I feel the Company Lacks pricing power, The Promoters are the customers here ! and they also sit on board & are Key mgmnt personnel. That one of the main reason i can see why the price is not moving up.

2 Likes

Hello,

The last message in thread was in Sep,2022. Since then the thread is quiet, but the stock price has increased by almost 15%. I understand we may not discuss day-to-day price movements, my question is that is there any important business update that is being missed?

1 Like

I am a bit surprised Petronet LNG’s stock price is still muted given that it’s been a while since LNG prices came off, and they have stayed low. Currently LNG prices are at less than $10 mmbtu as per this article.

In addition, South Asian buyers have increased their offtake, and I assume, Petronet must be one of those. End-use industry demand should be quite robust at these prices and should help increase the utilization of their terminals after a difficult FY23. Dahej, in particular, should see much better demand. Kochi terminal utilization is still poor, but nevertheless, I would expect better results in Q1 and possibly, going forward as well.

Any thoughts on why the stock price continues to be depressed?

Disclosure: Hold it, and have added a bit recently.

3 Likes

This stock has a tendency in the past to remain range bound for long periods, and then it rises sharply. You can check this on screener.in as well.

In FY23, there was good increase in Sales and Profits in first 2-3 quarters but still stock price was stagnant. Now in the last quarter, there have been reduction in PAT. OPM has reduced from earlier 11% to 7% in Q4 FY23, which seems to be the lowest OPM in past few years.

I believe that, with some capacity expansion happening, and inflation being stable, OPM should revert back to Mean in next few quarters.

I consider this as a low growth moderate Dividend Yield stock, and it looks undervalued in this stretched market.

Stock Price often takes it own time to reflect some of these fundamentals.

Disc: Holding.

4 Likes

Petronet is required to renew their import contracts with Qatar this year. While the management has expressed their intention to extend the contracts until 2028, it is uncertain whether there will be an increase in import volumes. Given the diplomatic tensions that have been escalating between India and Qatar, it would be prudent to wait and observe how the situation unfolds.

Disc: Not invested

4 Likes

Yes, if Petronet is dependent on Qatar for supplies, then it is going to be restricted a lot by the GOI; all commercial contracts wth Qatar are being reviewed across all Gov sectors. See aviation, Qatar airlines taxes issues with the Itax dept.

I would like to know - the alternative to Qatar if the Gas contracts are not renewed due to certain non-economic reasons by GOI? Which are those other sources of the Gas for importing? Will those nations give Gas at lower rates?

Also, would like to know the impact of above 20K investments on Top Line and Bottom Line, as my understanding is limited in this sector.

Invested due to good Dividend Yield and undervalued stock price few years back, but no major gains so far.

1 Like

Petronet LNG and Qatar have a long-standing strategic relationship based on mutual energy interests. Petronet LNG is India’s largest importer of liquefied natural gas (LNG), and Qatar is a major global supplier of LNG.

- Long-term LNG supply agreement: Petronet LNG has a long-term LNG supply agreement with Qatar that expires in 2028. Under the agreement, Petronet LNG imports 8.5 million tonnes per annum (mtpa) of LNG from Qatar. The two parties are currently in negotiations to extend the agreement beyond 2028.

- Joint ventures and partnerships: Petronet LNG and Qatar have been involved in several joint ventures and partnerships to explore and develop natural gas resources. These include:

- RasGas-Qatar LNG Terminal: Petronet LNG holds a 30% stake in the RasGas-Qatar LNG Terminal, which is one of the world’s largest LNG export terminals.

- Qatar LNG Terminal 2: Petronet LNG is considering taking a stake in the Qatar LNG Terminal 2, which is currently under construction.

- Investment in Qatar’s LNG infrastructure: Petronet LNG has invested in a number of infrastructure projects in Qatar, including pipelines and LNG terminals. These investments have helped to strengthen the relationship between the two countries.

Petronet LNG is a key customer for Qatar’s LNG exports, and the company’s investments in Qatar’s LNG infrastructure have helped to develop the country’s LNG industry.

Source: Bard

I hope they work something out. A break up with Qatar is a loss-loss game for both Petronet and Qatar.

4 Likes

Few observations from Q3 FY24 Results:

- OPM has increased to 9.7% and may go to the 5 year Avg levels of 11% in next few quarters.

- Investment in Petrochemical projects may generate more revenue streams after few quarters / years.

- Stock is trading at P/B of 2.0 and 10 or 5 Year Median P/B is 3.2. This is looks attractively valued now. Stock Price has been stagnated since 2018 even though ROE is improving in past 2 years.

It seems that, currently there are negative perceptions about the stock (similar to Coal India in 2022), and it may give good returns with Dividend Yield of > 3.0% in next few years.

Holding the stock since 2022 and will remain invested for some time as I believe that, Reversion to mean in terms of P/B can happen.

1 Like

Petronet – A business analysis

Background

As of 2023, Petronet is a simple business. It has two, port-based LNG regasification terminals in Dahej and in Kochi, with current capacity of 17.5 and 5 MMTPA respectively. Petronet has long-term contracts with several suppliers like Qatar (7.5MMTPA) and MARC (1.425 MMTPA – an Exxon branch), as well as long-term contracts with customers like IOCL, BPCL, GAIL etc. (8.25MMTPA). This part of the business is like a utility business and is not sensitive to LNG prices, since it is pass through at (pre)negotiated rates. A smaller part of the business also buys LNG on the international spot market and sells it to customers, like the fertilizer industry, that are price sensitive and will swap LNG for alternative fuels like coal, if LNG is too pricey. This part of the business is like a commodity business and also has inventory risk.

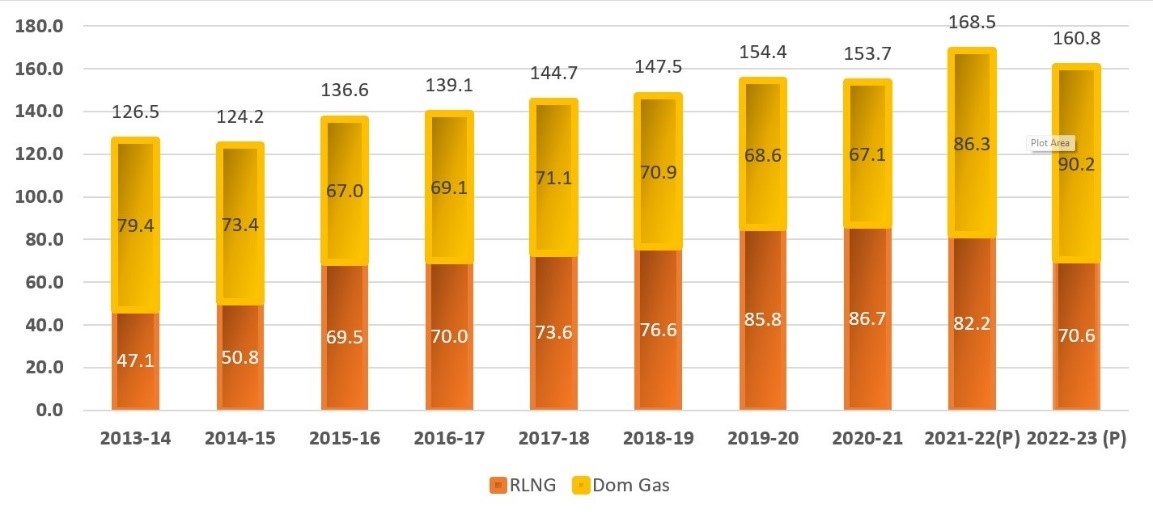

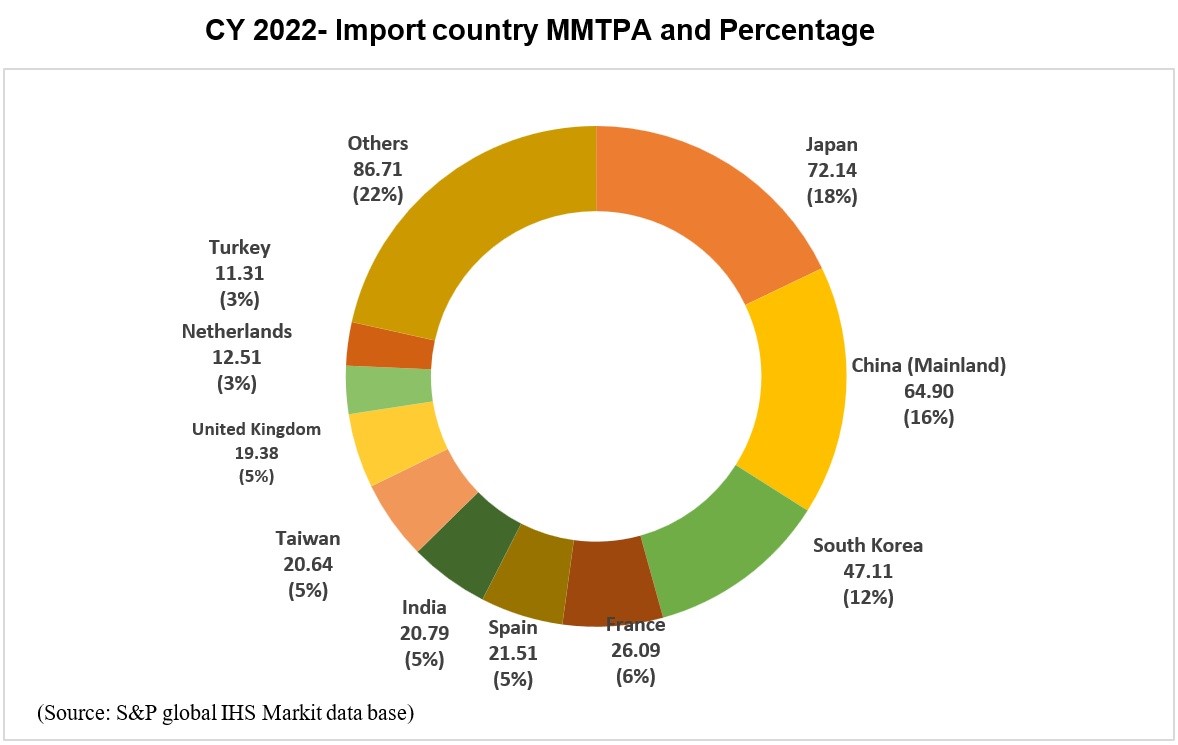

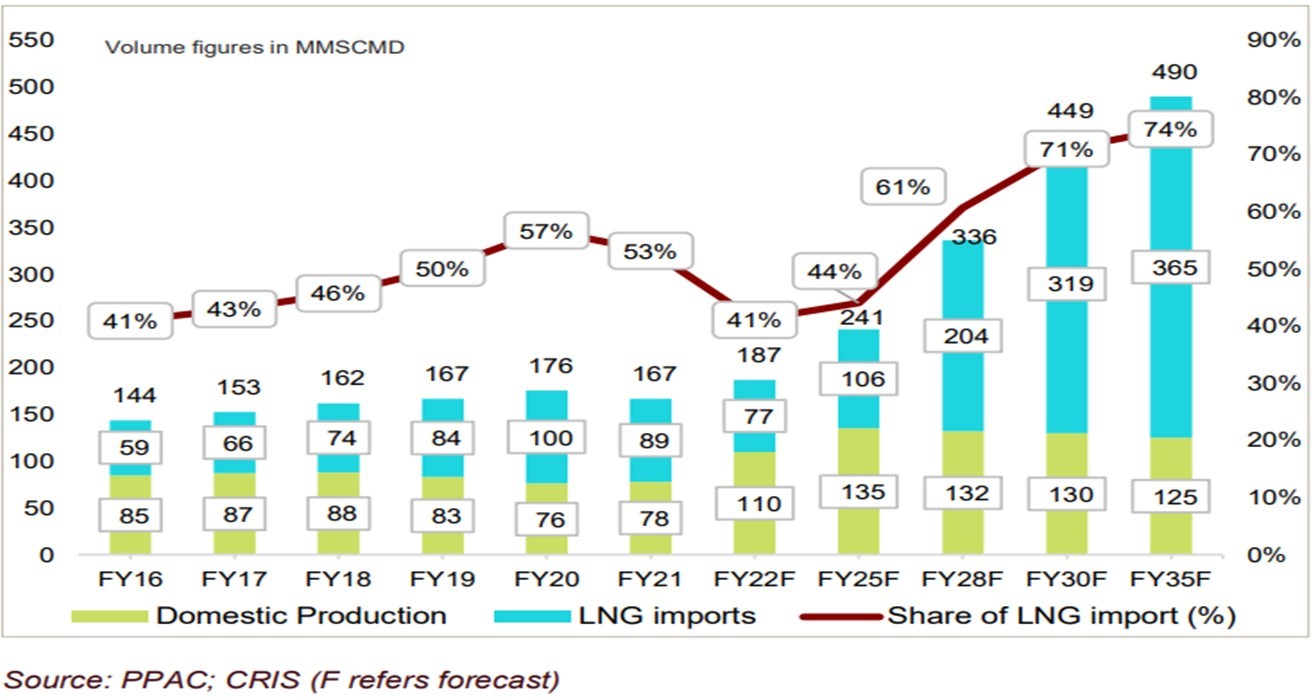

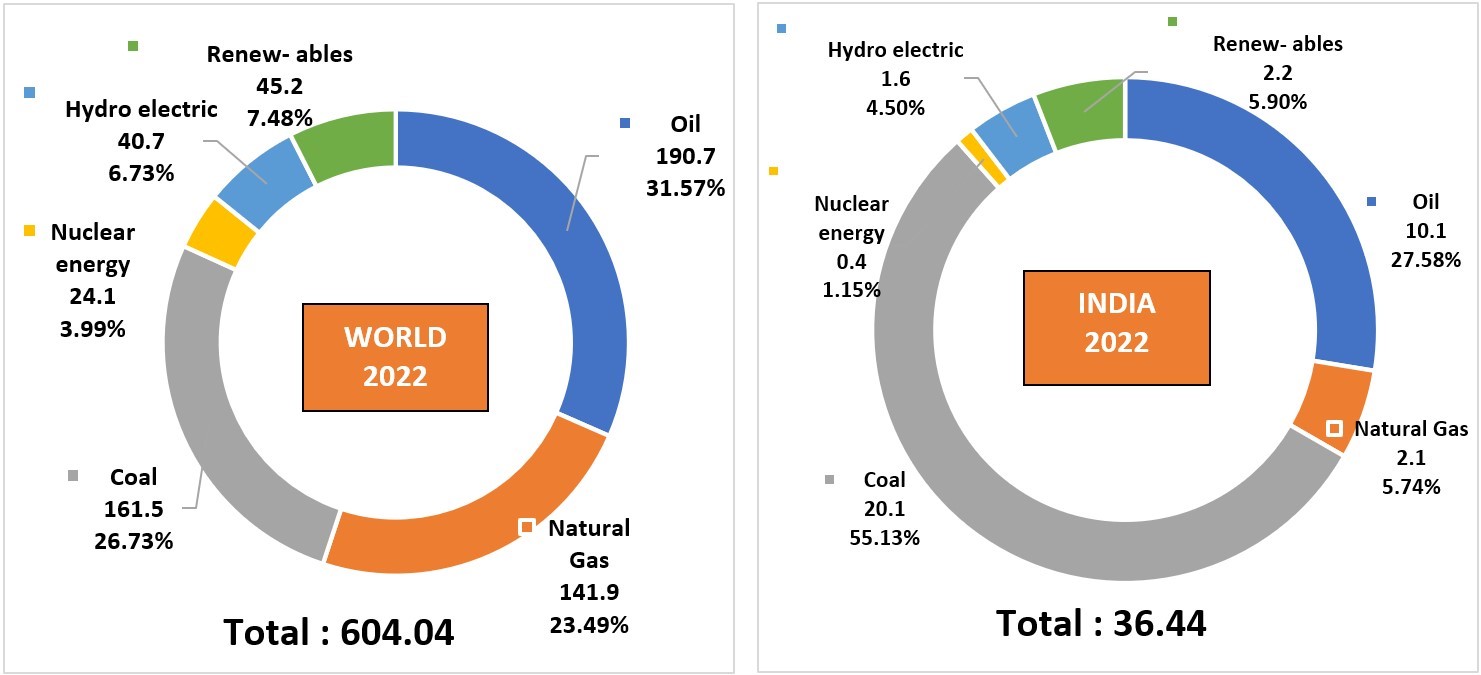

In the CY 2022, India had long term LNG contracts of almost 20 MMTPA, which constitutes approximately 95% of around 21 MMTPA LNG consumption (Annual Report 2023). Since India is a gas deficit country and relies heavily on LNG imports, Regasification Terminals play an important role in the country’s gas development plans. The share of LNG in India’s gas consumption mix stood at around 44% in the FY 2022-23. See Figure 1, Figure 2 Figure 3 for more details.

Figure 1: Gas consumption in MMSCMPD (to convert to MMTPA, divide by 3.6).

Figure 2: LNG imports by different countries.

Figure 3: LNG as percentage of expected gas consumption in India.

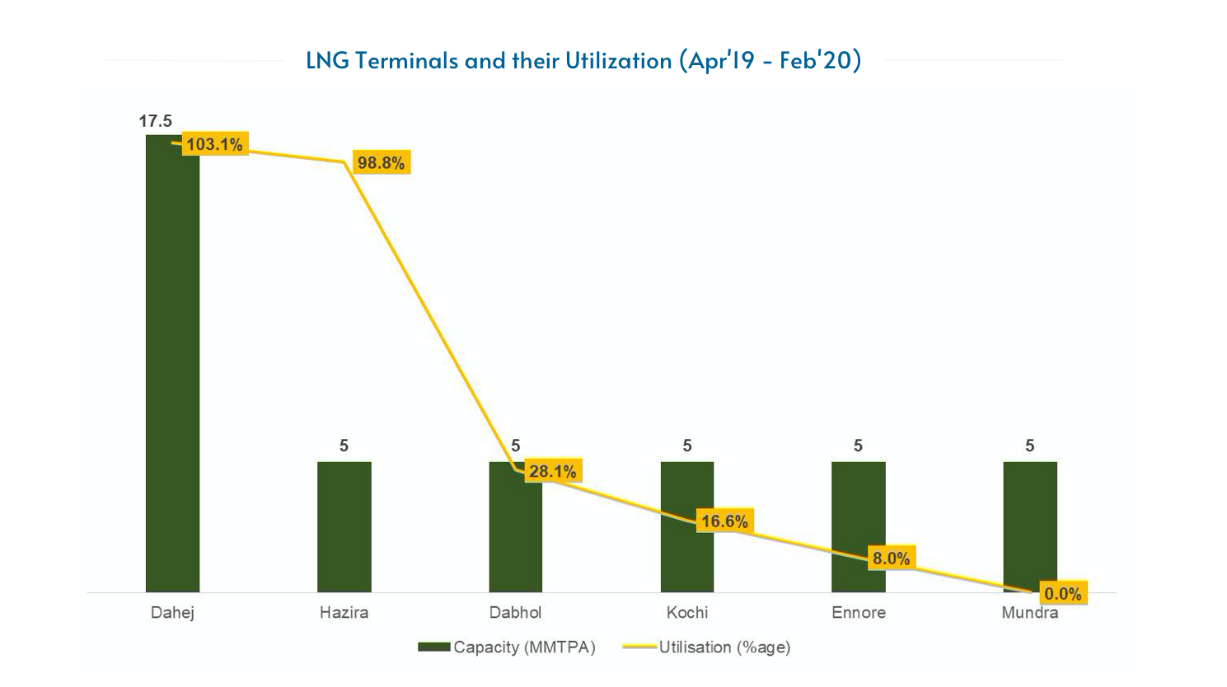

Current regasification capacity in India is 47.7 MMTPA. Only Petronet’s LNG terminal at Dahej and Shell’s terminal at Hazira are operating at near optimal capacity. Other terminals remain underutilized and operate at less than 25% of their regasification capacity. 17.5 MMTPA of the 21MMTPA of pan-India imports were at Dahej. Figure 4 gives details.

Terminals at Kochi and Ennore are operating below capacity due to insufficient pipeline connectivity with the demand centers. The 5 MMTPA Dabhol terminal is being operated at low capacity owing to the absence of breakwater required for protecting LNG ships during the monsoon season (H-Energy).

Figure 4: Capacity utilization at various LNG terminals.

There are new Regasification projects under construction by different companies at various locations namely Jaigarh, Jafrabad, Chhara and Petronet’s greenfield floating stage regasification unit based LNG terminal at Gopalpur on East Coast along with expansion of Petronet’s existing regasification terminal at Dahej from 17.5 MMTPA to 22.5 MMTPA. It is expected that with the completion of all these new terminals and expansion projects, the total regasification capacity in India will increase from 47.7 MMTPA to 72.7 MMTPA.

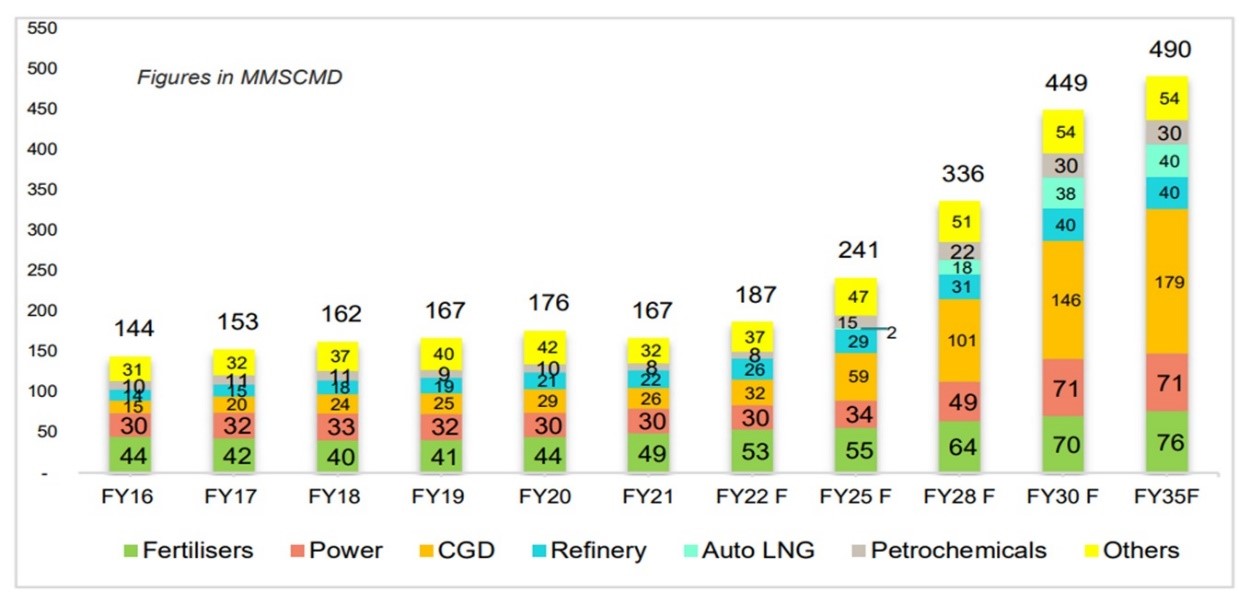

In order to achieve 15% share of Natural Gas in the energy basket of India by the year 2030 (from 6.2% at present, see Figure 5), India would require around 150 MMTPA of LNG re-gas infrastructure. Thus, creating additional capacity of over 77 MMTPA is necessary. The drivers of increased gas demand are shown in Figure 6.

Figure 5: Energy consumption mix by world versus India.

Figure 6: Drivers of gas consumption by industry.

Since domestic capacity is limited, growth in gas consumption can only be met through importing LNG unless there are piped gas connections to India, e.g., underwater piped gas from the middle east to the western seaboard. Such a project, however, takes decades to conceive and develop.

Business drivers

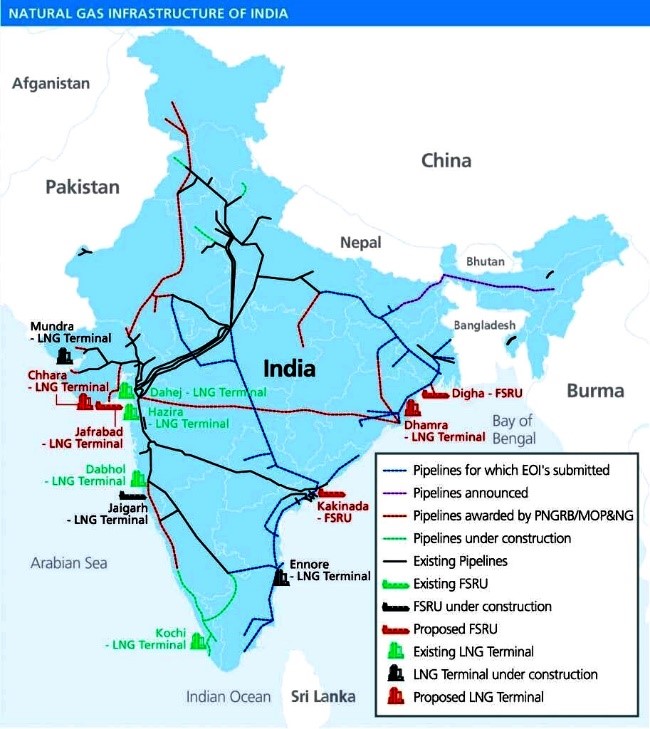

While the regasification capacity of India is more than 2 times the current imported volumes of LNG, the Dahej terminal alone is responsible for 80% of pan-Indian imports. Dahej is the crown asset of Petronet because of the dense network of gas-pipelines that connect to Dahej and its proximity to the Middle-East (primary supplier). See Figure 7! While terminals run by other companies will slowly get connected to the gas network, its going to be a long and unpredictable process. With secular demand for increased LNG, that though is not going to be a problem for Dahej.

Also, Dahej’s capacity is increasing from 17.5 to 22.5 MMTPA with 2.5MMTPA increase expected by 2024. The pipeline between Kochi and Bangalore that has continuously had challenges, in the coming years, will get completed (thus integrating into the national gas grid) leading to a huge increase in the capacity utilization from 20-30% to 80%. So effectively, for Petronet, its gas-pipeline connected capacity will go from 17.5 to 27.5 MMTPA (60% increase). Keep in the mind that the pipelines are not owned or maintained by Petronet, thus no maintenance capex related to these. That’s why, Petronet has a high ROE and ROCE, 26 and 22% respectively.

Figure 7: Map of gas pipelines in India (2021). Source here

Analysis of Financial Statements

From a balance sheet standpoint, there is no debt – in fact the market cap is INR 321000 million while the TEV is 270000 million, so nearly 5000 million in cash on the balance sheet. Book value is nearly 50% of the market cap (150000 million).

From an income statement perspective, revenue and EPS growth is 14 and 10% respectively over the last 5 years. These should expand considerably as new capacity becomes available in the coming years. A dividend yield of 3.3% that grows regularly is also decent.

In 2023 FCF was lowered because of capacity expansion and the building of a 3rd Jetty at Dahej – no worries, a good use of capital!

Table 1: Key metrics from financial statements in millions INR over the past five years.

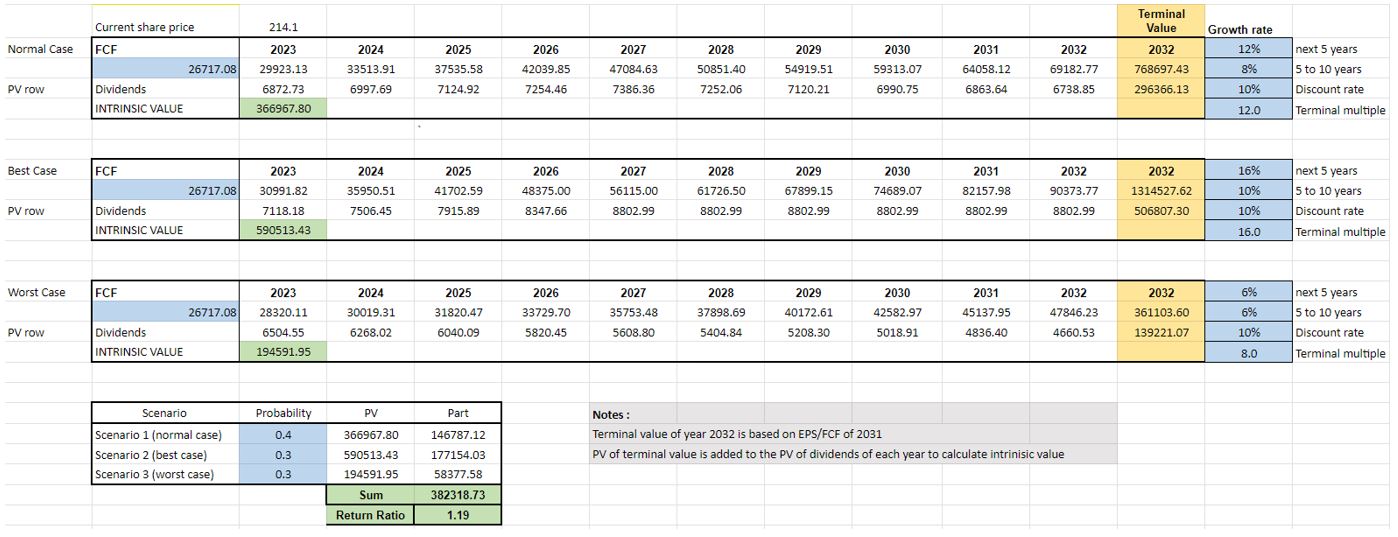

Under average 5-year FCF assumptions and modest growth rates, Petronet seems like a decent investment with returns of 10-12 percent with limited downside. FCF should increase with nearly a 60% increase in planned capacity that is almost guaranteed to come online in the next years.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

With a strong balance sheet, good ROIC and excellent gas pipeline connectivity to its terminals, Petronet is a predictable business that produces reliable FCF – these might vary year-to-year based on new contracts being negotiated and the ongoing spot market rates, but over a few years, things will even out. With secular demand for increased gas use, importing of LNG is unavoidable. Petronet gets a piece of the pie, come what may. Just keep in mind that one of the risks is that Petronet is still a government company.

Company news

Petronet on 31st Oct 2023 announced a greenfield expansion into petrochemicals at Dahej – an entirely different business and likely deworsification. The proposed project includes 750 KTPA of Propane Dehydrogenation (PDH) & 500 KTPA of Propylene (PP) plant including propane and ethane handling facility. The cost will be INR 210,000 Million and will take 4 years for development. The cost per se is not an issue – it can be covered by the coming 4 years of FCF and the cash on the balance sheet. Of course, taking some debt will not be a problem either. In effect we will be transferring FCF for the next 4 years into tangible equity. The question to ask is what will the ROE be on the invested capital? I assume, the project will take about 7 years – 4+ years for development and then a year+ for the factory to get fully operational. So, worst case, we are going to see cash flow from this development only from 2030. I expect ROIC for Petronet to get to and stay in the low teens for the next years and no meaningful change in stock price. Here’s a report by Emkay on the Petrochem foray.

Catalyst

I like the regasification business and at current prices would be willing to buy it. But the foray into Petrochem means that FCF of next years will disappear and ROE on this new investment is not visible. Frankly, even the management likely has no idea but since they are paid to ‘have answers’, they will be confident and give analysts what they want to hear. If price falls by 25% to around INR 150 per share, then wake me up as that would give some margin of safety!

18 Likes

Very detailed explanation of Petronet LNG business. Looks much better than most of the analyst reports.

In nutshell, the upside looks negligible for the buyers who have bought this at 220 levels 2 years back thinking that, CNG penetration story is strong. With the entry of EV and Hydrogen fuel alternatives, CNG story is already in trouble.

I am not sure whether existing investors should continue holding or better off with some other growth story.

Disc: Holding from 220 levels in 2022 onwards with only 2-3% Dividend Yield as gains.

1 Like

I wouldn’t put too much faith on Hydrogen/EV stories despite the press and ESG stuff. IF you believe in climate change, then reliable sources of energy is a must; the outages are now into 3+ days after natural calamities/damage. There is no renewable solution for this; only baseload from CNG and other nuclear assets.

CNG itself will end up being starter chemical for lots of industry and CBG will push its volumes higher. Short of H2 splitting cheaply by a new method for energy, CNG is actually a good space to be in the energy sector.

2 Likes

Petronet LNG seems to be in the same boat like Coal India 2 years back.

Its dividend yield is improving since P/E and P/B are both contracting. ROE has improved marginally after 2020 & 2021.

Main concern seems to be their capex plans in Petro-chemicals (looks like diversification in unrelated area) and usage of EV going up in next few years.

Stock has not moved much after 2021, and could be the right candidate to move in next few years.

Lot of patience is needed here.

PLNG may increase their presence in EV charging space, but that may not add meaningful revenues in near term. So mainly stock can go up only if P/B reverts to Mean.

Continue to hold the stock as long as Dividend Yield is above 2-3%.

Could you please explain the rationale here? It makes sense for BPCL and HPCL to foray into EV charging as it could become a natural extension to their Gas stations, but where does Petronet fit in?

I was wrong. PLNG is not investing in EV charging stations.

I was confusing it with Indraprastha Gas. They have said that, they would be also setting up EV charging stations to expand their revenue base outside CNG/PNG.

Indraprastha Gas has already installed and commissioned 4 fixed EV charging stations in NCT of Delhi and has also rolled out its battery swapping facility for two-wheeler and three-wheeler segment. Besides this, in order to explore the investment opportunities in EV value chain viz. battery manufacturing / swapping, EVs manufacturing etc., the company is in discussions with leading players in the field of EV landscape.

I do have investment in Indraprastha Gas as well hence the confusion.

1 Like

Anyone tracking charts of petronet lng pls share ur views…

It has surpassed 5 years moving average…

Disc.invested

The key trigger in the near-term is the contract with Qatar for gas supply renewal. The indications are that it will be at a lower rate from what the press is reporting. If that is so, I expect it can lead to a small degree of rerating. However, gas volume pick-up and higher utilization is what will drive a bigger rerating. There is a good chance of that happening, but it is hard to predict these things.

There are also some concerns about their recent announcement to expand into petrochemicals, but I think we have to wait for more clarity to emerge on that.

1 Like

Renegotiation concluded with contract renewal for a 20-year period. No disclosure yet on the rate at which the contract was renewed, but media reports mention it was at a lower rate.

https://www.business-standard.com/markets/capital-market-news/petronet-lng-to-purchase-7-5-mmtpa-lng-from-qatarenergy-124020600903_1.html

I guess price action will let us know how favourable or otherwise the new rate is even if the renewal tariff is not disclosed now. Also, in the earnings call, the MD indicated that the Coimbatore-Blr pipeline section is likely to be ready by CY24 year-end. If it does happen finally, that can lead to a substantial rerating. But given past history of delays, have to take such comments with more than a pinch of salt. In any case, so long as gas prices remain benign, the stock should do reasonably well.

2 Likes