I don’t want to clutter @phreakv6’s excellent thread, but given the extraordinary geopolitical climate we’re living through, I felt compelled to share a few thoughts and clear my own head which readers might find useful. With Bharani’s kind permission, here’s my couple of cents—

Over the past few months, I’ve been exploring several books to deepen my understanding of the historical forces and policy choices that have shaped America’s current debt predicament. The U.S. now carries a debt-to-GDP ratio of roughly 130%—or about $38 trillion—an unprecedented level for a global reserve currency issuer in peacetime.

How did the U.S. reach this point, and why might it be nearly impossible to escape this fiscal trap without significant economic and geopolitical consequences.

The current U.S. national debt stands at around $38 trillion, or roughly 130% of GDP. It’s important to remember that the debt-to-GDP ratio matters far more than the nominal dollar figure—it’s the best measure of a nation’s fiscal sustainability.

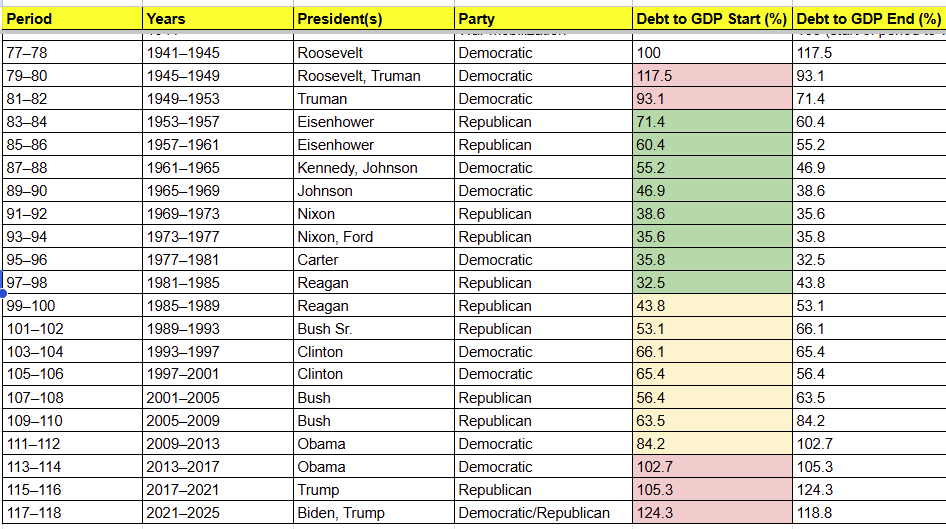

Interestingly, this isn’t the first time the U.S. has faced such elevated debt levels. Right after World War II, in 1945, when President Roosevelt took office, the nation’s debt-to-GDP ratio was around 118%. Yet, over the following decades, it steadily declined—falling to nearly 33% by 1981.

That remarkable reduction was not accidental. It reflected an era when fiscal discipline was a bipartisan priority, and maintaining manageable debt levels was considered both economically prudent and morally essential.

The chart below illustrates this long-term descent—spanning more than four decades—showing how deliberate policy choices and responsible governance shaped America’s postwar financial recovery.

In hindsight, the 9/11 attacks may stand as one of the most profound economic and geopolitical turning points in modern U.S. history—an event that arguably marked the beginning of America’s long fiscal decline. The country’s debt-to-GDP ratio, well-contained at around 56% before 2001, began a steady ascent in the aftermath of 9/11 and the dot-com bust, eventually reaching today’s level of roughly 130%.

Since 2000, neither Congress nor the White House has demonstrated the same fiscal restraint or long-term discipline that guided earlier generations, especially those who led the post–World War II recovery. Tellingly, the United States has not recorded a single balanced federal budget since 2001—a stark contrast to the ethos of responsibility that once defined its economic governance.

Let’s put America’s $38 trillion debt—or roughly 130% of GDP—into perspective, and understand why it has reached a level where a true reversal seems almost impossible.

In the fiscal year 2024–2025, the U.S. federal government collected around $5.2 trillion in revenue, while total expenditures reached nearly $7 trillion—leaving a deficit of about $1.8 trillion. This gap is routinely covered by issuing new debt, effectively printing more money. No sitting president wants to risk slowing the economy through deep spending cuts, since growth is seen as the only viable path out of this trap—though that strategy assumes the rest of the world cooperates, which rarely happens in practice.

Now, consider the interest burden. At an average rate of 3% on $38 trillion of debt, annual interest payments amount to roughly $1.14 trillion—about 22% of federal revenue. A mere 1% increase in rates would push that figure to $1.52 trillion, or nearly 30% of total revenue.

This math alone explains why there is so much political pressure on the Federal Reserve to pivot toward lower rates—something figures like Trump have been vocal about. The higher the rates go, the faster the fiscal situation snowballs.

Typically, government debt levels rise during recessions—when revenues contract and government spending expands to stabilize the economy. However, today’s environment poses a troubling question: if the AI-driven market boom were to unwind or the U.S. were drawn into a major conflict, does Washington still have the fiscal firepower to respond as it once did? Realistically, the answer appears to be no. Yet, the government would likely spend aggressively regardless, simply because the alternative—doing nothing—is even worse.

What’s more concerning is the lack of political will to restore fiscal discipline. Neither Congress nor the White House seems intent on charting a path back toward sustainable debt management. Instead, U.S. foreign policy increasingly reflects efforts to project economic and strategic dominance—sometimes targeting resource-rich nations—as a means of maintaining leverage amid growing fiscal vulnerability.

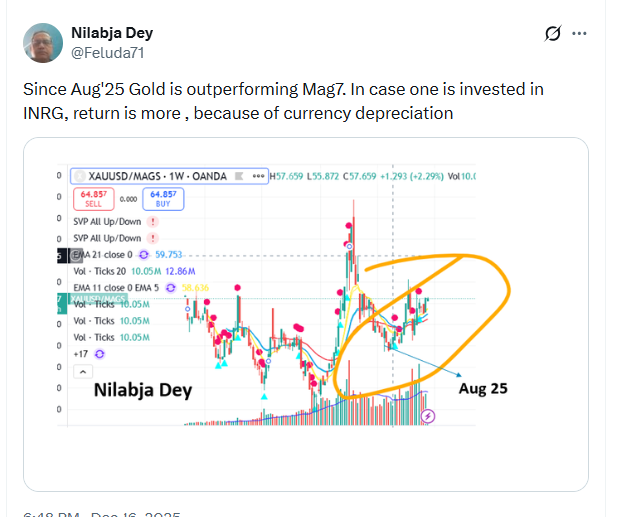

We are possibly living through an era of profound transition—one that occurs perhaps once in a century, if not centuries. The U.S. dollar’s status as the world’s reserve currency faces mounting strain, and within our lifetimes, we may well witness a shift toward alternatives such as gold or stronger, more disciplined national currencies for global trade.

Disc: have been long on gold for last 2+ months…..will average up if it goes higher and can cut my entire position in a single day…..do your own diligence and don’t blindly speculate in gold and silver