7 Likes

Some questions (please excuse me if they are silly, I began studying PDS only recently):

1 HBS case mentioned 80% success rate- how has this number changed over time? One would expect it to rise as they learn from experience, and also as they enable collaboration between subsidiaries. Any idea whether this has happened?

2 What is the difference between design led sourcing and sourcing as a service?

3 Their average wallet share with top customers? How much of the customers’ design/sourcing is done by PDS?

4 Any update on sale of PDS tower (24 Cr book value)?

5 They mentioned investments raising 2nd and 3rd rounds at 2x valuation but have they had any exit events (M&A/IPO) in any venture tech investment?

6 Any answer on reason for doing unrelated venture tech investments like fertility clinic and indoor cycling?

7 Mr Pallak Seth’s LinkedIn says angel investor

Is this same as venture tech investments of PDS or are there any angel investments in personal capacity too?

Disc- no holdings as of now, tracking closely

PS: Kudos to @Chins on his excellent work on PDS!

6 Likes

Great questions :)

That was the point of a few posts just above. I’m tracking subsidiaries made after 2017 to understand if their CAGR / profile is different from subsidiaries formed in 2014. Will write an update after adding in FY22 annual report data.

Great question, and my next task in Q1FY23. Was hoping to meet management to ask them this instead of working it out myself, but I’ve been lazy. Please join me in working out their right to win globally, and data on your question, and how it’s changed in the last 5-6 years.

My current understanding is based of Q2FY22’s concall, where they discuss venture tech investments as selling points to clients, and proof of concepts for their sustainability initiatives. I’d be surprised if any of them delivered an exit, and treat that as a back of the mind optionality.

I completely forgot about this. Please bring pitchforks to the AGM on the 29th, or Q1’s concall ![]()

I think if there were investments in a public capacity, it would show up on CrunchBase or Tracxn. Will dig deeper!

5 Likes

Sharing some interesting snippets from interviews:

“I’d rather invest in people than plant and machinery-that has always been my motto”

(All Seth and done - by Richa Bansal - Fibre2Fashion)

(A case study in crisis management – What next for PDS Group? - Just Style)

12 Likes

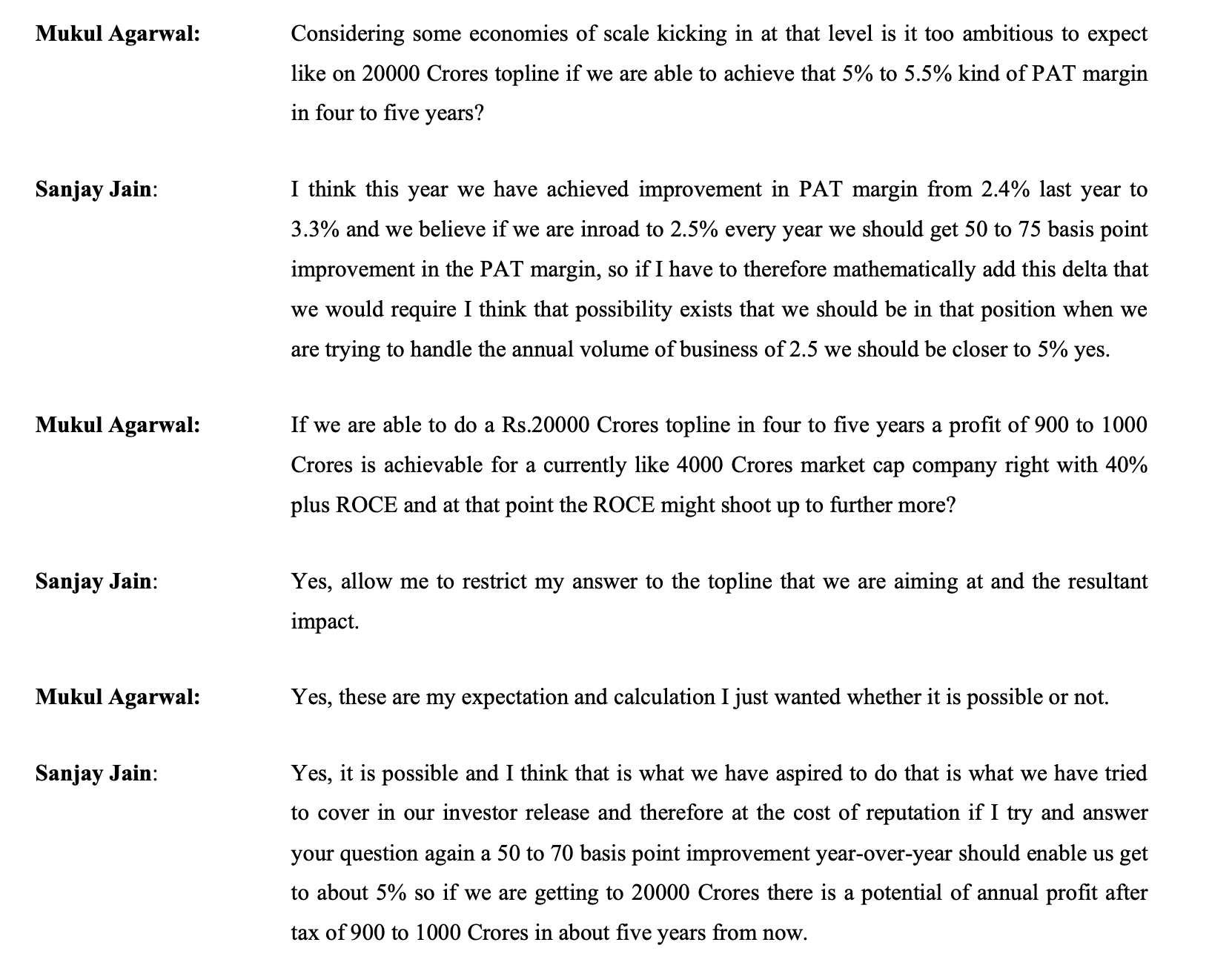

Did anyone attend the concall? Any notes?

78 bps improvement in gross margin

73cr EBITDA, 113% improvement, 102 bps improvement

ESOP charge 7 cr vs 2 cr y-o-y

12 crore investment in new business – expensed from P&L

Sourcing clocked 42% growth, 60cr EBIT, RoCE 42%

Manufacturing continues to be profitable (1.6% PAT margin)

Net Debt 77 crore, NWC increased from 2 days to 3 days

Will continue to focus on monetising non-core assets

Continue to focus on increasing US focus

China + 1 helping as people looking beyond China/Vietnam-Hong Kong relationship. Movement to sourcing from Bangladesh/Sri Lanka is helping PDS (one of the biggest reason is governance standard trust in PDS) fill up this vacuum. Vietnam also we are trying, we are late to the party, but doing not bad.

Whenever recession happens, we double in size as we help both retailers (one stop shop design free delivery) and factories (working capital + orders).

We have business, now with softening cotton and freight as well as currency depreciation, will see margin improvement.

80-90% budget is booked – strong orderbook – confident to meet guidance – cautious because of geopolitical issues

Seasonality of Q4 strongest – so QoQ not relevant

8 Likes

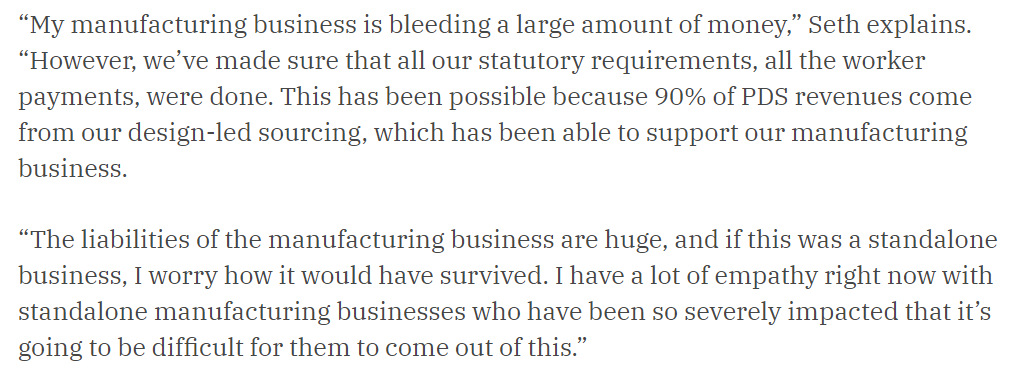

Since textile industry itself is struggling, can PDS be immune to recession in the sector? That too since PDS is positioning itself as a manufacturer rather than trader / service provider.

2 Likes

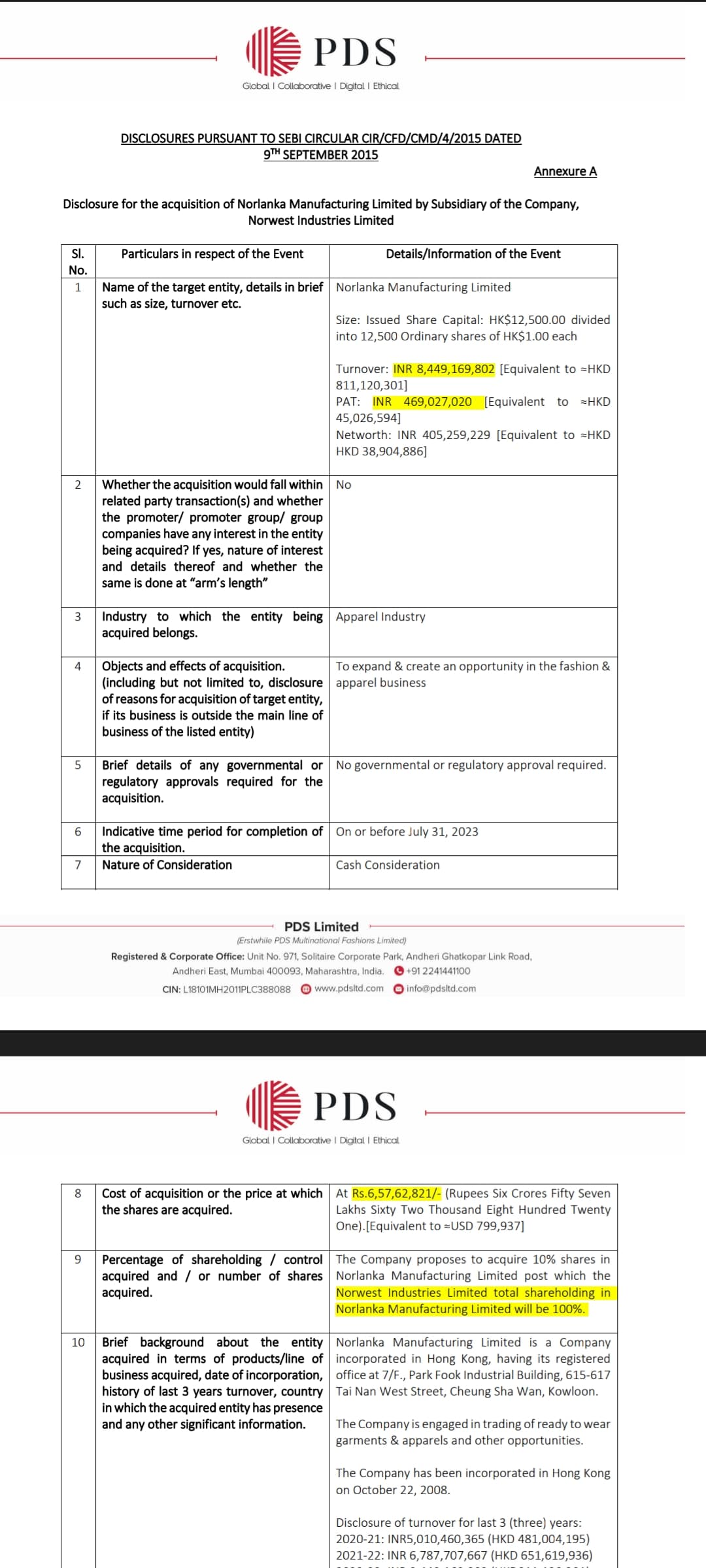

PDSL’s subsidiary acquired 10% stake in a company doing Rs.844 crores in turnover and Rs.46 crores in net profit for just Rs.6.57 crores.

Now they own 100% of it.

This seems too good to be true.

Who sold their 10% stake at just a valuation of 1.5x PE?

Though they were minority shareholders but 1.5x PE sounds absurd.

0fea6d43-ba0d-40a8-aac1-69f8e30fa068.pdf (335.9 KB)

4 Likes

Agreed that the cost of aquisition is very low. They haven’t disclosed much about the seller so can’t tell much. Maybe they were distressed seller. Norlanka Manufacturing Limited is a sourcing partner for many global brands.

They have made another aquisiton of 24.99% Class A shares in Green Apparels Industries Limited. I was not able to confirm if Green Apparels is a sourcing company or a pure manufacturer.

I see that the sourcing part of PDS is the money making segment with best ROCE. Norlanka being a sourcing partner is a great value add for the company. If the same is true about Green Apparels, it would unlock immense value for the company.

Looks like PDS is using this industry slowdown as an opportunity to aquire stake in companies at a discounted valuation.

The key metric to track is the balance sheet as it has considerable amount of receivables, inventory and debt.

Disc: Not Invested, but might add.

6 Likes

A fantastic thread on very interesting company. Better than any brokerage report in my opinion. It’s a complex business with a lot of moving parts, and estimating the growth or assigning value to the consolidated entity is no easy task.

The company seems to have some sort of competitive advantage, is generating cash, has negative working capital, and is run by a seemingly competent management. One concern I have though, is that the proportion of non controlling interest is growing.

As shown in their investor presentation, it was around 15% in FY22, rising to almost 19% in FY23. It is essentially dilution of equity. I suppose this is a consequence of the business model Pallak Seth pursued, of offering equity and creating subsidiaries for competent people to grow the business. But it does lead to the question- is this the only way the company can grow? How much dilution will happen as the company grows? And will it significantly affect minority shareholder returns?

I would be grateful if some of the experienced investors could share their thoughts on this.

Disclosure - Not invested. Tracking, looking to invest in future.

8 Likes

Slight decrease in performance (with management expecting next few quarters challenging) and 1 yr’s returns get wiped off.

PDS proposes to acquire New Lobster Limited (Ted Baker Brand), UK through its UK subsidiary for Rs.150.51 crores.

7 Likes

I presented a summary of my investment thesis, and all the key updates from the last year to Valuepickr Europe. This is a recording of the presentation, and subsequent discussion.

53 Likes

Hi Chins

Well made thesis. Can you share the links to the case study (and other reading material) you mention in the video? Also, your basis for saying it is available at < 4PE of FY27?

There has been a lot of interest in the HBS case study. I’ve uploaded it to this link:

17 Likes

Looking for more info on the CEO ,Mr Sanjay Jain in past was associated with ZEE group, Future group & Avantha group. All 3 had CG issues .

7 Likes

Latest Company Presentation.

Really beneficial to understand and scale of company operations.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0fb3f95c-3330-4a25-a391-fc24dee8eef9.pdf

7 Likes

Latest company filing for Board Meeting has one of their agenda as ‘The proposal for raising of funds…’

I find this strange as it was only in the May '23 concall that Mr Pallav Seth had mentioned “we are not tapping the capital market for further expansion.”

Between may & October, 5-6 months have passed, at least at my corporate i have seen strategy change every 2 months, strategy changing in 6 months is reasonable. If they are raising funds, most likely for a significant capital deployment opportunity. So need to hear management out to build independent opinion whether it’s good capital allocation or not

4 Likes