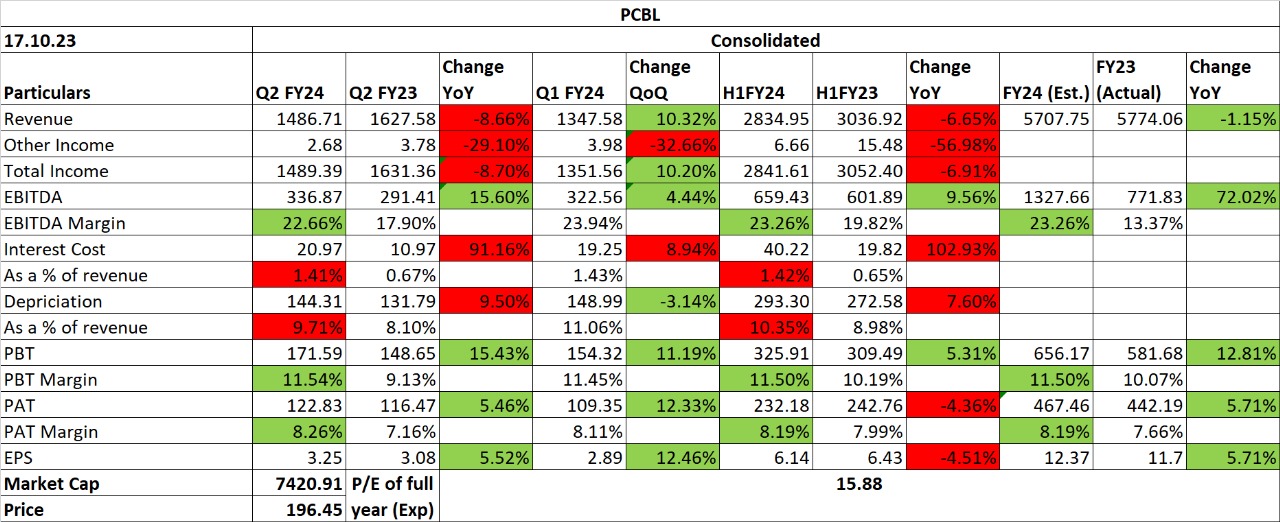

PCBL Ltd Q2FY24 Concall Highlights

PCBL | CMP: INR 198 | Mcap: INR 74.76bn

Volume is expected to grow 12% to 13% over the next 4-5 years.

Capex of INR 12.8bn would bring additional revenue of INR 17bn – INR 18bn per annum going forward.

EBITDA per tonne is expected to reach INR 20,000 by FY27E.

Europe exports are expected to double in the next 2 years.

Revenue

Revenue is expected around INR 16bn to INR 17bn per quarter if crude remains stable.

Margin

Specialty chemical black margins are 2-2.5x of Tyre margins.

Volume

Volume growth is expected around 12% to 13% over the next 4 to 5 years.

Domestic sales volume stood at 82,276MT and International sales volume stood at 47,835MT in

Tyre volume stood at 79,793MT, Performance chemicals volume stood at 34,744MT, and Specialty chemicals volume stood at 15,574MT in Q2FY24.

In the Chennai facility, production volume is around 9,410MT (~50% utilization) and sales volume is around 9,008MT in Q2FY24. Overall, the Chennai facility sales volume was around 14,000MT in H1FY24.

Specialty chemical volume is expected around 50,000MT to 55,000MT in FY24. Q3FY24 volumes are expected to be better.

Capacity & Utilization

The capacity stood at 7,72,000 MTPA as of Q2FY24. The company is expected to ramp up utilization in the next 3 to 4 months. The maximum capacity achievable is around 6,25,000 MTPA (~81% utilization).

The Chennai facility is expected to reach around 80% capacity utilization in the next 3 to 4 quarters. The approvals are expected to come from Tyre manufacturers which will ramp up production.

Specialty chemicals capacity stood at 92,000MT and another 20,000MT is expected to be added going forward.

Around 90,000MT rubber facility is expected to be commissioned in the next 1-2 years.

The company has commenced a 12MW captive power plant in Chennai and the total captive stood at 112MW. Another 12MW is expected to commence going forward.

Capex & Incremental Revenue

Chennai greenfield facility capex is around INR 9.5bn and incremental revenue is expected around INR 14bn. Mundra facility capex is around INR 3.3bn. Mundra facility has two phases. 1st phase capex is around INR 2bn and Incremental revenue is expected around INR 2.2bn going forward.

Maintenance capex is around INR 120mn to INR 130mn per plant which comes around INR 600mn to INR 650mn maintenance capex annually.

Patents

The company has received two patents and started manufacturing for 2 grades. The initial market potential is around 2,000MT-3,000MT and is expected to reach 6,000MT-7,000MT over the medium term. the specialty products contribution realization is around $1,200 - $1,300 per tonne.

Exports

In exports, around 70% of sales from Asia Pacific remain from other countries. The company is exporting to more than 50 countries.

Europe has larger potential and the company is focused on supply chain improvement. Europe volume is around 3% to 4% and expected to be 2x in the next 2 years.

Realization

EBITDA per tonne is around INR 18,427 in Q2FY24 and is expected to reach INR 20,000 by FY27E.

Other highlights

The company is focused on adding capacity every year.

The company is supplying battery chemicals to 2nd and 3rd generation batteries.

Tamil Nadu facility is efficient from a tax point of view.

Outlook: PCBL volume is expected to grow 12% to 13% over the next 4 to 5 years. The capex of INR 12.8bn in Chennai and Mundra facilities would bring additional revenue of INR 17bn to INR 18bn per annum going forward. Europe exports are expected to double in the next 2 years.