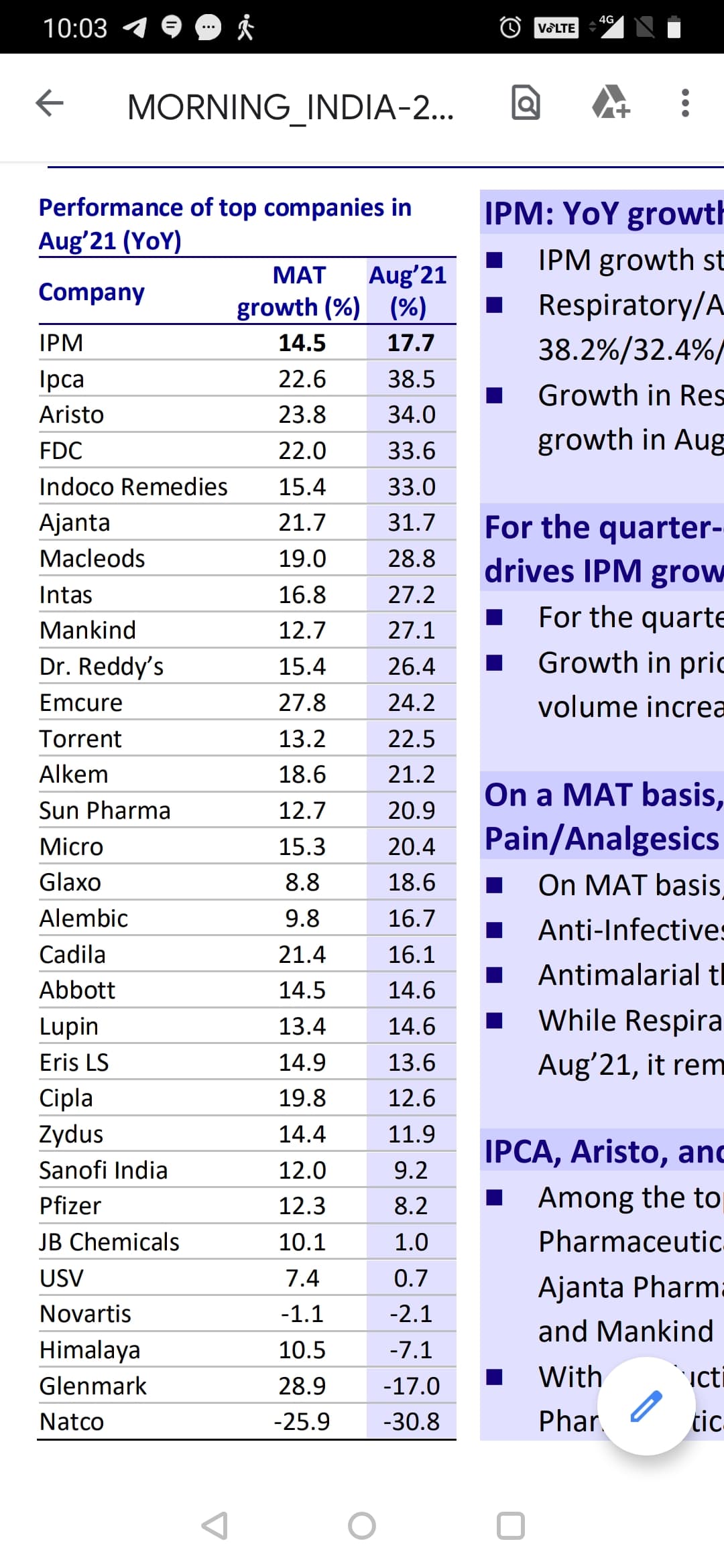

Domestic Pharma growth for August ![]()

12 Likes

hello sir , if possible please share enitire report, thanks in advance.

Motilal Oswal - Healthcare

https://vid.investmentguruindia.com/report/2021/September/PHARMA-20210903-MOSL-SU-PG060.pdf

7 Likes

We have a very good news of Mosquirix approved by WHO.

" Despite its approval for use, it is only 30% effective at preventing severe cases, requires four doses and the protection it gives fades after a few months. Although side effects are rare, they could include fever and convulsions."

2 Likes

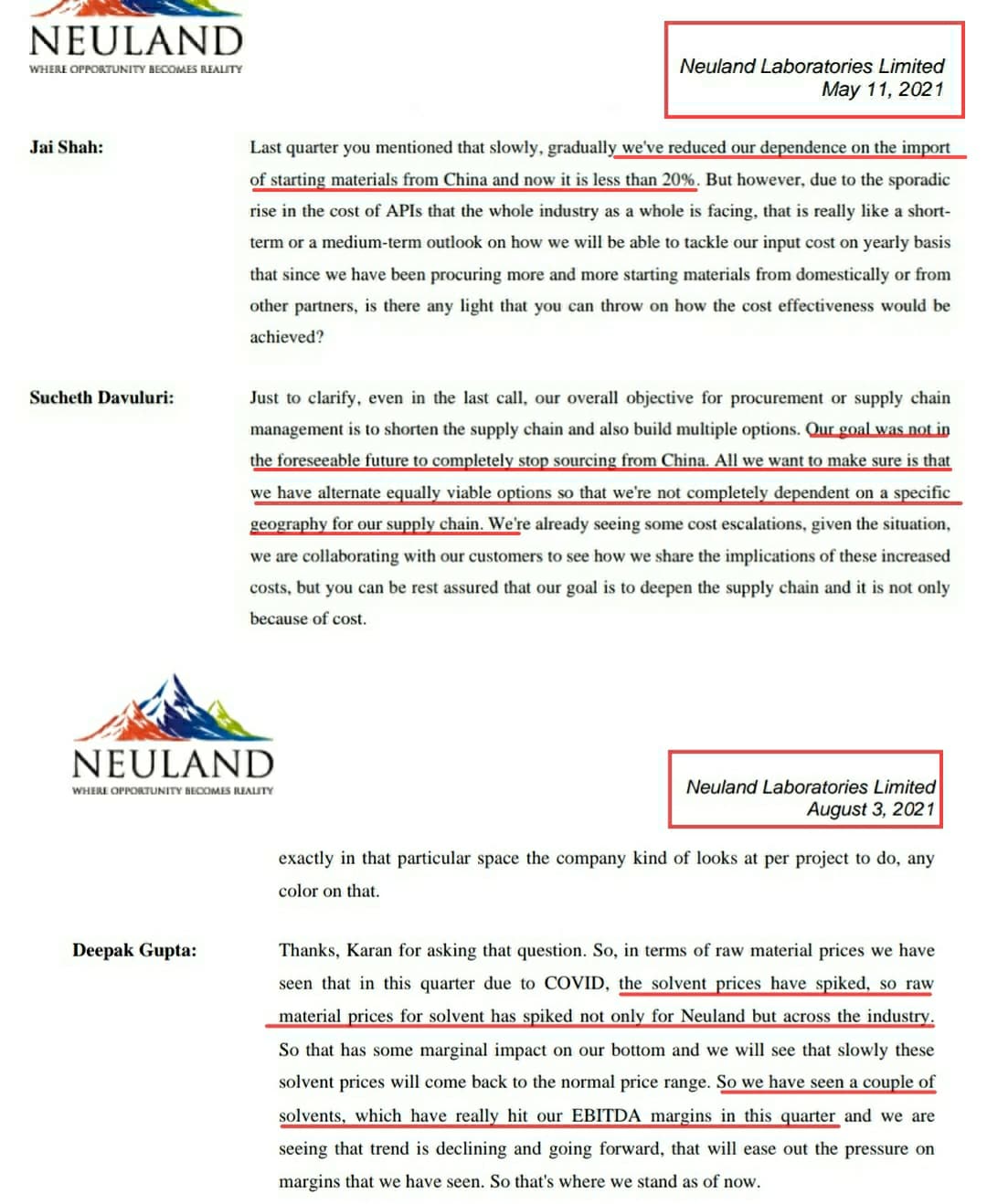

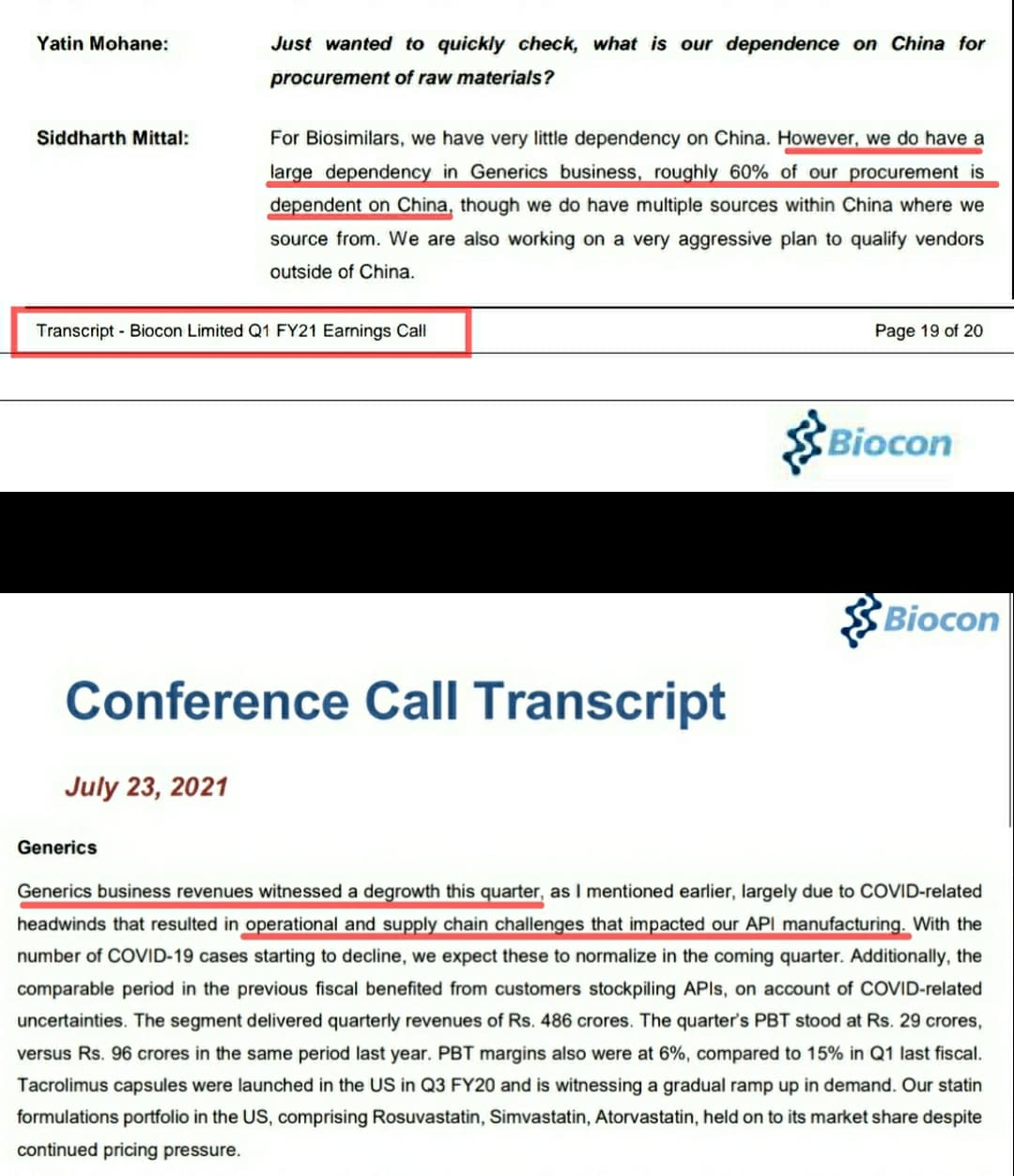

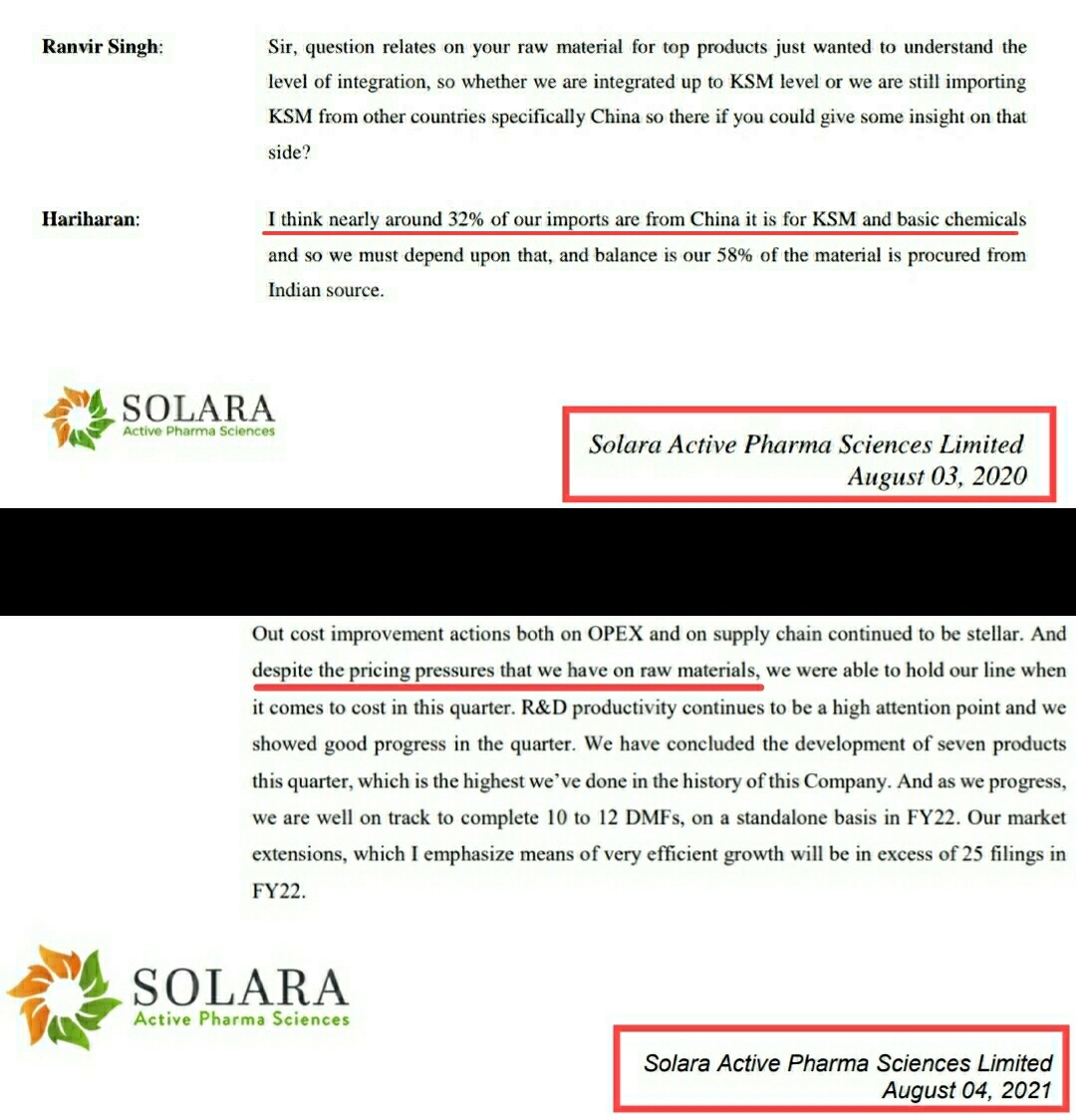

China’s power crisis has caused rise in price of intermediate chemicals and key starting materials. Pharma players who are dependent on China for raw materials will see rise in input costs and subsequently margin contraction can happen in coming quarters as they can’t pass down the cost in a short period of time.

I’ve analysed conference calls of few players and I’m sharing that here.

Supply chain disruptions, higher freight charges and rise in raw material prices were already there on Q2. I believe, China’s power crisis may aggravate the problem.

If anyone have other opinion or something to add, kindly share.

24 Likes

Dr Saheb This guy has the data and said clearly how it will affect. But the bottom line is it is a short term phenomenon. Long term investors need not worry about it. Use the dip to make some attractive buys/additions. Pharma so far defensive has become dynamic now with so many things happening on so many fronts. One needs to choose the picks very smart.

In all your images posted above, everybody talks about supply from China. Nobody talks about supply to China. Is it possible to find out those companies .

It might be a short term phenomenon. Over dependency on China for raw materials is always a risk, I believe. We should closely watch how each company mitigate this impact. How a company responds to a challenge will tell us about their culture. At the end of the day, one needs to pick the right ones based on their conviction. (Yes, current situation ‘may’ offer a buying opportunity)

CNBC interview

SuvenPharma is in focus today as its input costs have surged in the past month due to the China power outage. @_soniashenoy & @SurabhiUpadhyay speak to CMD Venkat Jasti who says that margin could be impacted by 5-7% due to high input costs. @ekta_batra https://twitter.com/CNBCTV18News/status/1446313668774285320/video/1

2 Likes

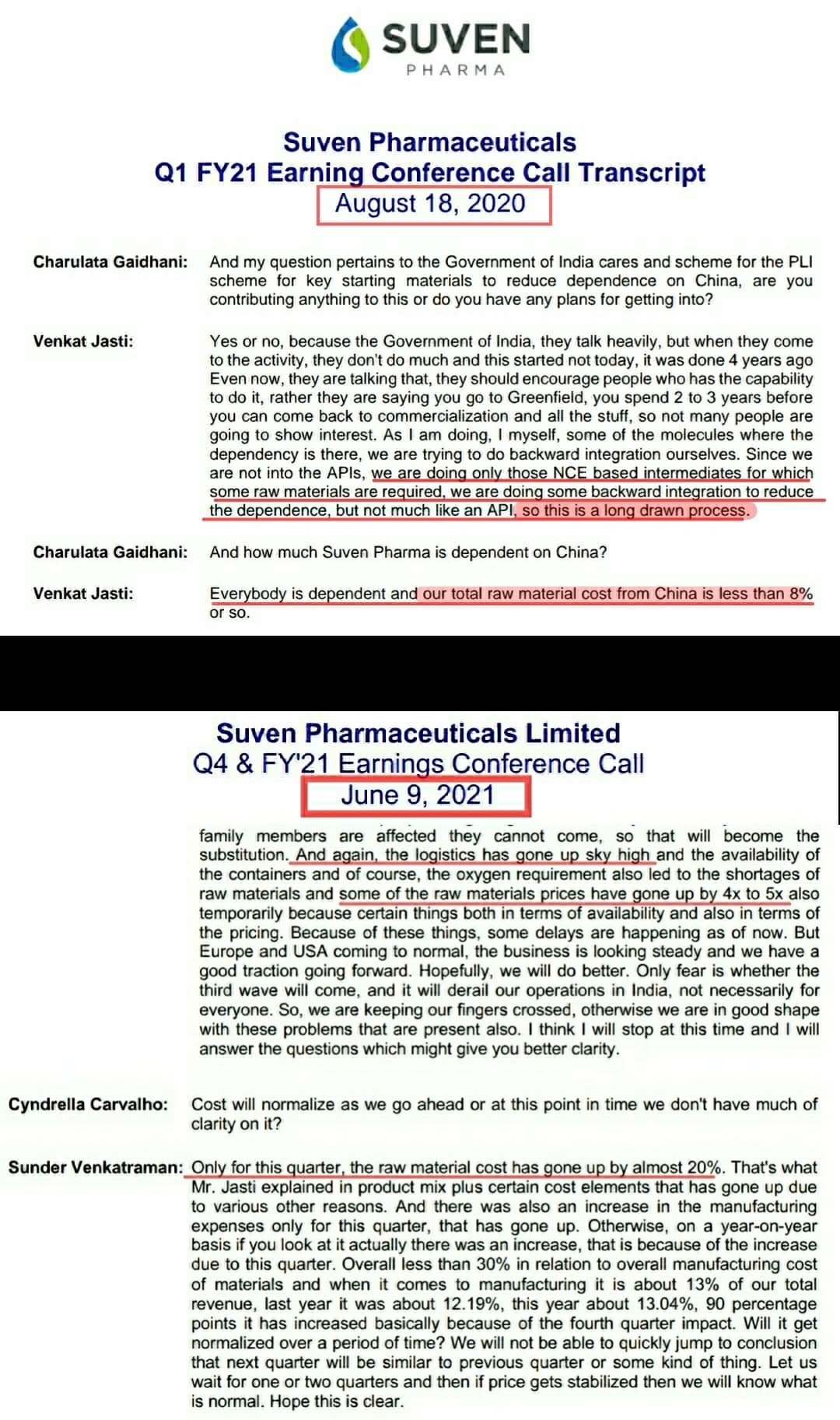

Suven pharma with 8% dependency on China for raw materials is commenting that they are expecting 5-7% margin contraction. Then what will be the scenario for other players with much high dependency? (He also says some of the raw material prices have gone 6x). I don’t think this has already priced in for many players.

Suven management is more worried about delays in executing their commitments to clients and maintaining their credibility than margin contraction. They are willing to suffer, but not willing to lose their credibility.

3 Likes

It is the only stock which shows resilience and as per my system it is a BO now and I have added. But we can only have a macro picture unless we have a clear data . What is the impact of this 8% ( though we assume it is less as compared to others) on earnings we can never know. It can be 8% but impact can be huge if volumes are huge. This is where studying PA comes handy. Limitation of data and analysis compensated by TA.

2 Likes

Dependence on Chinese Raw Material:

- Hikal- 35%

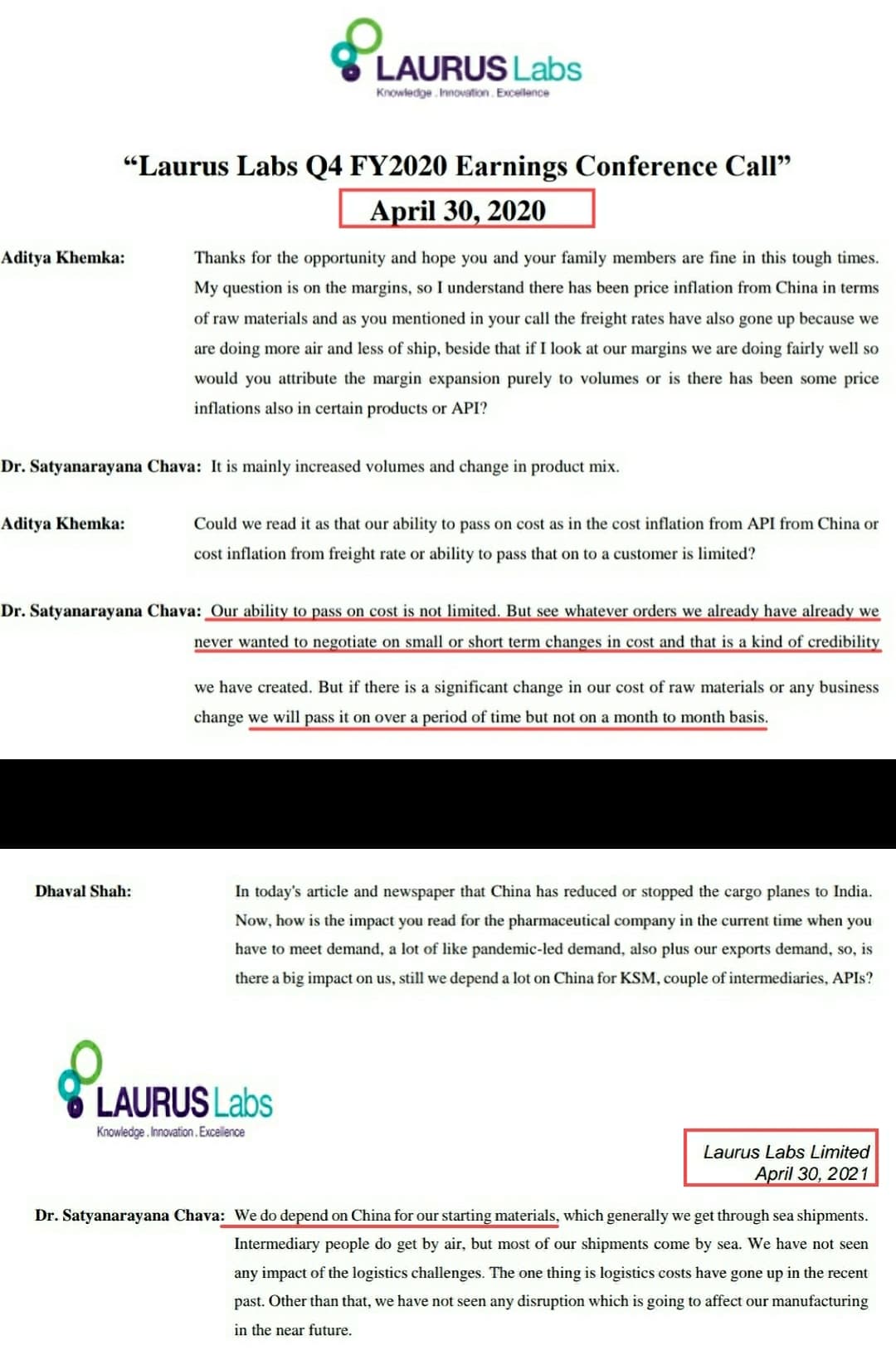

- Laurus-60%+

- Solara- 30%

- Granules-30%+

- Neuland- 20%

- Pi industries- less than 10%

- Suven Pharma- Expecting 5-7% hit on the margins

- Piramal Pharma: 15%

29 Likes

Would be helpful if you can share the source of your data.

1 Like

1 Like

Industry ANDA approvals list:

1 Like

I think any generic company that is doing business in the regulated market can’t make better margins.

- Business in US is not branded, one is at the mercy of the big distributors

- Due to this too much price erosion, only time they have some joy is when someone is first to file and have 90 exclusivity period. If the innovator decides let me sell at the same price after expiry then even this advantage is also gone

- Too much competition between companies in india, all are trying to launch the same generic (recent example Molnuprivar, Revlimid etc… )

- Some are claiming bio-similars and all, biologic innovator itself are selling at the price of bio similar (remind you unlike synthetic drugs biosimilars are not exact replica ) after the patent expiry , the cost of producing biosimilar is very high and approval period also very high

- Generic companies always have to innovate and the costs of getting approval of FDA etc… are very high .

- Another threat is china, they are now getting into the next level of generics (biologics)

- I think domestic pharma is the good space to play compared to export

4 Likes