733 crores of new orders in this quarter?

1 Like

Q4FY25 Conference Call Summary

- Expecting a double digit growth in PEB segment, Ascent, Boilers and Process Equipment.

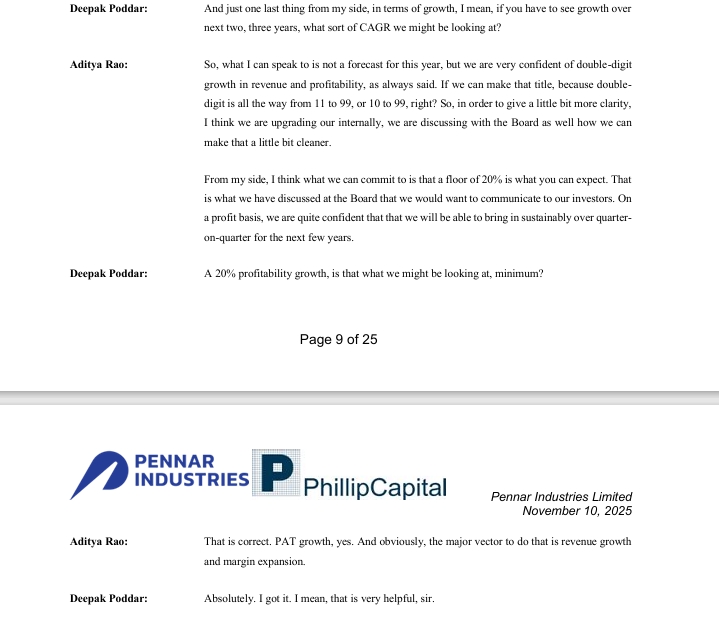

- Expect margin improvement due to increase in higher margin products, working capital days to reduce to 72 and long term target of 60 days. They are confident of strong double-digit profit growth. Over the next 3 years a 200 bp improvement in PBT is achievable.

- Targeting D/E to be 0.7 in the long term and interest to net sales to less than 4%.

- Order book for PEB India business is 780 crores, US business is $53.1 million. The India and US business are completely independent and most parts for US are sourced and produced locally (5% is imported which they can pass on). Hydraulics however has an overlap.

- US PEB business has quicker execution timeline and margins are significantly higher compared to India.

- The 10% gap of ROE and ROCE is due to interest costs and working capital days. They have a long term target of 30% ROCE which they will achieve by reducing the working capital day and growing their EBIT by selling higher margin products. However there would still be 5-7% gap due to interest cost structure.

- 100 crores capex is confirmed for the fiscal.

- Engineering services is not expected to improve the topline significantly but more of a margin enhancer.

- The de-prioritized segment which includes railways, steel, etc. contribute 35% of the consolidated revenue.

- Acquiring Telco which is a structural steel fabrication company located near Birmingham, USA, a promoter driven business with a revenue of $25 million and healthy margins.

- The PEB market in US is $8-10 Billion while the structural steel fab market is even more which helps them open new revenue stream.

- It has been approved by the board but not yet completed, planned to complete the deal in next few weeks and revenue stream from next quarter.

- Long term target to have a A+ credit rating.

- Peak revenue from Raebareli plant would be 36000 tons per annum which would be 38 crores gross sales aka 30 crores net sales per month

- Current capacity utilisation is 60-65% and once it reaches 75% they will look to expand.

Disclaimer: Tracking

20 Likes

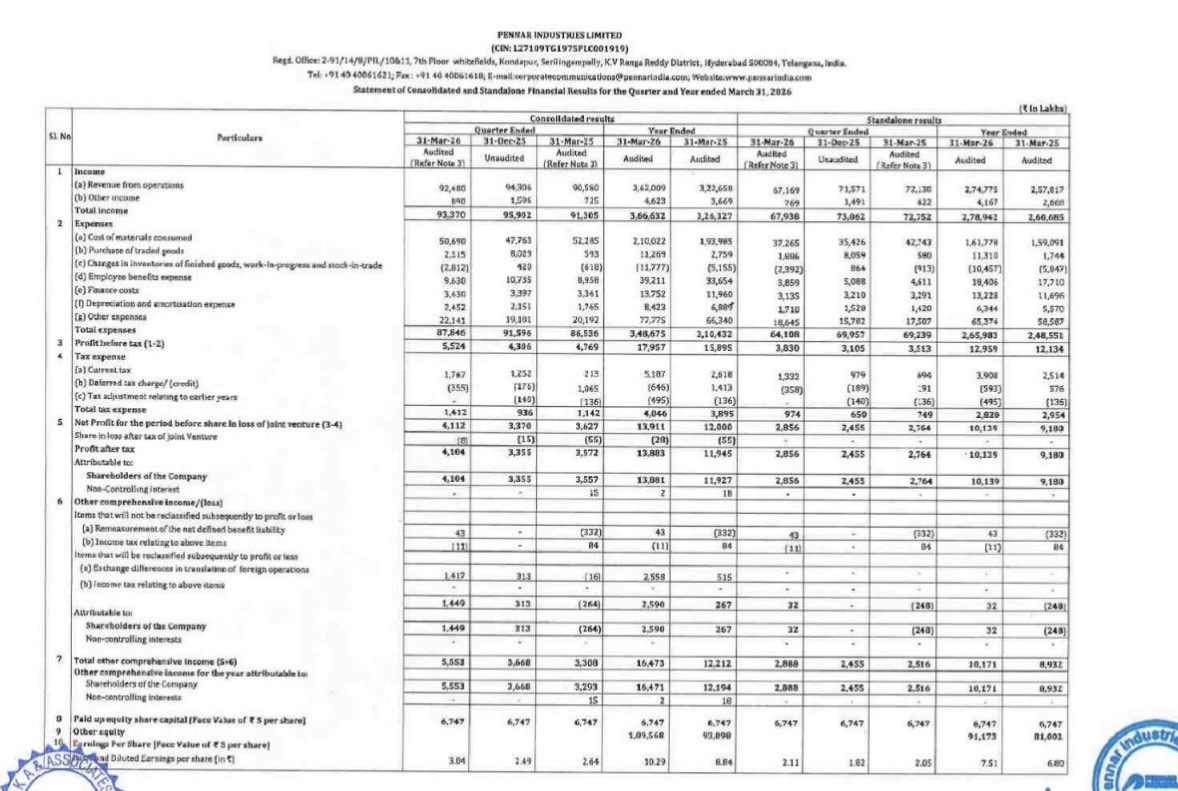

Results declared

Honestly results look disappointing compared to its peers

Also missed guidance by management on margin expansion.

4 Likes

It’s a bad miss.

Pennar very rarely declare results on Saturday. I kind of figured they had missed some numbers somewhere when the result dates were declared!

3 Likes

Management was very confident of good revenue and profit growth in the coming quarters.

Steel price increase is a concern. Anything else that has come up taking all the stocks in this space down??

3 Likes

so Pennar issue warrents worth 50 crore to promoters, and promoter pledged 31 lakh shares to bajaj finance to get personal loan of 50 crores

does it mean, they are investing this 50 crore to buy warrants?