This business has very low margin and only 50cr investment they are doing. Just a assembly business. High volume low margin business.

Valuations should lower

This is high asset turn vertical, they can get almost ~ 10x asset turn. Even though this vertical going to contribute 400-500 Cr to the top line, existing verticals demand could be huge going forward.

IT Hardware business may contribute good chunk once its kick in as Avg price of the unit would be high like RAC. We may get some clarity in few quarters on hardware PLI

4 Likes

PGEL subsidiary was approved for the PLI scheme investment.

2 Likes

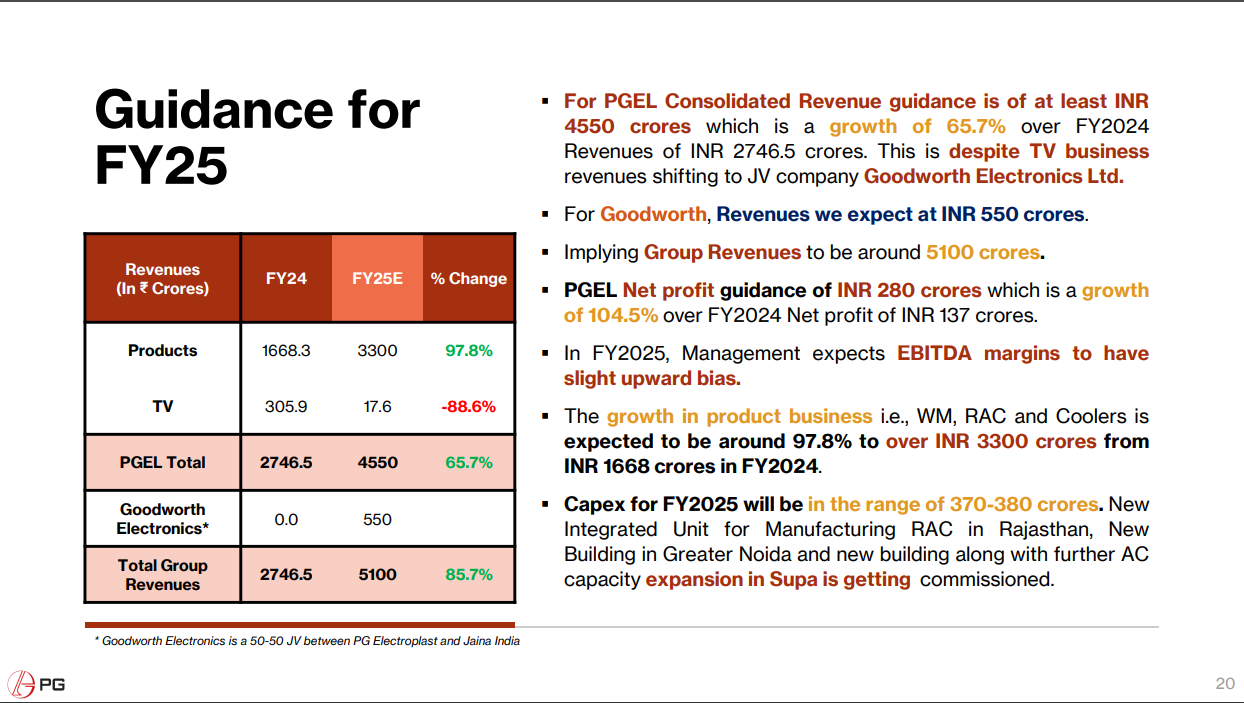

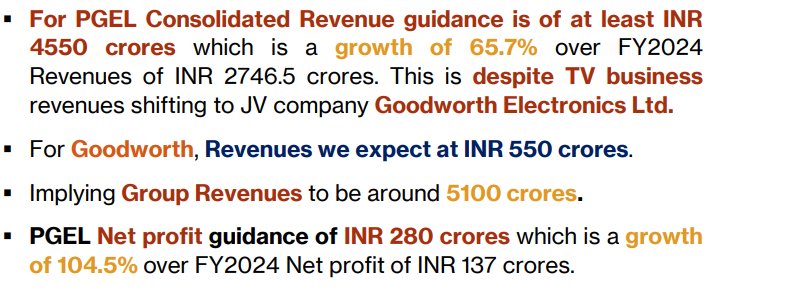

PG Electroplast (PGEL) – FY25 Guidance

- Revenue Target: ₹4,550 Cr (+65.7% YoY); Group revenue at ₹5,100 Cr (+85.7% YoY)

- Net Profit Target: ₹280 Cr (+104.5% YoY)

- EBITDA Margins: Slight upward bias expected

- Product Business Growth: ₹3,300 Cr (+97.8% YoY)

- Capex: ₹370-380 Cr for RAC unit (Rajasthan), Greater Noida expansion, AC capacity in Supa

- TV Business Shifted to JV with Goodworth Electronics (₹550 Cr revenue expected)

13 Likes

PG Electroplast | Management Interview

- Management said to maintain growth rate of 30-35% over the next few years

- Will announce agreement for manufacturing RAC compressors soon, 60% of these compressors will be used captively

Watch here

3 Likes

The company’s sales for the first nine months are ₹2,960 crores, with a net profit of ₹143 crores. They are providing a sales guidance of ₹5,100 crores and a net profit guidance of ₹280 crores for the full year. This implies they are expecting sales of ₹2,140 crores and a net profit of ₹137 crores in the final quarter. Don’t you guys think this is too optimistic? Instead of setting high targets and potentially falling short, shouldn’t the company provide more conservative targets and then overachieve?

Falling short of the guidance could raise unnecessary questions and potentially have a negative impact on the share price.

7 Likes

This 30 cr PLI benifit was included in earlier guidance also, revision in PAT guidance is purely based on improvement in business (early offtake of AC season)

2 Likes

In FY28 PLI benefit will peak at 60 Cr for existing facilities and it will become Zero in FY29 .

Request to all investors to make a note of this. In the meantime they may get eligibility for some more new capex but it may not be significant amount like 60 Cr . We may see some dip in PAT in FY29.

4 Likes

Q3FY25 Concall short notes::

- Rev: 82%, EPS: 89% (YoY)

- FY25 - Rev: 4550+550 cr, PAT: 280cr (Revised Upwards)

- Thinking of backward integration in compressor manufacturing.

- Goodworth Electronics (TV Joint Venture) in loss (1 to 2% Profit expected in FY26)

- Mutual Funds increased from 3.7% to 10.5% (Source: Tickertape)

5 Likes

3 yr cumulative operating cash is just 153 cr.

Operating cash to price is 175 X ! Doesn’t already priced heavily.

1 Like

Markets are surprising, classic case of over valuation.

1 Like

Imho ..it had not been overvalued till now and has grown enough to justify it ..

At the present moment , its certainly not cheap but if it continues its growth rate ..its not very overvalued either .

Had bought some at around 250 and sold all around 625 thinking it has run up too much too quickly..but it has proven me wrong . Even during the bearish phase in markets in Q4, it did not go or stay below 700 for long.

The scope of growing the business is huge for these companies and markets are likely paying for it .Considering Kayness and Dixon , its better to say not my cup of tea than to say it is overvalued .

Disc. Not invested in it and not buying above 750.

3 Likes

I entered kaynes around 2000, over the last few months overvaluation was the meme going around so called overvalue stocks. Guess what kaynes P/E inspite of correction never went below 100 and it has moved about 80% from that point. Look at P/B of bajaj finance / HDFC bank / supreme industries etc. in its high growth years. Analogy is difference between a merc and a maruti. For a high growing company like pgel, kaynes, if one looks at value it is a futile approach and many will miss a big potential wealth creator. Selling early because of valuation is a big mistake as long as other parameters like growth, TAM, corp. governance are in place. I have heard from several big investors about mistake of selling early. Titan has been over value since years yet sir late RJ held it and we all know what profound impact it had on his wealth. It is the relative thinking and looking at many data points which helps. It is never linear thinking

7 Likes

Now they are targeting 30-35% growth over the next 2-3 years, Making 100% is not possible anymore as base is very high as of now

1 Like

Very correct. One should stick to one’s own conviction. After all it is your own money. Sometimes market cacophony affects sentiment, especially in downturns. At such junctures it is essential to stay calm. I missed out Kaynes recently due to this factor and learnt a lesson. Good stocks are rarely available cheap and you should grab whenever they give opportunity.

4 Likes

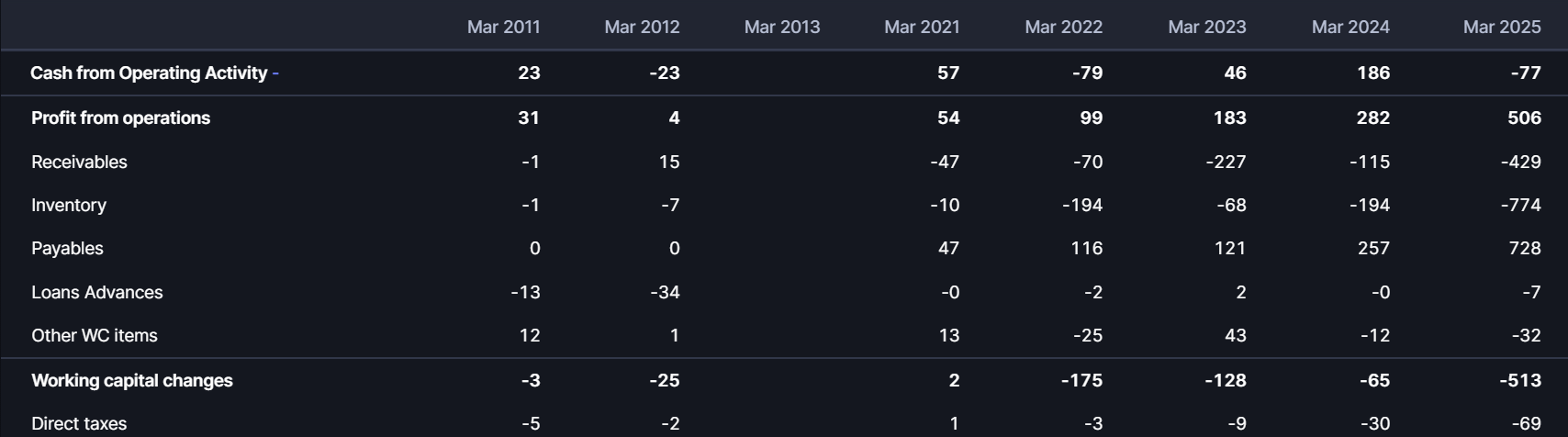

PGEL Q4 results seems awesome. Though CFO is negative due to high Receivables and Inventory

2 Likes

What concerns me is their payables, they are also very high… Maybe I am just overly cautious on the debt part now

I think if we consider 405cr PAT it comes out at 60 PE on FY26 fwd basis which seems reasonable for 30%+ growth engine. AC Compressor manufacturing might also bring some backward integration benefits and slight improvement in margins. Refrigerator business is a bonus. Overall outlook seems good.

3 Likes