As per value of PGInvIT’s equity holding, Total value = 11091+1513+6836+6298+4038 = 29776 millions = 2977 Cr.

NAV/share = 2977/91 = Rs 32

And thats wrong. I think both the methods are wrong.

As I remember that there is significant dip in revenue from 2027(around 20-25 %) and same can be checked in this year valuation report. I dropped my investment plan considering Indo Grid a better option for long run. Power Grid also doesn’t have much plans to monetise assets via PGInvit . Market already punished PG Invit from 130 to 95 levels and I may get interested if price drops to 80 levels.

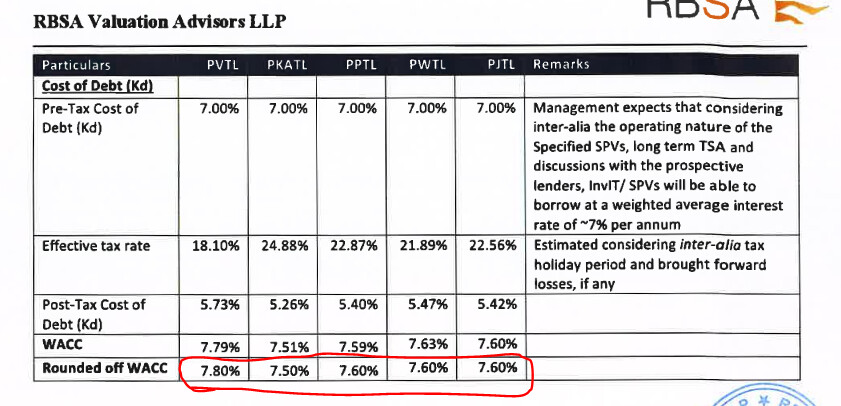

But WACC (cost of capital) is taken as 8.85% in sep-2023 valuation. It appears WACC changes with respect to REPO rate. In 2021-22, WACC was 7.6%

If WACC is 7.5% due to repo rate reducing by 1.3% anytime in the next 3 years (high probable event), the share price can stay at Rs100 even if DPU reduces by 15-20% to Rs10 p.a. This must be considered while investing in PGInvIT.

I too think that asset monetization should be considered as a bonus and not something that can be taken for granted.

3 Likes

Enterprise value of pginvit is 84.7 billion rs per latest presentation - slide 5. That would mean NAV of around 93 with around 91 cr units. With no additional asset acquisition in sight, likely optimistic nature of these valuation reports and wacc numbers being what they are, this should be quoting well below NAV to have a margin of safety. Looking at current yield could be myopic IMHO

2 Likes

Strictly speaking, it does not matter what the valuation report states about its NAV. The returns from PGINVIT is obtained from its distribution and not from its NAV. The REPO rate of 6.5% looks like peaking since the last time it was above 6.5% was in 2015 (9 yrs ago). So even now, the pre-tax yield of 12% is significantly higher. When rates come down to nominal 5%, even if distribution comes down by 20%, still PGnvIT gives a 2% yield higher than other risk-free investments.

It depends upon the investor’s perspective. Does one approach PGInvIT as a equity or a bond ? I view it as a high yield bond and IMHO, its already below its intrinsic value (Rs100-110).

3 Likes

PGINVIT definitely till the time they are able to give 12/- yearly payout, is a value buy for an alternative stable income. The day rates start decreasing from RBI, the pre-tax yield will be even more lucrative.

Yes, other valuable boarders have mentioned, the delay in new acquisition is a challenge to keep on servicing 12/- payout, but this should happen sooner or later, is what the situation seem to hinge upon.

The promoter Power Grid is currently not willing to transfer any assets and currently getting money for more work is not a challenge. But this will happen as GoI will be there to take some call, even GAIL has denied to launch pipeline InvIT which GoI was willing to come up and this also seems to be in cold box.

However would like draw the attention that Powergrid lines are not only pure play of power transmissions but also for telecommunications. OPGW can be a dark horse for all transmission lines asset valuation increase and it can increase the valuation substantially. Power Grid and INVIT both have this and this should give some trigger in near future as currently management has also not spoken much about in public for OPGW ability. The high voltage lines surely have it as it helps in decreasing power losses, signals travel more distances without repeaters requirement and they act as sensors to detect any fault in lines, in fact can act as shield for lightning strikes. Companies, Govt etc use OPGW for their own purposes for last mile connectivity and speed enhancements and companies like power grid can sell there spare capacity to these institutions, generating some value out of it.

This is no way a cover up for the delay in assets acquisition but more of a structural theory that their payout could sustain 12/- till FY25-26, however, post that serious acquisition only can help for regular payouts. INDIGRID INVIT is better placed currently in terms of types of assets and the size of assets, so buying a mix of both of these would be better for visibility of stable pay-out, not for capital appreciation though. I

6 Likes

Looks like this quarter PGINVIT is not planning on keeping a conf call. I don’t think they will have one unless they get an acquisition. Any thoughts on this?

Not sure if still it could be seen as pattern. Haven’t seen latest investor ppt of India Grid as well. AGM held few days back. So possible.

But mgmt must be aware of potential Qs around acquisitions. If the trend continues next Qtr, then will take fresh view. Being Govt backed, complacency expected but difficult to comprehend as PSUs have been very aggressive from past 2-3 years. Need to keep track

INDIGRID has already uploaded investors ppt and also completed the investors call.

Then I have missed it, to be honest.

I’m not that particular for these developments every Qtr for Invit & REITS. Thank you for highlighting this.

But I’ll still hold same view for 3-4 qtrs or if mgmt gives clear sign, payout will be difficult. It could be trigger in fact for promoter to then sell assets.

Yes… Management is fed up with acquisition and drop in distribution post-FY26 queries which they have clarified many time. Right now, mgmt & investors can only wait. So they may rightly opt for skipping concall.

1 Like

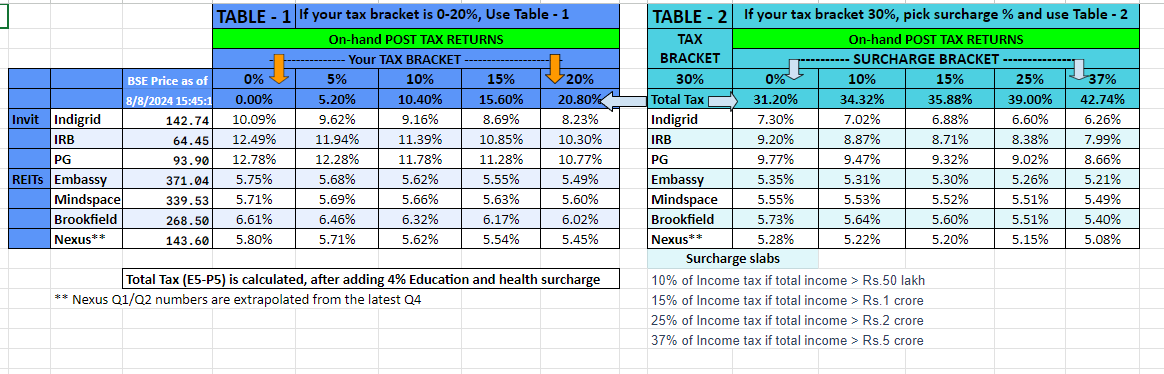

The yield table below gives the values, if you had bought at closing price of today 8/8 (all the Q1 numbers are updated to reflect the latest DPU additions…as always, I calculate these based on running 4 Qtr numbers

6 Likes

Investors dont care even if DPU falls to 10 in FY26 temporarily but the worrying factor is the attitude of management/GoI. For the past 2-3 years, no attempt to acquire and it looks like aquisition can not happen for the next 1.5 yr. Thats totally 4 yrs of no performance at all. They have conceived this idea of PGINVIT and its their responsibility to maintain a post-tax return of 9% (DPU > 11%) for investors. Else it is sheer mismanagement.

6 Likes

The CFO’s statement regarding exploring the new opportunities available in the sector is baffling.

If the top management is so scared of a well penetrated and proven technology like solar energy that is successfully implemented in most of the California, these guys are not good enough.

they dont need to do any adjacency to their existing business model of transmission for higher DPU - instead of doing nothing and twiddling thumb and collecting a salary, they need to go after state level transmission projects and push for govt to monetize sponsor Powegrid assets-when they came to market govt did have plan for asset monetization- voume of transmission projects next 5 years in ~150 lac crores

2 Likes

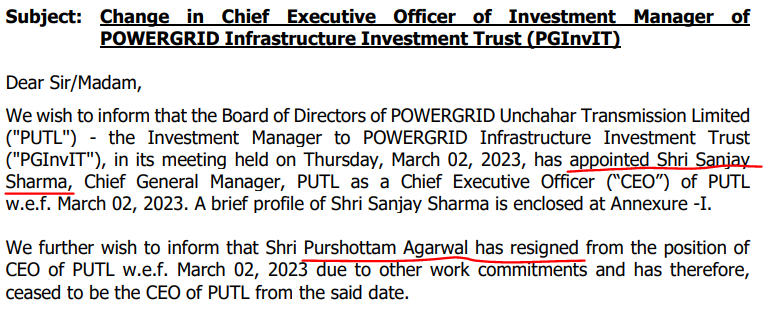

On that note, this could be a positive news as PGINVIT now has a new CEO:

https://www.pginvit.in/uploads/7de9a137-afda-422d-b380-10ada36ffeaf/INTIMATION.pdf

The new CEO, Smt Neela Das seems to be having 32 years of work experience at Powergrid.

Fingers crossed. I hope this could be the turning point for PGINVIT.

3 Likes

This is a no event. PGINVIT has changed the CEO every year since 2022. I think these are dummy roles.

1 Like

Has anyone got any idea, if they are really talking to state Transcos for acquisition of their assets ?

It’s a strange situation where in the sponsor (PG) has lost interest in invit route and thrown baby (PGinvit )out of the bath tub just after the birth (IPO ) . PG has adopted securitization route instead of Invit and unitholders are left to the mercy of junior babus of PG who rotate as senior management position in PGinvit! If boss (top leadership at PG) has lost interest in invit then it’s just a vacation posting for junior guys who rejuvenate by their stay in invit and once reenergised go back to parent company for productive service…

I don’t see any real hardwork and efforts these stop-gap management at invit are doing for AUM growth.

Now they have stopped concalls also, so no pressure of answerability to unitholders.

Disc: invested.

3 Likes

@praveen_sham I mailed PGInvit regarding concall. Their response as follows.

"Regarding the earnings call, we would like to inform you that the Annual Meeting (AM) was held on 26th June 2024, where investor queries were addressed. Given the short time difference between the AM, the quarter ending, and the release of results, an earnings call was not conducted. While it is not mandatory to hold an earnings call every quarter, we have consistently conducted them each quarter. Once the next earnings call is scheduled, the information will be disclosed on our website and through stock exchanges for the public at large.

As for our growth strategy, we are actively pursuing acquisition opportunities for operational power transmission assets. However, it is important to note that the availability of such assets from private developers is currently limited. The adoption of the Government of India’s guidelines for asset monetization by state entities is expected to be a gradual process due to the novelty of the proposed mechanisms and the complexities involved in their implementation. We are in continuous touch with the Government authorities on the issue and updates shall be provided to the unit holders as an when the clarity emerges on the subject."

5 Likes

Thanks @sambandham82 for sharing the email. It’s really valuable.

Now, The moot question is : Why and how IndiGrid is able to garner assets after assets in the same ecosystem ?

Is it because IndiGrid is managed by KKR (PE giant) which are more agile and dynamic vs sloppy PGInvit management?

Also, it should be very helpful, if someone can enlighten as to which state governments and private parties PGinvit is actively talking to and how close they are in closing the deal?