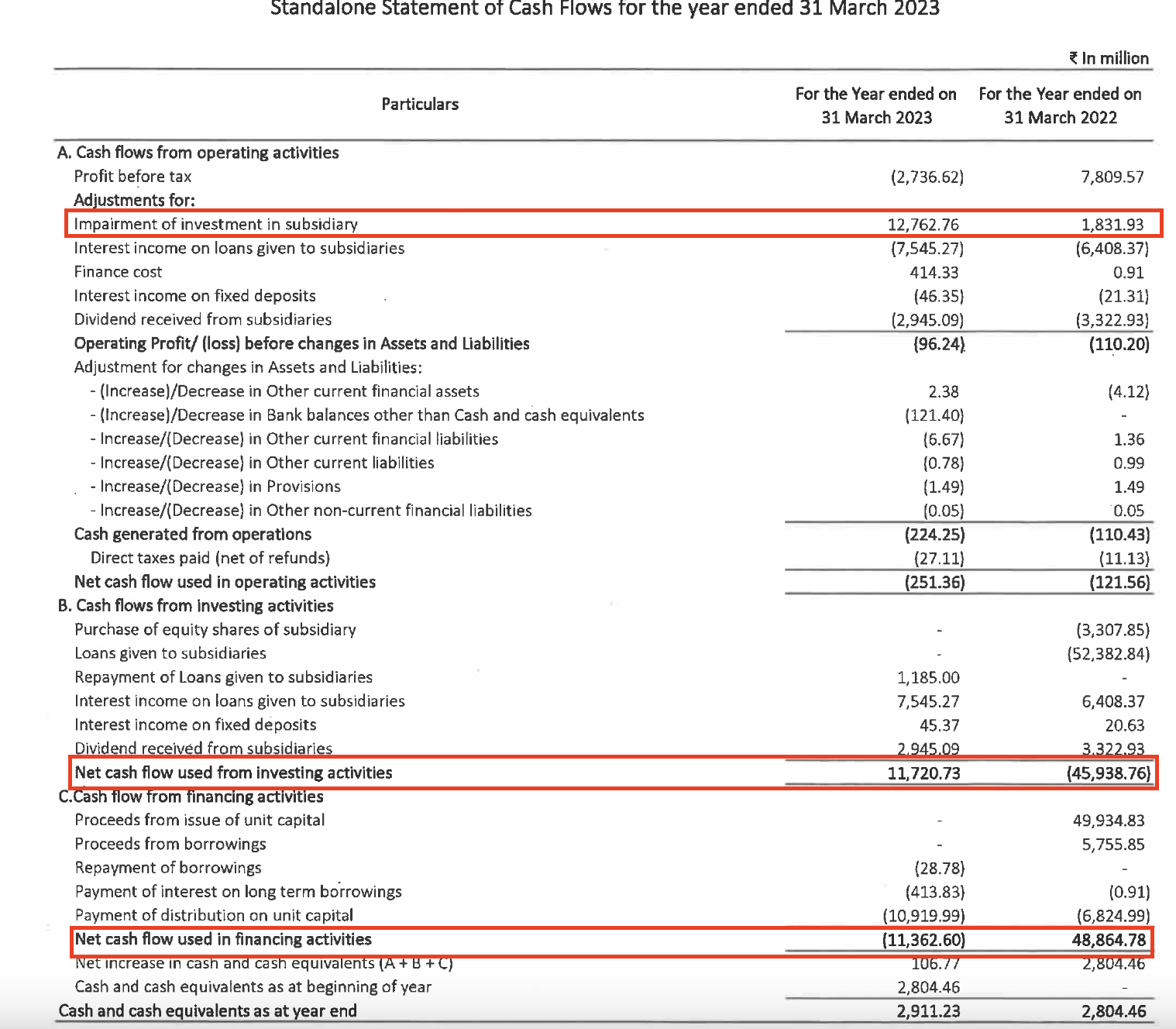

I have difficulties in understanding the cash flow statement of PGINVIT.

The item “Impairment of investments in subsidiary” seems to be extremely high compared to last year. How do we know what led to this and in which subsidiary?

Do the numbers inside brackets like (11362.6) mean negative values?

In spite of the huge impairment, we still see the cash flow is positive and better than last year. Is my understanding correct that (45938.75) invested last year is an outflow of cash and this has given returns, a positive inflow of 11720.73 in 2023?

All REITS/INVITS undergo a periodic exercise to determine the net asset value of their underlying investments in subsidiaries. Whenever there is a difference between the asset value on the balance sheet and the likely future cash flows the asset value gets revised and possibly there is impairment.

This is similar to depreciation, the difference being depreciation is more predictable and regular

https://www.pginvit.in/uploads/65d94e0b-bee6-42f2-b39b-1513880a91f6/Financial_Results_31.03.2023.pdf

If you see page 18 of the annual report you will notice impairment has been done across the board for all assets in PGINVIT. This could be a one off exercise and may not happen every year. Current cashflow will get a boost as impairment is a non cash activity (it should be balanced out in the balance sheet and income statement). However would be good to keep in mind the potential of future cash flows from these assets. Hope this helps

However , i have a small question to ask , i.e what is the future scope of this INVIT i mean will there be only 5-6 transmissions lines in the future or will Powergrid will win and then allocate to this invit ?

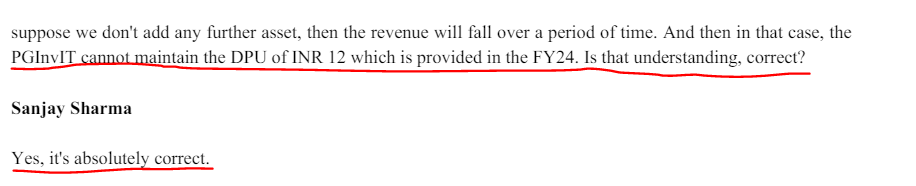

Why do you think its not sustainable given the current assets. Where will the money leak? the price of transmission will escalate with inflation if it not already built into the pricing. Secondly, even if they dont escalate Rs 12 dividend looks steady unless management says so. Last quarter the management had to dig in about few paisa ( i believe they took 10-15 paisa from reserve to meet their stated Rs 3 per quarter goal). I dont think management is smart in quoting a yield ahead of time when so many variables could impact cost. They should instead talk about long term PPAs etc so that investors get visibility into future cashflows.

As i see it, its a good place to park cash and get 9-12% yield and if govt bond rates go down then this stock will rally as it provides a much higher yield. So if govt rates stay put u get paid a good yield but if govt rates fall u get capital appreciation too.

Management quality is good since these are PowerGrid guys with experience. Holding for 20-25% gain in capital while collecting 12% yield.

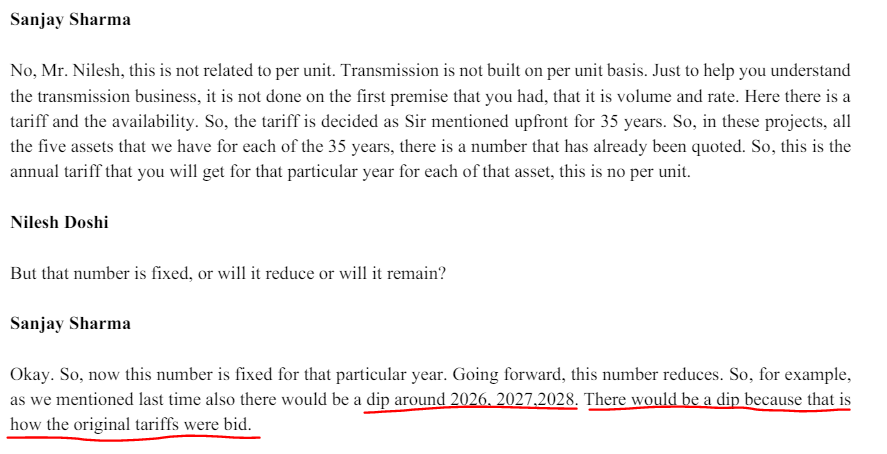

There is a significant dip in revenues from FY 28 and same is available in the valuation report . Although management confirmed Rs 3 quarterly distribution for current FY but they indicated some dip in next year. Acquisition of balance 25 percent from Power Grid for 4 balance assets is also not going to contribute much to distribution. Conservative commentary by PSU employees and no enthusiasm for other asset additions has led to gradual decline from 130 levels. Investors who invested at those levels have already seen significant capital depreciation with only solace of 3rs quarterly distribution.

I am watching the scrip for last one year and looking for an entry and current yield is luring but risk of capital depreciation is keeping me at bay. Looking for initiating position from 95 levels and increasing one every fall as these yields for AAA rated govt instrument is already at lucrative levels .

with transmission invit the problem is capital will not be returned back on expiry (30-40 years), if you take that into consideration then its not great yield 12%.

Respectfully disagree. Most of the projects are awarded on BOOM basis - Build, Own, Operate and Maintain. Even at the end of the contract period, ownership is not an issue - only the O&M comes up for fresh tendering. This has been clarified by IndiGrid management in multiple concalls - perpetual ownership.

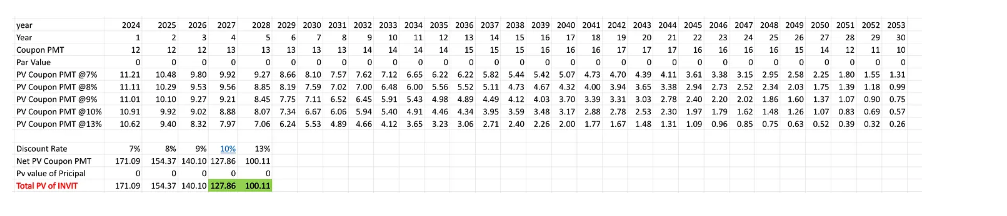

Even if the capital is not returned back (which is not the fact as rightly pointed out by @Rezang_La), the corpus that will get accumulated by reinvesting the distribution amount (Rs 3 per quarter) will be Rs 3110 for a single share of PGINVIT with permanent loss of capital which is Rs 100.

If Rs 100 investment has to transform to Rs 3110 in 30 yrs, RoI CAGR is 12.14%. In spite of a total permanent capital loss, the 0.14% additional CAGR is available due to quarterly return of Rs 3 and not annual return of Rs 12.

So how does it matter whether company return the initial investment or not ?

In this calculation made in dhruva.substack.com, it is assumed that DPU per year is Rs12 till 2026 and Rs13 between 2027 and 2031 and increases so on till 2044 upto Rs17.

But reality is that the revenue and hence DPU decreases due to the way the tariff was bid and agreed upon initially. Even if it is very small decrease, that is sufficient to alter the overall CAGR.

I have huge investment in PGINvit, assuming that it will continue to manage 2.5-3.5% more than FD returns (10-11% pre-tax yield) for the next 25 years (Assuming, yield can decrease only due to interest rate/inflation going down) but now looking at this management comment, i think i should review the weightage in this stock especially when we do not see any fresh asset acquisition and we do not know how much the DPU is going to dip due to this tariff change not in line with inflation in that given year.

Any one has any idea about this dip in DPU due to tariff bid factor?

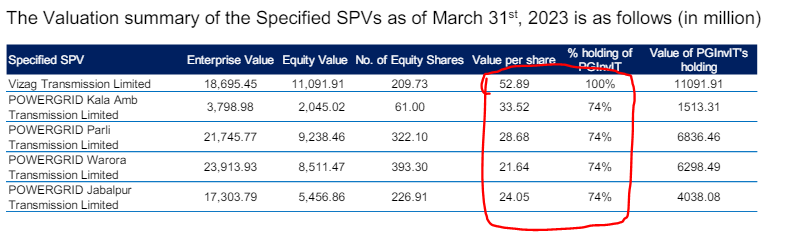

Also it would be worthwhile looking at latest valuation report from NAV perspective. If no new assets are added, theoretically NAV is what one can expect to get. One hopes NAV calculation makes realistic assumptions. Typically these reports end up making optimistic assumptions.

Not sure that depicts the right NAV. One would need to total the equity share of pginvit for each of the assets and then divide that by number of units i.e. total of last column in the table above. I think that should give a different number.