Phoenix lamps – rising up from the ashes ?

CMP – INR 115

Having learnt from both Warren

Buffet and Phil Fisher, I have developed my own unique style of stock analysis

– that involves about 40-50% of analysis on the ground (which a lot of analysts

miss out on) the rest in desk research- reading AR’s, analysing numbers etc. I

would like to call this the Holmesian way of analysing stocks - unlike

conventional analysis that relies heavily on secondary research, this creates a

double loop mechanism that feeds into the other engine and helps validate or

reject the thesis. This has often proven to be quite an advantage in micro caps

where often “what you see is not what you get in the numbers” and vice versa.

Said all of this, it is seldom

that I come across a stock that is a purists value investor’s delight which

offers a triple play of reversion to mean, de-merger/spin-off optionality and

pure and simple undervaluation. I must thank my friend, Gokul raj who introduce

me to this stock and also shared his note with me from which I have generously

borrowed.

Company background – phoenix

lamps – left for the dead, about to fly higher

The company is Phoenix lamps and

is a small/micro cap with a Market cap of INR 3,250 MM with no analyst

following (don’t I just love these) and of course low liquidity and

institutional interest.

The company, which was majority

owned by Actis was a classic study in “di-worsefication”. A near monopoly

business in automotive head lamps/tail lamps gone terribly awry through a

diversification into CFL’s which is cut throat, high intensity, B2C, branding

heavy business. A decade later and the mistake corrected through a slump sale

of the loss making CFL business, look at the ratios and you will be impressed.

High RoE, high ROCE, FCF positive business with high asset turns (11 x FA

turns) with a 20 % + EBITDA margin with ROCE of 30 % +. It’s got near FMCG

characteristics given the standard nature (My friend at bosch says the key to a

higher margin business in auto is a. high standardisation b. high value to

weight/volume c. OEM + after market possibilities and that’s why bosch is

always in things like ABS, wipers, air bags which are critical parts and fairly

standard. The only exception are high finesse items which involve a lot of high

end labour like machining and critical engine parts.

I looked at the company in the

past and the only reason why I let it slip was the lack of alignment between

shareholders and management – the existing shareholder actis wanted to sell,

the management guys were all professionals who had no clue about shareholder

value.

Recently the company got bought

over by suprajit engineering and this got me delving deeper again.

Triple play – great, proven capital allocator at the helm + improving

business prospects + re-rating possibilities

Let’s get the easy one out of the

way –actis has been stuck in the company for 9 years and started selling down

their shares (from 70 % to 60 % ) and this has resulted in the share price

going down from Rs. 180 to Rs. 100 over six months with no change in

fundamentals. That’s gone and a simple reversion to mean should take this at

least 50 % up.

The business is the largest and

one of the top 3 (Philips, osram) in the

automotive OEM. It’s the largest with 55 % market share in cars/PVs, 60 % + in

CVs and 80 % in two wheeler OEMs. Had lights are a small value but critical

item where there can be no downside – since that entails warranty claims and

OEM’s prefer to play safe with an indian manufacturer. Inspite of all the mega issues involving loss

of focus, it is to phoenix’s credit that it continues to be a leading player –

the threat of Chinese exists in aftermarket but not at OEM level (double

verified) because of quality/warranty issues.

Given the research I have done by

talking to a dealer/distributor, this can be a 15 % growth in the aftermarket

and a 7-8 % in OEMs, going forward.

Suprajit is well known to value

investors in the indian market. I have personally interacted with ajit rai and

I think he is an outsider CEO – buys cheap and is an exceptional operator with

a focus on bottomline and cash flows. He has been looking at acquisitions for

long and finally bought one which in his own words was a company that

manufactures :

Scalable, global standardized product

With a market leadership position in indian

market

With export possibilities

Complementary to his core business of two

wheeler cables

High margins and strong cash flows with minimal

debt

Given what he has done with

suprajit – have a look at ROIC of 30 % consistently and his own

salary/remuneration etc. and I am sure that he will do a good job of at least

maintaining status quo – which by itself should lead to a re-rating

Scuttle butt and research

Spoke to a couple of distributors

and a friend at Philips ;

Philips guys’ inputs – already exited

this market by selling their entire global lighting division. Used to be focussed

on auto market but has slowly exited – still sells high margin products in

after market but for all practical purposes has stopped supplying to OEMs

because of pricing pressures – they exited this business as they were

manufacturing in high cost locations and they want to concentrate on high

margin medical business

Distributors :

Phoenix brand is well known in

north but not so in south/west

Quality is still the best – very few

customers come back for returns

Supplies white labels to even

brands like bosch and has a good reputation for quality

Last 3-4 years have been playing

hot, playing cold – not enough attention in the market

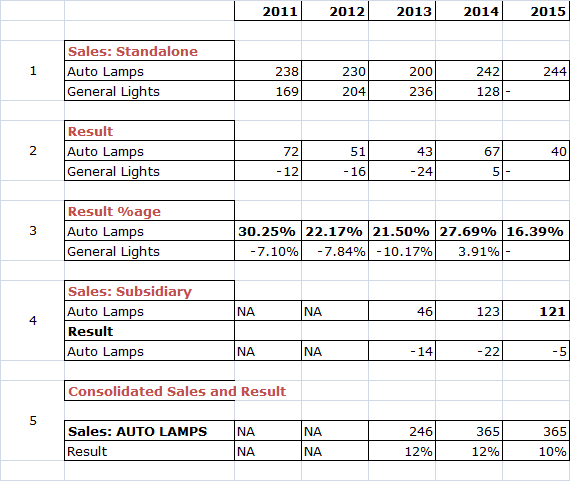

Valuation :

I am attaching an excel sheet

from the screener template and you will find that both EBITDA, asset turns and

RoCE are increasing and last year’s dividend yield was a whopping 11 %- expect

this year’s to be at least 4- 5 %. (that’s a 5 % off on an already discounted

price for suprajit). It’s trading a 8 x

FY 15 and at about 1.8 x PB with an RoE of 30 % translating into a shareholder’s RoE of about

16-17 % - I look for fat pitches with a minority shareholders’ RoE of 10 % (viz., ROE divided by P/B) and that’s a fat

pitch IMHO.

Just mere re-rating to 12-15x

with an EPS growth of 15 % which is doable can lead to a 3-4 x over a few years

and of course if this gets merged into suprajit (which by all means it should),

it should be a fairy tale ending similar

to sun/Ranbaxy.

This has characteristics similar

to companies like Bosch (definitely a notch inferior) on EBITDA margins etc. –

not for nothing does Bosch think highly of this company.

I also expect modest synergies

from cross selling to suprajit’s clients.

The fly in the ointment is the

acquisitions they made in Europe which had a zero profit – they apparently

repackage the bulbs manufactured here and brand them and sell them in Europe –

which IMHO, is a so-so business unless suprajit can turn this around. I expect

zero contribution from this going forward and I would be pleased if there is no

good money to be thrown after bad.

LED’s are a risk but from my

talks with several industry experts given the :

Price differential

Harsh indian conditions of frequent hits which

lead to replacement of expensive bulbs

Wear and tear and rattling that result in LED

life getting shortened

LED’s are not a threat at elast

in the low end cars/CVs/ two wheelers for a long time to come. Even otherwise,

LED’s are only a supplement and cannot replace head lamps – most have only day

time running lights that are LED’s. Only Rs. 20 lakh plus cars have xenons and

LEDs’ and that will take some time to percolate down given the huge costs and

maintenance issues.

I see this as a high RoE business

in a slow growth industry (similar to Duracell purchase of warren buffet) which

can maximize FCFs and grow at a steady pace of 10-15 % easily without any

incremental capital and provide for a dividend yield of 3 – 4 % with a PE

re-rating upside.phoenix mills - numbers at a glance.xlsx (74.2 KB)phoenix lamps - value pickr.docx (18.7 KB)