Found a somewhat compelling idea in the largecap space - Hindustan Zinc. Everybody knows the technicals and can look up the chart - its hit a fresh 52w high after 6 months and trading at 2 yr highs but considerably below (~30% lower) than ATHs. Rest of the post is on fundamentals.

Brief

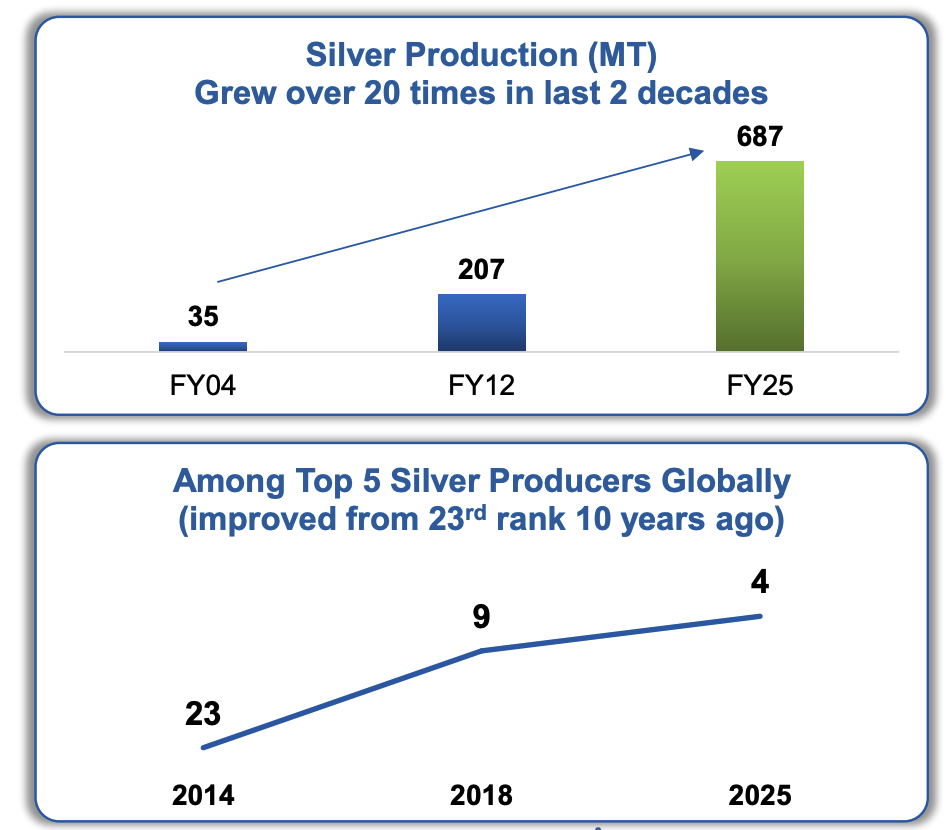

HZL produces predominantly zinc, lead and silver. It is one of the lowest cost producers in the world and has also is 4th largest in Silver and its impressive how the company has vaulted from 23rd to 4th position in a span of ~10 yrs in silver.

Silver Macro

Before you do anything if you haven’t read, take an hour off and read this. Silver has been added as critical mineral last month by US. The context for the same is explained in great detail in the post.

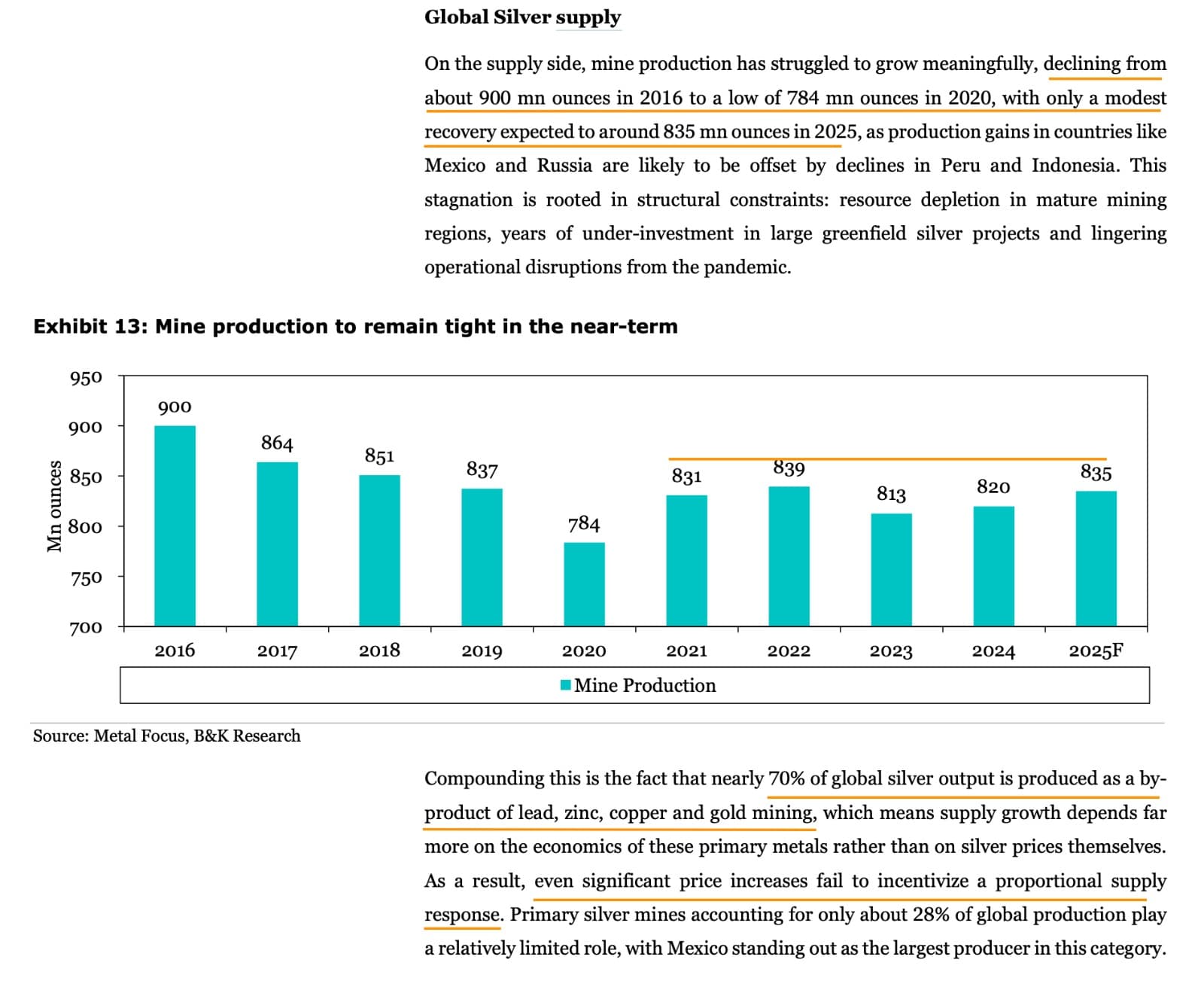

The reason I got interested in HZL is because of the way Silver has been behaving in the last 3 months. These are taken from B&K report on HZL (phenomenal report)

Silver has been in deficit last 5 years and being a monetary as well as industrial metal, the demand is going to remain strong going forward with QE + AI, Drones, Humanoid Robots, Data Centers, 5G all competing for Silver.

But the production hasn’t kept up - mainly because Silver is mostly a hitchhiker mined along-with other minerals like Zinc, copper etc. There’s no big production bumps expected in the near future.

There are some calls for even triple digit prices on silver. But I think better to take them with a pinch of salt. They do make some pertinent points about silver:gold ratio though and how it used to be 6%+ even not so long ago but is today ~1.5%. Maybe it is silver’s time to get re-rated. But our assumption here in this post is very, very conservative at just ~$50. Anything else is bonus.

Thesis

Its a decent way to play Silver through Indian equities. The Zinc-Lead part of business can hold their own as prices are firm there as well. As of recent quarter it derives 40%+ of its EBITDA from Silver and silver prices have gone parabolic.

People playing commodities have been excited about Silver since Oct so this is nothing new. HZL still struggled to break past the 520 barrier which it did for the first time yesterday.

It is also shielded from daily volatility one has to endure while playing Silver as a commodity because as long as the avg realised prices for the quarter is higher than in the past, the company would make higher profits and that is good enough, given the low starting valuations

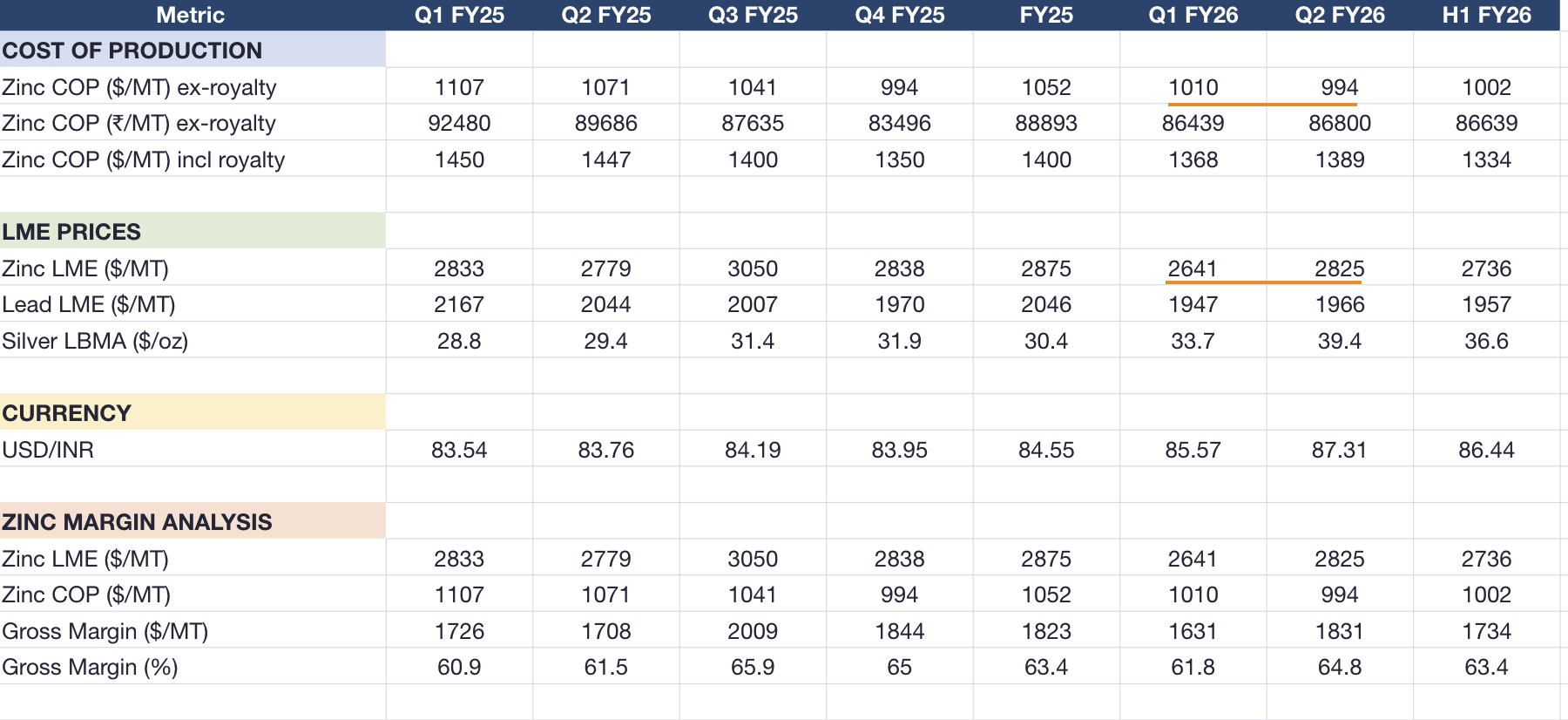

The company has a silver production capacity of ~700MTPA. In H1 they have produced 293MT and in guidance they have 680MT so H2 should have ~400MT production. Of this 130MT is hedged at $37/oz while silver price today is trading $60+/oz. So the rest of the capacity of 270 MT will be sold at spot as per management - this is where every incr. $ goes directly to bottomline.

Levers

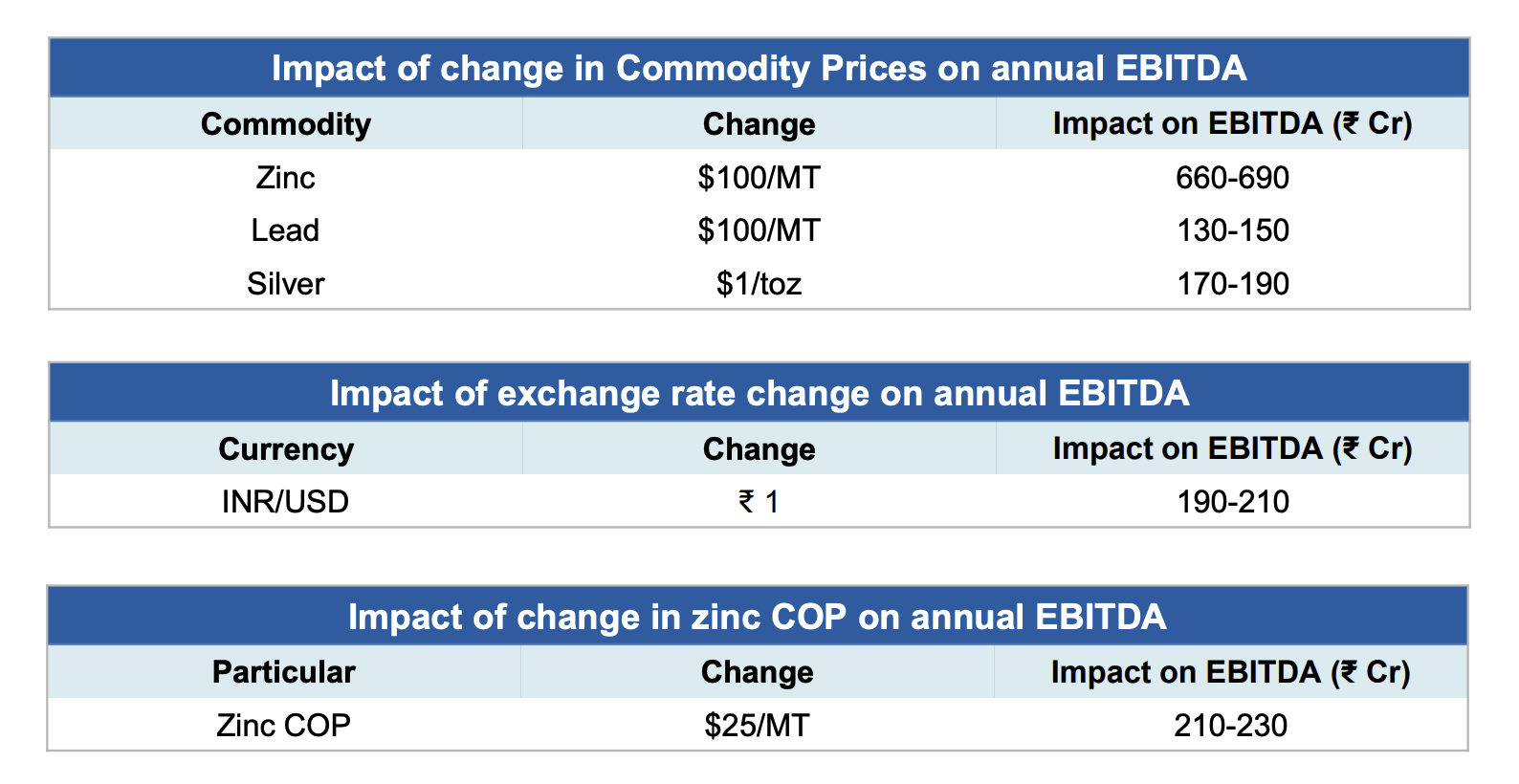

Several levers in this are currently playing out. Silver $1/oz adds ~180 Cr to EBITDA.

In Q2 silver realised price was $39.4 and that already made silver contribution to EBITDA go up to 41%. Silver volumes were lower than production capacity as well in H1 at 293 MT vs 350-400 MT possible in H2. We might be looking at $45/oz avg in H2 and $50+ avg next yr (spot prices are already 60+ but being very conservative here) which can add ~2000 Cr to EBITDA.

Also exchange rate has seen a bump from 87-88 levels to 89-90+ levels this qtr. That should add ~400 Cr to EBITDA.

Zinc prices in Q2 were ~$2800/MT. There’s a bump up by ~$300 in spot prices. Zinc ~99kt seems to be hedged out of ~800kt, so we can assume a $200 bump in realisations which should add 1300 Cr to EBITDA.

The other thing is Zinc COP - the company has gradually reduced cost of production of zinc which is now down to $994 and guidance is go as low as $950 by Q4. This adds another 300-400 Cr to EBITDA from efficiency improvements.

So overall, even with these conservative assumptions (mainly on silver), we can see a ~4000 Cr EBITDA gain in next 12 months (~22% growth). If we assume another $10 gain in silver (bull case) - then we are talking another 1800 Cr (33% growth).

Valuation

Given the considerable growth levers available, the company is still priced in cheap at 20 P/E when global peers are all priced ~30 P/E. Fresnillo which is the largest is priced at 62x. Southern copper corp (silver byproduct) trades at 32 p/e. Pan american silver corp at 29x. All are trading at ATHs, unlike HZL which has not participated in the silver run at all until this week. HZL is the world’s 4th largest silver producer and their mine is the 4th largest producing mine (though India ranks 12th - thats how big HZL is).

Risks

Promoter has played tricks here in the past. Mainly dividend stripping - even borrowing to pay dividend. But maybe ~25% of the dividend paid came from debt and rest from accruals. This risk might be contained in the near future because there’s a lot of capex commitment that requires maybt 20-30k Cr to be invested over the next few years.

Promoter might still raise money by selling stake increasing float. This again has happened in the past. But the company is very underowned and is cheap - I see a considerable shift globally towards precious metals that its possible that these start trading higher than historic valuations because of geopolitics and macroeconomics.

Since we aren’t overpaying, commodity cycle risk here is low - might be different if buying 30-40% higher.

Disc: Invested