alright thanks a lot

1 Like

PCBL – A Business analysis, 5th Jan 2024

Background

PCBL is in the business of producing carbon black from petroleum-based feedstock (Figure 1) and selling it globally (Figure 2). 17% of the feedstock is sourced domestically while the rest is procured internationally (AR 2023). 2% of PCBL’s revenue also come from selling power – too small and ignored henceforth.

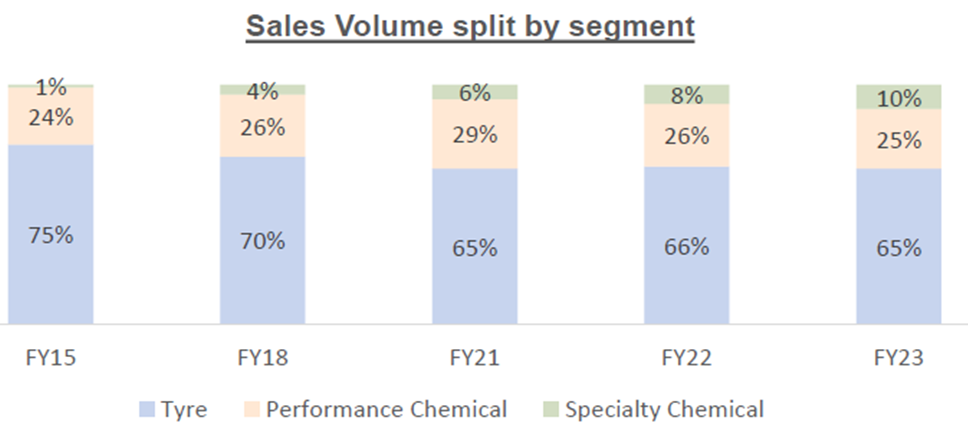

PCBL offers a comprehensive portfolio of tyres, specialty and performance chemicals. Carbon black used for the tire business (20% by weight of all tyres) is largely a commodity play while specialty and performance chemicals, whose share of overall revenue is steadily growing and is now at 10% (Figure 3), constitutes a higher margin business (2-2.5x margins compared to tyres). Figure 4 shows the application areas of these performance and specialty chemicals.

Globally, non-rubber specialty blacks constitute 7% of the total demand so with 10% sales, PCBL is doing well on this front (JM Financial report, 15th Nov 2023 – this is a good report by the way; perhaps too optimistic but a good read nevertheless to understand the business).

Figure 1: Using carbon black feed stock to produce carbon black

Figure 2: PCBL has five manufacturing locations in India and markets its products globally (50+ countries, 6 continents).

Figure 3: The share of the higher margin specialty chemical business is growing steadily. The absolute numbers for the revenue are also sensitive to crude oil prices.

Figure 4: The tyre business is a commodity play while performance chemicals (used for rubber-based products) and specialty chemicals are a higher margin business.

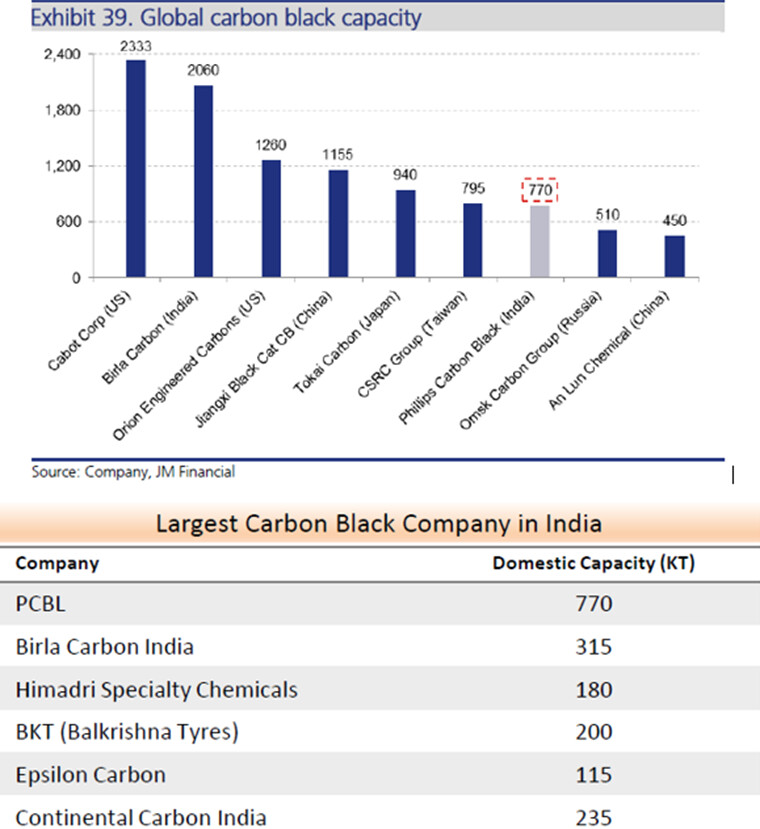

Figure 5: PCBL is the seventh largest carbo black player globally and the largest in India (JM Financial report – 15th Nov 2023, Investor presentation Sep 2023). Birla Carbon, while an Indian company has large manufacturing capacity in the USA.

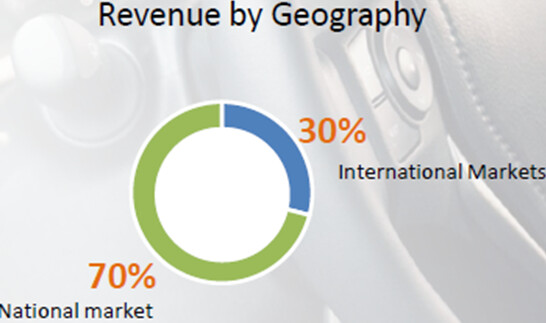

PCBL happens to be the largest producer of carbon black in the in the Indian market and the 7th largest globally (Figure 5). Within India, PCBL has a 35% market share. Overall, 70% of PCBL’s revenue comes from the domestic market (Figure 6).

Figure 6: PCBL’s revenue split by geography.

After all planned expansions are completed, PCBL’s capacity will be 790 KTPA of which 112 KTPA will be for specialty blacks. The Mundra expansion is brownfield while the Chennai expansion is a greenfield project with future potential for brownfield expansion (additional 90KTPA, concall Oct 2023). Capex for Mundra was INR 3400M, for Chennai was INR 10,000M). Brownfield expansion takes about a year while greenfield, after land clearance has been obtained, takes about 1.5 years to completion (concall July 2023).

Figure 7: Carbon black manufacturing capacity in MT per annum after all planned expansions. (JM Financial report – 15th Nov 2023).

Business drivers

This is an inherently cyclical business owing to the exposure of the company’s margins to crude oil prices. Further, its fortunes are linked to the growth of the tyre industry, a proxy for economic growth.

There is also the risk of competition and dumping by Chines manufactures – on the wane off late since China uses coal tar pitch as feedstock and its price is trending higher (see details in JM Financial report)

Basically, PCBL is still largely a commodity business that is slowly growing the specialty space.

Analysis of Financial Statements

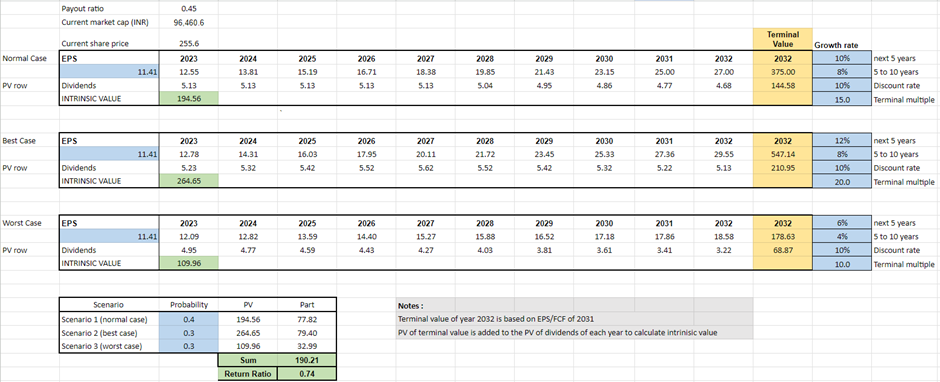

As shown in Table 1**,** the business has had decent growth rates on the equity, EPS and revenue front. These are likely to continue given the recent expansion that will be fully online in 2024. EPS is a good metric to value this business considering that share count has gone up by 10% over the last 5 years and that FCF is unpredictable given growth capex for expansions and working capital changes. The ROIC of 16% is pretty reasonable for such a business – considerably higher that cost of capital, say about 10% for debt – but lower than what a pure specialty chemical business will have.

Table 1: Key metrics from financial statements in millions INR over the past five years.

As Table 2 shows, under current EPS assumptions and current dividend payout ratios (sustainable as planned capex will end), the company is fully priced for a 10% return (best case scenario). More realistically, given the current price, henceforth the return will be only 7.4%.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

It’s a straightforward business but with no real moat and no pricing power. But a useful business nevertheless. The key to such businesses is buying them cheap and not counting on more than 7-10% growth. One can also think of it as an opportunity to buy a decent commodity business whilst acquiring a small stake of a specialty player at commodity prices. In 2023, I had purchased a small amount at INR 120 with limit orders set to exploit further falls. As luck would have it, it has gone straight up and is now a 2x in a year. Too pricey for me to buy in now.

Company news

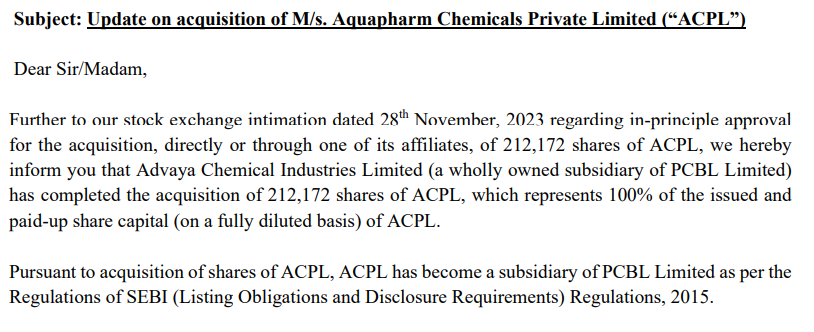

Aquapharm acquisition, general info : All the analysis above is valid for the PCBL business before PCBL announced that it would be acquiring Aquapharm Chemicals Private Ltd (ACPL) for INR 38,000 million which is approximately 40% of the market cap of PCBL, so a pretty large acquisition!

ACPL is active globally, particularly in the water treatment sector, manufacturing a range of specialty chemicals such as phosphonates, biodegradable chelating agents, polymers, biocides, and oil field chemicals with applications in diverse industries. ACPL, operational since 1974, has manufacturing facilities in India, the United States, and Saudi Arabia. So, with this acquisition, PCBL is surely moving into the specialty chemical space although it’s a different space than its current business of carbon black.

According to a March 2022 Crisil report, Aquapharm derives a major portion of its revenue from exports to Europe, North America and other regions. Aquapharm, had a revenue of Rs 20,000 million and EBIDTA of Rs 4170 million in 2022-23.

Insights based on Concall info , 28th Nov 2023 : Phosphonates are 53% of ACPL sales; oil and gas chemicals is 25%; and polymers, rest. The purchase price of Rs 38,000 million is approximately 9xEBITDA so it’s a good to a fairly priced acquisition considering that the EBITDA margins are 20% whilst that of PCBL are around 14% (selling at a 13xEBITA multiple). The promoters of ACPL were looking to cash out and that’s the reason for the sale.

Aquapharm is debtless and the acquisition will be paid for through raising debt of Rs 38,000 million. The promoter of PCBL in the concall was pretty clear that he does not like debt and wants to pay it down quickly – his assumption is that it will be paid down in 30 months since the combined EBITDA of PCBL and ACPL would be around Rs 40,000 million over 30 months.

I don’t buy the narrative that the total EBITDA over 30 months of Rs 40,000 million is enough to pay down Rs 38,000 million in debt. Interest and taxes are real expenses, i.e., money out of the company and also, a certain amount of maintenance capex is needed.

In the concall of July 2023, the promoter mentioned than the maintenance capex per plant is about Rs 130 million, so with a total of 5 plants that’s about 650 million. Let’s say that for ACPL is about 40% of 650 million, so about 260 million per year.

I have an approximate calculation of cash flow of the combined entity in Table 3 with the following key assumptions:

- Interest rate of about 10% on additional loan on Rs 38000 million which is what PCBL is paying on its current debt,

- EBITDA growth rate of 10% for the next years

- Depreciation of PCBL remains constant at 1600 million per year (which is the current rate). Assume about 40% of this for ACPL so about 700 million per year.

- Maintenance capex of 910 million per year (650 + 260, PCBL + ACPL)

- Through the course of every year PCBL tries to pay down the loan with its FCF. And it pays no dividends during this period.

- No further growth capex of PCBL or ACPL – this assumption will likely not be true but depending on how the business is doing it might well be worth it to invest more in growth a couple of years down the line.

Based on Table 3, the cumulative cash to pay down the debt after 4 years is approximately 32,000 million (5700 + 7069 +8670 + 10420). If EBITDA growth rate is 15% then its about 35,000 million.

So, 30 months is quite optimistic to pay down Rs 38,000 million and would require really high growth rates and perfect execution. On the positive side though, the debt should not be too much of a problem. If the company pays no dividends, it can get the debt down to reasonable levels in a couple of years.

Table 3: Cash flow outlook after acquisition of ACPL

Catalyst

Execution on the acquisition and the rate at which they pay down the debt will determine how the business performs. I am going to wait and watch over the next couple of years, likely earnings will contract because of large interest payments. A good opportunity to buy a 50% specialty chemical business at commodity business prices might arise. On the watchlist!

15 Likes

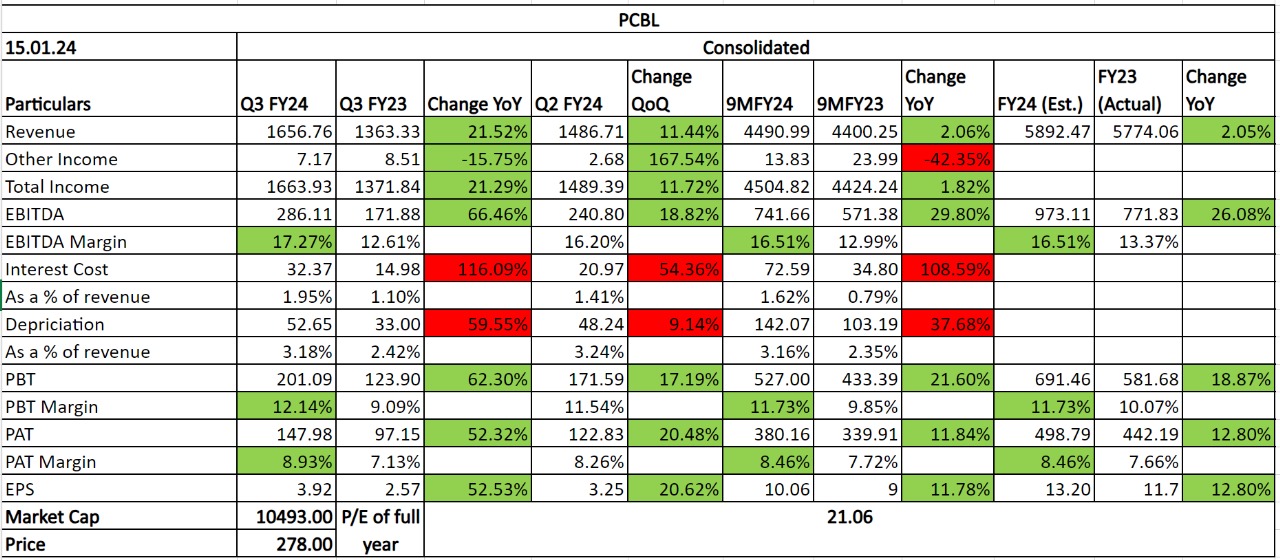

PCBL Q3 Results: Net profit up 52.6 percent at Rs 148 crore vs Rs 97 crore and revenue up 21.5 percent at Rs 1,656.8 crore vs Rs 1,363.3 crore, YoY. Company also declared dividend of Rs 5.5

1 Like

The finance cost has increased by 11.4Cr qoq which means a debt of around 700Cr for a year going by their current interest rate of 6.3 percent. The pdf talks about debentures issued for around 700Cr.

As per my estimate revenue should cross 6100 crores and profit 500 crores

2 Likes

Hi valuepickr members,

PCBL is corrected by almost 20% from its 52 week high.

Is there any news or development which can justify this correction? Is Mr. Market expecting weak upcoming quarters ?

Seems margins have peaked and now market expecting drop in margins as crude market is likely to remain right in the coming days.

1 Like

almost all the small caps have undergone corrections since the past 2 weeks no matter how strong the companies are. Also i feel that PCBL was indeed a little over heated with low of 108 and high of 340ish. (3x within a year is bullocks!).

So a lil bit of profit booking is justfied imo

3 Likes

Integration of the acquisition is a key item to monitor in the coming quarters. Any positive management commentary regarding the integration can be a potential trigger for the stock since analysts have been skeptical about the management’s ability to execute large acquisitions.

2 Likes

PCBL did Aquapharm acquisition followed by INR 448 Crs warrants issue (equity at maturity) which stands at around 7% of current net worth. Below is my brief thought process:

Thesis:

- Management is trying to move towards more stable margin business from commodity highly cyclical. They have selected market leader in the segment (2nd biggest globally). In case this works then we’ll see totally different PCBL in few yrs.

- Warrants at reasonable price is a signal that management is doing walk the talk. I have seen many companies issue warrants at quite cheap rates (as they get at older average price) when stock prices zoom, taking advantage of price movement. But PCBL seems to have not taken advantage of this. Also reason for this equity infusion was guided well in advance.

- Promoters are connected to chemical business. Though not openly revealed but Nov-2023 concall hint is there about know-how of opportunity in this acquisition.

- Valuations for Aquapharm are quite reasonable. As an optionality, in case this chemical company’s earnings/margins are right now temporarily suppressed due to overall chemical industry headwind, then it can be great acquisition.

Antithesis:

- It is definitely a divesification into unrelated business. Management will require able team to run this business.

- As new company acquisition is still its at early stage, no management guidance exists. Quantification of future size is difficult at this moment.

Overall:

I have taken small tracking position, mainly due to confidence and walk the talk from management. But definitely it’s an early stage, actual benefits will take some time.

11 Likes

5 Likes

4 Likes

PCBL Limited Q1 FY25 Earnings Conference Call Key Takeaways:

Financial Performance :

PCBL Limited achieved record operational and financial performance in Q1 FY25. - Consolidated sales volume (Carbon Black) increased by 25% YoY to 1.54 lakh tonnes. - Consolidated revenue from operations rose by 59% YoY to Rs.2,144 crores. - Consolidated EBITDA grew by 72% YoY to Rs.369 crores. - PAT increased to Rs.118 crores, marking an 8% YoY growth. - Ecoform Q1 FY25 Revenue stood at Rs.359 crores. - Ecoform Q1 FY25 operational EBITDA reached Rs.55 crores. - The current annual revenue run rate has exceeded US$1 billion and is expected to accelerate further.

Operational Performance

PCBL Tamil Nadu achieved a sales volume of 28,228 tonnes. - The new Chennai plant gained approval from all major tire manufacturers in India and reached 85% capacity utilization. - Carbon Black sales volume: 90,438 metric tonnes domestically and 63,480 internationally. - Export sales volume saw a strong growth of 56% YoY in Q1 FY25. - Highest ever power generation and sales volume was recorded, with an average power realization of Rs.4.16 per kilowatt-hour. - The Ecoform business witnessed a steady improvement in performance post-acquisition, with efficiency improvements and cost optimization measures expected to yield positive results.

Future Outlook

Confident in achieving 11.5-12% CAGR volume growth in the Carbon Black business over the next 4-5 years. - Operating margin and EBITDA per tonne are expected to increase over the next five years. - Management sees a strong possibility of EBITDA increasing by Rs.4,500-5,000 per tonne. - Significant growth in international sales volume is anticipated in the next few years, driven by European tire manufacturers increasing sourcing from India. - Expansion of the product portfolio and customer base is also expected.

Capacity Expansion

PCBL Limited is pursuing an aggressive capacity expansion program across different segments. - The Carbon Black capacity is expected to reach 8.8 lakh tonnes, including specialty capacity of 1.12 lakh tonnes. - Power capacity is set to reach 134 megawatts upon completion of expansion. - The Ecoform capacity will be doubled in the next five years across geographies.

Capital Expenditure

Long-term CAPEX will involve adding roughly 4 lakh tonnes of additional carbon black capacity and doubling of Ecoform capacity across geographies. - Total CAPEX is estimated to be roughly Rs.3,300 crores in the next five years.

Debt

The current gross borrowing stands at Rs.4,400 crores, with estimated cash flow in the next five years reaching ~Rs.10,000 crores, which is sufficient to cover CAPEX and repay entire debt.

Other Key Points

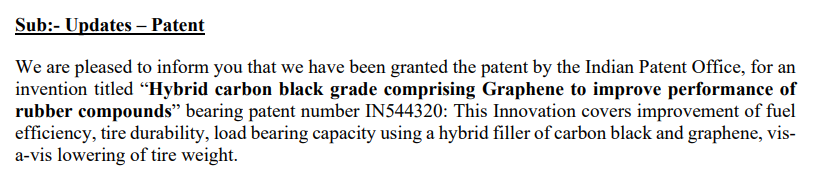

PCBL Limited is focusing on R&D for technical advancement and business expansion, with recent patents received for hybrid carbon black grade with graphene. - The company believes that the long-term prospects of all business segments look positive. - Exploration of backward integration for Yellow Phosphorus in the Middle East and other initiatives beyond the current segments are underway.

Disc: Invested

3 Likes

Do I understand it right?

- Company expects to generate 10k cash in the next 5 years.

- Gross Debt 4400 cr

- Capex expected 3300 cr in the next 5 years.

Seems like there is a possible downside and not a lot of upside interms of FCF.

2 Likes