Oh ok. In that case, I might look at this as a harbinger of good news. Only one thing that can make them raise funds, in my opinion - concrete headway into US market ![]() . But yes, better to seek out mgt reasoning.

. But yes, better to seek out mgt reasoning.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/4c4d956c-6434-422f-b49e-9d0a28266935.pdf

Good Q2 results.

2 Likes

Hi @Chins , Great write up on this company.

I have few questions on the numbers: If anyone can help here:

Design led sourcing segment:

Should One think it has happened because of JV turnaround of margins from negative to 4 - 5% margins ? 80 - 300cr pat in last 3 years ? Design led sourcing PBT are sustainable that means this 300cr PAT will be sustainable going forward ?

Coming to Brand Management and SAAS:

Brand Management → As you said it is 250-300CR EBITDA Opportunity.

SAAS → 200 cr PAT Annually.

How this numbers are achievable ?

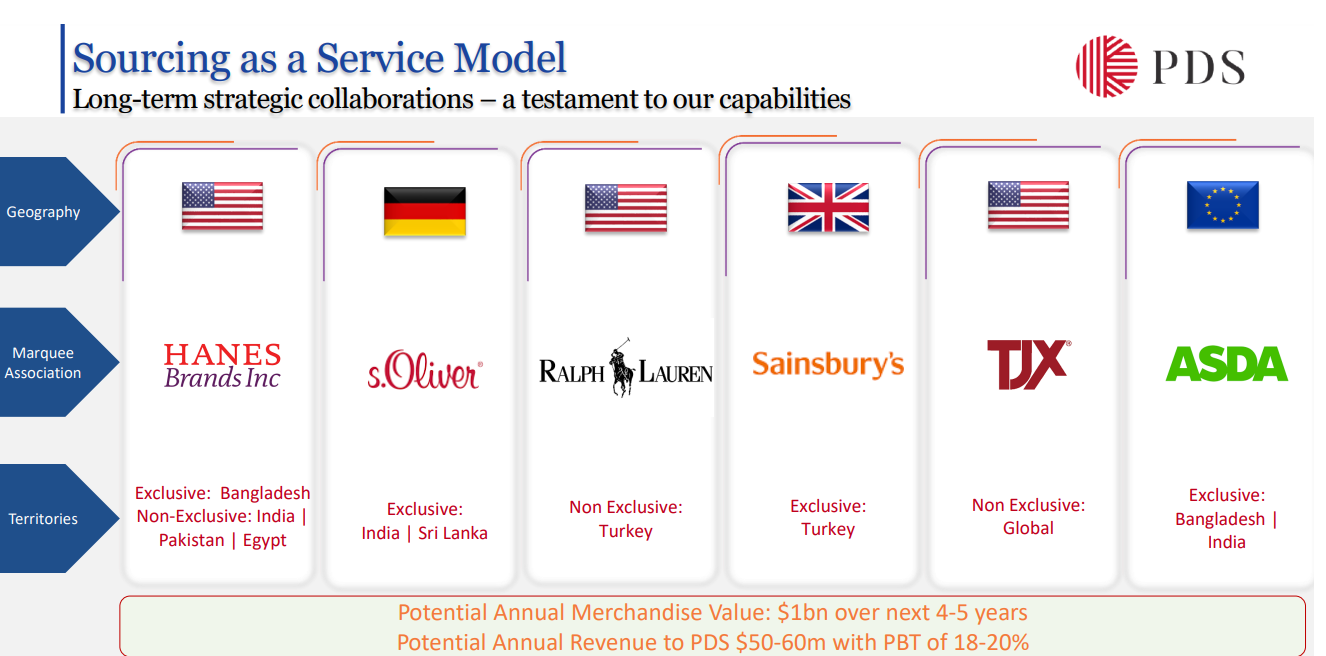

For example: Attaching the below screenshot:

It says potential revenue of 350 - 450cr annually and PBT of 18-20% i.e 70 - 100 CR PBT.

Likewise, on Ted Baker monthly revenue is shown below:

Roughly if I take up monthly 50-60cr so annually it comes around: 350-400cr.

and PBT as - 35cr.

Based on current deals: SAAS and Ted baker deal ~ New offerings it is on annualised basis PBT of => 35 + 70cr => 100cr - 120cr PBT Annually.

Above are for Fy24/25/26 annually for current order wins.

For long term horizon: (Not looking on QoQ)

On 500cr-1000cr PAT in next 3 to 5 years.

According to me, this can be achieved with more deals. Current deals won’t make them achieve 1000cr PAT and their top 10 verticals needs to be scaled up. That needs to be seen. (More revenue from poetic gem etc…)

Huge respect for Pallak to create PDS like platform. His journey has been inspiring. Looking forward as Pallak said, company is at inflection point.

Below snapshot:

Thanks for writing the thread @Chins Your work on this has been amazing !!!

Anywhere you see numbers aren’t making up. Do correct me.

Thanks.

2 Likes

any specific reason why the are degrowing from last 3 quarters be it in sales or in profits YoY?

Slow-down in Export market. Compare result for all textile companies .

1 Like

Saurabh Mukharjea has added PDS ltd to the “Little Champs” Portfolio. Full interview here which covers PDS ltd among other cos

Link to the video

2 Likes

Can anyone reply what could be impacts of Bangladesh workers unrest , which resuled almost 85% export from here. Since company having major present in Bangladesh.

1 Like

@Chins thanks for the work you put in!

Was trying to do some digging from my end as well, could you point me to the source where management talks about 1000cr PAT by 2027

The cost of acquisition and the PAT of the acquired entity are not commensurate ?

2 Likes

As per the disclosure its a subsidiary of ASDA stores. Probably a sourcing arm based in Turkey. It may not have any assets. I think it would be more like a sourcing contract. As for ASDA, the PAT mentioned may be a very small amount, which would make sense for them to outsource the activity to a specialised company like PDS.

4 Likes

I have listened to management saying 2.5billion dollar target revenue and improving pat margins to 5%, which gives you 1000crs in PAT. by fy27 is what they had said, but may be by fy28 given the current slowdown

1 Like

Any thoughts on the above news?

2 Likes

Can someone explain me why EPS is down by 50%yoy Fy24 over Fy23 when the PAT is down by 34%.

market cap is at 5800 crores while Full year PAT is at 203crores this should work out to PE of 29x, However screener shows PE of 40, why is this so?

I see there is no dilution of equity capital either

1 Like

Ah got it it has to do with non-controlling interest

1 Like

Even if they were to make 1000crore PAT i am not sure how much of this will be attributed to the owners of the business as there non-controlling interest as share of PAT is going up, Any experienced investors who can help calculate how much of this will be attributed to shareholders?

2 Likes

Good information about the company, business model.

2 Likes

I have gone through their annual reports, investor presentations, concalls, online videos, full form of PDS is never mentioned anywhere. I guessed it as Pallak Deepak Seth Multinational, asked the IR team for confirmation they never got back. Doesn’t have bearing on the company’s performance just on my sense of completion.

1 Like

What are non controlling interest?

PDS is an aggregation of subsidiaries. PDS ‘the company’ has a controlling stake (usually around 75%) in all its subsidiaries. The other shareholders (usually the entrepreneurs) in these subsidiaries are non-controlling interests.

The sales and earnings you see are the cumulative sales and earnings of all the subsidiaries. Of that, the propoportional amount to its shareholding is attributed to PDS.

5 Likes