This website shows that Carborundum universal is supplieng to Bloom energy. I’m not sure if this is a reliable source or not. Correct me if I’m wrong.

5 Likes

Sai Life PE 62, Market cap/Networth 10, Market cap to cash flow 67, EV/EBIDTA 32, ROCE 14%, Promotor stake 35% and CDMO is a lumpy business, stock is priced to perfection

10 Likes

I feel valuation is not always just the TTM P/E. Doing so ends up in a lot of value traps. The differential insight can only come from looking at capabilities that aren’t captured in the balance sheet as intangibles. That’s what tells us about the longevity and durability of one’s moat and a bulk of the valuation actually comes from these two (how much can the earnings grow AND for how long) than what the company did in the past alone (while it still matters). Its the growth and longevity that are primary drivers of valuation (see how a growing annuity is valued vs a lumpy one-time cash flow for eg.)

Most of the winners for me in the last couple of years have come from this approach and I have bought 50 P/E+ consistently in this period (Wocky, Shaily, Axiscades etc) and have had 2x-4x in few of these even when market did nothing since Sept ‘24. A business like Sai isn’t as lumpy as the other CDMOs. It has no commodity business which can drag while another molecule or two is growing. It is not reliant on one or two molecules. It is 100% innovator business. Doesn’t mean it wont suffer from lumpiness - but at least it will not be as lumpy as the others.

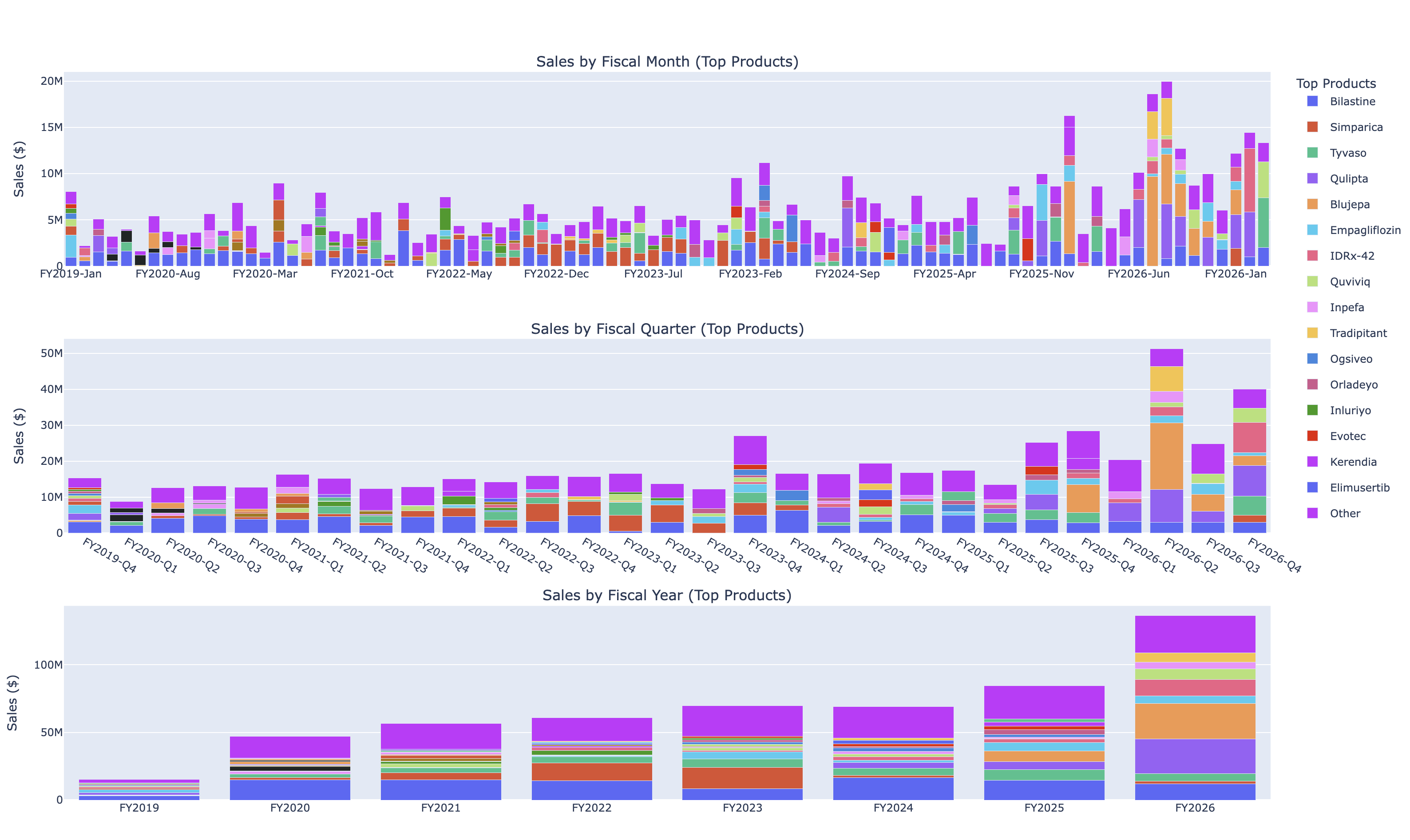

Take this for eg. The biggest molecules for Sai are Qulipta and Blujepa (in the last 2-3 qtrs that is). In Feb exports there is no Blujepa and still IDRx-42 made up for it. In Mar (20 days data only) there is neither Qulipta or Blujepa and yet Tyvaso and Quviviq have made up for it and for this quarter as a whole, none of the molecules are > 20% (Still this is the best quarter almost for Sai already if you remove Tradipitant from Q2 since this was from earlier quarters but shipped later)

Even this doesn’t cover the work they are doing for numerous innovators every month and how complex such of those chemistries are and how capable some of those molecules are in clinical trials. Do check out Sai thread and I have covered in depth some of these.

My pf is filled with high P/E stocks - Aeroflex, TD, Mtar are all 60 p/e or higher. I have seen how markets react in times of crises - capital seeks comfort in businesses that have good earnings visibility and relatively undisrupted cashflows and these bounce back durably after a market-wide correction. I have made mistakes of buying 12 P/E stocks only to see them derate to 8 P/E in such times even though they have strong counter-trend rallies that end up being bull traps.

This is of course not the only way to invest - its a way of protecting one’s capital and one of the important things in the market to know are when to protect capital and when to attempt growing it aggressively. Sometimes even protecting capital yields decent alpha by simply not losing and sometimes gaining. This strategy will not work as well in a roaring bull market and I am aware of it quite well. We are nowhere close to a roaring bull market at present.

88 Likes

Appreciate your detailed reply phreak, its all about your strategy you follow in different market conditions. Problem with high growth and high PE stocks is these may go in price or time correction once growth moderates and stock price comes to mean valuations. Timely exit is also important as any bad news is known at last to retail investor. There are very few business with consistent 20% plus growth.

Congratulations for new ATH, here fight is to limit losses. Conviction is getting tested on daily basis. ![]()

![]()

16 Likes

This small paragraph talks hell lot of experiene and not sure how many understood the power of this. In the recent past, i have taken time out, read more, introspected my past way of investing and used lot of AI to understand better. This paragraph is a good summary of my learnings. But knowing and practicing this is another level. Thanks for re-iterating this for me.

13 Likes