technically, both Gold and Silver have seen the top for this bull run.. just my view as amateur technician

1 Like

My thoughts on specific companies I have been invested in or following and some new ideas and thought-process behind them.

Sai Life Sciences - I have a thread on Sai which delves into the company in some depth, at least on the molecules and capabilities. The latest EC is a clear indication of doubling of capacities in several high value molecules - I have parsed it here. I think the company can double its CDMO revenue even from here in 1.5-2 years time (~65% of revenues) even as CRO (~35% rev) continues to grow near 20%. The margins guided by company are 28-30% but there are enough levers here which is there in one of the earlier posts here (all of which are playing out).

Few observations -

- I think the write-off in Q4 for 35 Cr, FY25 pertains to Tradipitant. Sai was very prudent in taking immediate write-off after FDA did not approve the molecule for gastroperesis in Sep 2024. But the innovator sued FDA post that and took delivery of the molecule (~$7m) in Q2 FY26 (and eventually got FDA approval for motion sickness on Dec 31, 2025) and now Sai made a write-back for 16 Cr in Q3, FY26 (might mean 20 Cr writeback in Q4, FY26). I was quite impressed with the prudence here.

- Sai appears to have not only got Zoetis back but seems to be setting up much larger capacities in high-value intermediate for Simparica as well. To me it looks like Simparica alone could be ~500 Cr contribution to topline from the two intermediates CF3-Ketone and BOC-Ketone at full capacity. Qulipta/Ubrelvy, Blujepa, Simparica, Lorundrostat, Quviviq all have potential to be ~500 Cr+ molecules (first 3 are very high probability). There will be numerous $5-10m molecules (maybe 20+) which will form the base reducing volatility

- Management mention 3 out of 5 in top 5 animal health companies as customers. There is a very interesting Boehringer Ingleheim deworming molecule which seems to be under trials (going by the export quantity which is substantial). This one can be a big revenue driver as well but it isn’t yet clear which one this is since BI Vetmedica is privately held company

- There is a good chance that 2-3 years down the line if CDMO contribution is ~75%, the EBITDA margins can be as high as ~35% and PAT margins ~20% (this is my guess based on what I am seeing, and not management guidance)

Hind Zinc/Silver/Gold - My views here remain same, however my allocation has reduced considerably here as I have found equity ideas to invest in (These were meant to be a cash position). It gave very good returns at a time when rest of the market was bleeding but I think its job is done for now.

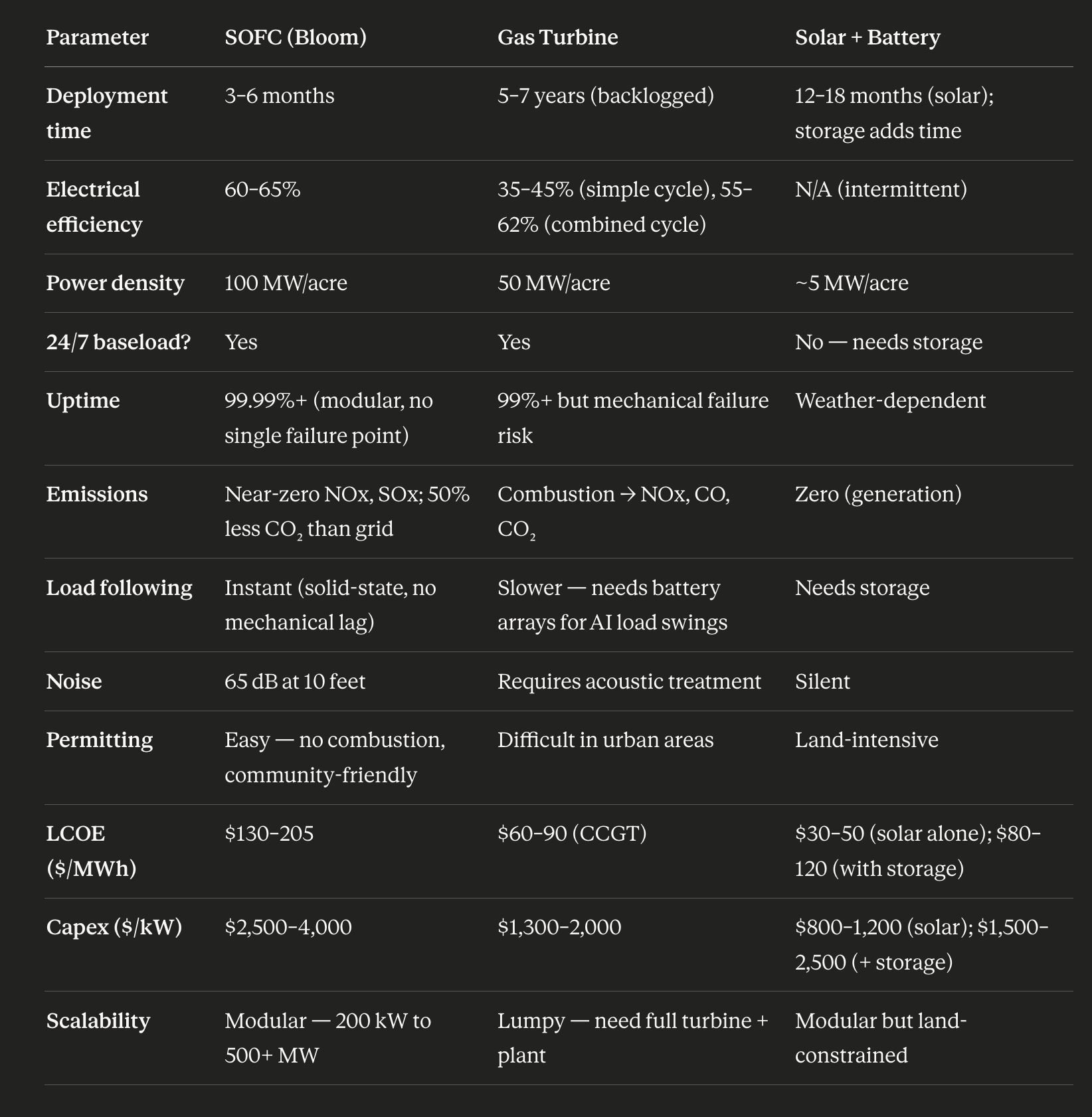

Mtar - Thanks to @Rokrdude for briefing me on the idea and sharing some good videos on bloom energy. I did some deep work as well over the last few days and I have exhaustive amount of data and insights but I don’t know how much I can or should put in here. So will keep it short as a first cut. Mtar is a play on US data center capex. Mtar derives ~60% of its revenue supplying hotboxes, sheet metal enclosures, eletrolysers to Bloom energy. The names of the products sound incredibly dull and low complexity - but it is anything but. Hot box is a very complex, precision engineering marvel which contains fuel cell stacks, fuel reformer, heat exchangers, and gas manifolds. These have to withstand 800-900 deg C temperatures and still maintain 5-10 micron tolerance (very few companies in the world can pull this off - Mtar with its nuclear background is one of the few).

Bloom has been a very long term story in US markets with its forming in the 90s and decades of research and listing in 2018 and actually turning profitable only recently with $1.47b in CY24 and $2.02b in CY25 revenues (founded and led by an Indian - Mr. Sridhar). It is in the cusp of a J-curve of 3 decades of research and hardwork. Bloom has an installed capacity of 1 GW and is projecting $3.2b for CY26 (~50%+ growth) which will be roughly 1GW and is doubling capacity to 2 GW. Proportionately, Mtar as well has announced increases in hot box capacity from 8000 to 12000 units by Mar ‘26 (~40 Cr capex) and further to 20,0000 units by Dec 2026 (another ~60 Cr). If my math is right, 1 GW of SOFC will require 15000 hotboxes from Mtar and Mtar makes ~$5500/hotbox and with value-add that can go up to $7500/hot box (~1000 Cr/GW maybe max).

What is driving the tailwind is US data center BTM strategy (behind-the-meter). Essentially, it is impossible for US utilities to provide power to these data centers in any reasonable timelines (mostly 5-7 years+) so most of these are investing in gas turbines (TD Power provides generators to these) or solar power and of late, also SOFC (Solid oxide fuel cells which bloom makes). SOFC is currently a rounding error (< 1%) in overall capacity with Gas taking 40% and renewables 24%, nuclear 20% and coal 15%. Today only 1% of data centers is self-powered (off-grid). This number will be 27% by 2030. So SOFC can potentially double in growth for Bloom every 2 years (limited only by ability to put up capacities to support growth).

Technically SOFC is far superior in terms of energy density, emissions, ability to follow spikes in load without need for batteries etc. So though overall capex and LCOE here in this table is relatively high - Gas turbines need lot of spend in sound dampening, batteries and water requirement which pushes up costs further.

SOFC might finally be ready to overcome the skepticism and this might have just happened over the last quarter with Brookefield placing a $5b commitment with Bloom.

Mtar also has received 500 Cr orders in nuclear power for Kaiga 5&6 (Nuclear plant in KA, with units 1-4 already generating 880 MW at 220 MW each. Plants 5&6 will use PHWR tech taking overall capacity to 2280 MW (700 MW each). India has plans to put up 10+ such PHWR reactors in fleet mode, so this itself is 10k Cr+ opportunity for Mtar over next 10 yrs, so this 500 Cr is just the beginning here.

Mtar has good capabilities in aerospace & defence as well - having made the propulsion systems for Mangalyaan and Chandrayaan-2 and Agni missile assemblies. They also work with Rafael, Elbit as well as GKN Aerospace and Thales. Currently this division contributes just 72 Cr in revenue but can grow to 400 Crs in 3 years and this too is a fast growing vertical. Mtar also bid for AMCA project alongside Adani (leaving it as a footnote here, to show capability and ambition).

So in short, things are all turning around for Mtar across divisions and its on the cusp of exponential growth (order book at 2394 Cr with 1370 Cr orders coming just in Q3 - incl 500 Cr for kaiga 5&6). It has disappointed in the past but things are changing this time around and it can be verified from multiple publicly available independent sources.

Valuation isn’t cheap at maybe 20x EV/EBITDA FY28 but I don’t think this company is going to trade cheap being one of a kind, with seriously strong moats, growth and tailwind.

Aeroflex Inds - Thanks to @ananth for this idea. This again is similar kind of bet to Mtar, riding on data center tailwind, but this time for Indian DC capex (confirmed order book is for India but they can do the same for US as well). Aeroflex makes flexible hoses, bellows and liquid cooling skid assemblies. The last part is what got me interested. They have capacity of 2000 units scaling to 15,000 units in skid assemblies by Jun 2026. At peak util, liquid cooling alone can contribute 300-350 Cr in revenue (TTM 408 Cr) and they can make 25% margin on it (Capex < 100 Cr which means ROCE is incredible - couple that with tailwind and you get good value creation).

Hoses - ₹650–675 Cr. Liquid Cooling ₹300–350 Cr. Metal Bellows ~₹85 Cr. Hyd-Air Fittings ~₹45 Cr. Miniature Metal Bellows ₹25–30 Cr So peak revenue for overall company can be ~1100 Crs from current capex plans. Its a simple business. They do have a moat since these liquid cooling skids are designed with Vertiv and Aeroflex has an exclusive tie-up with Vertiv to be their only partner in India. The liquid cooling for data centers itself will grow 33% cagr over next 7 years as per industry reports - so this might be a good way to play the tailwind in a relatively simple, easy to understand business. The company hasn’t done much over last 3 years in terms of price performance, so we aren’t overpaying for all the new developments. Other interesting thing is the company otherwise also is very export-heavy (72% of topline with 60% to US alone) and has been hit by tariffs in Q3 - despite that they have 23% margins!

I have certainly missed a lot of details (and this post is already quite long), so will try to make a separate post in Aeroflex thread if I have time. They have had corp gov. issues 10+ yrs ago at the holdco (Sat industries) and it doesn’t make good reading - however, I am willing to look past it, as the business is now run by the son and he comes across well in interviews (subjective thing - suggest you look up recent interviews on youtube and make up your mind)

Kitex - This business and promoter have a chequered history as well but again, am willing to look past it because of few things that are interesting. Will keep it brief - Kitex has put up massive capex in Telangana (in Warangal and Hyderabad) - total capex will be ~3500 Cr in TS. Revenue potential is ~2000 Cr from Warangal and ~2500 Cr in Hyderabad. These are fully backward integrated plants that will generate 25000 jobs in TS. Obviously this is not small for a company of Kitex’s size but it is feasible (on paper) because of ridiculous generosity of Telangana govt. (Which is almost Chima level subsidies). In short

- Kitex is eligible for a 25% to 35% reimbursement on fixed capital

- 8% interest subvention upto 8% for a period of 8 years

- Power subsidy of Rs.2/unit

- SGST 100% refund for 7 years (for sales from Little Star brand in India)

- 5000 Rs. per employee subsidy for training

Couple these investments, subsidies with tariff tailwind and there is potential for good growth here. Kitex predominantly has exports in two HS codes (61112000 and 61113000).

In cotton stuff, Kitex has good market share alongside SP Apparel from India but India itself has just 15% market share and we are now at an advantage to China - so there is potential to grow our overall pie and Kitex and SP can both benefit here.

In synthetic clothes for kids, Kitex has 67% market share from India and India is not even in the top 5 - we could have a much stronger tailwind in this.

Overall, the thesis is simple - large capex, subsidies meets tariff adv tailwind. The risk is reversal in tariffs and Telangana govt’s poor fiscal situation - every single subsidy is where Kitex pays upfront and collects money later - so it can bomb spectacularly and this might be the final thing that buries the company. Interest costs have started hitting from Q3 so we need to see how the company handles it from here. But if it does work out, if at all India does well in garment exports to US in infant wear, it has to be because Kitex does well, so am hopeful. Two things to watch out for 1. There is a merger with promoter entity KCL which will make the related party transaction that have plagued the company go away. 2. Company plans to do a 3000 Cr QIP, presumably post merger. I am unsure how they will do it, considering company has barely any institutional holding at present. If these two go through, then odds of things working out improve a lot.

Apologies for the long post.

Disc: I have positions in Sai from Sept and have some recent buy transactions few weeks back. Mtar, Aeroflex, Kitex are newer and I have positions pretty much around current levels. This is not advice and I am not qualified to advice and am just a novice sharing my thoughts.

134 Likes

Thanks a lot for the wonderful writeup. I have always been a reader of your posts and helped me immensely.

Just to add, I am not sure Kitex promoter Sabu is a politician and that counts as a risk in this case. He is always at odd with Kerala govt, but now that his major revenue comes from Telangana may make this risk smaller. His party joined NDA in kerala recently.

3 Likes

Thanks for the write up once again and the thesis behind your latest bets. Are you still holding Axiscades by any chance? The recent deal wins along with the latest concall was fairly interesting.

1 Like

Thx for making efforts to share the detailed analysis/thesis.. Did you came across another potential benificiary of US data center capex STLTECH? Its margin were impacted due to tariffs , but with trade deal they should make good profits..

Discloaure: Hold MTAR from lower levels ever since Bloom story started last year.. Bought STLTECH recently .. I have been reviewing AEROFLEX for past weeks

8 Likes

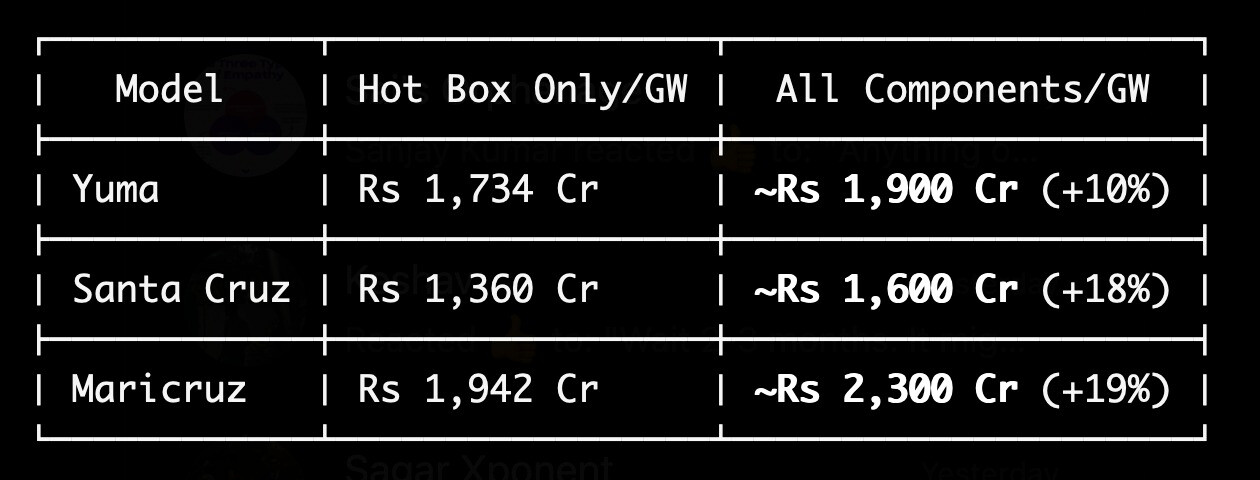

This is a follow-up to my last post, specific to Aeroflex but with also one correction on Mtar. On Mtar, I think my estimate per hotbox is wrong. I re-worked it based on export data and this is what I found - My earlier estimates were only ~1000Cr/GW which is incorrect. Its much higher, esp for the latest Maricruz model hotboxes that they are shipping recently.

Moving on to Aeroflex - there is a great piece on semianalysis on data center cooling that came out last week which I think is essential piece to understand the importance of cooling systems in data centers. In addition, I did some research on the lay of the land as well as Aeroflex’s capabilities in DC liquid cooling. The crux of it

- Every watt of electricity consumed by the chip is converted to one watt of heat and needs to be dealt with. So 1 GW DC would need proportionately more cooling than a 100 MW DC

- Cooling is the second-largest capital expense after electrical systems. Without cooling, both life and performance of GPUs will reduce (thermal throttling)

- DC effectiveness is measures using PUE (Power Usage Effectiveness). It is simply Total Facility Power / IT Equipment Power (1.0 means zero energy wasted). 1.5 is industry avg. Microsoft/AWS report 1.15-1.22. Google/Meta have custom solutions that give them ~1.10

- In the past (2000-2015) we had 5-10 kW per rack which went up to 10-20 kW per rack between 2015-2023 for hyperscalers like Google/Microsoft for cloud compute (mostly cpu workloads for web applications). Now we are talking 120 kW for a Nvidia GB200 NVL72 rack for AI workloads. 120 kW/rack cannot be evacuated using fans - it needs liquid cooling

- Vertiv co-developed the standard for cooling for GB200 NVL72 platform with Nvidia and this will be most ubiquitous design gaining market share going forward for all Nvidia Blackwell based chips. Aeroflex is exclusive partner for Vertiv in India for 5 years and Vertiv is also building a supply-chain in India for export markets as per recent call

- Nvidia Rubin and Rubin Ultra platforms which will hit the markets in 2-3 years time after Blackwell have energy density of 600kW/rack. So liquid cooling is going to be the future. Currently liquid cooling is a small part of the market but it can be 60-70% of the market going forward

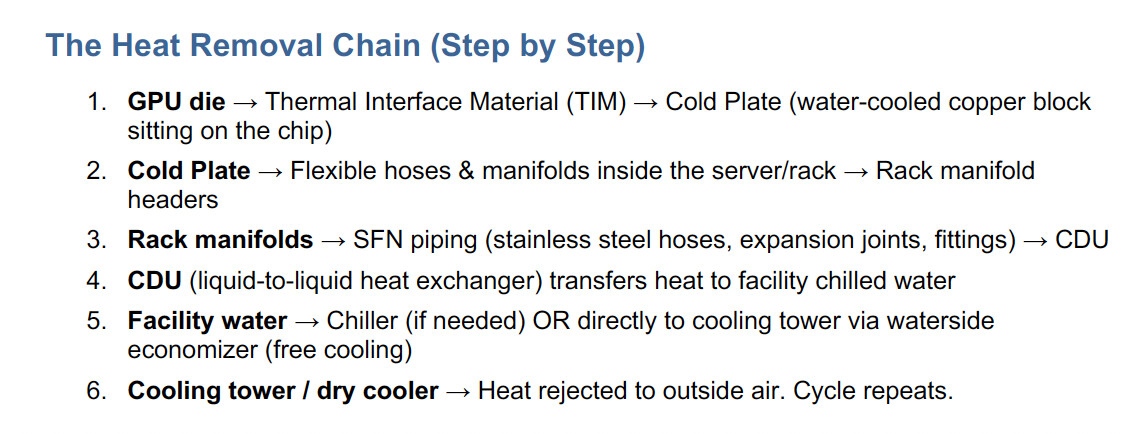

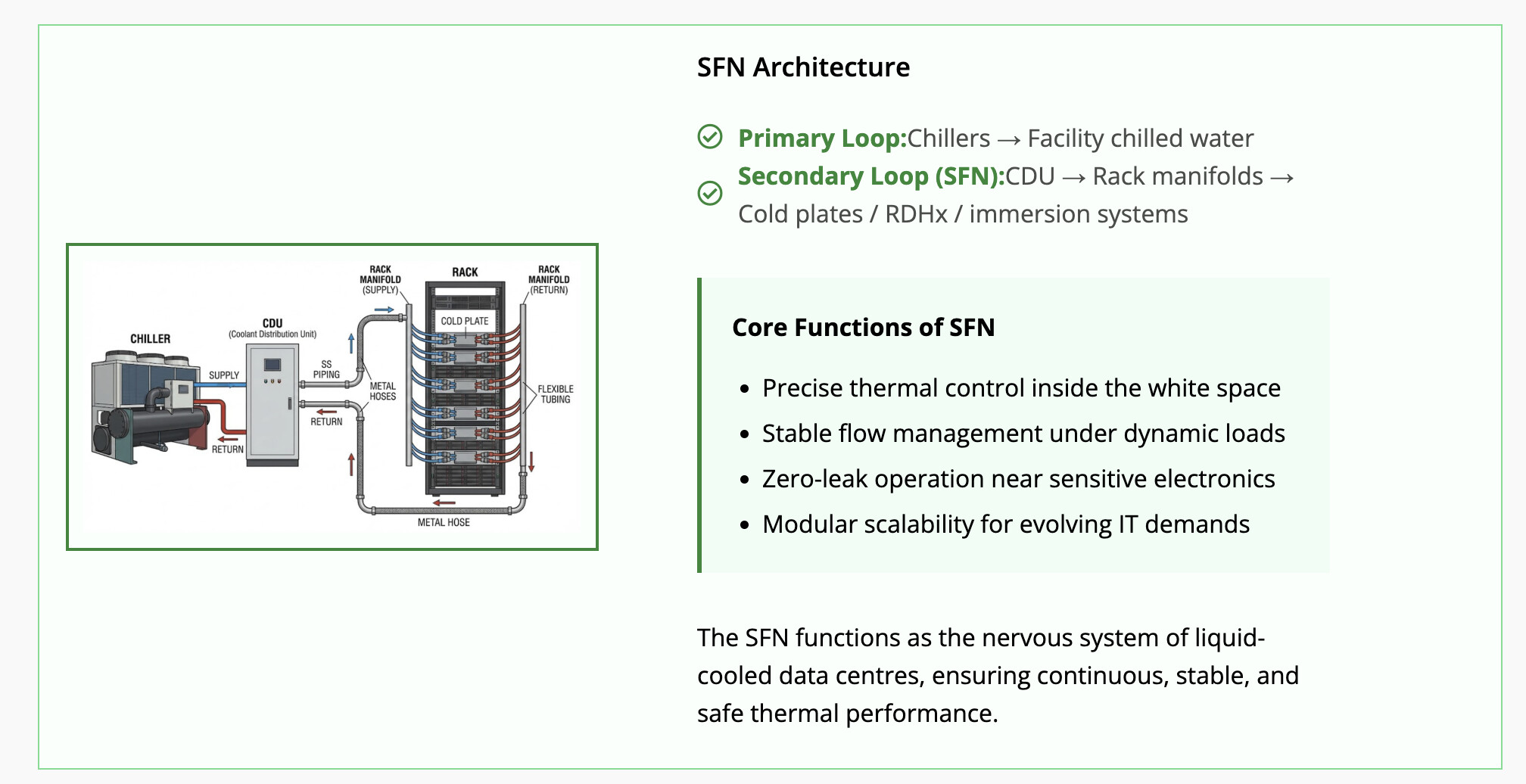

The basics of how liquid cooling works is - there is a loop of water flow that carries heat away from the chip and another loop of water/air that carries that heat out to the environment. Strangely, the loop that carries heat from the rack is the secondary loop (I was initially confused by this) while the one that carries it outside the building is the primary loop. When I saw Aeroflex was in secondary loop, I assumed they do building level cooling but that’s not true since they are in SFN (Secondary loop). This is roughly what happens

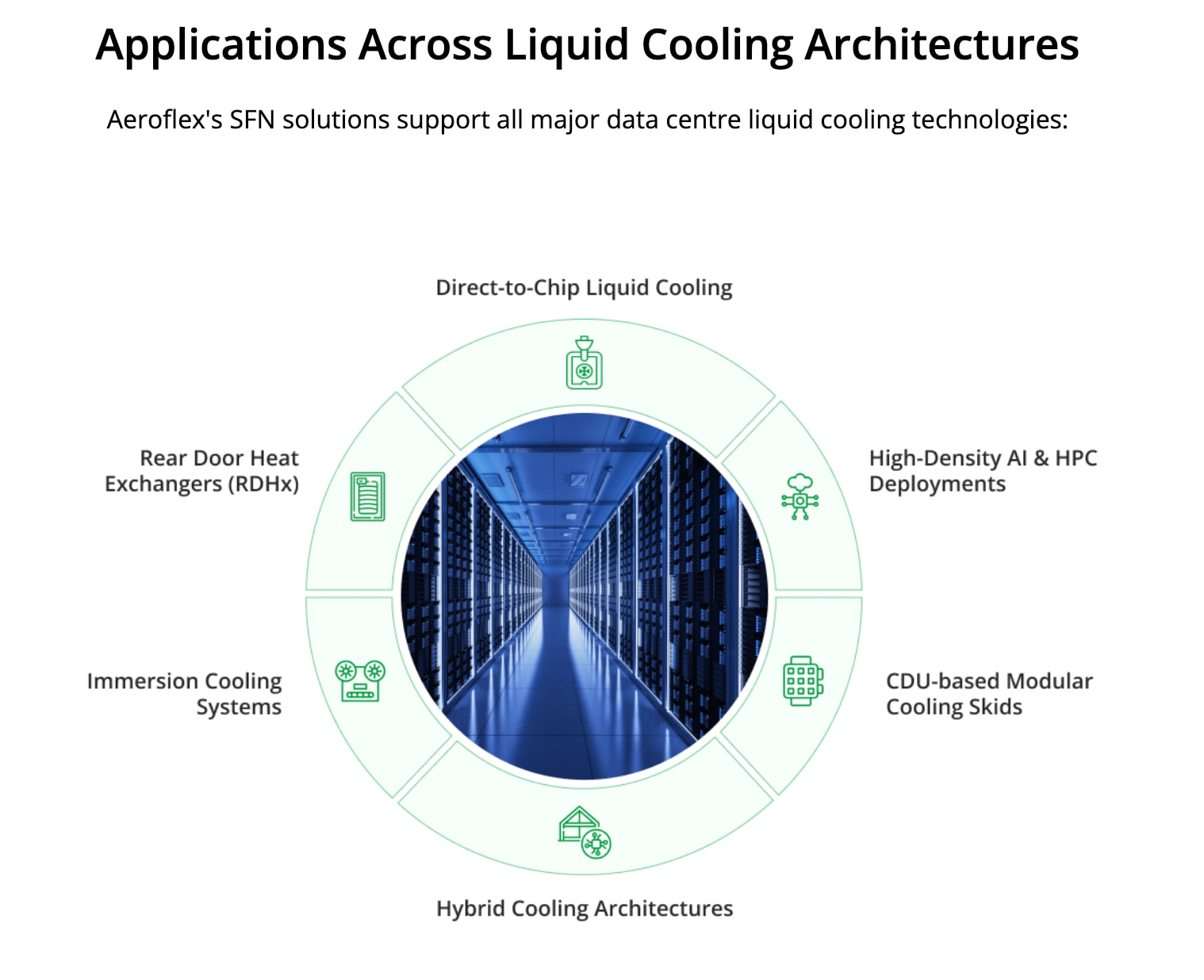

Where does Aeroflex figure in this? They are present in all different types of heat removal from the rack (check the semianalysis piece to understand RDHx, immersion cooling etc.). The one above I described is basically Direct-to-Chip liquid cooling which is what Vertiv-Nvidia GB200 spec is for Blackwell.

This is also from Aeroflex DC Liquid cooling page. In this again the primary loop vs secondary loop (being in the data hall and removing heat from rack) is clearly explained in the diagram

So Aeroflex provides Stainless steel flow systems for CDU skid piping, Rack manifold headers, High-flow trunk lines and metal hoses for Rack-level manifold connections, Modular skid interconnections etc. and also Metal bellows/expansion joints and precision fittings like quick release couplings, ferrule fittings etc. (interestingly the semianalysis piece talks about how even simple stuff like quick disconnects are in short supply currently).

Competition for Aeroflex is mostly international - companies like Parker Hannefin, Penflex, Swagelok (these 3 are the biggest). Aeroflex might have cost advantage being an Indian player to compete in export markets.

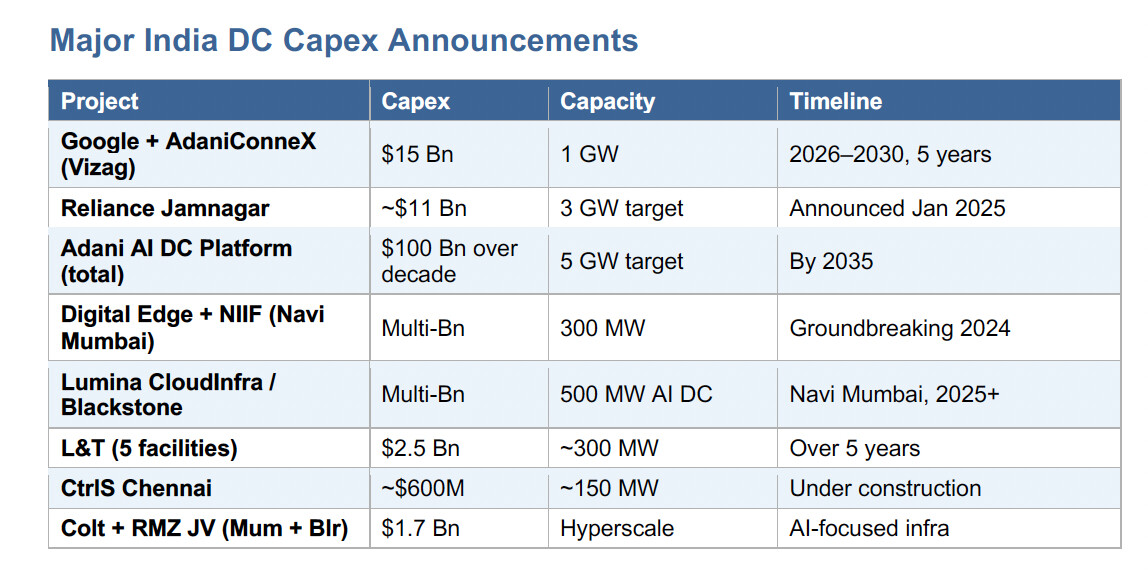

Indian DC capex announced so far

There is very good chance for Aeroflex to make it big considering we are currently at ~1.2 GW of DC capacity (mostly for CPU workloads, so mostly air-cooled) to ~5-8 GW by 2030 and most of the incremental capacity being for AI workloads - within that most would use Nvidia Blackwell chips and thus would use GB200 and Nvidia-Vertiv’s liquid cooling design.

Disc: Invested, have recent transactions

80 Likes

Thank you for sharing great details, very useful.

Any thoughts on orbital data centres being pursued by SpaceX? Would they both co-exist?

1 Like

thank you for sharing your notes. Another DC play related to Bloom and Mtar is Carborandum Universal. They make ceramic product that goes into these SOFC made by bloom. Though they have never mentioned Bloom, but they have talked about fuel cells and expansion plans and margin uptick. As per my basic research this is linked to Bloom and Mtar expansion plans. I do a very high level research for my investments. If you end up doing a detailed research , pls share with me as well. I have a decent position entered recently and looking to increase the same. Need to understand future earnings as currently this is not the major business of the company

16 Likes

Thanks for the insightful research.

I was doing research on the similar topic, you have already listed most of the things that i found.

Some more information/inferences that i found/made are as follows.

Reliance has announced recently much bigger capex ~$110 bn. This is for there complete AI stack, 100% might not be for data centre but definitely much much bigger than ~$11 bn.

A quick search would show that ironwood (v7 TPU) google’s in house chips are around 40 to 50% more efficient than nvidia’s blackwell (nvidia tax). Also Google majorly uses tpu to train gemini and its own AI workload.

Google also continues to buy from NVIDIA to provide computes to its cloud customers (it is not easy for them to move out of CUDA software)

This concludes that Vizag data centre might be a very TPU heavy facility.

The above inference is drawn cause, for TPU, google has its own internal design for cold plates which it has open sourced recently under project Deschutes. And its preferred vendor for this is CooliT systems, so maybe.. maybe.. vizag will not use Aeroflex/Vertiv cooling systems. Though i could not find any manufacturing facility of CooliT in India.

The Vertiv and Aeroflex partnership is very obvious. Vertiv has its chakan plant just 7 kilometres from Aeroflex/hyd-air facility.

Mukesh Ambani in the AI summit confirmed 120MW would come up in second half of 2026. To scale this to 3 GW is not normal task, and i really think instead of putting together the chips at jamnagar, Reliance would go for completely integrated solutions offered by Vertiv which are all tested and ready to plug in.

Something on the lines of RD500N listed here Accelerate your AI deployment with Vertiv™ 360AI . Might be also a completely custom solution for Reliance. But since the blueprints are not available could not read into how many cooling plates and how much of plumbing would be required in this kind of setup.

The plant in India and the 5 year exclusive contract means vertiv has a good visibility of revenue from India and wants to keep its supply chain friction less.

Was not holding due to valuation discomfort and not a huge revenue clarity from vizag plant. With Adani and Reliance in picture will have to evaluate what peak revenues could touch other than ~400 crs post current capex completion (even with 400 cr peak utilisation current valuations doest not look very juicy). And if current capacity of 15000 units will suffice or more expansion might be on the way.

Disclaimer: Not holding, tracking actively.

35 Likes

Dont have much to say on the war. It is about as chaotic, random and value destructive as the tariffs. It is strange how we have become agents of chaos ourselves, looking to parse signals and act, only to regret it shortly after. Ones acting very less because they are diversified into other asset classes, hedged or have sufficient cushion of cash/liquid assets or a rare stomach for volatility are doing alright because it has helped them act less. And that has been the key - acting less or not acting at all is the best strategy because the whipsaws seem almost manufactured at will to create volatility and profit from it. I don’t think we are anywhere close to a resolution or an end to this war. Its going to be a grind and we may not have seen the last of $100 crude. Even $80 for a few months is terrible for us.

Few things have changed since I wrote this post

Opinion on this post was very divisive here then but most people are now in agreement that claude code is amazing and its easier to vibe-code things into existence with little to no skill. This was apparent back in Sept/Oct where the first big boom happened and then again in Nov/Dec where the harnesses improved a lot more than the model itself and made it a joy to use and actually be productive.

On this as well, there are substantial improvements now

I have been using a bunch of open weights models (most Chinese) over last few months for different things. Few just to benchmark capabilities, few to fine-tune/distill. The recent qwen3.5 series models are just so good that they have become my daily drivers for a few things, instead of using cloud APIs.

I could not have said the same 3 months back. The latest models, coupled with claude code are doing reasonably well at ~30-40 tokens/sec (m4 pro mac mini with 20 core gpu) which was unimaginable a few months back. At this trajectory, I think a year or two from now, most devs should be able to run local models on their macbook pros for their development workflows for generating code.

Where does it put the data center thesis? I was very pessimistic in Nov but changed my mind reluctantly after vibe-coding a bit and took some bets in DC space (Which i continue to hold). I think the economics as it stands today, heavily favours DCs becase

- They can sweat their assets a lot better than a hobby coder like myself can. Consequently, AI companies have bid up prices of DRAM/SSD (incidentally some of my best investments last year were the 6TB spend on SSDs). Also they have priced plans lot cheaper even if it means making losses. The price being bid up has made Apple remove the 512 GB Mac Studio from their stores due to DRAM shortage. This is a win of sorts for DC theme

- Companies/people preferring opex to capex when payoff is uncertain

- As a consequence of #1, companies like nvidia, samsung etc. diverting production towards DC products than retail focused GPUs, RAM modules where they make better margins

However, things can change if Samsung/SK Hynix capacities come online by mid/late next year making RAM/SSD prices cheap again (lets not forget that these chips are a deep cyclical commodity), and open weights models continue their trajectory of improvement - I think a dev can hold a macbook pro costing 1.5 - 2.5 lakhs and comfortably build with local LLMs in 2 years for certain imo. This is the future that should worry companies investing in DC capex. We should pay attention to pullbacks of capex plans like this. The other thing to follow is funding for DCs coming mostly from middle-eastern sovereign funds through private credit in the US markets and how it gets impacted by the Iran war.

27 Likes