A very thoughtful analysis. I m watching this business and had similar questions in my mind. Their margin is very low that bothers and it’s decreasing Y-o-Y. I guess we should watch for improving.Aldo , Having 600+ supplier and partners makes it like a platform or integrating type business . Simply They are connecting every one and earning fee like marketing fee. Sometime brand’s would like to work directly or at the end no-one will make money .due to competition.

1 Like

Their sourcing as a service segment has higher margins, in design led sourcing the entire merchandise value is accounted to the topline and hence the thin margins, whereas in SAAS only the actual commission charges is reflected into the topline. Also operating leverage can kick in with SAAS as the existing employees and network can do more than what is being done now.

Game changer would be if somebody like a Walmart uses their SAAS segment for all their apparel(textile) needs.

Disc: Invested, patience has started to wear.

4 Likes

This is a very good write up on PDS.

Is there any timeline to achieve the 1000 Cr PAT that the co is targetting ?

Their PAT margins seem to be around 2%. So going by that they will need a revenue of 50K to reach a PAT of 1000 Cr. And I am talking about the overall PAT here not the one accrued to shareholders.

So unless some operational leverage plays out and their subsidiaries start contributing positively to the bottomline and push the EBITDA margins to early double digits and PAT margins to 5%, these nos seem far fetched.

Investing in FD would earn more than double of what PDS is earning if we go by their PAT margins.

1 Like

They guided for 50 dps of incremental margin expansion year on year, so by 2027-28, they should have 4-5% PAT Margin

1 Like

Did they mention what will lead the margin expansion? Anything apart from the product/service mix?

1 Like

It is combination multiple factors, such as operating leverage kicks in, fixed cost such as employee expresnes getting observed by higher revenue recognition, new vertical such as Brand management and SAAS are higher margin business which are growing and becoming bigger share of the pie. Interest Cuts are expected this year, which leads to low interest cost expense.

So basically they have guided for 2.5Billion(20K crore rupees) dollar revenue and margin of 5% PAT by 2027, that’s the basis for 1000cr PAT, and also so far the management has been walking the talk, about first half of prev FY being drag down, then the flat/recovery at the second half. Investing in business and talent while the industry was not buoyant. I liked these qualities in them

Them being a Platform business augur well for the shareholders IMO.

3 Likes

I would say PDS is operating in a cyclical industry that’s going through a downcycle. Demand is yet to be revived. Poor cycle brings with it a lot of opportunities as well. The company has been able to increase its stake in many manufacturing companies( esp in Sri Lanka. They have also been able to sign many sourcing agreements with major brands. I would say PDS is in a growth phase now and with the cycle turning so will its fortunes. Company has also published an investor FAQ which explains the business well.

PDS Investor FAQ.pdf (1.4 MB)

Discl: Invested. Have purchases in last 30 days

5 Likes

Based on latest quarter, Profit Growth of PDS is bit concern here. They talk about order book inflows more than 30% , but profit growth too less when compare to current year.

PDS have released their Investor Day Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d7d4e6ae-3884-49ed-a6cf-8276a63278ee.pdf

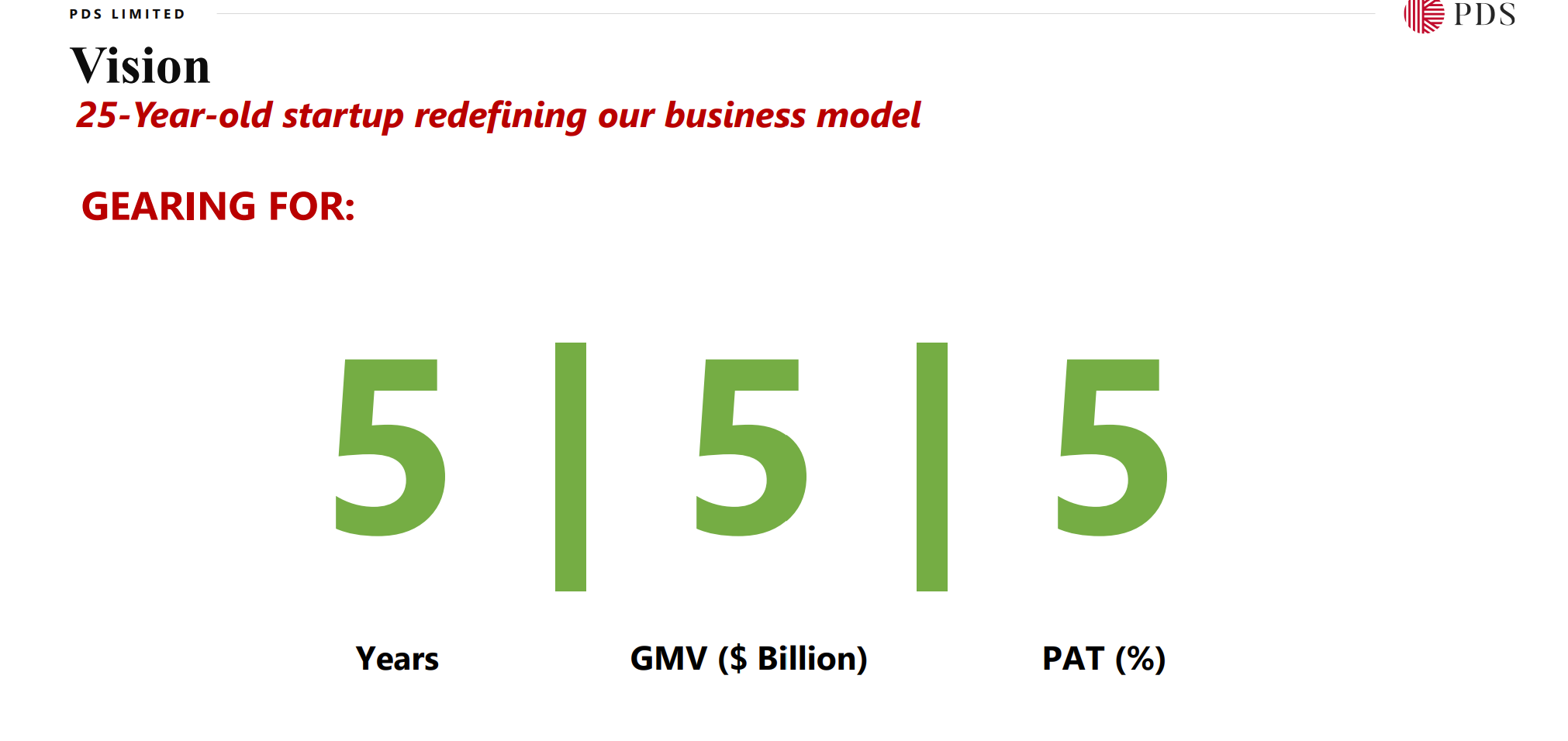

What amazes me is this slide

If they are really able to pull this off in next 5 years then we are onto something big

2 Likes

Initially i was excited, about this, however, then i realised, the 5 billion GMV part might not translate in Revenue, especially in the sourcing as service part , so need bit more clarity on this, if any of our member(s) have any better understanding who has attended the Invester day conference, kindly give us some sense.

Second point is, By 2027, they were suppose to be 2.5B with 1000cr profit , atleast that was the thesis, i was working with, and as per their guidance, is that they plan to increase 50dps in PAT margin every year, which should amount 4-4.5% PAT margin. Now it was kinda feels like delayed.

Disclaimer:

Largest position in my Portfolio - biased to do well

3 Likes

Let me try to add some context to this. Let’s go over the sourcing as a service(SAAS) business query first. So GMV is not reported as the topline for SAAS business. PDS earns a service fee for the volume of the business it manages and that service fee is reported in the topline. The Gross margins for SAAS business is 100% and EBIT margins are around 38%. Last year SAAS contributed 1% to the topline. Based on the numbers that the management was quoting on the Investor day, my guess is that the service fee is around 2% of the total order. Last year PDS managed around 700 million USD worth of sourcing for George and Asda. 2% of that comes to around 14 million which is around 116 Crores in Rs and that is around 1% of the total topline of 10500 crores. This year they would be handling around 1 Billion USD in SAAS for Asda and that lead to a meaningful topline of 20 million this year. They have also added Myntra in India for SAAS business. So I don’t think GMV is reported in the topline for SAAS business.

Coming to the 2nd question on PAT margins. The PAT margin is at 2% based on last year’s numbers. But management said that the actual PAT margin is actually 3% because they have reinvested 100 Cr back into the business to forge new partnerships in other businesses. They don’t want to raise debt and put load on their balance sheet. They are going to utilise money out of the bottom line every year and reinvest as and when needed. So it is debatable and depends on you how you want to perceive that. If you add 0.5% growth in the PAT margin every year then it will hit 5% in 4-5 years time if you consider 3% as the PAT margin for last year.

Overall I would say that the Investor day was very insightful and I got to learn a lot about the business and understand lot of things which I would have never figured out otherwise. MDs of Poetic Gem, Simple Approach and North America region gave a good detailed presentation on their businesses and vision going forward. Things look promising on the face atleast.We will have to see how things shape up.

3 Likes

@dm88 Can you make detailed summary of your learnings and insights you have got at Investor day presentation.

Also, i am aware, that SAAS part of business earns in commission rather than the GMV itself, what i wanted to get a sense is that, how much of that 5 Billion dollar GMV, translates to revenue, Let’s say SAAS GMV CONTRIBUTED 1% of the total revenue now, in the next 5 years, what could be that number.

As per second, point if we take 5% PAT margin as target in next five years means, if they add .5 percent every year, then i guess the PAT margin gets stagnated after 2-3 years right ?

Since they are platform business, i was presuming that the margins will improve, even though not at the pace it used to, still 200-250bps makes huges difference in bottom line given their huge volume in nature of revenue.

(Although I am happy if they just maintain the margin, if not expanding after 5% on a steady basis, bcoz market likes the stable margin business - like a consistent compounder)

1 Like

I will try to summarise the minutes of Investor day meeting over the weekend.

As to which vertical will contribute how much out of the 5 Billion ambition, they said Manufacturing will be around 5%. They are betting big on Branding business and the goal is to make it a Billion dollar business so that would be 20% if they manage to grow it to 1 Billion USD. Rest 75% would be distributed between design led sourcing and SAAS. They did not give precise numbers around that and asked to connect offline for details.

For Branding, North America projections are very ambitious. They are not expecting any revenue from Branding from NA till 2025 and then 200 million in 2026, 400 million in 2027 and 800 million in 2028. So we will have to see how that plays out.

For SAAS, the more lucrative thing is the ROCE. ROCE is infinite because PDS does not invest a single penny in this business. So I don’t see this business as a margin game. It is more of a volume based game where the ROCE will be on a higher side and working capital will always be on the lower side.

Moreover they have PDS ventures through which they invest in early stage promising businesses. Right now I think 6-7% of the earnings go into this and some of their investments have already become 10x from the time they invested. So they would be strategically planning to take an exit as and when feasible. This would generate some cash in the books. The goal is to make PDS ventures self sufficient and stop feeding off the earnings of other verticals.

They are also expanding into homeware category and they already have some orders for that. So even with PAT margins stable at 5%, it is going to be a huge boost to the bottomline. Let them hit their target of 5-5-5 first and then we can see where things go beyond that.

4 Likes

I m more eager to see on their first target which is 2.5B dollar revenue with 900-1000cr PAT.

In 2022, earlier they guided to double their revenue in 5 years (2.5B), However, now they are guiding to achieve 5B GMV by end of FY-2029. Although not all of them will translate into revenue, even if we take out the SAAS part let’s say roughly 10-20% of total GMV, still they should clock around 4-4.2B in next 5 years, which translates into revenue CAGR itself around 25%, (effectively doubling their revenue itself in every 2.5years). Added wtih PAT margin expansion comes into play bottom line improves much faster , assuming 5% at the end it should be around 1700-1900Cr of PAT at the end of 5 years.

Not sure how much of it will play out as we expect, Ofcourse the risk would be another industry level slowdown in next 5 years, which will delay their target, @dm88 ,

do you think any other risk that could play out in Your opinion, or have anyone else at the Investor day presentation has asked about it?

Note: As per their presentation, the only risk was mentioned is reputation, and in general pallak seth seems to more risk averse , they seems to manage it well so far and walking the talk. If things play out then i expect 10 bagger in next 5 years.

1 Like

I am not really sure what % of GMV converts to revenue. For FY 24, GMV was 15000 Cr and revenue was 10000 Cr. So 67% GMV got converted to revenue. Now they said FY24 had 25% GMV growth over FY23 in Q4 concall. So for FY23 GMV was 12000 Cr and revenue was 10000 Cr so the conversion was 83% there. With SAAS business picking up and contributing more, this conversion would go down further and I am not sure how much out of 5 Billion would actually convert to revenue. If we assume that 50% of 5 Billion converts to revenue then it will be 2.5 Billion USD. Last full year revenue was around 1.25 Billion USD. So it is just doubling the revenue in 5 years and with 5% PAT margin on a revenue of 21000 Cr, PAT comes around 1050 Crs. This is 5 times current PAT so we will end up with an EPS of ~50. It will need a highly premium valuation of 100x to become a 10 bagger from here in the next 5 years. Ofcourse the above numbers are based on assumptions and we need to get a sense from the management as to how much of those 5 Billion USD would actually translate to topline.

Somebody from this forum who has done more research on the business can throw some more light on this. It would be really helpful to dissect this better and get a sense of where the business is heading. I am hoping that 5-5-5 strategy is not an eyewash.

1 Like

My initial question was on 5-5-5 strategy only, but i don’t think so it’s an eye-wash, at the same time it is not something exceptional either, however, the revenue will be around 2.5B coz that they have guided to achieve in FY 27 , so five years from now see it won’t be as low as 50% realization, even with the exisiting growth they should reach, 3-3.5B (given this FY24 is a downcycle year for the industry, so i presume it should be around 70-75%), in next 5years, @dm88 , since i don’t know. and can’t get definite sense of what revenue realisation of GMV will be, thought you would have already asked that to the management.

In the long run SAAS revenue is a good thing, this means high ROCE, and bottom line grows faster than the top line. Also having high ROCE is always a good thing. Even though High ROCE business are always attract competition, but in PDS case i think their moat will be quite stronger by the time market realises it strength and it ll be harder for the new company to breach. Hoping to hold this stock more than a decade, would like to be part of their journey as pallak seth asked too in the long run.

Anyways requesting our valuable members, if anyone can get in touch with management offline or may

be on the next con-call, it would be great to track their progress.(@Chins @Vineetjain111 )

Note: It was @Chins writeup which got excited me into this company. He has made wonderful write-up and detailed video about PDS. Thankful for that. As far as i know, there are three people i would follow to get a sense of PDS. chins, vineerjain, and sahil sharma. May be they no longer track this company, still i learned about this company , and ofcourse through concall too (especially pallak seth).

3 Likes

Did anyone attend the AGM earlier today?Would really appreciate if someone can summarise the findings and if there are any new interesting developments apart from what was said on the concall! Thanks in advance!

A great thread on this unique business in India. Many people have contributed diverse views and its helpful for others to understand the business as one go through the thread.

I have known about PDS for some time now. However, today I decided to read more about it. I went through the above 98 comments in this thread. The thread started in Oct ’21. As I went on reading, parallelly I also used screener to see how (financial) performance has moved and how share price has moved.

I always liked the business model of PDS. A unique business in India providing platform to global customers and suppliers. So I wanted to study this company before I decide to invest. (I was almost certain I will invest in this company). After studying this company for past 3 hrs. I am certain, I WON’T invest in it. Why? Because there is no margin of safety in current valuation (downside is not protected) and upside is in imagination. Errr… Management guidance.

My first suspension developed when I read company will start manufacturing operation in Bangladesh. But why? PDS was demerged from Pearl Global to focus on SAAS model whereby manufacturing business remained with latter. Then why go back into the same capital intensive, labour intensive diversification? The logic of “state of the art factories” doesn’t justify starting a vertical from which they were separated in the first place.

For the past 3 yrs (since this thread has started), share price appreciation of ~100% is only because of rerating. There is no increase in profit (profit has actually reduced).

Rerating seems to be because of management guidance of $2.5Bn revenue by FY27 $5bn revenue in 5 yrs (5-5-5 guidance). A game of guidance works wonder in bull market.

For FY24, PAT margin to a laymen investor will look like 2% (i.e. 203 / 10373). However, it seems management think this is 3% after doing some financial calculation. I wonder what will be actual PAT margin when management will say 5% in FY29 (provided they reach there).

In US, they will grow multiple from 0 revenue in FY25 to $800 mn revenue in FY28. I never knew doing business in US is so easy.

A simple business that started as SAAS has spanned out into multiple verticals having too many moving parts.

As a reader, I am sure you will sense sarcasm in this post. My point is, this investment looks good because we are in a bull market. When the tide turns, there might be nothing but memories. I am sure many will not agree with me (and they shouldn’t). But that’s the whole purpose of this forum to have diverse point of view.

Disc: I am a devil’s advocate.

27 Likes

How will it be a catalyst?

They have some manufacturing units because of some regulatory needs. Or else they are also not interested to set up manufacturing units.