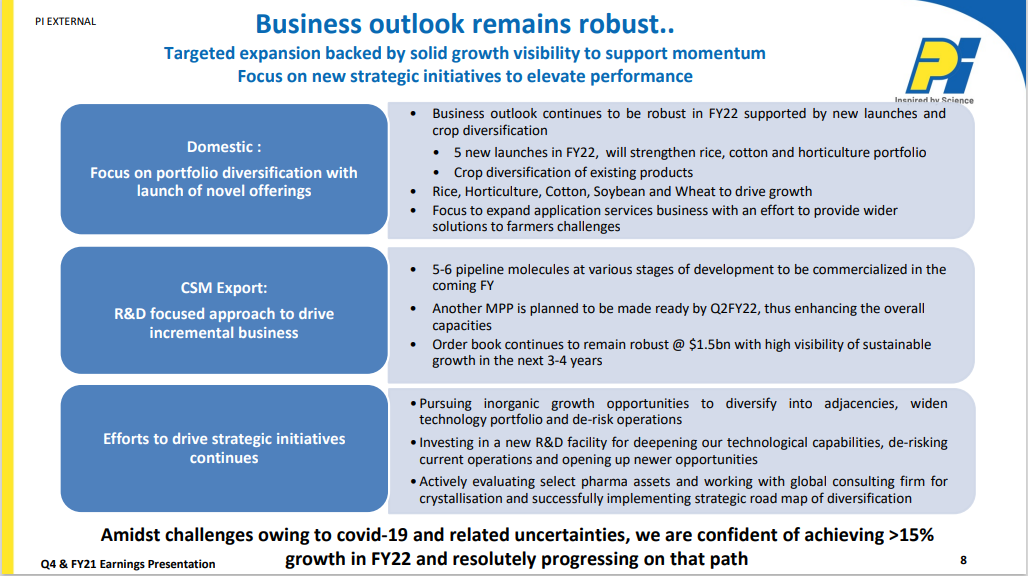

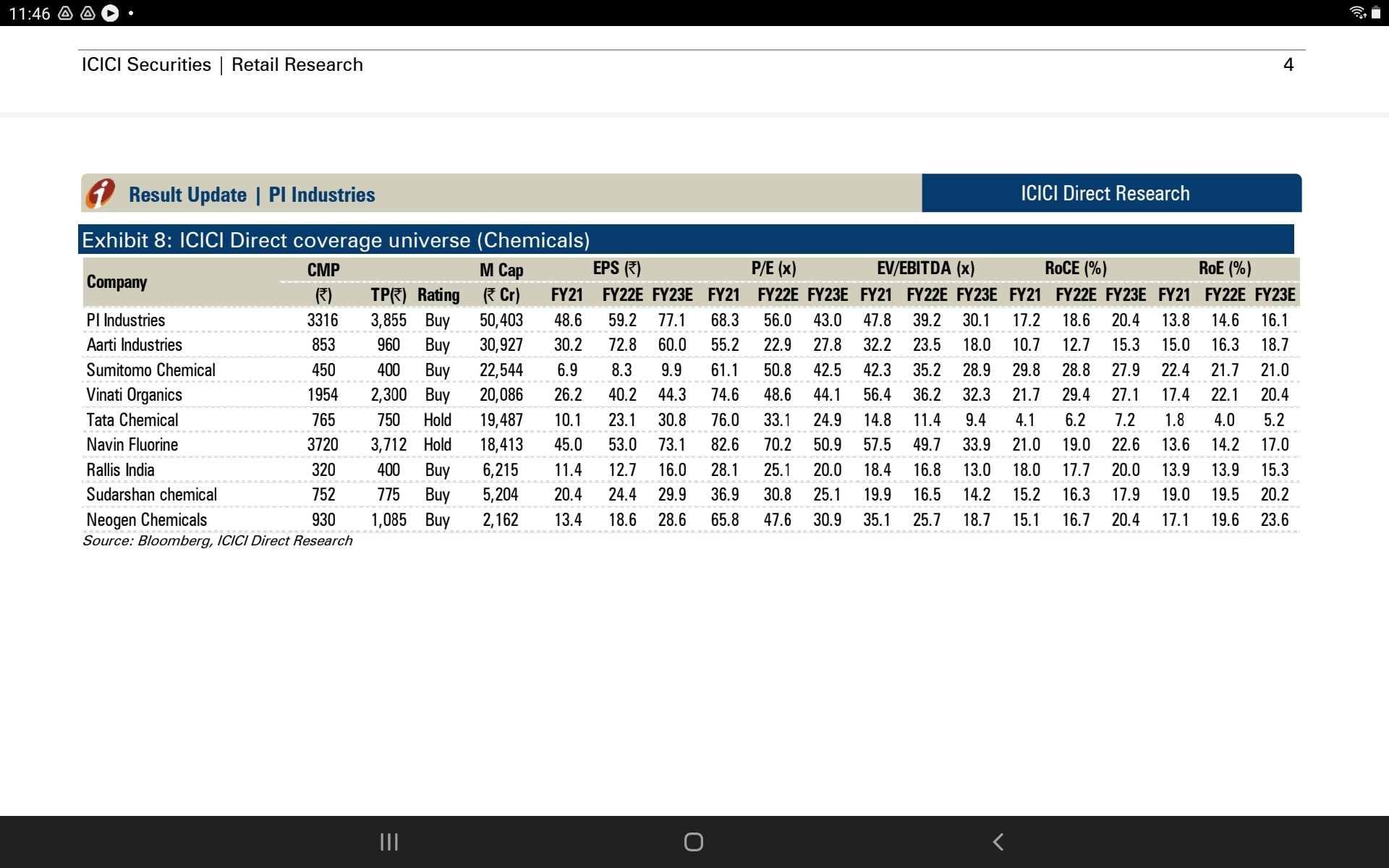

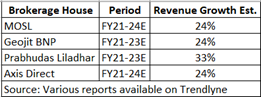

In its Q1FY22 analyst call, the management gave a guidance of 15% organic growth for the current year. The company also said the order book is more than $ 1.5 billion (Rs.10,000 crores plus) and sees “robust growth in the coming years from new commercialisations”. Elsewhere, Joint MD Mr. Rajnish Sarna is reported to have said “inorganic growth is the way forward” (click here). Most brokerages are factoring in 24 – 25 % growth for the company going ahead.

Let us try to join the dots.

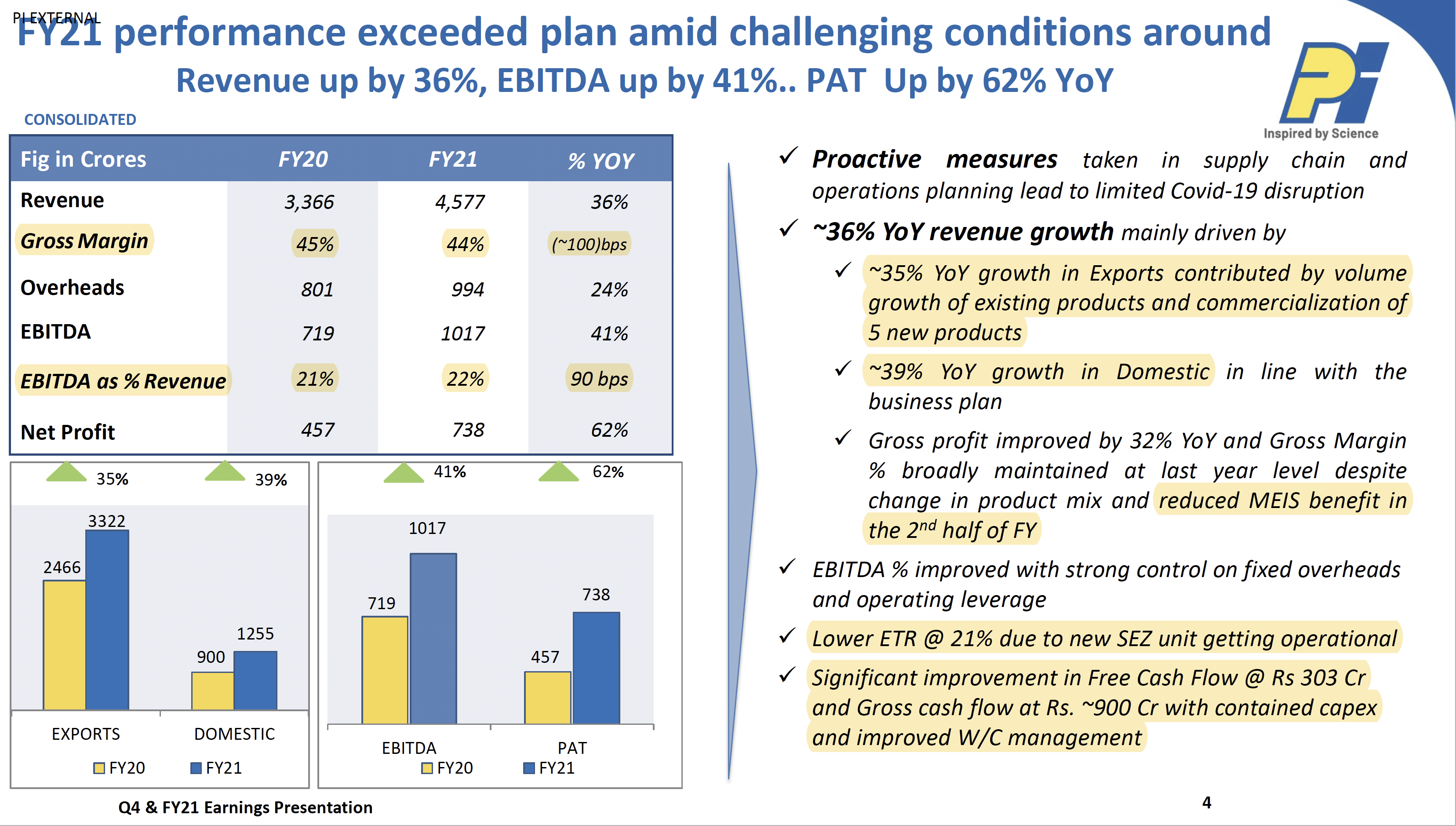

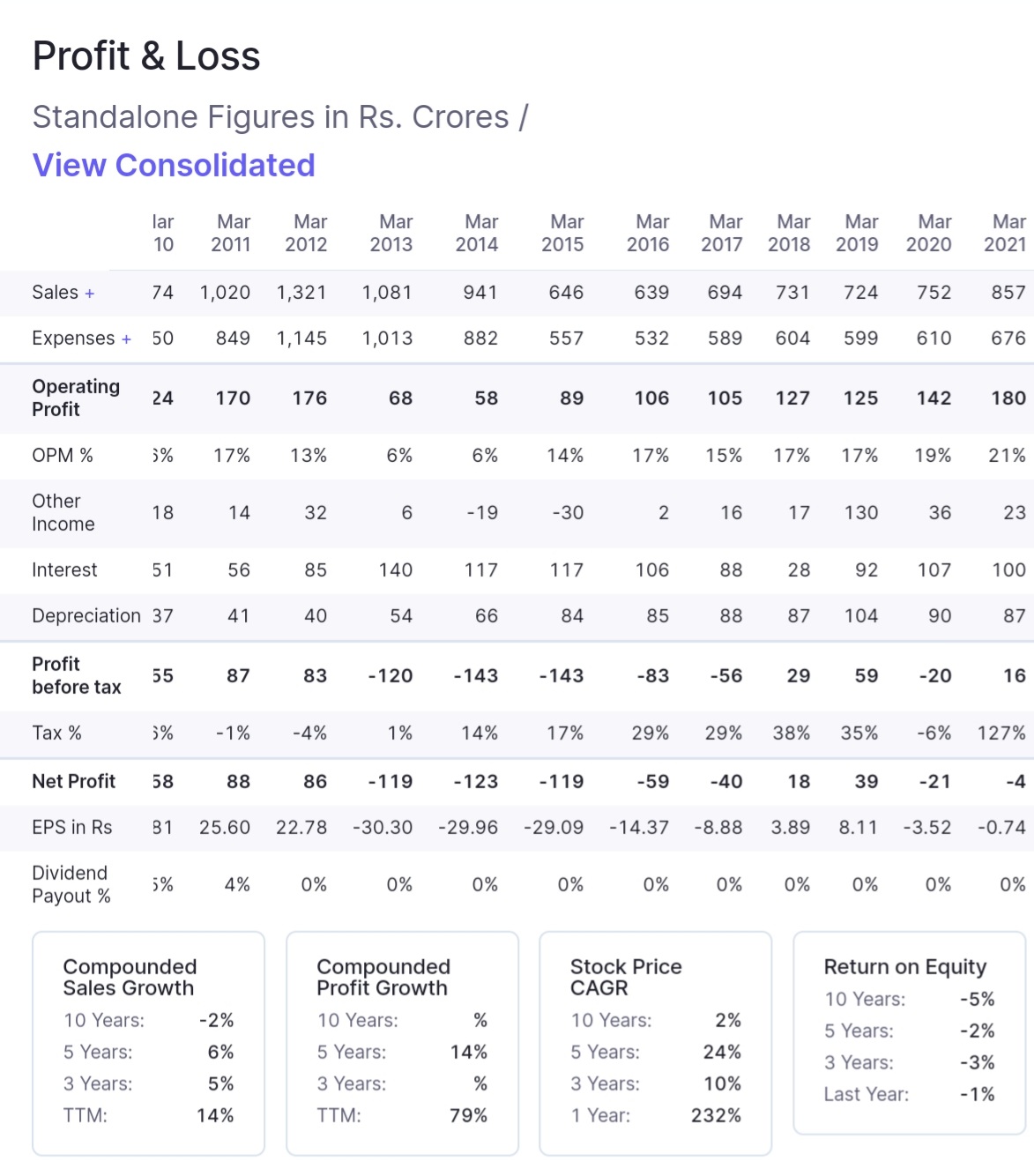

Over the last six years, PI Industries has grown its revenue at 17% CAGR, from Rs.2,096 crore in FY16 to Rs.4,577 crore in FY21 – an absolute increase of Rs.2,481 crore (all figures Consolidated).

To meet expectations of 24% revenue growth over say the next 5 years, the company would need to clock revenues of Rs.13,418 crore by FY26E – an absolute increase of Rs.8,841 crore from the current level.

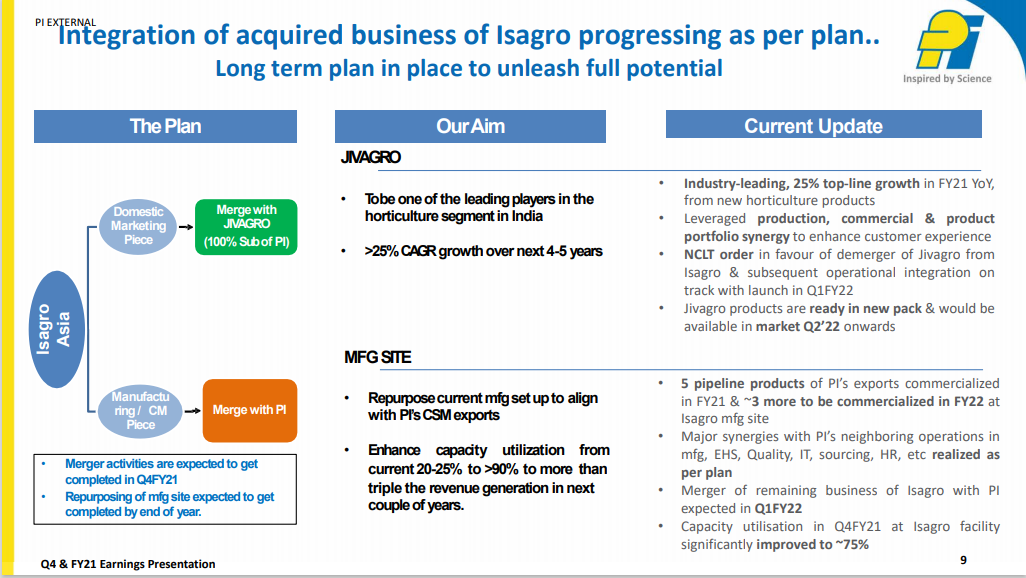

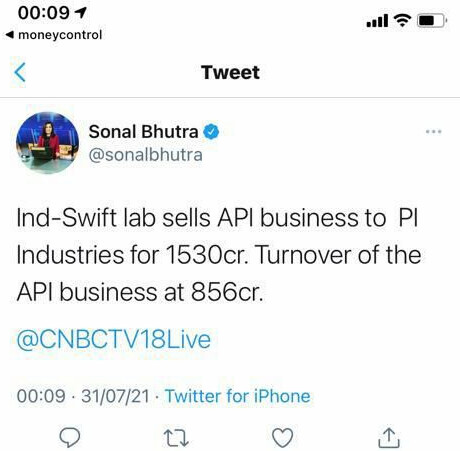

In other words, PI needs to add almost two more PI Industries to itself in 5 years. Organically, this may simply not be possible physically even if PI has the money. The export CSM business, which constitutes 3/4th of the turnover is a capex intensive business. Acquiring land, building capacities and scaling them up takes time. That is why the inorganic strategy comes in. Inorganic brings down the asset turnover and return ratios initially but helps to buy time. PI purchased Isagro at around 1X the sales and Ind Swift assets at more than 1.5X.

From the table below, we can see that the organic route costs much less with asset turns of around 2X.

I expect PI will manage an asset turnover of 2X going ahead on its 15% organic growth. Further I assume Ind Swift assets would contribute around Rs.250 crore this year (one quarter), Rs.1,000 crore in FY23 and grow 20% thereafter. This is how all of this looks:

From these two, PI can reach a revenue of Rs.11,000 approx. by FY26E. This still leaves around Rs.2,500 crore gap to be filled (Rs.13,418 minus Rs.10,934 crore) in order to achieve 24% CAGR from the current level. This gap will be bridged through the inorganic route.

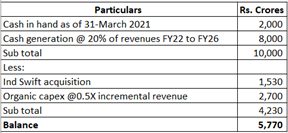

Let us look at the cash position now. As of 31-Mar-2021, PI had cash balance of Rs.2,000 crore. Annual cash generation last two years has been around Rs.700 crore. Based on past trends, I assume PI will manage a CFO 20% of revenue. Of this, part of the cash would be spent on organic capex (which gives asset turnover 2X). And Rs.1,530 crore is going into Ind Swift acquisition.

Putting all of this together, we get:

Essentially, company will have around Rs.5,500-6,000 crore cash left which can be used to make acquisitions. This should generate revenue of around Rs.2,500 crore, thus meeting the expectations of 24% growth over the next five years. Therefore, a minimum 24-25% growth seems easily achievable without any further equity dilution or taking on external debt. I have ignored dividend and interest payments which are relatively small and don’t make a difference. It needs to find good acquisition candidates though, that is the main challenge.

(Disc.: Invested)