- PG Electroplast Limited targeting 46% growth in group operating revenue for the next financial year.

- Company aims for a consolidated net profit of at least INR 200 crores.

- Anticipated 44% growth in the product business for the upcoming financial year.

- Focus on developing cost and product leadership for room ACs and washing machines.

- JV partnership established with Goodworth Electronics for TV and hardware business.

- Jaina Investments close to INR 6 crores invested in the TV business, potential additional INR 5-6 crores.

- Jaina provides sourcing capabilities and credit from Chinese vendors for TV kits.

- Potential update on IT hardware PLI orders post-election mentioned.

- Plastic molding margin at 7.5% and electronics at 2%, driving growth in the product business.

- Expected turnover of INR 2400 crores in the product business for the next year.

- Seasonality shifted, with RAC business starting late January and extending to late June.

- Actively engaged in discussions with clients for new products and opportunities.

- High interest in RFQ and RFP.

- Capex set at around INR 370-380 crores for infrastructure development.

- Optimistic outlook for revenue growth in ACs, washing machines, and new categories.

- ROCE target set between 15-16% pre-tax for new projects.

- No immediate plans for high-margin, low-volume businesses like aerospace.

- Aiming for a slight improvement in pre-tax ROC E of about 20%.

- Emphasis on growth and seasonality influencing the target of achieving a 25-26% ROC E by FY '26 or '27.

- Cash balance of about INR 180 crores and a gross debt of INR 360 crores reported by PG Electroplast Limited.

6 Likes

PG Electroplast Ltd

PGEL (established in 1977) specializes in Original Design Manufacturing (ODM), Original Equipment Manufacturing (OEM) and Plastic Injection Moulding. At current price the share is expected to give a return of 45% for next year

| Date of report: | 04-06-2024 | Competitor PE | 61.71 | Sector | Electronic Components |

|---|---|---|---|---|---|

| CMP: | 2346 | Current PE | 45.2 | No of Years | 47 |

| Market Cap: | 6107Cr | Highest PE | 77.9(2022) | Key Products | RAC & Plastic Moulding |

| ROCE / ROE | 18.7% / 18.8% | Lowest PE | 33.4 (2024) | Key Competitor | Hind Rectifiers |

Business Model and Industry Analysis

Overview:

Company is into OEM manufacturing of AC, Washing Machine and Air coolers termed as Product business which contributes 61% of revenue followed by plastic moulding business. Company serves as an OEM for many leading brands such as Blue Star, Godrej, Haier, Voltas etc. Company also is an ODM where it also helps in designing products which then consumers sell them under their own brand name. It operates only in domestic market. Co pricing works as Fixed Cost + Markup where it is able to recover increase in cost but is not required to pass on any reduction. Thus the business is naturally hedged from commodity price fluctuation.

Industry Growth:

AC Industry: Expected to grow at CAGR 16.7% till 2029. Currently AC penetration in India is only at 8%

Washing Machine: Expected to grow at CAGR 7.43% till 2029. Currently AC penetration in India is only at 15%

Air Cooler: Expected to grow at CAGR 7.7% till 2029.

Plastic Molding: Expected to grow at CAGR 4.18% till 2029.

Capacity Utilisation:

The company has 5 plants namely 3 in Uttar Pradesh, 1 in Maharshtra and 1 in Uttarakhand. Co is not providing any numbers on capital utilisation. Co stands second for selling of Washing Machine units in India. Co has invested Rs150 Cr in expansion for doubling washing machine capacity while also further expand Room AC capacity to 200,000 Indoor Units and 100,000 outdoor units, along with further backward integration by adding the set up for Room AC controllers.

Opportunities:

Co has huge potential for growth in AC segment as disposable income in India is rising along with the summer temperature in India leading to higher AC sales. Further in Washing machine segment, with rising female employment, there is rise in sale of washing machine. Co is also availing grants from government under PLI scheme leading to better gross margin. It has also entered into JV with Goodworth Electronics for TV segment. This JV will help strengthen sourcing capability from China as company is planning to double its TV production. The pricing mechanism acts as a natural hedge for the company and is guarded against commodity inflation.

Risk:

Co has major risk of debt trap. With the expansion taking place the company has also been taking up debt. Although co has started mitigating this risk. To get out of the debt trap, co has raised funds from QIP for purpose of debt repayment. No other major risk is seen in company

Future Expansion:

The company has given guidance of 370cr to 380 cr of capex to expand its RAC Capacity by setting up a unit in Rajasthan and further adding up on washing machine capacity by ~60% by taking up a plant in Noida. The SUPA facilities will be expanded further with new buildings and further capacity enhancement for room AC business.

Management:

Management is genuine and decision are taken in line with investor interest. Few examples being share split to increase liquidity in market, QIP to pay off debt etc. The concerning point is that management and repalted party draw salary of around 10% from after tax profit which is significantly high. Promoters hold 53.7% in the company which is free from any pledge

Institutional Investor:

FII and DII continue to hold around 22% in the company

Historical Data and Financials

Profit N Loss Account:

* Sales have historically grown at **65%** over last 5 years and at **27%** in last year

* Margins have continuously improved and stands at around **10%** currently

* High salary withdrawl by related party amounting to 10% of PAT

Balance Sheet:

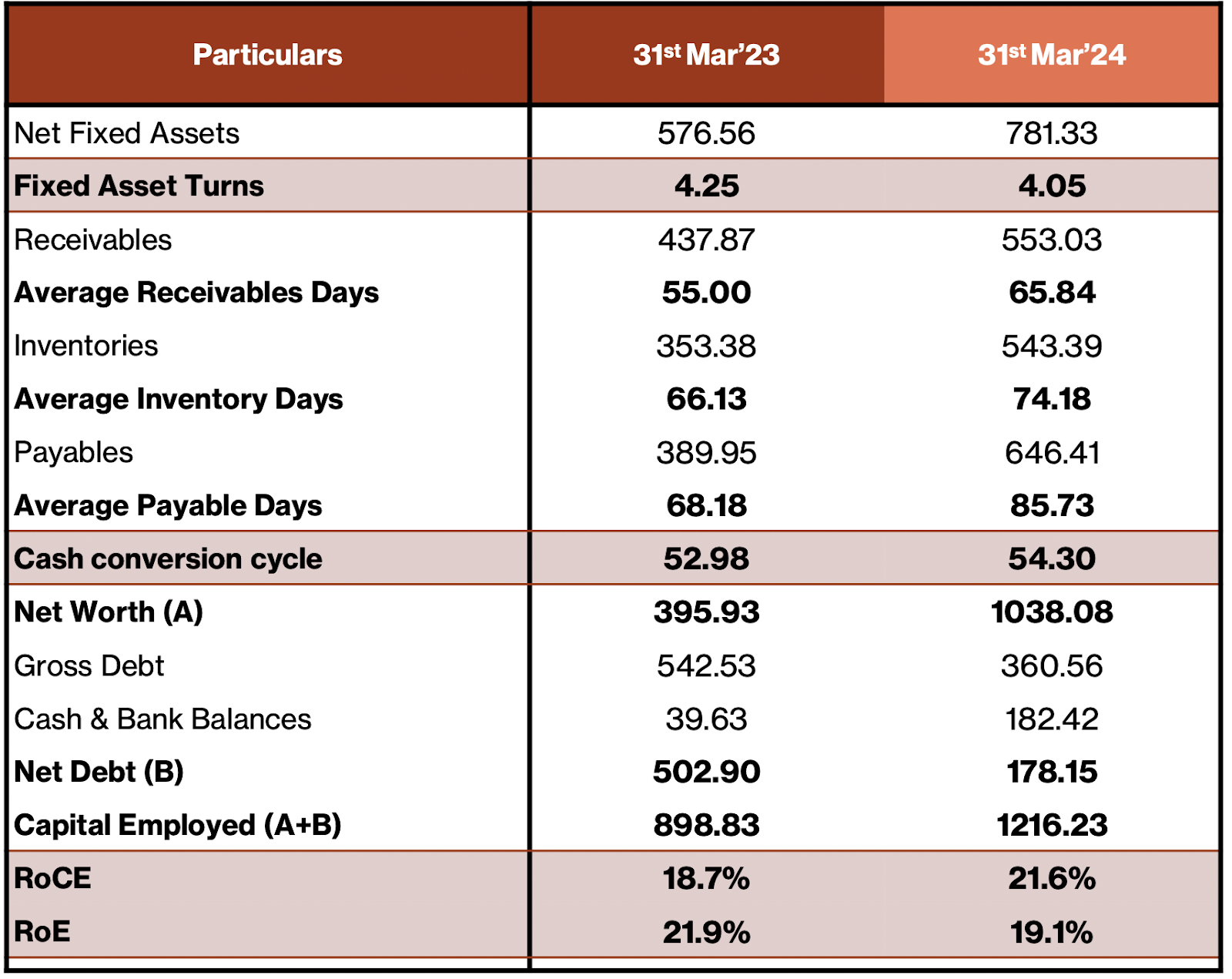

* Company has reduced its debt by raising QIP and debt/equity stands at **0.42** from **1.46** in 22/23.

* Interest coverage ratio is **4 times**

* EVA of company is negative

* Inventory days have increased from **73** days to **90** days

* Debtor days is constant

* Working Cycle and Cash conversion cycle have improved YoY

* Current ratio has improved from **1** to **3** from 22/23

Cash Flow:

* CFO/PAT is at lower side standing at 75.61% due to long working capital cycle

* FCF/Earnings is negative due to high capex investments by the company to support revenue growth

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 2346 | 2734 | 1459 | 2734 | 35.2 | - |

| PE Ratio | 45.2 | 57.7 | 33.4 | 77.9 | 33.4 | 74.86 |

| EPS | 51.9 | 51.9 | 41.9 | 51.9 | -5.15 | - |

| Price/Book | 6.2 | 13.5 | 3.1 | 13.5 | 0.4 | 5.83 |

| EV/EBITDA | 8.4 | 29 | 16.6 | 111.8 | 11.2 | 25.22 |

Valuation:

| Particular | 23/24 | 24/25 | Comments |

|---|---|---|---|

| Sales | 2746 | 4000 | Management Conservative guidance |

| Profit | 137 | 200 | Management Conservative guidance |

| No of Share | 2.7 | 2.7 | - |

| EPS | 52 | 75 | - |

| PE Ratio | 45 | 45 | Average PE traded |

| Share price | 2346 | 3411 | |

| Return | 45% |

Disclaimer: This is a study report, not for any decision making or investment advisory.

Made by: Nidhi Devidan

Date:4th June 2024

5 Likes

@devidan.n Good Analysis. I have one doubt regarding the revenue. Goodworth revenue will not consider in PGEL imo. Company will do only 3400 cr

2 Likes

Should I take only 50% in profit? As JV is at 50% partnership.

Yes JV is 50%. But not sure about that revenue will add in PGEL books. In Concall also company told that group revenue will 4k cr. But PGEL 3400 cr.

2 Likes

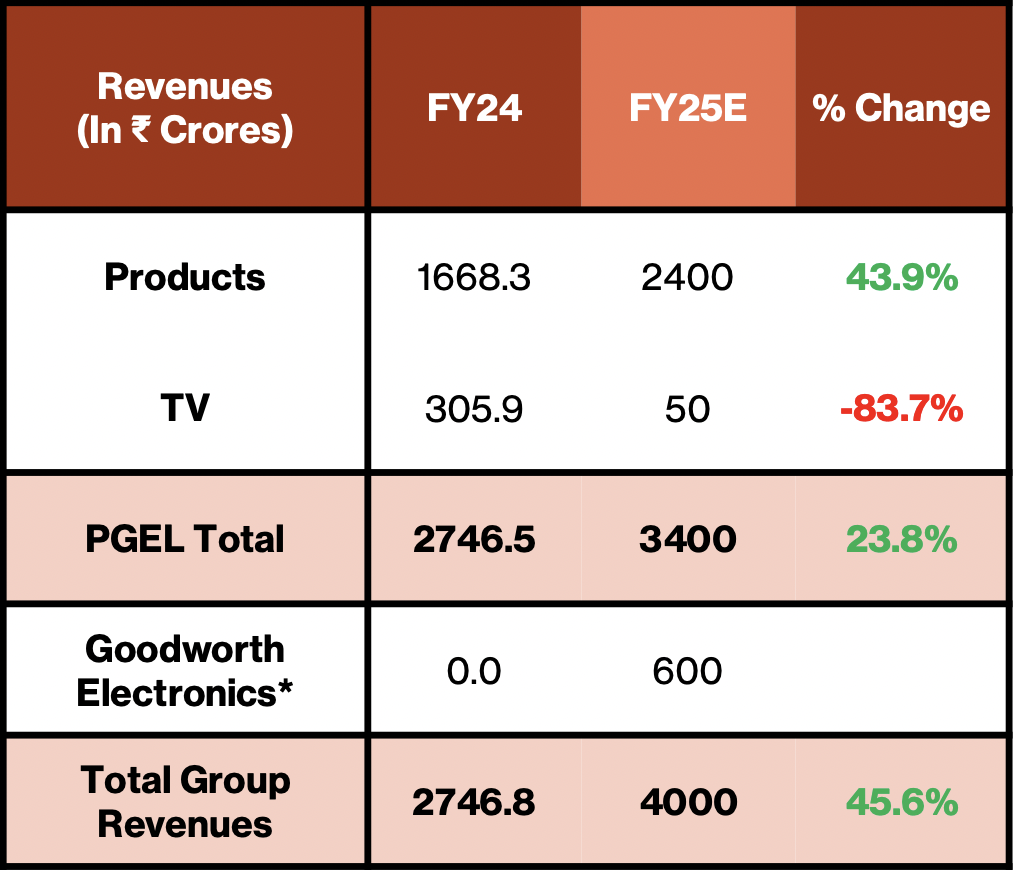

In case of a JV, only the proportionate share of profit is accounted in the company’s financial statements. So, as per management’s guidance, the PGEL is targeting Rs. 3,400 Crores of revenue in FY25 (Rs. 600 Crores of Goodworth shall not be considered here). However, the management has guided for Rs 200 crores of Net profit - This will include the proportionate share of profit from the JV.

In summary, management guidance for PGEL for FY25 is 3400 Cr revenue and 200 Cr Net profit.

Hope this helps!

About the company

Specializes in: Original Design Manufacturing (ODM), Original Equipment Manufacturing (OEM) and Plastic Injection Moulding.

- Original Design Manufacturing (ODM) is a business model in which a manufacturer designs and produces products according to its own specifications and sells them to another company, which then markets and sells these products under its own brand name.

- Original Equipment Manufacturing (OEM) is a business model in which a company manufactures products or components that are purchased by another company and retailed under the purchasing company’s brand name. Unlike ODM, where the manufacturer also designs the product, in OEM, the purchasing company typically provides the specifications and design, while the OEM company is responsible for producing the product or component.

- Plastic injection molding is a manufacturing process used to produce large quantities of plastic parts with high precision and repeatability. It is commonly used in various industries, including automotive, consumer electronics, medical devices, and packaging.

Q4 FY24

Financials

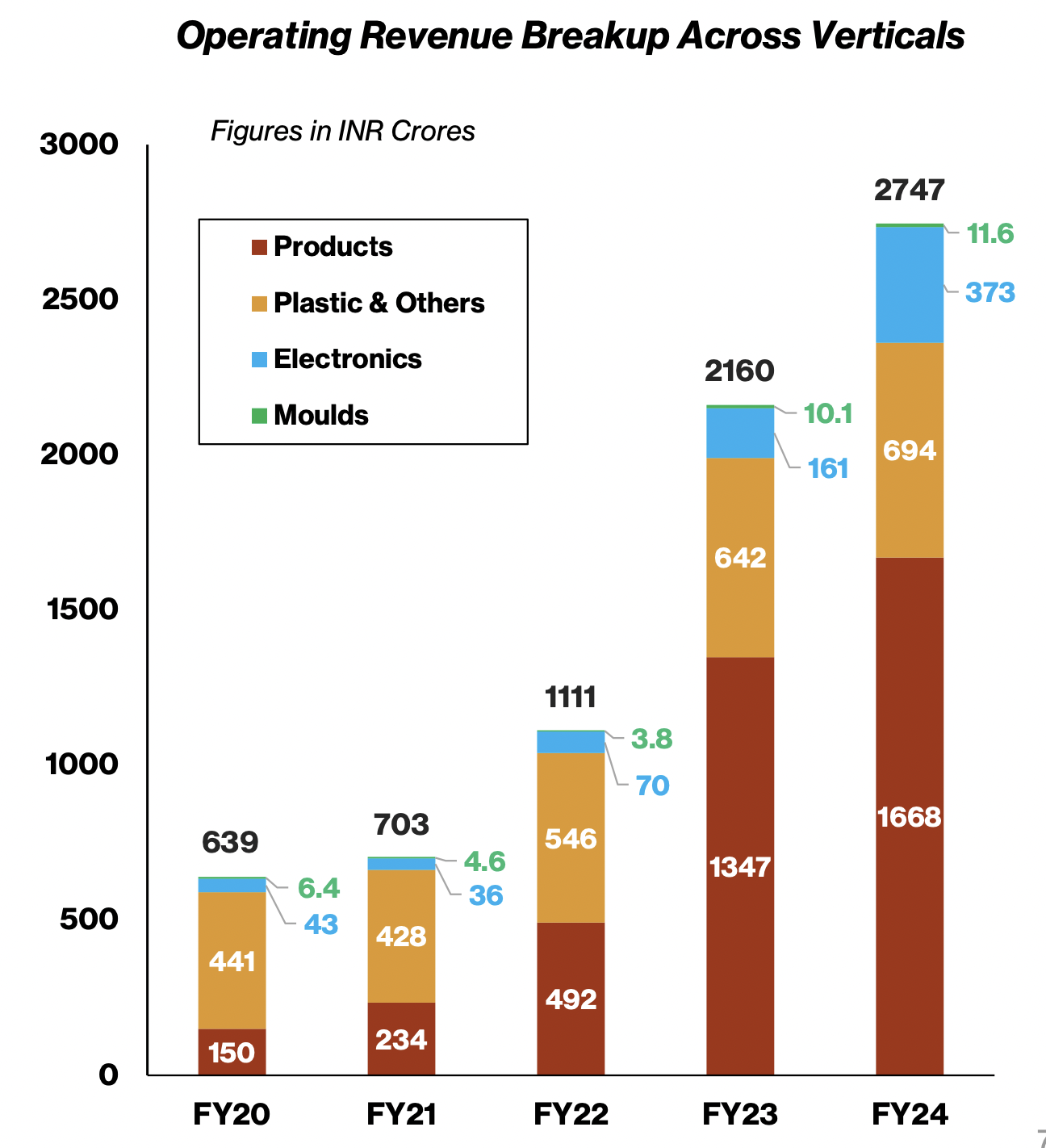

- The Product business contributed 60.7% of the total revenues in FY24. Room AC business at INR 1317 crores grew 26% during the period while the Washing Machines business had a growth of 20% YoY.

- PGEL’s 100% subsidiary, PG Technoplast, crossed INR 1456 crores in revenue in its third year of operations. Company’s Bhiwadi AC Unit became operational during the year

- operating margins have improved QoQ and YoY due cost control, softer commodity prices and operating leverage.

- Net debt has decreased by almost INR 325 crores in FY24 despite Capex and acquisition of NGM.

- The room AC business contributed INR1,317 crores, which is a 26% growth on a year-by-year basis. The washing machine business had a growth of 20% on a year-by-year basis, and coolest operating revenues were flat, largely because of steep fall in ASP

Business details

- The company has also forged a new JV partnership for the TV and hardware business, and the JV company, Goodworth Electronics, was selected for IT hardware PLI 2.0. Jaina had a Google ODM license which only two other people have in India Dixon and one more company. So that comes into the JV because of the JV with Jaina. Second thing is that they have very good sourcing capability because they have been the promoters earlier of Karbon brand and they still own the Karbon brand.

- Posted a 26% growth in product segment despite of the average selling price being down by 8%

- The room AC business contributed INR1,317 crores, which is a 26% growth on a year-by-year basis.

- The ASPs in the RAC washing machine and coolers were down significantly due to low commodity prices during the year and especially in the fourth quarter. Also, the business in the first half of FY24 suffered due to unseasonal rains, and despite these challenges, we have posted industry-leading growth in RAC revenues of 25% for the full year.

- 20 crores as a part of incentive is accounted for in the earnings

- This year, plastic molding is about 7.5% margin business electronics is about 2% and then the rest of the margin whichever way you look is coming from the product business.

- The business has seasonality because a high chunk of revenue comes from ACs, coolers etc and hence we cant extrapolate the margins of one quarter for the whole year. Q1 and Q4 are good margins because of high demand which leads to operating leverage.

- Our pricing is almost same as the competition or slightly in some cases slightly better than competition and we are not compromising on the pricing because we have some cost advantage or we have some PLI benefits as of now.

- In the AC revenue, 85% or so goes to branded players and the rest goes to private levels.

- When they take up a project, they aim for 15-16% pre tax ROCE

Outlook

- PGEL Net profit guidance of INR 200 crores which is a growth of 46% over FY2024 Net profit of INR 137 crores.

- FY2025, Management expects EBITDA margins to have slight upward bias because the TV business which is low margin in nature isn’t a part of the company anymore. Q1 will still have some inventory worth 40 crores to be sold but after that no contribution.

- The growth in product business i.e., WM, RAC and Coolers is expected to be around 44% to over INR 2400 crores from INR 1668 crores in FY2024.

- Capex guidance for FY25 is in the range of INR370 to INR380 crores, and the company has planned to further expand room AC capacity by setting up a new integrated unit in Rajasthan. It will largely be funded internally.

- hopes to accelerate the product business growth in FY2025.

- Aiming for 25-30% growth for the RAC business.

- total INR65 crores will get incentive next year. PLI of INR30 crores and INR35 crores-INR40 crores of state government incentive. Out of 200, around 30 crores is PLI scheme which was 11 crores this year.

- They want their asset turns to improve and expect minimum 4-4.5 of asset turns.

- Over the next 3-5 years, they expect the industry to grow 15-20% and they are also gaining market share so they believe they can grow around the industry average or a little higher.

- Employee cost should grow in line with the revenues, In the last 1 years, 2 years there has been significant portion in employee cost almost 10% to 12% in the last 2 years which is coming from the hit on account of ESOPs. So we have given quite decent ESOPs, almost 200 people in our company are covered under ESOP and we have taken INR15.5 crores hit this year which is a part of our employee cost because of the ESOP and therefore our employee cost looks slightly higher.

- In PLI: if we meet all the targets then next year the number is in FY25 we should

- get INR30 crores after that INR 36.5 crores then year after that INR51 crores and year after that last year’s number was INR60 crores. In case of state government benefits, the first year is going to be little bump up maybe INR35, INR40 crores and then year after that every year about INR20 to INR25 crores.

- If the seasonality isn’t very stark, can expect 25% ish ROCE

Risks

Industry

- why we are doing such a heavy capex, as I told you last year this year we are doing a huge capex on creating an infrastructure which is land and building for future growth. We are seeing some very exciting huge opportunities coming at our doorstep, which we are in the active stage of discussion with significant clients which are looking to shift their work to India from China and some clients which are looking to actually expand their relationship with us. Now because of that, we think that we are getting into a phase where the growth could be accelerating in the coming year and we may be short of infrastructure for growth, because ready sheds are not available typically for leasing out and therefore we need to create some of those optionality for us and that money is going into creating those optionality and that, we should be able to utilize most of it in the next 2-3 years in our opinion.

- We are seeing industry overall being slightly short of the capacity right now on the monthly demand which we saw in month of April, May and June probably. April, May, also there was a little bit of planning shortfall, nobody actually anticipated such strong growth in the demand and therefore people were probably not ready to take care of such a huge, I’ll say demand and therefore probably in the coming weeks or we will see some stock outs in some of the major brands, probably because the material is just not there.

these are just my notes on Q4. Very strong growth ahead. I wish I could have picked it earlier when it corrected.

14 Likes

From your notes, it seems like most of the recent growth is already accounted for in the PE.

1 Like

60 PE would be reasonable for such growth company, PE is down from 80 levels in 2021-2022 to 37 levels in Mar’24.

There was some correction after Q3 call where management cautioned about the growth prospects due to in house capacity building by brands, but they keep on acquiring the new customers and introducing new products to maintain the growth.

Q4 comments are very strong and growth would continue for medium term.

7 Likes

stock investing always has regrets. for not buying, for not buying enough, for not booking profit, for selling early.

8 Likes

I had bought at 350 and sold at 1000 as it was looking expensive to me at 1000:joy:![]()

![]()

1 Like

They may be crossing 3500 to 4000 Cr on consolidated basis in FY 25. As per management, they are eying more than that.

4 Likes

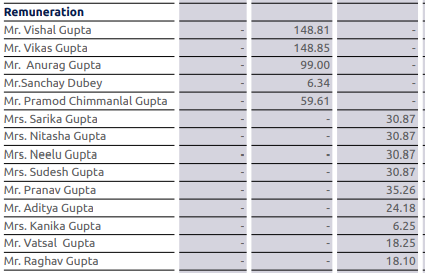

The salaries drawn by the relatives in FY23. Are they part of the company in revelant roles?

Regards,

Ashutosh

2 Likes

Market overall is growing at a rapid pace!

Chennai & Sri City are becoming new hubs for manufacturing.

Almost every OEM is setting up new capacities.

Overall AC market in India is expected to grow 2.5x - 3x in the next 5-6 years!

Huge growth runway ahead

PGEL should be a huge beneficiary of this. No wonder why the management sounds so confident and the numbers have been reflecting the same.

Disc: Invested

9 Likes

CELLECOR_25042024192715_PPTCellecor25042024signed.pdf (2.2 MB)

New customer addition for PEGL and also we can see growth in cellecor aswell

3 Likes

Q2 FY25

- The company has revised the guidance of revenue from 3650 cr to 4250 cr and pat from 216 cr to 250 cr. And have said that they have orders book to fulfill this till March 2025.

- 370 capex on going in Bhiwadi, Rajasthan for ac and in Noida for washing machines and in the expansion of Supa plant (from 370 cr, 165 goes to product business(plant and machinery) and 185 cr goes to the acquisition of land (infra) and 20 goes to maintenance capex(for plastic molding and sanitary product)

- only looking for organic growth ( when asked if they will acquire some company for growth from 1500 QIP).

- Inventory may seem high because the company said supply chain challenges might be faced in the coming month, so they have kept necessary items in inventory to fulfil guidance.

- The company is not looking to reduce debt significantly right now

- The company has created a separate team to look into the export market. And probably look into export in 1-2 year in Middle East and Africa part

7 Likes

I am waiting for the new product announcement, which is not yet disclosed.

Hardware PLI and New product launch are key things to watchout.

1 Like

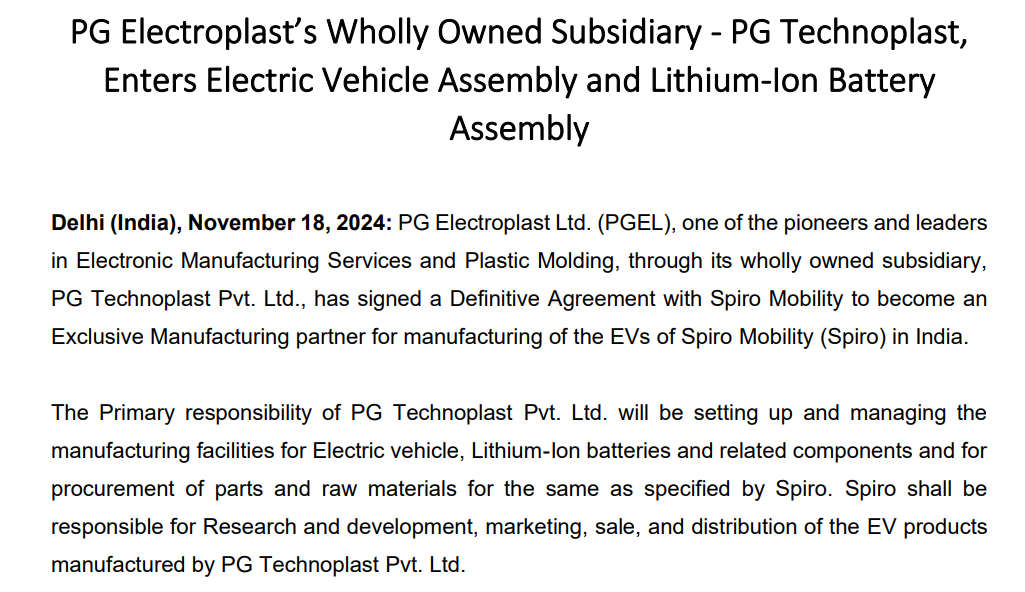

Entry to Electric Vehicle Assembly and Lithium-Ion Battery Assembly

Source - https://www.bseindia.com/xml-data/corpfiling/AttachLive/c32d2d29-d093-431b-a730-69a03349a069.pdf

7 Likes

QIP amount will be used for the below new vertical, Interesting thing we need to know is asset turn of this vertical whether its similar to the existing verticals asset turn of 5-6x or its lower than that.

I hope that with the foray into new business vertical, PGEL will grow exponentially in the coming 3-4 years

2 Likes