which are the key raw materials of PI Industries

Thanks @Worldlywiseinvestors and @Mahesh for your earlier replies and insights.

I quickly allocated a significant portion of my portfolio towards PII in the last couple of months In hindsight, it appears to be a wise decision. Since I buy any company with a very long term view (virtual holding period is forever), I would like continue to continue buying PII for some more time given the monopolistic nature of their CSM business, prudent capital allocation history and seemingly clean management.

Even after the recent run-up and nose bleed valuation, I am still finding value in this company - any thoughts, please?

Disc: Invested and my view is biased.

4 Likes

PI Ind Business Performance.pdf (3.5 MB)

3 Likes

Got logged out of the call a bit early but here are my notes:

|o|Strong growth in domestic demand partly due to bunching up of orders from last quarter

|o|Isagro business has lower gross margins (this quarter topline: 99 cr.; exports: 30 cr; domestic: 69 cr.)|

|o|Domestic growth driven by Nominee gold, Elite (for corn), Osheen (insecticide brand for cotton and rice), Cosko (new product launched 3-4 years ago; used for rice and sugarcane) and Isagro integration|

|o|Domestic industry growth of 10-15%, PI domestic growth will be 1.5x of market growth (20-22%) [excluding Isagro]|

|o|In FY20, 4 products were commercialized|

|o|4-5 custom synthesis products will be commercialized this year|

|o|New molecule development and scale-up requires 2-2.5 years|

|o|550-600 cr. CAPEX/year will be invested in the next couple of years|

|o|QIP proceeds of 2000 cr. will be utilized over the next 5-6 quarters|

|o|Aggressively looking to diversify into pharma intermediate space; creating two wholly owned subsidiaries|

|o|Domestic price realizations better than last year but worse than expectations|

|o|Less than 10% imports from China (down from 30-40% dependence 4 years ago)|

|o|Supplied COVID-19 intermediary to a Japanese company and some leading players in India|

|o|Looking to de-risk Indian operations by looking at International opportunities|

|o|Broad revenue composition going forward: 70 (international), 30 (domestic)|

|o|Export growth of 20% going forward|

12 Likes

7 Likes

News share

2 Likes

news on expected lines, incorporation of two new subsidiaries.

Very interesting description of company objectives ( the scope is vast !)

disclosure: Invested, looking to add more on dips for core portfolio

3 Likes

ICICI Direct has initiated coverage on PI Industries

3 Likes

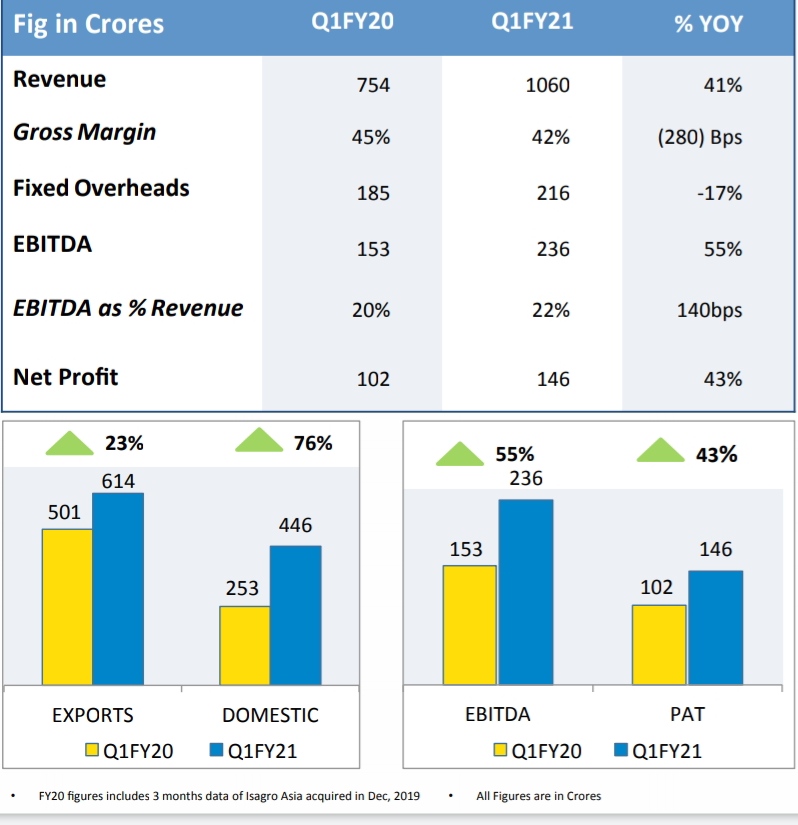

Pi Industries Q2FY21

Strong Performance continues

Gross margins came down YOY by 200bps(Plausibly due to Isagro Acquisiton and higher domestic business in the mix)

Topline grew by nearly 28%

Operating margins expanded from 21% to 24% on the back of operating leverage as Capacities have been capitalized and utilization levels have started picking up

Very well positioned to take the benefit of tailwinds, let’s see how the diversification into Pharma crams plays out. There is a period of gestation that is involved in that business, let’s see if acquisition can shortern the period.

Q2FY21 PI.pdf (969.4 KB)

Disclosure and my views: Pi has to expand the size of opportunity as going forward in next 8-10 quarters, sales will double and profitability will more than double. However, by that time they will reach double-digit market share. Diversifying into other lines is a necessity. Closely watching how it plays out. Invested and biased.

22 Likes

Q2FY21 Business update:

All manufacturing units operations and capacity utilisation back at pre covid level.

All MPP are operational . one MPP under construction to be commissioned next year.

Domestic:

Domestic revenue increased by 35% yoy( modest growth in domestic segment +Isagro brand)

Two new products in Q2(Insecticide and fungicide).

Positive outlook for Rabi crops. High growth expected from wheat herbicide portfolio.

Exports:

Increased by 25%. Demand for key material remains strong.

Global customers continue to remain positive. Expected volume pick up in some products commercialized in the last 1-2 years.

Order book @US$1.5Bn.

Key ratios like net sales to fixed asset, net sales to WC increased. Higher inventory (990 cr vs 691 cr ) in view of expected growth and to mitigate uncertainties due to covid

Actively evaluating few pharma assets for inorganic growth.

10 Likes

P I Industries Q2FY21 Concall

I will be dividing this concall into 3 parts: Business, Risk and Management

Business

-

Both the existing molecules and the recently commercialized molecules have seen a good uptick.

-

More than 10 products in the R&D pipeline in pharma. Commentary of Global Agri Innovators has shown robust strength.

-

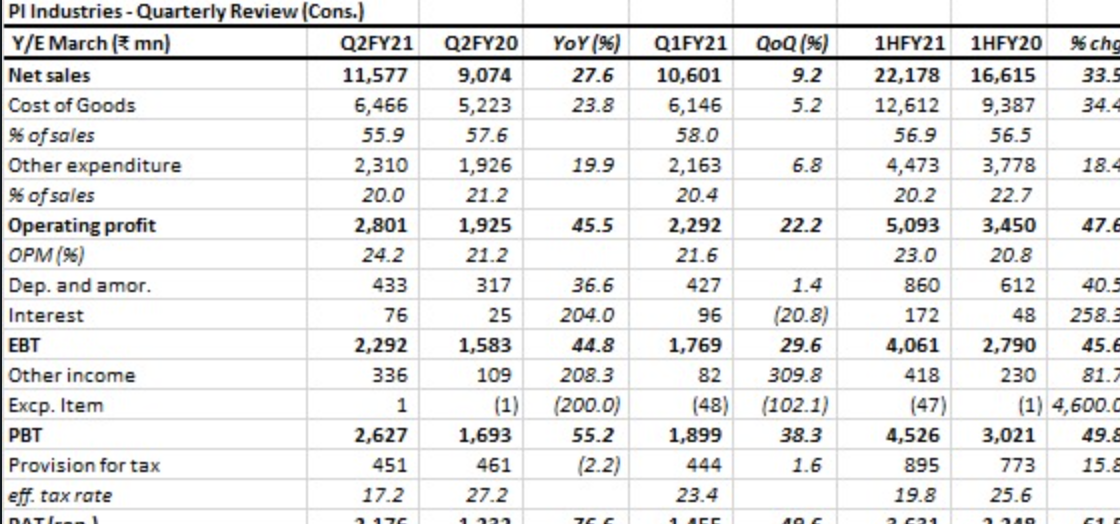

Domestic Business improved by 33% and the export business grew by 25%. Topline grew by 28%.ISAGRO forms 11% of the consolidated topline.

-

Utilization levels are heading back to Pre-covid levels. Going forward, focusing more to improve the asset utilization levels.

-

EBITDA margins expanded by 293 bps due to better product mix and operating leverage. Capex done till H1FY21 is 116 crores, target for the entire year is 600 crores. 100-150 crores of CAPEX will likely spill over to next year due to covid disruptions

-

Order book was maintained at $1.5 billion. Domestic business ex of ISAGRO grew at mid-single

digits, as we are rationalizing the portfolio and a substantial part of the portfolio, comes from Early post-emergence Herbicide, parts of India has experienced early monsoon, this impacted demand (rice). -

ISAGRO continues to enjoy high double-digit growth, has helped us diversify into other pesticides which are used for vegetables, fruits and Plantation(Tea plantation was extremely good this time). It has helped to hedge the Domestic Portfolio.

-

1 Multipurpose plant to be commissioned by next year.

-

Have launched 1 molecule in CSM business and 2 in the Domestic business. Few products to commercialize in the next half in the CSM business and both the molecules launched in domestic business are targeting rice.

Management

- All about acquisition

-

Focusing on utilizing the QIP funds within next 6 Quarters, can expect to do something in next few quarters and not wait for the next 6 quarters.

-

We have opportunities insights where we can easily deploy 3000 crores and sustainably generate returns better than what we are doing today.

-

Key criterion for capex and acquisition: deploy additional capital at a higher ROCE.

-

Acquisition is mainly being done to shorten the process and sustainably create another growth engine for next few decades like what we have done with CSM business.

-

Actively looking for Pharma assets and have engaged a leading consultant to help us evaluate synergies and potential areas of business.

-

Given the pipeline we have, few more plants are in the pipeline. Not expecting this speed of growth to accelerate, guiding for 20%+ growth in next 6-8 quarters.

-

In next 3-5 years, we see ourselves achieving the next level of scale and to emerge as an innovation-led organisation with diversified businesses.

RISK

-

MEIS eligibility has been capped by the government at 2 crores(last year at 15-18crores quarterly). Government has announced an alternative plan.

-

Sluggish mid digits growth in the domestic agri ex of ISAGRO.

-

Acquisition-related risk is there as in the past many acquisitions have failed.

My view: Last year they acquired ISAGRO for 350 crores, 300 crore topline and 20% utilization with single-digit margins, this year margins have improved and the topline has increased to nearly 450 odd crores (Multiple of 3-3.5 times EV/EBITDA) .

Given the past track record of execution and capital allocation, can the management successfully diversify into Pharma and create another engine of growth successfully? Such is the nature of high-quality managements is that they always bring an element of optionality which can help them to keep expanding their size of the opportunity.

Disclosure: Invested, this is not a recommendation to buy or sell.

32 Likes

PI Industries added to MSCI india Index.

4 Likes

I have only recently started tracking this company and I wanted to ask as to why it’s ROE has been continuously falling from 26.8 to 17 (source annual report) ?

2 Likes

Any updates on this, I was following the thread bottom up and couldn’t find any updates for this .

1 Like

So many investors following this company and yet none have been able to answer my Nov 15 query. Here’s a link to this :

5 Likes

Check the recent acquisition which has just started generating (last 2 quarters), adjust the QIP funds sitting on the b/s+plants commercialized cannot run at 100% utilization from day 1. Typically takes 18months+ in PI’s case depending upon the cycle they are in.

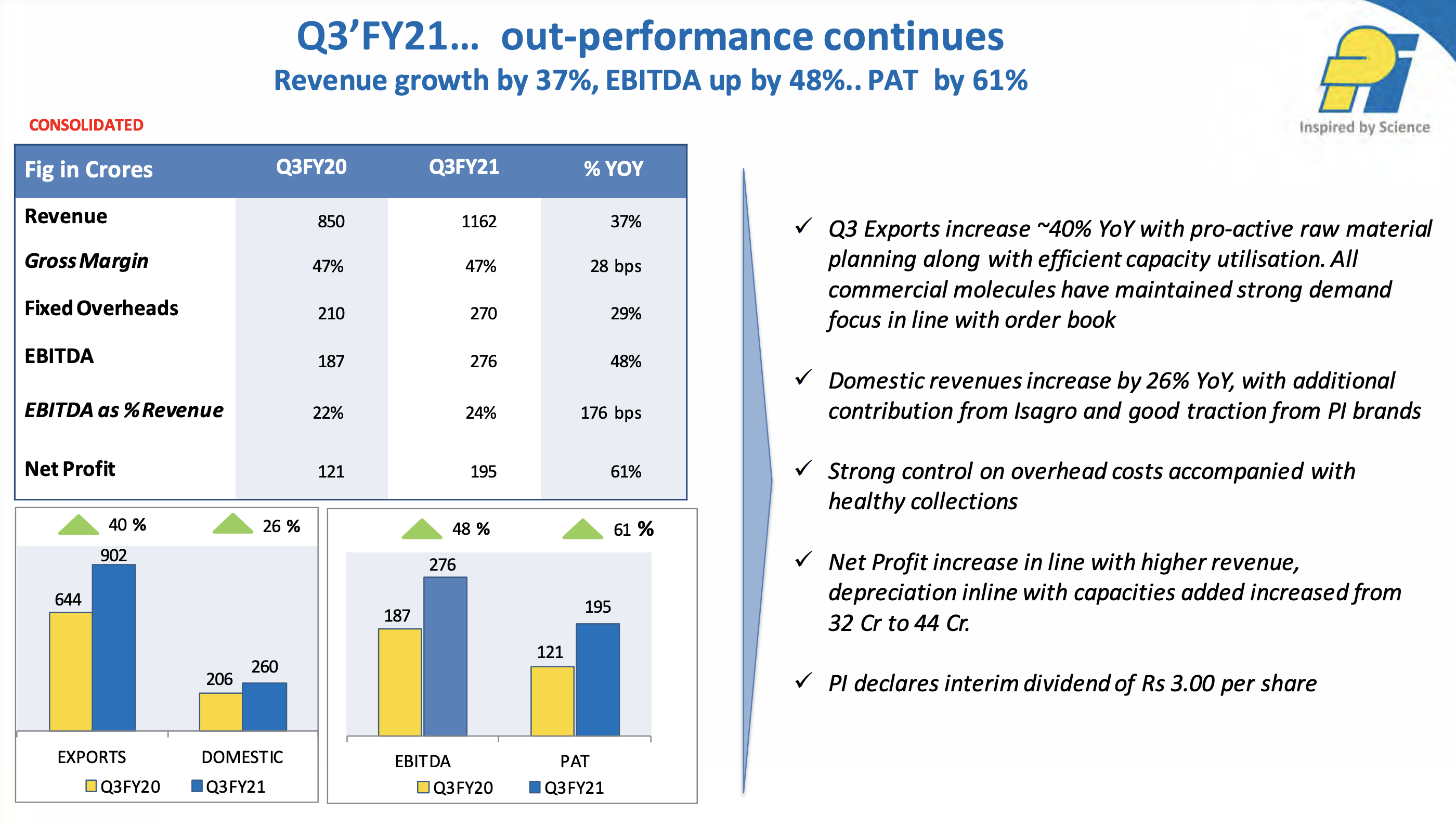

The stellar business performance continues:

11 Likes

Q3F21 Result Concall Notes

About business

-

Exports have increased 40% YOY with pro-active raw material planning , had effective capital utilization and inventory management.

-

Companies domestic revenue increased by 26% YOY .

-

Company have strong control over their overhead costs.

-

The companies manufacturing facilities are building back to pre-covid levels.

-

Despite Covid disruption company managed to deliver increment in net working capital to sales.

-

Company have expanded a lot in specialty chemicals and have taken many initiative to max out the synergies.

-

Many new propitiatory products are in pipeline of the company.

-

Company is focused and keen to hire like minded people to grow more.

-

Capex done in past 9 months was around 320 cr.

-

Company sticks to the target benchmark they have set.

-

On M&A side company is evaluating new options. In last 2 quarters many deal were rejected.

-

Company have multipurpose plants for which the teams are planning for more better capital utilization.

-

After 4 molecules commissioned, Within this financial year more 5 to 6 molecules are planned to get commissioned.

Research

-

R&D pipe line have a sizable composition of non-agro products as well.

-

The company have covered 100+ patients ,which along with technology scale up will become a great deal.

-

More talents are hired and foreign collaboration is also done to get highest growth.

-

Company is trying to cover all aspects to reduce risk.

-

Out of QIP money is not segerated for pharma or non pharma but it will be based on the deals and technological opportunity.

-

Company to cater large markets geography will keep on moving for further spread.

Technology and Mergers

-

Company have taken many initiatives apart for plant expansion to improve efficiency like technology support.

-

New plants might come up in Q4 and Q2 or 3 of next year.

-

Not major information is lead out by company related to plants as they might acquire someone rather then setting up the plant.

-

No big challenge for container need is been seen in Exports part of business.

-

Isagro gave 20% of the domestic growth.

For pharma

-

The strategic direction is to start with API space and develop out technology platform. And get into CDMO like agro business.

-

The company looks to differentiate itself from the technology point of view and get into less competitive areas at first.

Products

-

In synthesis pipe called as r&d pipeline they are at 40 -45 products at different stages.

-

In commercial 24 to 25 products which gives out the revenue.

-

The relationship with The customer have deeper due to technological package hence company delivered value.

-

The utilisation of the 2 plants initiated in FY20

1st plant in 70 to 80 % level.

2nd plant is working under below 50 % as of now. -

Given current plan of company they are confident to continue in next financial year as well.

-

Farm law dosent affect the company much.

Source: https://twitter.com/tycoonmindset05/status/1356904741750493186

14 Likes

The most interesting aspect that they have worked on is introducing analytics and using Technology to improve the efficiency of the plant. With the same MPP(Multi-Product Plant) they have improved the output/throughput by 20%. The output they were getting at 85-90% utilization can now be achieved at 65-70% utilization. Thereby, improving the capital efficiency and effectively ROCE and lesser capex (2.5x asset turns are the revised norm vs 1.8x to 2x earlier) going ahead.

Disclosure: invested and biased

15 Likes

PI Industries is in active talks with Ind Swift Labs for promoter stake buyout.

Jefferies is said to be the advisor to this transaction. ET NOW queries sent to PI Ind & Ind Swift Labs went unanswered.

7 Likes

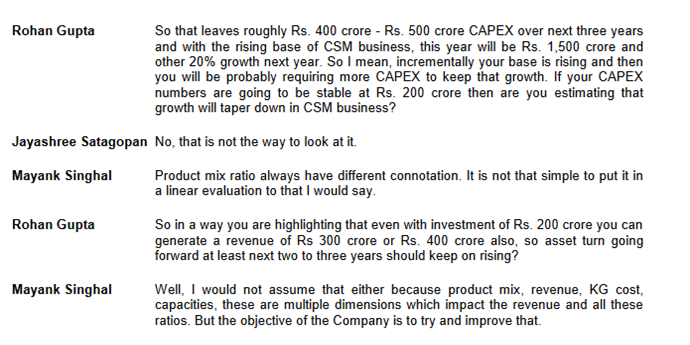

I was looking through the financials of PI and notice that there is barely any cash flow generation in the core business, pretty much any operating cash flow is consumed in capex and finance costs, which seems a continuous and recurring feature essential to growth with no sign of operating leverage, cash flow or capacity wise.

Going through investor calls from the past, the company doesn’t have a v consistent answer as to why its capex cycle always scales proportionately to growth, or when it would scale to the point of generating true free cash flow. They also never give any clear guidance on how they plan for capex, beyond growing the guidance each year. The stated reason for this is they have multi product plants with different products for different clients, and as such the capacity utilization across the product mix is not strictly comparable, and that plants can be single product or multi product as required. There are also various other reasons for capex that come up, such as for backward integration, technology upgradation, debottlenecking etc. While this may make sense, its also conveniently vague on how capex outlays are laid out.

1

They make the same case for utilization, that product mix makes having a common standard for utilization difficult, yet guide in FY19 that many assets are at 90%+ capacity utilization, while the recent QIP document states otherwise

2

3

At different points, they guide that capex is planned as per the existing order book, and at another that capex is planned over and above the order book (for which capacity always exists), to account for future order flow and / or one off opportunities.

4

5

On the plant asset itself, they guide a plant may have 8-10 years of life, and a peak turns of 1.5x times investment (they clarify this is not total capex, but only the actual plant assets) building up over a 4-5 year period from commissioning. There also seems to be significant upgradation and maintenance capex, besides for debottlenecking the existing plants and for ancillary parts to these plants, so together this doesn’t look terribly efficient.

6

7

My interpretation after this is that the multi product nature of the business would make the plants rather difficult and complicated to run, which limits meaningful ability to create operating leverage through scale and specialisation. They also seem to have a product pipeline that keeps growing by 4-5 molecules a year, and at least some of these keep requiring new facilities, while the others add to the operating complexity of existing plants, requiring upgradations, debottlenecking and more tech. Besides this, they also set up one off capacities in niche molecules not based off the order book for more experimental growth. This all adds up to v large cash consumption that scales with business growth and I imagine gets more complex as the base grows. To add to this, they are now entering M&A actively and also investing into the plants they’re acquiring. The silver lining is that management has raised 2000 cr of equity via QIP rather than leverage excessively, and they are looking for pharma acquisitions which hopefully will improve cash flow substantially over the core business. Given that the capex is so recurring and consistent, it must be noted that when added to the income statement, it completely wipes out all profitability and margins. I would expect to see a few things here going ahead: earning compression as depreciation piles up, leverage build up after the QIP funds are used up in 1-1.5 years from acquisitions and capex, with further compression of earnings through increased interest cost. The positive could be a good acquisition that helps improve the cash flow profile and maybe divestment of some of the more onerous assets once their order books are done with. At current valuations, find PI Industries too richly rewarded, for earnings that I don’t feel accurately reflect the cost base of the business. Feedback from others more knowledgeable on the segment / company welcome.

Disc: not invested.

16 Likes