They should behave like big companies and start taking up investor concalls. Stock price fought for few mins and now again lower circuit. No clarity of geographical sales, work completed, about nse listing etc. More clarity would be helpful from here on.

I would like to add interesting data point i.e PAT as a % of revenue for different companies

| FY | 21 | 22 | 23 | 24 |

|---|---|---|---|---|

| UNITED SPIRITS | 0 | 2.61 | 4.05 | 5.41 |

| UBL | 1.12 | 2.79 | 1.83 | 2.24 |

| RADICO KHAITAN | 2.52 | 1.99 | 1.73 | 1.69 |

| SULA VINEYARDS | 0.72 | 11.5 | 15.18 | 15.28 |

| ALLIED BLENDERS AND DISTILLERS | 0.04 | 0.02 | 0.02 | 0.02 |

| PICCADILY AGRO | 3.68 | 5.06 | 3.66 | 10.91* |

| *The above figure excludes impact of other exceptional income. | ||||

| secondly, this figure of 10.91% can expand to 15% in FY-25 considering the current Run rate. |

Moreover, If things go well around Chhattisgarh unit expansion, warehouse capacity increase to 2-2.5x and currently DEMAND IS Powering than SUPPLY,

the result was not on expected line of Q3 but considering the premiumization of INDRI, CAMIKARA… i think it is just the starting point…

Disclosure: invested and biased

you are right -its just the starting point .According to me their profitability bcos of Indri will skyrocket . Simple example their closing stock at cost is valued at circa 200 cr -but malt under maturation is highest in India (7.8 mio ltrs ),this should be valued according to me over 1500 cr (the more it ages the more value ) ,triangulating this info and other data point I expect Indri to have gross margin of over 70% !!

Disc-views may be biased bcos of my holding

No senior here but from what I can analyze, the next support is around 640 levels followed by 620 if you are a long-term investor all of these shouldn’t be a matter of concern but if you are riding the wave then a breach of 620 might take the stock much lower.

In these sort of markets technicals don’t work that well . In October end it went to 630 …let’s hope it bounces from there . It’s testing times for conviction . I am also regretting not selling at 1000 level but problem with selling now is that no one will tell you when to buy it back .

Disc: It still remains the largest position in portfolio .

Not a pure Technical expert or fundamental expert, its true that sometimes it creates some shakiness in the mind too but well i am not great believer of PE ratio but i would say long term growth rate of 35 to 40% on topline can translate the net earnings to 3x to 4x by FY-27. The good thing to note here is long term PE range would be 45-60. At current levels Risk To Reward is still looking Favorable.

Disclosure - Invested and Biased

Interesting point is to note that PICCADILY AGRO is a net cash company meaning thereby it holds 234 crore of cash as against 209 crores of debt levels, moreover inventory holding levels are decreasing indicating demand is outpacing supplies.

some of the members shared in earlier replies regarding capacity building in Chhattisgarh, new company purchased in scotland ( Regarding scotland company which the company is acquiring are not having good fundamentals, rather it is a LOSS making, hopefully PICCADILY AGRO will turns the table.), if the capacity and expansion gets swiftly on the table then Top line growth will fire. Moreover, the current market condition seems to be more of Time correction, It will turn out to be value in conjunction with growth stock.

Disclosure: Invested and Biased

The new notification on the exchange of preferential allotment utilisation says that all the money i.e 12.5 crores were put in fixed deposit. Wonder why it was not pit in the business? Anyone any idea?

First of all, this is not a violation, so it is just an Unutilized amount raised via convertible warrants around September. moreover the amount which is raised via convertible warrants is being monitored by monitoring agency named ICRA as per SEBI (LODR Regulations).

The 12.5 crore of amount is just the unutilized amount and it is reported on quarterly basis and certified by a Chartered Accountant.

Hope it helps, thanks.

Disclosure: Invested and biased.

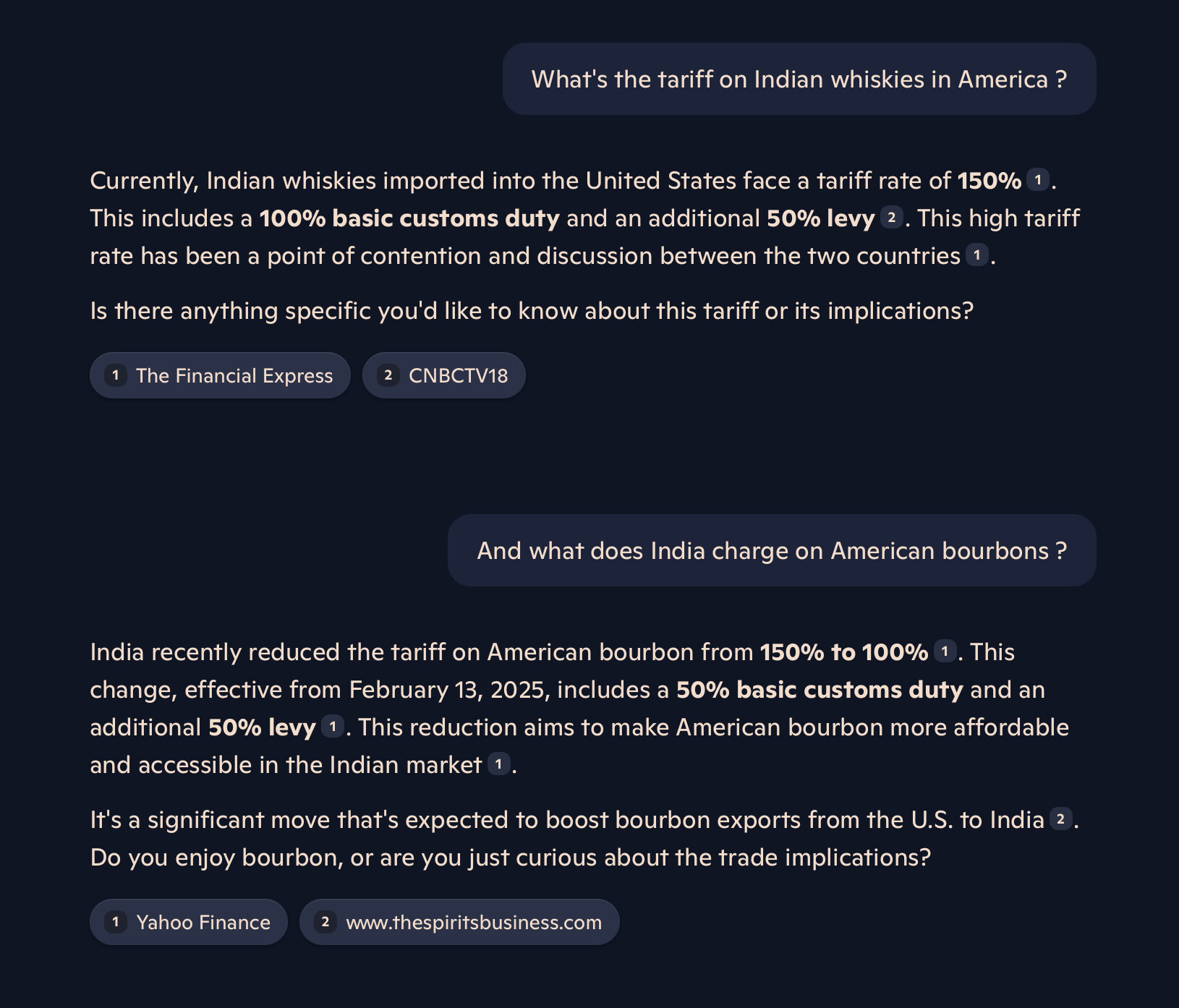

I am trying to assess the impact of this move on Piccadily.

I tried finding geographical revenue split (in PPT) however it wasnt mentioned.

Also even if I find it - I dont understand this market properly - and hence hard to comment. Any expert views on this duty cut and how this affects Piccadily (apart from the obvious that those US Whiskies now get cheaper to consume and hence pressure for Piccadily) ?

Simple Google search gives this information

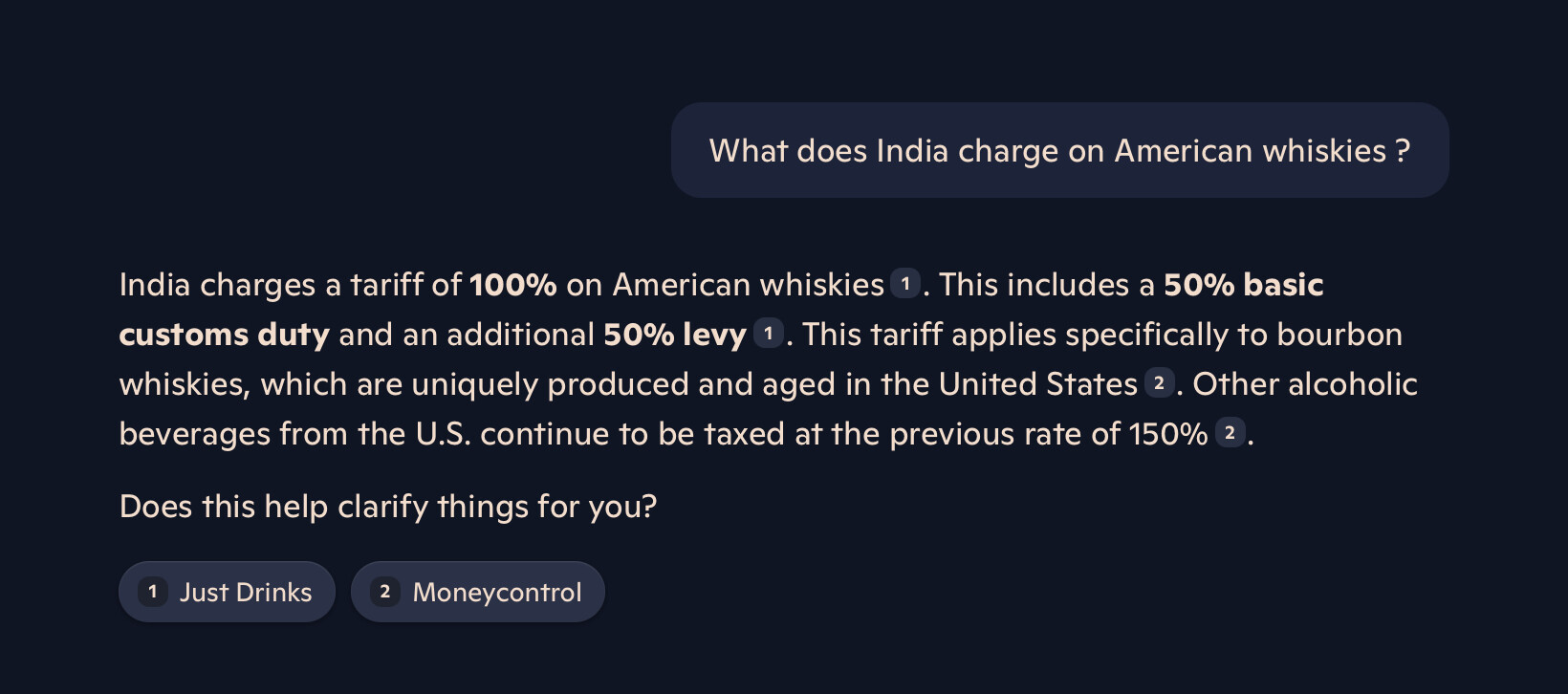

How is bourbon different from whiskey?

The main difference between bourbon and whisky is that bourbon can only be produced in the United States of America (US). Similar to how Scotch whisky can only be made in Scotland, bourbon whisky cannot be made outside the US. Some other rules need to be followed to craft bourbon.

Indri Whiskey is in Single Malt category and comparatively higher priced and competes with likes of Glenlivet etc

Summary - Its different category for Indri and US wants to push Made in America Whiskies(Bourborn) as part of Trade agreement

Recently Invested and At Loss

Below is what the new prices in Delhi should be of bourbons. Extracted through AI.

Yet, my assessment is that Picadilly should be slightly lesser affected as they don’t have problem of over supply, they had good demand and limited supply. Hence they should be able to sell in india or Export. But yeah margin can shrink as per my assessment.

Old vs new price estimate -

|Jack Daniel’s |₹3,250+ |₹1,800 - ₹2,000|

|Jim Beam |₹3,000+ |₹1,800 - ₹2,000|

|Maker’s Mark |₹4,000+ |₹2,200 - ₹2,500|

|Wild Turkey 81 |₹3,500+ |₹2,000 - ₹2,300|

|Four Roses Bourbon |₹3,800+ |₹2,100 - ₹2,400|

If anything scotch will become costlier in USA compared to Indri if reciprocal tariffs are placed. USA actually already charges more than India does .

Quarterly result were inline as far as the volume growth was concerned.

As per my analysis, Indri is on track to touch ~180k cases mark for FY25 implying a YoY growth of ~80% for FY25

(Growth of 236%, 443% & 43% in Q1,Q2, Q3 respectively. Q1 & Q2 was from a lower base before Indri became famous and hence the exponential YoY jump)

Other premium product, Camikara, also seems to be accelerating as premium products volume growth (at 51%) was greater than Indri’s volume growth at (43%) for the quarter Q3.

Distillery biz EBIT & EBIT % improved substantially YoY & QoQ as premium product gain saliency in the overall sales mix.

As per my analysis, EBIT & EBIT% would have been even higher had the other expenses related to sales and promotion for Indri & Camikara not been there. Hence, profit was slightly below my expectation. But its normal to spend on sales and advertising when pushing a new product in new markets.

Sugar biz was a drag with negative EBIT, but I guess none of us really bothers about that - we are here just for the distillery segment.

Stock price has reacted negatively over the last couple of weeks with market being in a bear grip. But not sure if such a fall is warranted. As I have said before, I believe Piccadily will be the biggest alcohol company by Marketcap - bigger than United Spirits - in India in times to come.

Disclosure: Invested and adding more in this fall

you mean Fy25,right?

Similar take. So many good things with the company in progress. Businesses takes time to become bigger. Its good time to enter given small size deter big fishes to remain on the fence. Seems they have already opened the nice looking experience center. Has anyone visited there and can share the experience and enthusiasm? Any new news/ideas on capacity expansion timelines?

Disclosure: Invested and biased and adding more at lower level.

The expansion plans may come live by Q1/Q2Y26. However, I am assuming that due to the required aging process, the alco-bev produced with this additional capacity would take time to become commercially available. This expansion would increase both their manufacturing and liquid storage (barrel) capacity.

If PAIL decides to export to US from the European site, would it still be subject to tariffs treating it as a European product or it would be considered as a Indian product and subject to Indian Tariffs?