Aspirational Margin 5% : one point to note is that the revenue was flat or perhaps fractionally lower than the corresponding quarter last year. Now this is as per our stated intent to replace our low margin revenue with higher margin products and services. We had guided to this in the previous few quarters. Specifically, our water EPC, our solar EPC, our retail revenue, and this is well over 100 crores for the previous quarter in the previous financial year has been replaced with higher margin and sustainable revenue from our pre-engineered buildings (PEB) division, tubes division, and our process industry equipment business, and also body in white.

Q2 PAT margin @ 2.75% (Track this margin on Q-o-Q basis)

2.Working Capital & ROCE : working capital. September 30th working capital days stood at 76 days. The annualized ROCE was at 21%, and our target ROCE for the year is 24%.

Our target working capital days is 72 days, and by the end of this year, we are confident we will achieve this target. However, working capital days in September at 76 days is a little bit higher than what we would have ideally liked to have been at. This is because of delays and liquidating some of our current assets in the revenue streams that we are closing. We consider this to be a short-term issue, and we will fully liquidate our current assets in the revenue streams that we are closing by the end of the year, and this will bring our working capital back to our target levels.

Capacity / Assets Turnover Ratio: 8X of CapEx

Aditya Sen: Sir, what would be the revenue potential of the CAPEX that we are going to commission by the end of this year?

Aditya Rao : We typically aim to have an asset flip of eight on an annualized basis on the CAPEX that we spend. So, the revenue to asset flip is about eight. That’s what we are adding. And the vast majority of our CAPEX is at that level.

Historically … they have been in business with say 1.50% and they hit their margin in last Quarter they are reaching. 2.75%!!! Their aspirational PAT margin @ 5%

I think one of the reason is they are highly diversified business and 2nd may be because they are cyclical business.

But management seems to focusing on few products as mentioned in their concall.

“So, solar EPC is not a sector that is identified as a major growth area for us. We have strong

capabilities in that business, and we have a strong order book in that business as well, but the

businesses that we would want to grow year-over-year 5 years from now make them, build them

into multi-thousand crore businesses each of them, that would be the PEB business or hydraulics business, PGI, tubes, engineering services, and a process equipment. And all of those have the

potential to all be multiple thousand crores, and if we focus on them, we will be able to scale.”

I am very new in these forum. Posting first time. I have been studying this company from few days and wanted to update things here in these company.

They are second largest pre engineered building maker in India. With a big growth opportunity in the same, management is doing a greenfield and brownfield capex. They have a US presence in the same with only 1% market capture, they have large room to grow there too.

Their other three core sectors Precision tubes, Engineering services (highest margin), hydraulics, are high margin and growth products.

Management is focusing on improving PAT to 4% from current 1.5% by improving product mix by increasing sales of high margin products and introducing new high margin products.

Pre Engineered Buildings (fastest growing business) (core)

Solar EPC

Products

Engineered Components Business (Core)

Engineered Components Business

Automotive Components, Braking and Suspension, Auto Electricals, Chassis & Body, etc.

Hydraulics Cylinders

Precision Sub Assembly Parts. Sheet metal components, assemblies, machined, welded & fabricated components.

White good Components, Product for Rotary and compressor Shell, Tecumseh, Emerson Climate Tech India LTD, Venus Appliances.

Solar Panels, Pennar Industries has set up a 2 Sqft state of the art photovoltaic solar module manufacturing facility, 250 MW Per annum

Steel Products & Profiles (capacity: 240,000 MT per annum) (Core)

a. Cold Rolled Steel Strips (CRSS)

b. Cold Roll Formed Sections(CRFS)

Electrostatic Precipitators Electrodes (ESP), electrostatic air cleaner is a particulate collection device that removes particles from a flowing gas (such as air) using the force of an induced electrostatic charge.

Purlins

Roofing / Cladding Sheets

Decking Profiles

Metal Crash Barriers

Sheet Piles

Automobile Products, sheet metal products for the Automobile Industry

You will attend next concall of the company and also read out earlier calls.They are focusing on margin improvement and Management in the same direction. From Low margin business to high margin sustainable business model.

Update

Share pledged by Pennar Holdings Private Limited (holding 15.57%)

Total share pledged 2.8% or 15,00,000 out of 5,36,33,327

Overall 1.11% pledged of share outstanding.

Pledge value is not big. But have to look into the reason for pledge.

not at all to worry about , its for working capital . they use LC instruments . company is sitting on close to 150+ Cr in cash . they can take out the pledge it in a flash

Q3 Results are good. They achieved 10% margin which is 2017 level. From the next quarter PEB new plant will start producing from Feb 24. So, revenue growth will be there from next quarter. Re-rating expected.

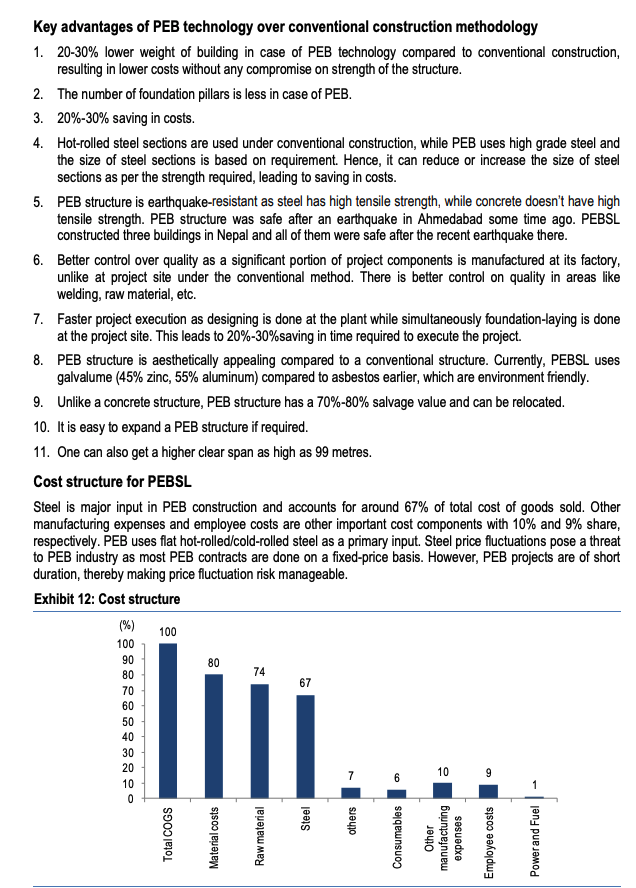

It’s 15% versus 28% (Contribution margins). From an EBIT point of view, we expect going forward about 10% in India and about 15% in the US for the metal building business.

US market leader in this space : Cornerstone or Ukor. They usually do 6%-8% EBIT margins.

For Pennar :

And our engineering is all done in India for that. While we have our design teams there, most of the high manners get done in India. And there’s significant cost arbitrage based on that.

Another reason why our margin would be a little bit better than their margins would be the fact that we can also backward integrate into other metal products. So our more diverse steel buying experience also gives us an additional margin.

Lower Cost Advantage for Pennar vs Market leaders in PEB