sir can you please tell the source from which you got the addressable market size for CSM segment i.e.$5 billion because i have read con-call ,annual report & investor presentation but i am not getting CSM segment addressable market size for PI industries

Government has proposed ban on 27 pesticides, with 3 products manufactured by PI (Pendimethalin, Dichlorvos, Phorate). The % of revenue derived from the 3 products are not mentioned in the annual reports. Does anyone have insights on the 3 products mentioned?

This is a draft proposal and hasn’t been implemented yet, it is likely to get strong opposition from the industry.

Q4 was impacted due to covid lockdown. Domestic segment degrowth of -12%, export grew by 12 % despite unavailability of one multiproduct. For FY20 revenue growth of 19% with improvement in margins.

Both domestic and export supplies have picked from early April.

Isagro Asia 10% growth.

Net debt of 214cr, capex of 635 cr in fy20. Asset turn and ROIC low due to year end heavy capitalization.

Capacity : 2 new MPPs to get full scale operations in FY21. commenced construction of 2 new MPPs( delays due non availability of labour, material)

Launched 3 new products. >70 new enquiries (20% in non agrichem area)

Initiated commercial scale business with 3 new customers

Order book >$1.5 billion.

Farm application services ; piloting new business model :spray machines

Integration of isagro Asia to be completed by Fy21.

ENTRY into pharma value chain:developed and scaled up intermediate for a promising covid 19 drug.

Tie up with large pharma companies in Japan and India :supplies to start from Q1

Domestic agri : normal monsoon expected. April/May data shows steep growth in agri input sales

CSM export: global customers giving positive views,no change in demand forecast

Co has 3 categories of business:

Custom synthesis manufacturing (exports)

Domestic business

Pharma business+other chemicals (very small right now)

We’ll be dividing this into 3 parts: Business, Risk and Management

Business updates:

Domestic revenue was disrupted due to Covid led disruption. Deferred revenue would be recouped in Q1FY21(100cr)

Higher input costs were mitigated by better product mix.

Sales growth for the full year was at 19% and margins improved by 104 Bps(1.04%)

-30% Growth in operating cash flows, further strengthening the Balance sheet.

Capex for FY20 stood at 635 Cr+345 Cr for the Isagro acquisition. (Recently got commissioned)

FY21 capex to be in the range of 600 crores. (Jambusar and Isagro)

Have seen significant uptick in enquiries in the recent times as companies are looking to de-risk from China.

About Pharma started providing an intermediate for a potential covid drug. If it is approved, expect it to scale.

Likely to see Pharma contributing double digits to the revenue in next 3-4 years. Host of new intermediate opportunities arising due to China de-risk approach.

Filed 22 patents this year and going forward in a position (next 3-4 Years), company is in a position to capitalize on its R&D work done in last decade on pharma.

It takes 2-3 years to commercialise a molecule in Csm business, and sometimes 4-5 years.

Capex of 600cr, most of it would be for organic growth, evaluating adjacencies in Imaging chemicals, personal care chem, speciality, Pharma or other chemicals for inorganic growth.

Domestic Business, core Roce has gone up due to cost cutting initiatives taken in the last 3-4 years.

Have taken price hikes in the ongoing season on a select few products in the domestic business.

There has been no postponement of orders in the Csm business.

Nature of growth is: work with very few customers, and growth is majorly coming from old and new customers+ new and existing products.

Have launched a new wheat Herbicide, Akira, expecting good response.

Management:

We never invest untill we have visibility on the order book. We do not sit on idle capacities, would invest when order visibility is there.

Have deferred the QIP of 2000 crores due to uncertainty in capital markets.

Would commit large capital in Pharma in next 3-4 years, if we create a differentiated process. (300-500cr)

Focused more on process technologies, this is higher margin and replicable like the CSM business.

Seeing good runway for growth in the next 3-5 years, expect to grow at 20% in FY21.

Looking at inorganic opportunities (acquisitions to fasten up the diversifying process)

Risk

Domestic business like every other pesticides company has Product concentration risks. Top 5-6 molecules are more than 50-60% of sales.

Follow a product life management process, planning to launch 2-3 new products every year in next 3 years to keep the portfolio fresh.

One of the products (Osheen)which had a good response in the last 3-4 years in the domestic market is going generic. Expect more competition in that product.

I was going through this thread from the beginning, the posts, and analysis from @Mahesh are like gold mines. Thanks a lot, @Mahesh for your highlighting this story in 2011, and all your forecasts were correct.

While checking the earning and price movement, the majority of PII’s price increase was backed by growth in earning. However, in the recent past, the PE expansion led to the price increase.

Requesting view from @Mahesh and other experts to throw some light on this scenario. Although PE sustainability depends on market mood, will the company be able to increase its earning to justify the price growth?

Disc: Invested and want to slowly increase allocation.

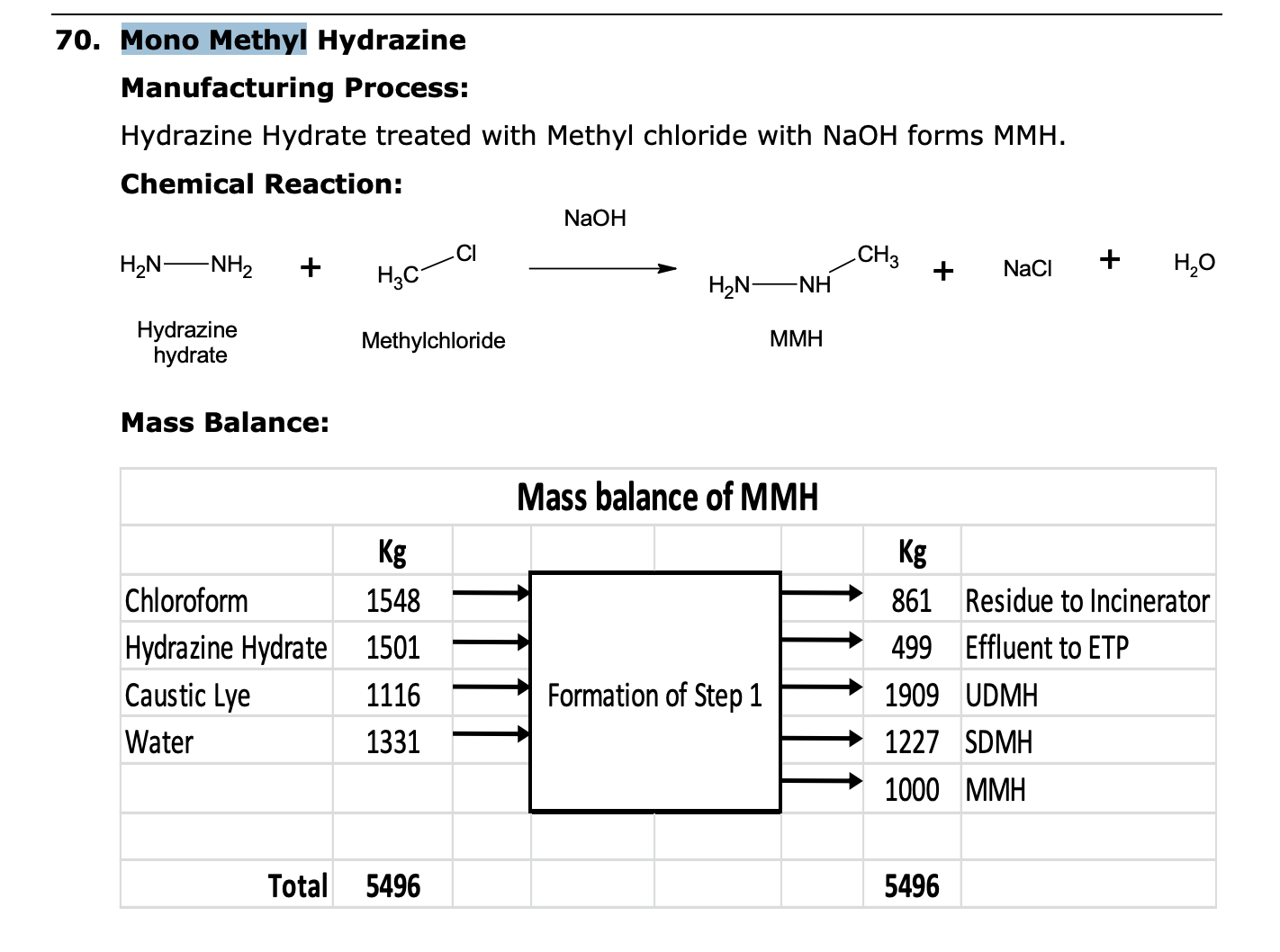

Markets have rerated the company ahead of the earnings growth. As capex of 980 crores in 2020(including acquisition) and Capex of 600 crores in 2021 along with potential of Pi trying to convert into a pharma Cdmo (which increases the size of opportunity by 8x,they might acquire) has rerated the stock. As benefits of capex are yet to be seen in numbers coupled with an order book of 11,000+ crores. Very few stocks in today’s environment provide such growth visibility. Moreover, recently the company has completed the absorption of Mono Methyl Hydrazine which is a technology used to make electronic chemicals, chemicals for rocket propellants, pharma intermediates and agri etc.

Thanks and very useful information. I did not find these in the AR or recent con-calls (probably I missed). Also noticed that the company took a small debt and hence the debt/equity is more than zero after many years.

Is the QIP planned for further fuelling the Capex in pharma intermediates and synthetic chemicals?

Yes, Qip is planned for further organic expansion (csm business) and expansion activities in pharma intermediates and other spechems. There might be an inorganic acquisition as if you just read the concalls since 2015. We’ve been hearing of the same, seems like this time it might be happening given the managements rationale of tying up equity in anew vertical rather than debt. Moreover, an overpriced stock is a very powerful thing in the hand of a capable management.

Significant PE expansion is the direct result of enhanced trust amongst investor community that company will deliver and chance of faltering are low. With this trust if you have an exceptional management quality like PI then such rich valuation is bound to happen because majority of rational investors would like to have the company in their portfolio and will be looking at first opportunity of entry which will limit downsides considerably. It is being observed that such stocks usually go through only time correction and not significant price correction.

Speaking of PI, management has delivered exceptionally well in past and have formulated a derisked sustainable business model which is a rarity in listed mid-cap space. Management has been proactive and have exhibited high corporate governance standards consistently over last more than a decade. On the scale where PI has reached, you get hardly few companies which still has high double digits growth visibility.

However as a rational investor it is always better to build a portfolio and strategize allocation by giving weightage to all aspects including valuation.

PI in my exp has been a steady compounder and still is for mid term ( we take pride in finding THE new compounders, while we may already have some in our portfolio - I myself has been of guilty)

PI capital allocation and growth strategy and execution history has been very strong and demonstrated and thus rerating which is accelerated by demand supply mismatch currently for growth visibility stocks with quality.

Next growth triggers IMO

pharma CSM giving access to new vertical and growth potential, Inorganic route - foundation laid out with QIP & MMH

Order book visibility and further margins expansion ( once capex normalizes)

sector tailwinds Continued china issues with global mkt - mgmt indicated higher enquiries

Corona impact - strong getting stronger

While newsflow, mkt price and volume action has got stock already rerated and may move sideways for sometime , delivery on multiple fronts will keep things exciting and watch mode and we have a steady compounder in our hands if one is content with 20%+ CAGR over med term - but sure many at VP can and would like to beat that

The table shows that between Apr-10 to Apr-20, in 10 yrs period, the share price went up almost 30 times, supported by growth in earnings as well as PE.

Can we expect the same rate to continue i.e. Share price to increase by another 30 times in next 10 years?( considering present PE of around 60)

OR

Are there companies, who are today in position in which PI was 10 years earlier and such companies have potential to grow like PI industries in next 10 years?

Take a look at Astec Life Science. I consider it at a stage where PI was around 2010 but it has much more renowned group like Godrej group backing it so all things equal, it can grow faster…

Added comparison (although not directly comparable due to time value of money)

Figures in Cr

PI Ind

Astec Life Science

Year ending 31 Mar 2010

Year ending 31 Mar 2020

P&L

Sales

543

523

Operating Profit

87

81

PBT

57

61

PAT

42

48

Balance Sheet

Share Capital

28

20

Total Borrowings

150

99

Fixed Assets

200

194

Source - Screener

In recent AGM as well as conference call, Astec leadership openly mentioned they aspire to become like next PI Industries… although it is very long journey