Why is this a downside, its a growing company, OCF is +ve which is being used to invest along with debt. Too much of unutilised cash will not help in compounding.

1 Like

I am referring to the downside where expected acquisition and demand don’t come through with high debt.

I would like this risk as long as upside is excellent. But looking at cash positions, within 5 year timeframe, does not seem there is any FCF left to Owners.

Do you think I am being overly pessimistic?

1 Like

One cannot predict the future, there is always the risk of an unforeseen event occurring. However, if you glance through the past few concalls, you will notice that the management’s assumptions for investing in capex (carbon black + specialty black) and the acquisition are fairly conservative in nature. It would be useful to track quality of execution rather than debate the reasoning for the capex.

4 Likes

Brent crude falls below $70 for the first time in 3 years…Direct beneficiary is PCBL

Disc:Invested

Raw material is pass through.

1 Like

Infact,

Volatility and Fall in RM is usually not profit accretive.

- cost of inventory is higher while finished goods are market linked leading to margin compression .

- In falling RM scenarios, end customers usually postpone buying in bulk in anticipation of further fall in their buying price. They usually maintain just in time inventory till prices again show uptrend.

3 Likes

PCBL Limited Q2 FY25 Earnings Conference Call Summary

Financial Performance:

- Consolidated sales volume for carbon black increased by 14% year-on-year to 148,000 tons in Q2 FY25.

- Consolidated revenue from operations increased by 45% to ₹2,163 crores, driven by better realization, higher sales volume, and revenue from the recently acquired Aquaform Chemicals.

- Consolidated EBITDA grew by about 53% year-on-year to ₹369 crores.

- EBITDA per ton in the carbon black business further increased to ₹2,324.

- Power generation increased by 25% year-on-year, with external sales volume rising from 103 million units in Q2 FY24 to 126 million units in Q2 FY25.

Margin Guidance:

- Management believes current margins are sustainable and sees potential for further improvement due to changing product mix, improving operating leverage, and ongoing efforts to enhance manufacturing efficiency and yields.

- Margins are expected to expand in a lower freight rate environment.

- Aquaform Chemicals is expected to achieve an EBITDA margin of around 25% by FY29.

- The battery chemicals business is projected to have an EBITDA margin of around 50%.

Business Segment Performance:

- The tire segment accounted for 82,83 tons of sales volume in Q2 FY25.

- The performance chemicals segment reported sales volume of 49,836 tons.

- Aquaform Chemicals reported steady performance with revenue of ₹362 crores and EBITDA of ₹50 crores in Q2 FY25.

- Aquaform’s capacity utilization remained above 75% during the quarter.

Management Guidance for the Future:

- PCBL is implementing cost optimization and operational efficiency measures at Aquaform Chemicals to improve capacity utilization and performance in the coming quarters.

- The company is undergoing an aggressive capacity expansion program in carbon black, water treatment, detergents, and oil and gas chemicals under Aquaform.

- PCBL expects to commission specialty carbon black projects in Mundra and Dhamra in Q3 FY25, with the second phase of the Tamil Nadu expansion planned for Q4 FY25.

- The company aims to reach 1 million tons of carbon black capacity by FY27-28 and is evaluating options for a proposed Greenfield capacity expansion.

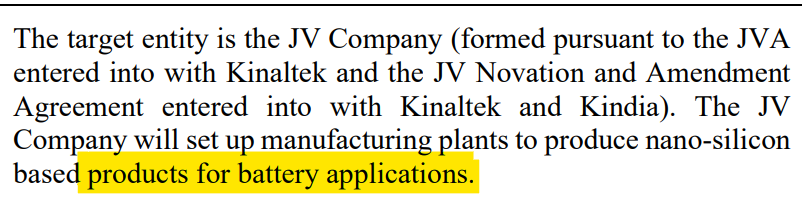

- A joint venture, Nanovea Technologies Limited, has been established with EV India Private Limited to develop nano silicon products for lithium-ion battery anodes.

- PCBL plans to ramp up global sales volume from FY26 onward, with a significant focus on European markets.

Key Risks in the Business:

- Global business environment remains turbulent, with freight rate volatility and uncertain global economic conditions impacting margins.

- Aquaform Chemicals’ oil and gas chemicals business is facing headwinds due to a challenging market in the US, leading to lower capacity utilization and margin pressure.

Industry Outlook:

- The carbon black industry presents a large market opportunity, with the global market size estimated at 15 million tons and a long-term growth rate of around 3.5%.

- Demand in India is expected to increase significantly in the next five years.

- China’s carbon black industry is consolidating, and future capacity additions in China are expected to be limited.

- Russia’s carbon black exports are facing challenges due to sanctions, limiting their capacity expansion plans.

- These factors create a favorable environment for Indian manufacturers like PCBL, with significant growth opportunities in both domestic and export markets.

Disc: Invested

5 Likes

Government of Andhra Pradesh has vide its notification (“Notification”) accorded approval for allotment of 116.62 acres of land, subject to de-notification of the Naidupeta SEZ in favour of the Company

4 Likes

One need to carefully watch the debt of this company and track how they are gonig to reduce

1 Like

Agree, debt is really a problem and with all these expansion and acquisitions, I don’t think its gonna come down soon. I exited today with some modest gains.

1 Like

The Q3 FY25 earnings call for PCBL Chemical Limited (formerly Phillips Carbon Black Limited) . The following is a detailed summary of the call.

Financial Performance

- Consolidated revenue from operations grew 21% year-on-year to rupees 2,100 crore. This was driven by an increase in sales volume and revenue from the newly acquired Aqua Farm Chemicals business.

- Consolidated EBITDA grew 15% year-on-year to rupees 328 crore. Profit before tax (PBT) stood at rupees 124 crore and profit after tax (PAT) at 93 crore.

- EBITDA per ton in the carbon black business was rupees 19,868. Total carbon black sales volume was 144,000 tons, representing a capacity utilization of over 90%. Domestic sales volume was 84,369 tons and international sales volume was 59,230 tons.

- Aqua Farm Chemicals reported steady performance, with revenue of rupees 328 crore and an operating EBITDA of rupees 51 crore. Sales volume stood at 23,000 tons.

Margin Guidance

- The company expects strong growth in both sales volume and operating margins in the remaining quarters of the financial year.

- Management expects the EBITDA per ton to remain stable going forward, with some potential for improvement due to the shift in product mix towards specialty products.

Business Segment Performance

- Carbon Black: The carbon black business saw a drop in realization on a quarter-on-quarter basis due to a decline in crude oil prices and a change in product mix. Crude oil derivatives are the principal raw material. Export volumes increased year-on-year but sequentially slowed down due to macro headwinds and customer destocking.

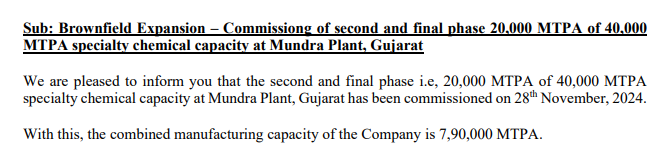

- Specialty Carbon Black: The company recently commissioned a new specialty carbon black line with a capacity of 20,000 tons per annum in Mundra. It has also begun work on another specialty line in Palej, which will cater to applications in conductive polymers and batteries. The company is expanding its specialty carbon black portfolio to move up the value chain and expects to see decent margin growth in this segment over the next 2 to 4 years.

- Aqua Farm Chemicals: Aqua Farm Chemicals faced headwinds from muted demand and stiff competition from China. The company is focusing on cost and operational efficiencies, increasing market penetration, and expanding its product portfolio. Management expects the business to deliver better performance going forward and to reach the profitability levels it was at before the acquisition by Q4 FY26.

Management Guidance

- Capacity Expansion: The company is undertaking a brownfield expansion of 30,000 tons in Tamil Nadu, which is expected to be operational soon. It has also started the second phase of expansion of 60,000 tons and 12 megawatts of green power in Tamil Nadu. The Andhra Pradesh government recently allocated 116 acres of land in Naidupeta for a greenfield expansion. This will be the company’s sixth manufacturing site and is expected to help the company cross the 1 million ton capacity benchmark.

- Debt Reduction: The company’s net borrowing increased by around rupees 980 crore in the quarter, mainly due to inventory accumulation. The company is focusing on repaying the debt it incurred for the acquisition of Aqua Farm Chemicals. It expects its overall borrowing cost to come down by at least 3% to 4%, with a quarterly reduction in finance costs of rupees 5 to 6 crore going forward.

- Nano Silica Project: The company has started placing orders for equipment for the pilot plant and expects commissioning to happen in the next few months. Commercial production is expected to start in 2027.

Key Risks

- Geopolitical Risks and Crude Oil Prices: The ongoing geopolitical situation and its impact on crude oil prices is a key risk for the company. Crude oil price fluctuations can impact margins as the company operates largely on formula pricing, which allows for variable cost pass-through.

- Competition: Stiff competition from Chinese players in the specialty chemicals segment, particularly in Aqua Farm Chemicals, is another risk factor.

- Slowdown in Demand: The risk of a slowdown in the global economy, particularly in Europe and North America, could impact demand for the company’s products.

- Inventory Levels: High inventory levels in the industry can impact demand and pricing.

- Currency Fluctuations: Although the company hedges its currency exposure, fluctuations in the dollar-rupee exchange rate can still impact profitability.

Industry Outlook

- The tire industry outlook in India and globally remains positive, with growth driven by investments in road infrastructure, rising income levels, increasing urbanization, and premiumization.

- The global aqua farm chemicals market is expected to grow at a rate of 1.5% to 2% annually.

Overall, PCBL Chemical Limited reported a steady performance in Q3 FY25 despite a challenging macro environment. The company is undertaking capacity expansions and focusing on improving profitability in its various business segments. It expects strong growth in both sales volume and operating margins in the coming quarters.

Disc: Invested

9 Likes