Any updates on the meeting with management?

Some comments on the results.

-

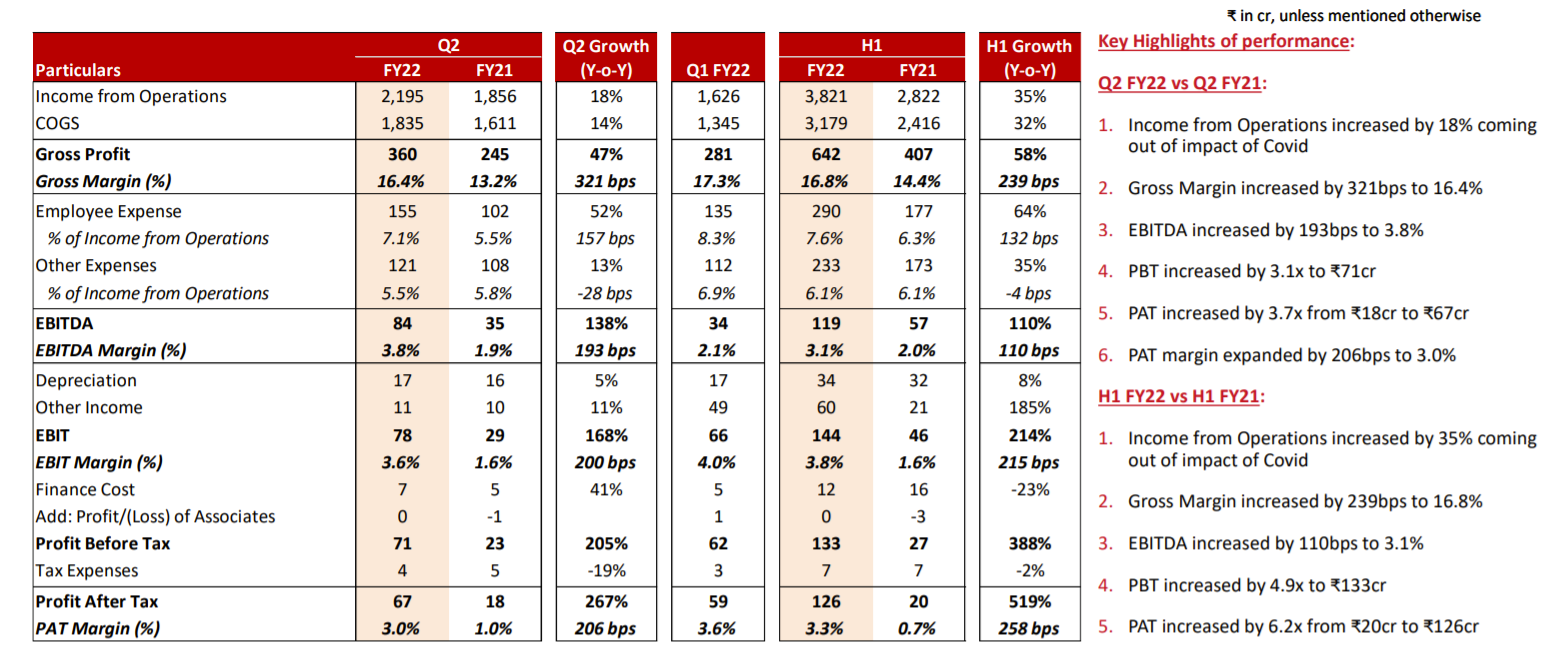

The gross margins are key, because the management sees this as the true revenue. Good to see gross margins increase, H2 should be the stronger half of the year and should see gross margins being between 16.5 - 17.5% (read post 1).

-

They brought down the losses in manufacturing by 85%, lowering it by 34 Cr, almost half of the PAT. Losses are now 6 Cr.

This trigger is playing out as we speak:

The annualised run rate from the current quarter is 240 Cr, going into H2 where Q4 is usually their strongest quarter.

-

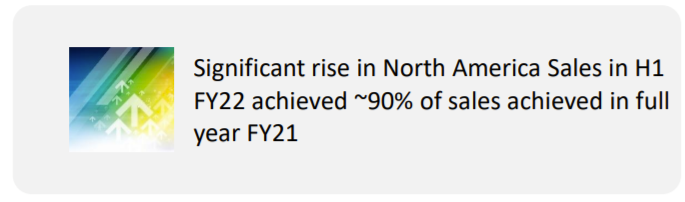

The two people they’ve brought on to improve sales in the US are on the right track.

-

Return ratios are improving, should see a consolidated RoCE between 35-40% by the end of the year depending on how the manufacturing facilities pick up. RoCE was 17% in FY21.

Unfortunately I haven’t been able to find time due to the difference in time zones and work schedule. Will definitely post here after something pans out.

Disclosure: invested

The Q2FY22 concall is one of the best presentations I’ve listened to amongst my portfolio companies (coming a close second to Ugro Capital’s concall this quarter). Lots of insight into the business model, and really pertinent questions from investors.

A lot of questions asked in this thread have been answered in detail, such as:

These are the highlights of questions answered during the concall, I was thinking of posting snippets, but would have ended up posting all 16 pages of the concall.

-

Why Bangladesh is so important to them - I’ve realised that thinking of Bangladesh as a way to increase margins completely misses the point. Bangladesh’s compliance setup ticks every single sustainability box for retail clients, making it one of the few such (low cost) facilities in the world. It’s not just for profitability, it’s a selling point.

-

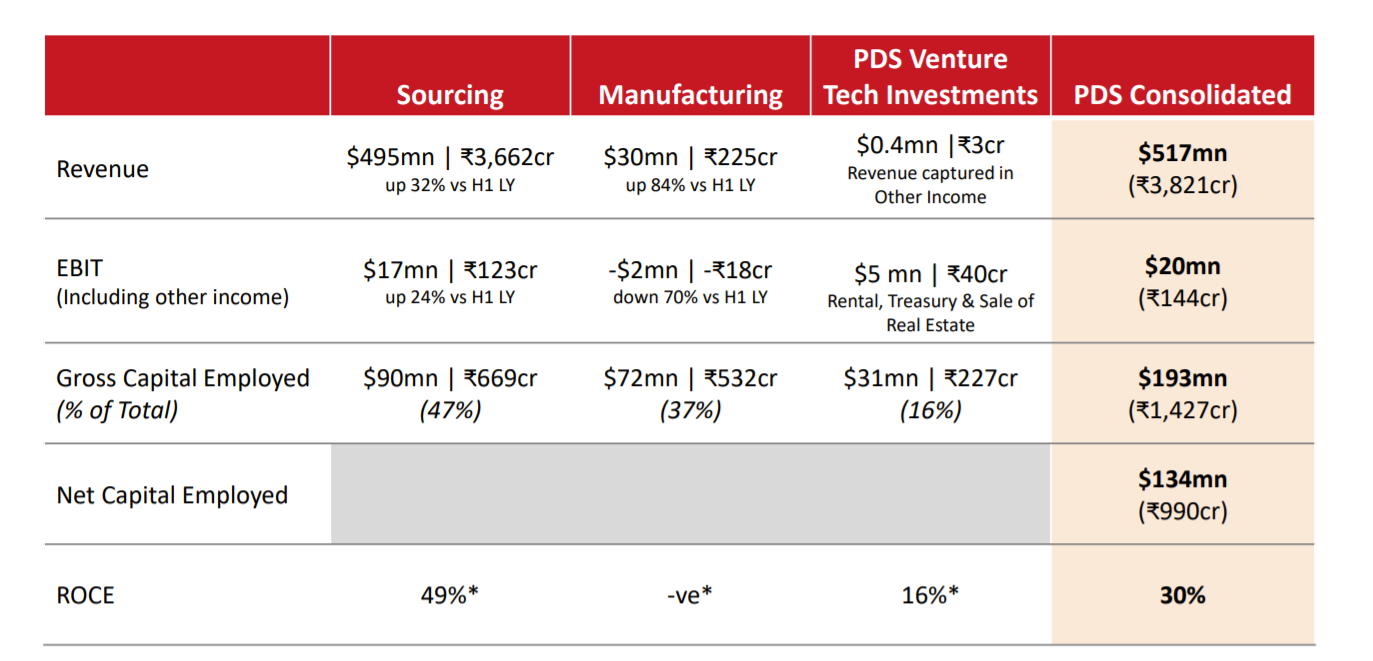

How one reconciles @Investor_No_1’s dichotomy between an asset light platform company, and also having manufacturing plants.

-

How Covid has impacted the industry, and what enables them to have no inventory, pre-sell all orders, and have the coveted negative working capital business model for their core business.

-

The timeline for Bangladesh’s profitability, how losses were down from 40 Cr. Q2FY21 to 6 Cr. Q2FY22. What full capacity top/bottom line can look like.

-

Their guidance of 12-15% growth was conservative due to covid. They’ve clocked in 35% growth in H1FY22, and are guiding a strong momentum for the rest of the year.

-

How the entire process of a sale works from start to finish, and why customers keep coming back to them.

-

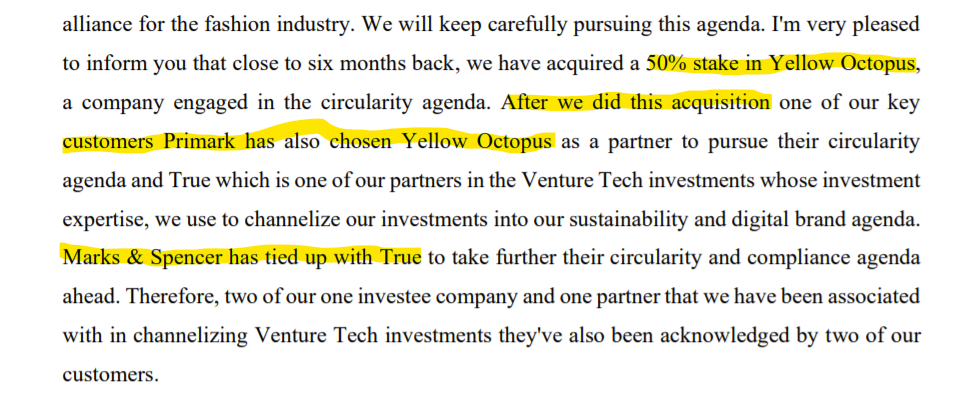

@Lynch The venture fund is not a traditional VC fund at all. They invest in these companies and buy from them as clients. They then take these technologies to retailers to further cross sell, start initiatives helping themselves and the investee companies. Win win.

Posting just one more snippet as a preview, but recommend going through the concall to have details about these 7 points.

I found an informative video on the Bangladesh plant, with nice visuals of the plant:

Limited.")

-

Is located within a special export zone with very close proximity to road, sea and air links. Enjoys a tax holiday for five years by law.

-

In 2019, they said goals for the plant were to hit 600 Cr. of revenues by FY23. Current run rate is 450 Cr. well on track.

-

Lots of details on the kind of infrastructure investments they’ve done, including wifi enabled sewing machines which provide real time data on needle points.

PDS Concall.pdf (391.3 KB)

PS: New improved website https://www.pdsmultinational.com/

Some pointers:

Recent pickup, could be cyclical as textile companies across the board have done well with the bullswhip effect setting in.

Is the “take-rate”/ gross margin revenue model appropriate?

Negative effects of having a complex structure - high compliance costs. Yearly legal fees - stands at Rs100 crores+ crores, rather large for a company of this size.

Complicated company structure makes following the money trail complicated.

Promoters took home more than the profits in “consultancy fees” through tax efficient payments.

292 crores of cash lying in current accounts - not exactly a problem, but the company has debt and pays interest at around 10%. Hence, cash on hand loses value.

The “platform” narrative and startup investments display a trend-following mindset.

Thanks for posting the article, given the limited amount of literature on PDS.

I think the author is quite dismissive of the startup fund, without justifying why they think it’s a narrative. The same holds for their take on the manufacturing plants.

But some really nice potential anti-thesis pointers on the cash held, and consultancy fees. Thanks for flagging them

Whether the start-up fund will do well is something we’ll get to know only in the future. It could do exceedingly well, given the power law returns some funds generate.

Rather, the issue is the timing of the fund. The company decides to become a VC right when we’re creating unicorns by the dozen, and the private markets are hot. And of course, the “platform” narrative was also peddled when it became a hot trend among investors.

As for manufacturing ,the reason for moving away from a capital efficient and flexible business model (sourcing)

, into a business model that requires high WC and ccapex and is quite unflexible is beyond me

Subject to approvals New Name to be: PDS Limited

INVESTOR PRESENTATION https://archives.nseindia.com/corporate/PDSMFL_08122021145153_Ltr_InvestorsPresentation_08122021_Upload.pdf

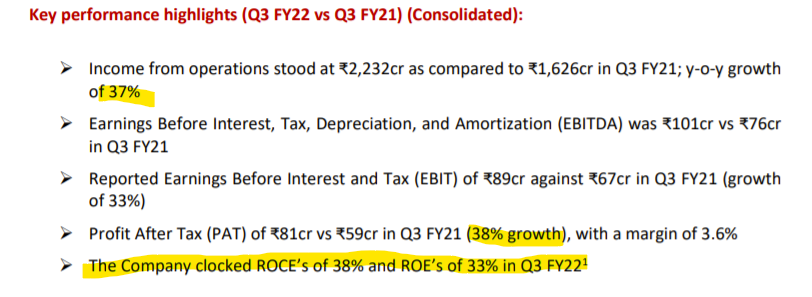

PDS posted an outstanding Q3FY22.

One of my key investment themes revolved around the reduction of losses in Bangladesh. My argument was that a reduction in losses would have a large impact on PAT improvement, and RoCE improvement.

This is playing out right now:

Other highlights from the quarter:

-

Has a negative working capital of 2 days.

-

Gross margin is down, this is management’s KPI. Need to understand why.

-

Debt is down from 206 Cr. to 26 Cr., almost debt free with a debt/EBITDA of 0.08.

-

Signed an exclusive deal with Hanes for sourcing, is an opportunity worth 3000 Cr. over the next five years.

-

s. Oliver sourcing deal has the potential for annuity revenues of 375 Cr.

-

North America business has gone from 9% of the topline two years ago to 16% of the topline TTM. Please see below post, and Q2’s concall for more information.

- Manufacturing segment has clocked quarterly revenues of 157 Cr. Order book is full for Q4. Annualising this run rate gives us over 600 Cr.

Link to investor presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/320556c7-fe09-4ccb-955d-d43a25c50d24.pdf

Will write further updates after the concall.

Disclosure: Invested, biased. Not a SEBI registered advisor, not a buy recommendation.

Q3FY22 Concall Highlights

- New business verticals have dragged down EBITDA margins, excluding these new investments, EBITDA margins up 48 basis points. Have a model for new investments that is a lot like capex.

-

Offering sourcing as a service. TechnoDesign, a German subsidiary signed a deal with s. Oliver for exclusive sourcing via India and Sri Lanka. This partnership has potential for 375 Cr. annuity. Similar deal for Hanes via Bangladesh with a higher opportunity size.

-

Manufacturing losses are down by 85% in Q3, YoY.

-

Now have negative working capital days of -2, compared to +10 days in FY21.

Q) More guidance on Hanes/s.Oliver deals?

A) Will take us 3 years to get to annuity of 375 Cr. We took charge of operations in November. Target is to do 60 Cr. by March 2022, and scale up from there. On Hanes, have a dedicated management team for this deal. We expect 5 years to get to the peak run-rate, will take a few months to start contributing to the top line of the company.

Notes: 375 Cr. annually translates to 94 Cr. quarterly. Hitting a runrate of 60Cr. by march is more than halfway there.

Q) Thoughts on domestic manufacturing? Do you see yourself putting up further capex, and what kind of profitability do you forecast in this segment?

A) We have a strong order book, utilisation and ramp up have allowed us to target profitability in Q4. In the near term, we target 3% PBT of sales, internal targets are 5% PBT at the end of next year. Our core business is the sourcing business, we’re inclined to continue sourcing first, and have our eyes and ears open for opportunities that come this way.

Notes: At 600 Cr. topline, manufacturing can deliver 18-30 Cr. of PBT annually depending on ramp up, compared to the losses of 20 Cr. presently.

Q) What kind of growth rate do we expect in FY22/FY23?

A) We gave guidance of 12-15% because of uncertainty in covid. There is a strong order book for Q4. FY23 will be a growth year, but we’ll maintain 12-15% guidance until we can put the pandemic behind us, and then we’ll give stronger statements.

Q) If our sourcing becomes stronger, will there be a chance for us to build our own brands?

A) We’ll always remain a sourcing partner. We are very conscious of capital employed. Will take up niche opportunities, like Lily and Sid, using the Ajio platform. We’re also following the D2C space through our investments, but these will always be a single digit % of our topline.

Q) Please tell us how the US business improved. What clients?

A) Kohls, TJ Maxx, Target, Macy’s were onboarded, we strengthened our relationship with Walmart. Our goal is to work on our relationships with larger clients, not add on as many as possible.

Q) Did these companies move from another company to us?

A) Some of these like Hanes used to do sourcing in-house, but have now shifted to us. We’re noticing that these companies are becoming more scared/aware of sustainability in the supply chain, financial stability of the sourcing partner, and global reach. This vigilance is motivating customers to shift from sourcing partners that are not ranked in these aspects to PDS, which ranks well in these scores.

We don’t do a price game, our strategy is not to get a foot in the door. we win the business on our strengths and offerings rather than on price.

Q) Volumes are not large on the indices, is there any possibility of a split?

A) Our endeavour has been to present better data to our investors and have deeper disclosures about our business, we listen to concalls to feedback, and will take this home to think about.

Questions from OldBridge Capital

Q) In the manufacturing business, what are the fixed costs?

A) In a well run manufacturing setup, one can expect 35% gross margins and 7-10% PBT. Numbers in between, 25-28% are operational costs - manpower, administrative costs of running a factory, and in the journey of efficiency, this improves and we bring down costs. 12-15% will be employee costs.

Q) Who are your peers that your clients choose from?

A) Most of the competition is from in-house sourcing teams. I don’t portray the manufacturing in terms of a topline opportunity. We offer flexibility in our network. If our clients want fast fashion, we have Turkey. In Kidswear, there’s Sri Lanka, and then there’s Bangladesh. We can cater to any need.

D: Invested and biased.

For those of you who enjoy reading Prof. Bakshi and the Safal Niveshak blog, professors at Harvard wrote a case study on PDS! This is a really nice read, and a refreshing difference to the usual analyst report style take on a company.

They sat down and spoke with management, and the point of this article was to create a case study for the classroom, and not dissect a business as an investment candidate. However, we do have more candid answers for some of the questions asked by people in this thread.

Case study is behind paywall.

https://www.hbs.edu/faculty/Pages/item.aspx?num=58910

Summary and takeaways:

- Industry changed immensely from the Rana Plaza collapse / fires in Bangladesh, earlier post is definitely on the right track: PDS Limited - A platform for entrepreneurs - #10 by Chins

- In the wake of these fires, and the stricter compliance requirements in the industry, management is quoted to have said: “Some of the big retailers—Gap, Levi’s, H&M—won’t work with sourcing companies anymore. They will only work with companies that own factories.”

Aside: Companies like Primark, H&M are now publishing transparent data on all of their partner factories. They require factories to have worked with them for atleast a year, and follow compliance standards. They also require factories to disclose data, such as the breakup between men and women employed.

Here’s PDS on Primark’s sourcing list https://globalsourcingmap.primark.com/:

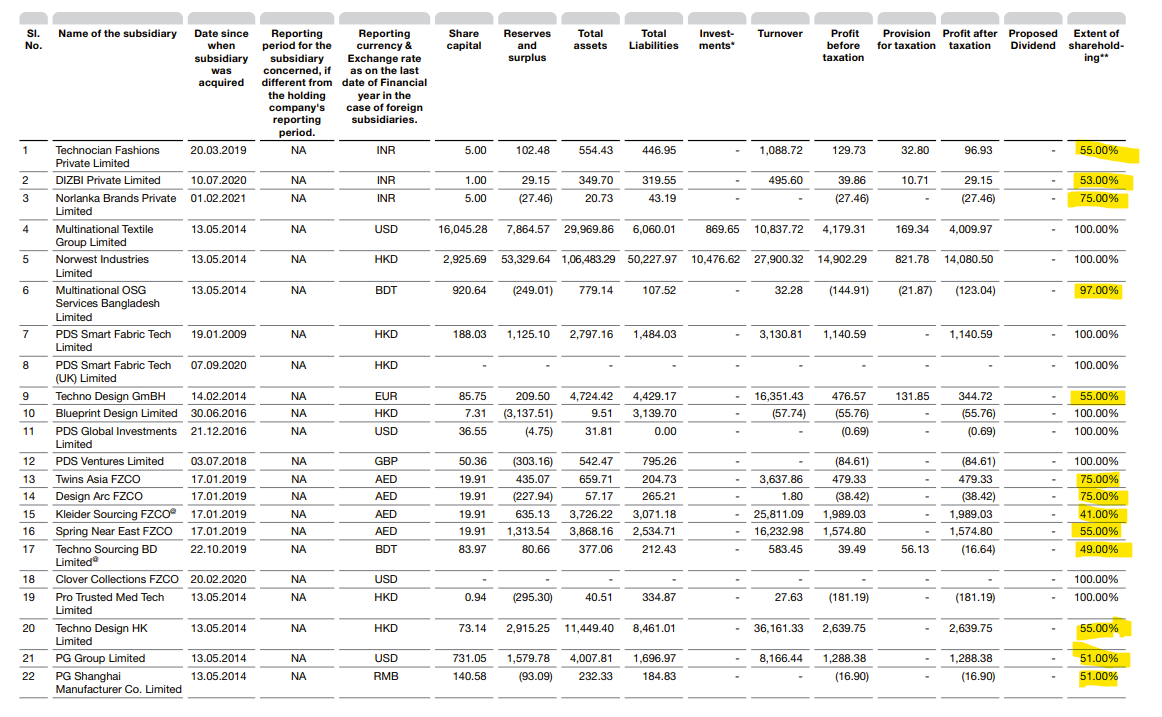

- The reason why we have 100 subsidiaries and a crucial piece of business understanding:

As he grew the Group, rather than acquire companies in the way competitors like Li & Fung had grown, he targeted successful individuals with extensive industry experience. They were often independently running sizeable P&Ls within a larger competitor firm and had varied work experience in sales and marketing, merchandising, design and product development, buying, and manufacturing. Seth brought them in to set up individual subsidiaries under the PDS umbrella, offering compensation and Group support, including financing, IT, and other Group best practices.

- They therefore headhunt people who are senior management/critical to other businesses, and they turn them into entrepreneurs under the PDS umbrella. Requirements for these people are to add product categories, expand footprint into new markets, or bring in a top dollar client.

Aside: this then explains why a lot of their subsidiaries are JVs, or not 100% owned subsidiaries. Each has an entrepreneus as a profit sharing partner.

-

Lots of details about how Mr. Seth picks the entrepreneurs, what kind of initial funding they get, remuneration, and how they have a three year timeline for independent cash flows. Success rate is currently 80%, with the remaining being written off.

-

They have extensive non-compete clauses with existing clients, and honour these with respect to new verticals/products.

Crucial business insight - the platform model we’ve spoken about in this thread so far is between customers and sourcing partners. However, the platform model management keeps referring to is the hub and spoke model with entrepreneurs.

-

Great story about how this model worked initially. and then started to develop problems between 2014 - 2017: had many entrepreneurs under them, and each unit worked independently. This meant lots of missed contracts, as each subsidiary negotiated sourcing for itself, and not the entire group. Top management worked to improve backend, and build a better model.

-

2017 was the turning point for the business, they sat down together and fleshed out corporate structures, how to incorporate transparent decision making across the group, and a better framework. Also, all subsidiaries reported that clients wanted a manufacturing company, not a pure sourcing company. This lead to increasing efficiencies, and the decision to start manufacturing in Bangladesh.

-

In 2018, they brought on multiple key people to do a full diagnostic of PDS. They set up a system where subsidiaries had quarterly forecasts, annual budgeting, management information systems, and set targets for KPIs. They also brought on a former L&F president to benchmark subsidiaries. They also have teams that do internal suprise audits on the subsidiaries to ensure 100% compliance

I believe these are the reasons for the improvement in ratios seen below:

Campbell, Dennis, Tarun Khanna, and Kerry Herman. “PDS: Ring-Fencing the Ranch.” Harvard Business School Case 721-361, September 2020. (Revised November 2020.)

Disclosure: invested, had a wonderful time learning more about the company.

Really nice interview with the founder. He describes his journey, and PDS’ story from 1998. This is almost the same story as the HBR piece, written about in the post just above: PDS Limited - A platform for entrepreneurs - #36 by Chins

")

Notes:

-

After studying abroad, Mr. Seth didn’t want to return to India to the comfort of the family business. Instead chose to move to Hong Kong with his wife to set up a new business there with some initial capital from the family and a few contacts.

-

Won deals by networking, biggest early win was a 10 million dollar contract, company made a 10% margin, which gave them confidence in their ability. After a certain level, he couldn’t scale the company any more, as the bottleneck was time spent entertaining clients / networking.

-

Studied how Li & Fung grew by acquiring businesses. Didn’t have the capital to acquire a business, nor did he see value in acquiring a B2B business. Instead, sought to find talent working for competitors; key people in firms that were essentially running the business, but didn’t have ownership in said businesses. Brought them on board and set up companies with them.

-

From 1998-2005, there were 7-8 verticals (subsidiaries) formed with these entrepreneurs. After more time, the plan formed in turning the group into a platform: let PDS group handle financing, IT, legal, HR, and let the business owners focus on running their own verticals.

-

The allure of being an owner entrepreneur, having a free hand without corporate politics and creating long term value / equity is what brings people onboard the platform. It wasn’t easy in the beginning: he had a small office in HK, had to meet entrepreneurs in a 5 star hotel to sell them the vision and convince them to join. They were senior executives in their 40s, and he was in his 20s.

-

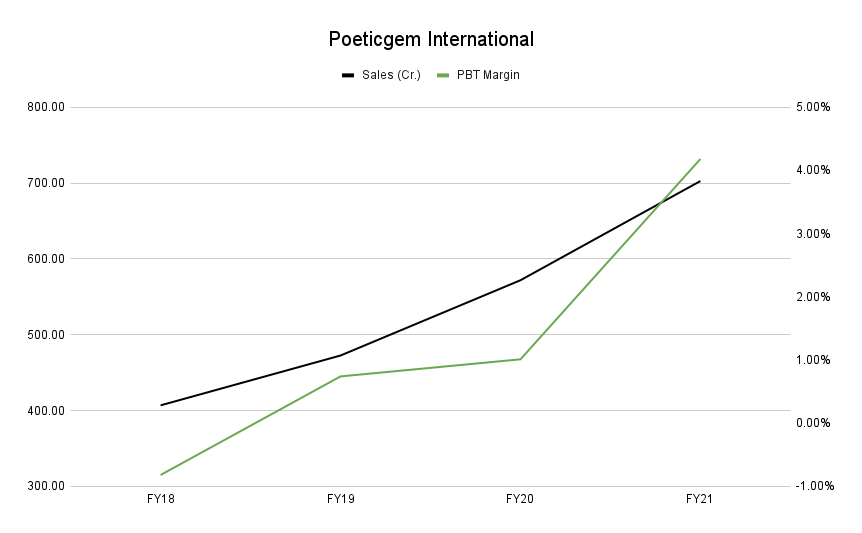

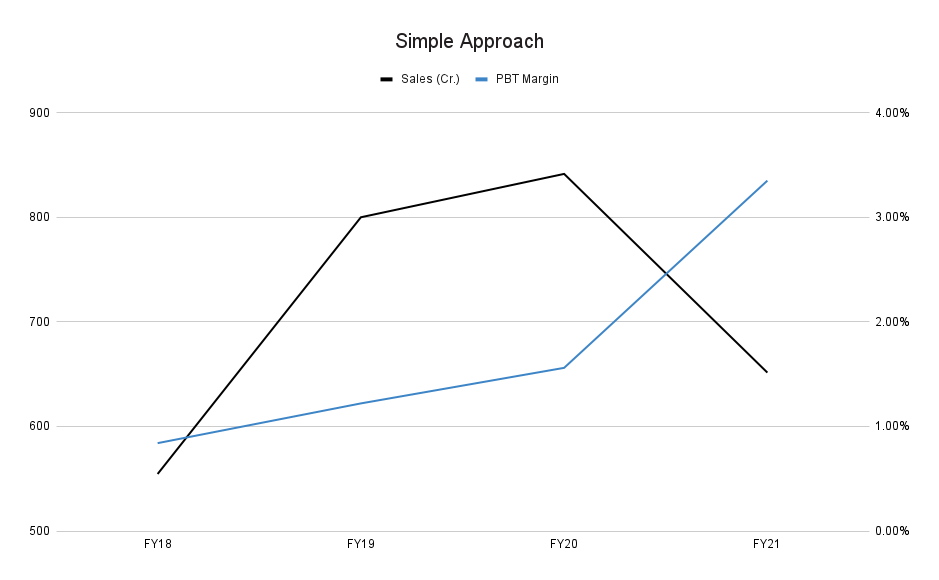

First success story was Sunny Malhotra. Left a big firm to join him in running a vertical. (Subsidiary is called Simple Approach, had revenues of 650 Cr. in FY21.) Used this story to slowly gain momentum in bringing people onboard.

-

Goal is to look for entrepreneurs who are honest, have ambition and the right mindset. Doesn’t matter if they’re in Bangladesh or Chile.

-

If these 60 smart people into one company, they’d kill each other with politics. However because of the vertical structure, they’re focused on their business. They have no worries about the backend. Therefore, their entire attention is on their clients.

-

As a holding company, banks look at the strength of balance sheet and offer support. Would not be possible for independent MSMEs to have the same support without the group.

-

Has a concept of 3 balance sheets for all subsidiaries. The first is a cash balance sheet that’s the conventional PnL. The second is a credibility balance sheet, with suppliers/clients/banks. The third is of capabilities they bring in.

So far in this thread, I have written about how loss making subsidiaries had lowered PAT by about 100 Cr. in FY21. In FY22, subsequent breakeven drove up the RoCE profile from 16% to ~38%, bottomline grew from 84 Cr. to 232 Cr.

What needs to be done:

-

Since my understanding of the business structure has changed substantially from the title post, a deep dive into the subsidiaries is crucial to understand the growth rate, what the margin profiles are for each of them, etc. My plan is to cover this before the annual report comes out, so that one is set up to understand FY22 numbers with context.

-

Results for the company will be declared tomorrow, with the concall happening on Tuesday. As usual, will post notes from the concall, and developments from the quarter.

Good results from PDS. Improvement in ratios. Manufacturing div turned ebit +ve.

I have added to my position. At current PE, many growth possibilities are not fully factored in.

DISC - not a professional, personal opinion, no recommendation…

Initiated position at 1600 level in May 2022

Investment Rationale for initiating position

First and foremost, like the leadership

The potential addressable market is large (tail winds owing to diversification away from China). Short term tail winds due to opening up are matched against short term headwinds of inflation, supply chain issues, logistics and freight issues. Network effects arise as each added group can synergize existing ones. Other competitive advantages include effects of scale - increasing size allows spreading of overheads, Switching costs for large customers is high as they would need to interface with ground level. Hanes deal shows that large groups might prefer dealing with PDS. PDS also taps into macro trends of sustainability and heightened ESG awareness. PDS seems to have studied Li and Fung and the factors that lead to its fall. PDS investments into startups in this space also opens it up for positive blackswan like events.

Monitorable in coming quarters

-

Management has guided fully profitable fy23 for manufacturing div. I will let one or two neg ebit quarters slip may reduce holding if way off guidance.

-

Margin contraction due to continuing inflation and freight issues. Despite these pressures, pds q4 and fy22 was commendable. May have to reduce holding depending.

-

Any new deals and successful execution of Hanes contract etc. Positive news in this regard in spite of margin contraction is a signal to ADD to holding.

Friends, please share your thoughts.

Q4 Highlights + Concall Notes

-

Excellent quarter by any standard, numerical highlights captured above.

-

Tough operating environment on account of cotton prices at multi year highs, freight costs still being elevated, EU seeing a knock on effect of Ukraine, and economic turmoil in Sri Lanka.

-

Shipping has two forms - FOB and LDP. Freight costs do not affect FOB business, but have an impact on LDP. Costs are negotiated ahead of season, so PDS has limited ability to pass on costs when freight costs rise in between next contract negotiation.

-

In FY21, the part of business affected by freight costs (LDP) formed 7% of the overall business. In FY22, it formed 12% of the topline. Goal is to try and do more FOB while freight is elevated.

-

Important case study from Sri Lanka - clients preferred to do business with Norlanka (subsidiary), as group had stable funding sources. Were insulated from crisis as funding comes from Hong Kong. Captured business/market share during this tough environement, competitors did not have access to working capital and some went bust.

-

US forms 16% of the topline compared to 9% two years ago.

-

Bangladesh manufacturing grew 92% YoY in FY22, achieved breakeven in Q4. Goal is to be profitable through FY23 and steadily increase margins from here.

-

Infrastructure improvements - had EY audit digital/IT infrastructure. Recommended standardising global IT system/network. Have outsourced application maintenance to PWC. Assessed group ethics / best practices with Deloitte.

-

Onboarded the following exec as CIO. Has 10 years of experience with IBM as head of analytics:

-

Growth in Q4 is driven by higher volumes, due to winning new businesses and mining existing clients. Management says a lot of small / mid size factories have come under pressure due to covid and inadequate working capital / sustainability lapses. This has allowed PDS to win business.

-

s.Oliver contributed 70-80 Cr. in FY22, Hanes will start contributing from Q1FY23.

-

Overall goal is to move towards gross margin accretive categories. Poetic Brands is a 50% gross margin business in the UK. Manufacturing should make 35% gross margins over time. Aim is to become stronger every quarter, and see benefits of measures taken now only after a few quarters.

-

Investment portfolio was 9% of capital employed. Venture fund is meant to be PDS’ contribution to the sustainability ecosystem, and is key in winning clients with additional optionalities. Goal is to bring this down to 6% in a few years, and hopefully any profits made from this vertical will go back into new investments.

-

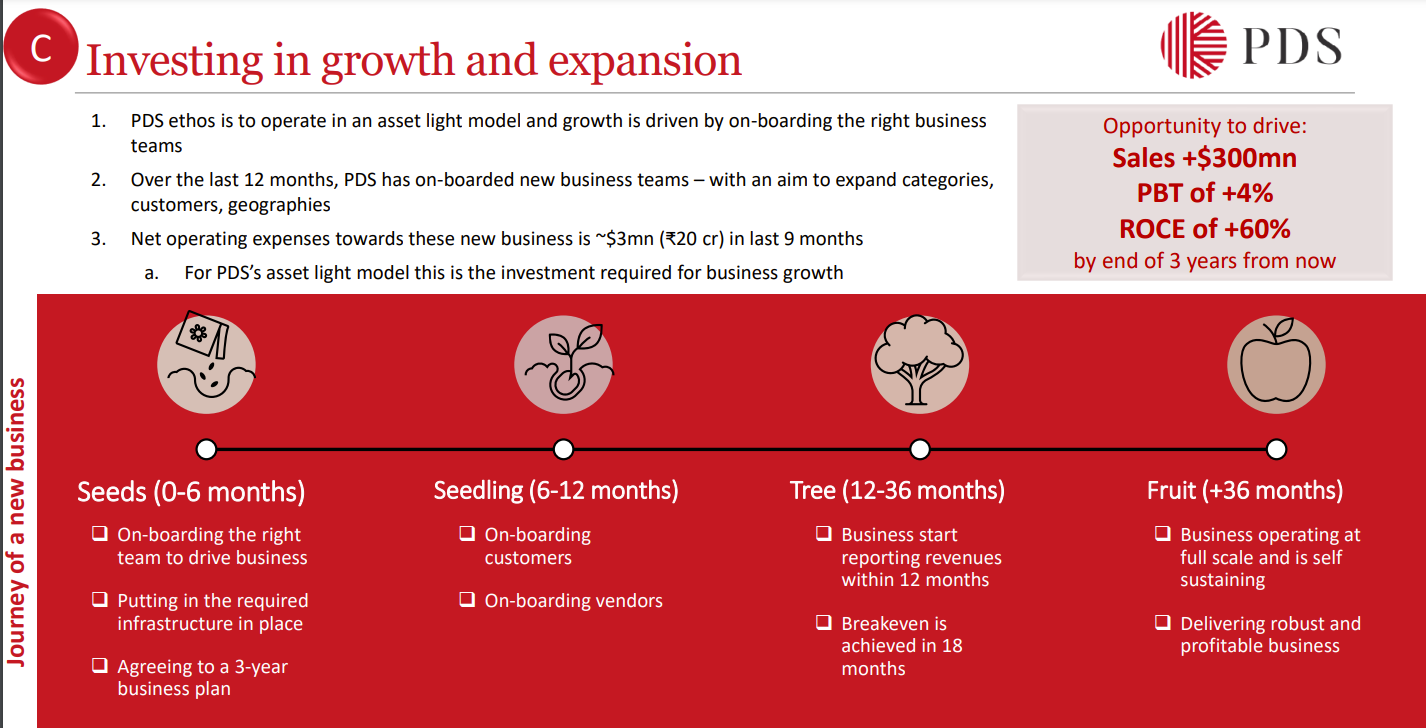

In FY22, new verticals (subsidiaries) contributed a topline of 300 Cr., but a loss of 44 Cr. Goal for these businesses is to do 500 Cr. in FY23 and breakeven. In general, for verticals the internal goal is 2000 Cr. of revenue over 5 years, 4% PBT and 60% RoCE.

-

Guidance for FY23 is 12-15% growth. Internal ambition is of 18-20,000 Cr. of topline five years from now, with 50 basis point PAT margin improvement every year. Goal is to have high RoCEs of 40%+, and eventually a PAT margin of 5%.

Personal investment thesis: The PDS platform is stronger than ever at the moment. 40% RoCE, net debt free and a much sought after negative working capital cycle. They have won incremental business where competitors have capitulated, and they’re agnostic to geographies.

The structure of subsidiaries needs to be done. Some are high margin, others are low margin, and all have different growth profiles, categories and jockeys running them. All due dilligence shouldn’t be done on the platform anymore, but on the potential of these verticals before thinking about a sum of the parts.

I welcome anyone reading the thread to join in this effort, there are 80+ stories to go through.

D: Invested from lower levels, no transactions in the last 90 days.

I begin the understanding of different verticals in this post.

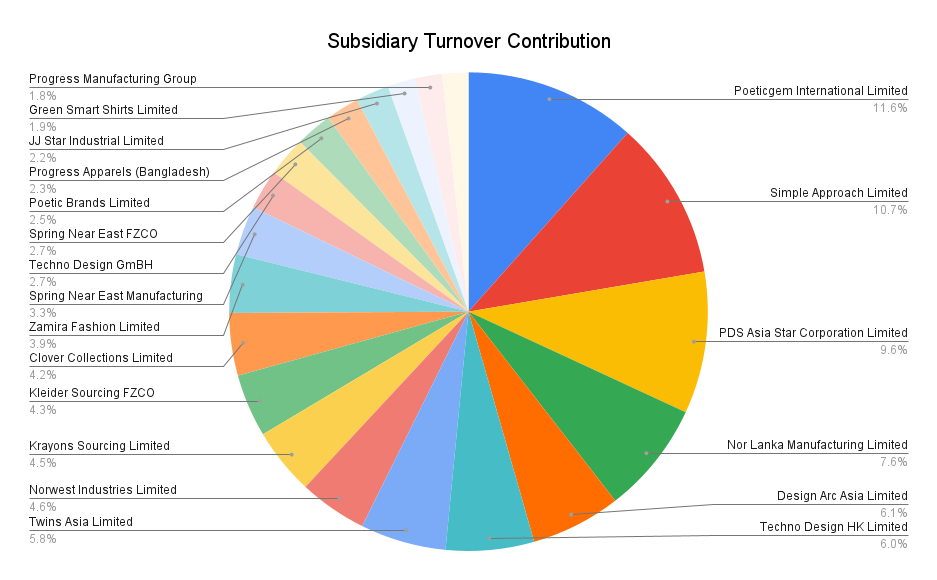

Here’s how each subsidiary/vertical contributed to the topline in FY21:

What I do now is to track each subsidiary from annual reports FY18-FY21 to understand how these verticals have grown.

Reminder, PDS headhunts executives working at other firms, who are crucial to the running of those businesses, and invites them onboard to become entrepreneurs. The model is given below:

Therefore, we expect all verticals to meet the benchmark of 4% PBT, and scale topline successfully. Here is the data for 10 of them in this initial post. Note how some of them show incredible growth, and almost all of them have seen PBT margins improve with time.

-

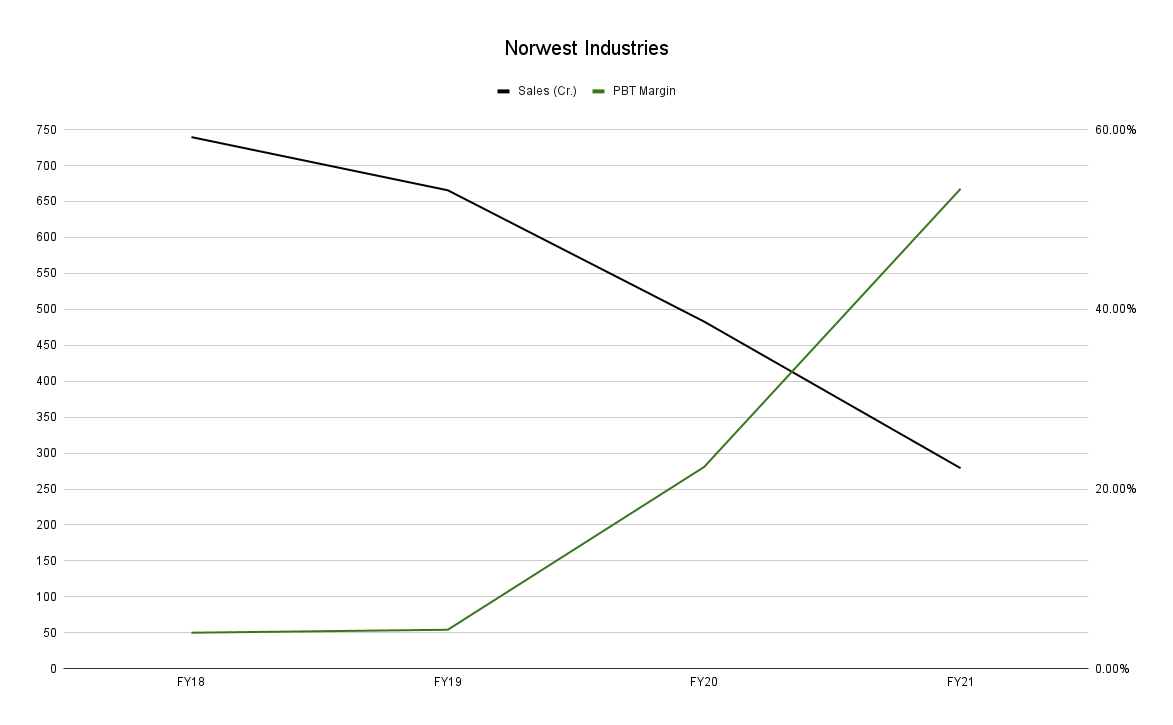

Norwest Industries is the highest margin vertical amongst these 10. They improved margins from around 4% in FY18 to ~50% in FY21. At the same time, topline has fallen drastically at a CAGR of -27%.

-

Multinational Textile Group forms the second highest margin profile, and is a textbook example of their business plan, scaling revenues from 0 to over 100 Cr. in two years. Margins improved to ~38% in FY21.

-

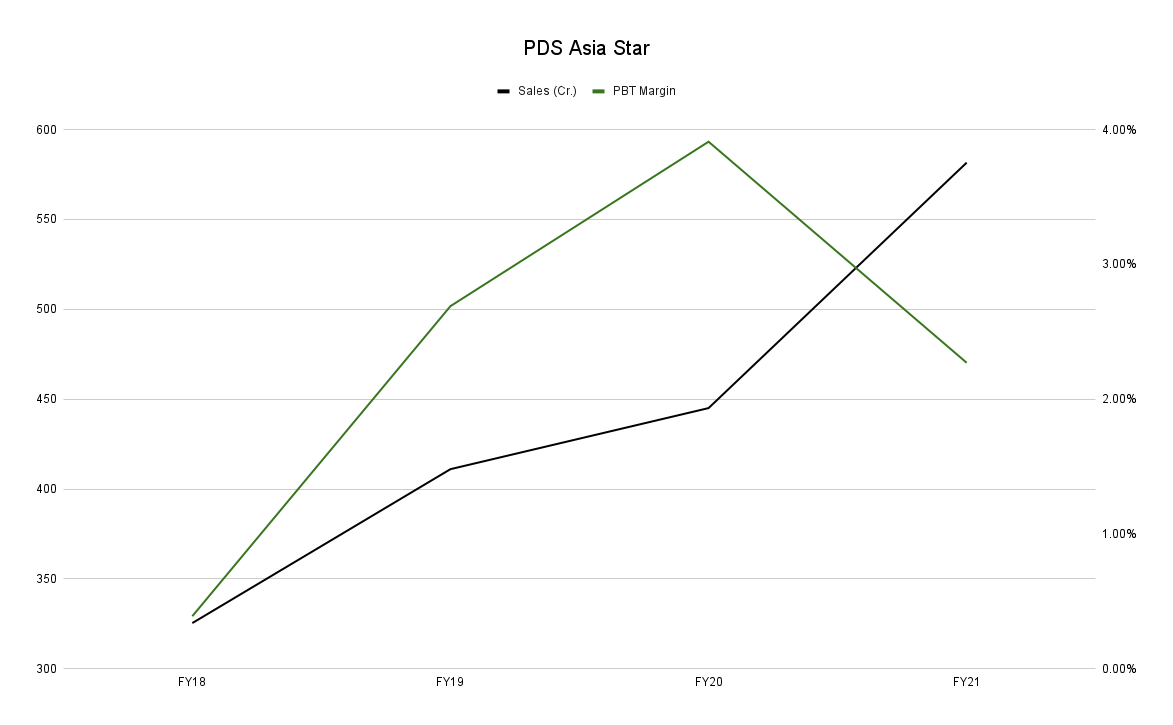

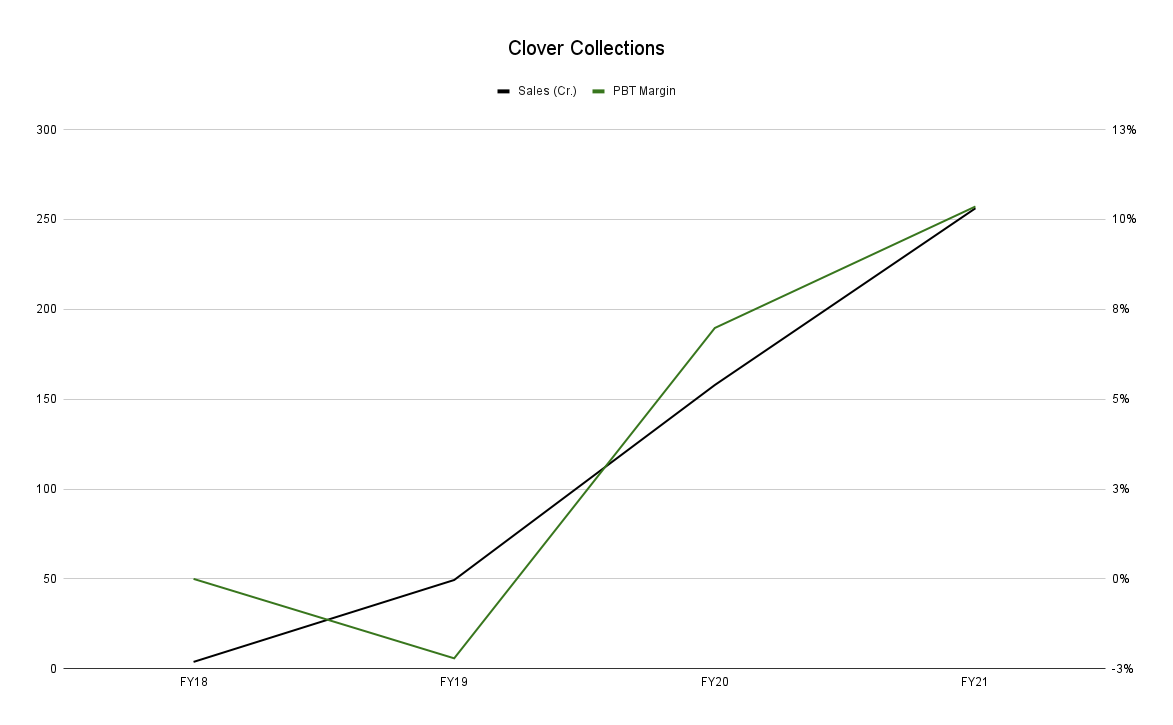

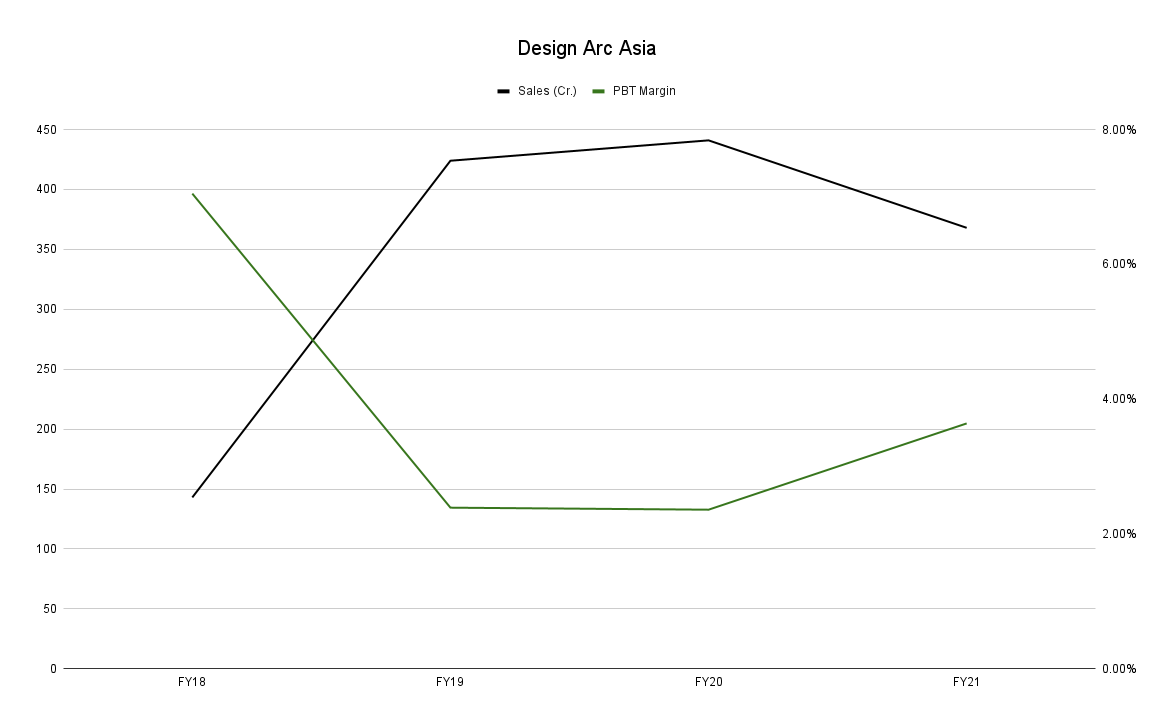

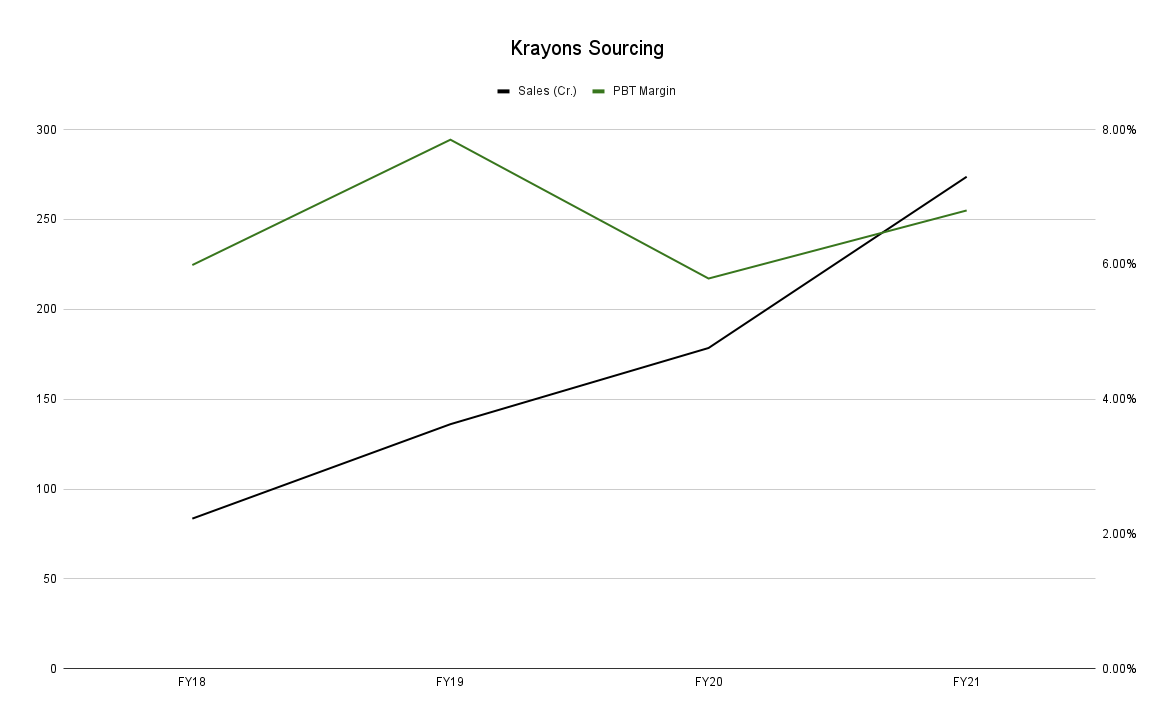

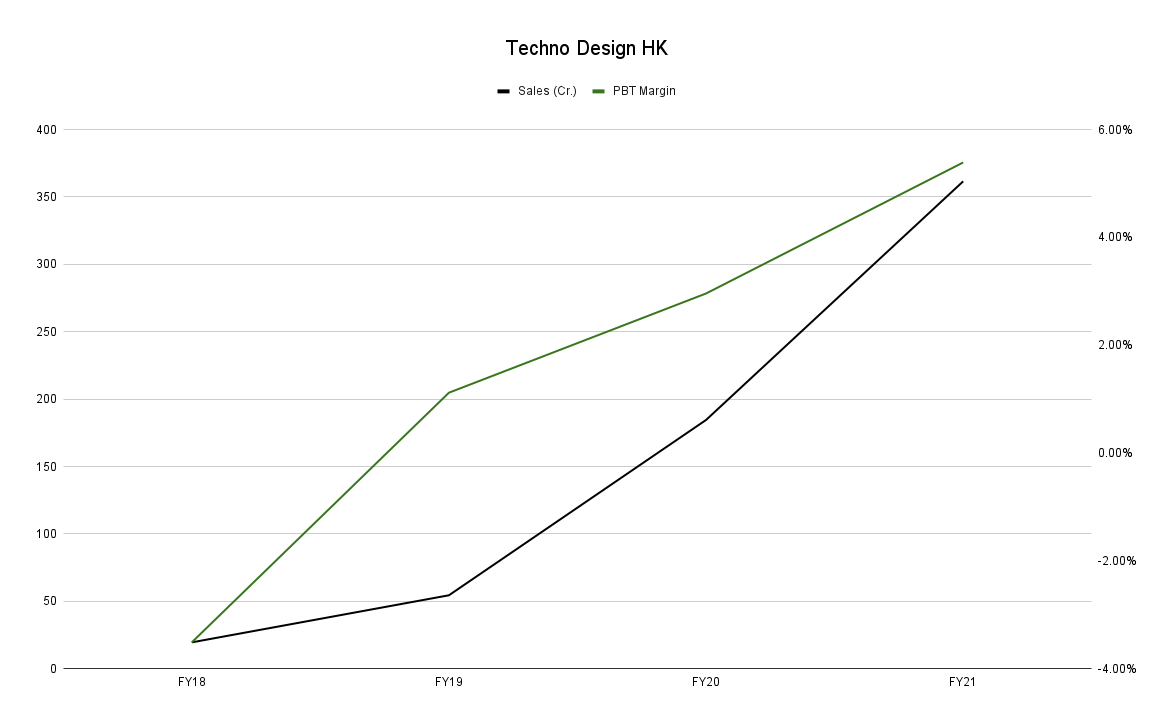

Techno Design HK, Clover Collections, Design Arc and PDS Asia Star are all high growth success stories.

Here’s the topline CAGR as a table, from FY18-FY21. These subsidiaries form 55% of the pie.

| Subsidiary | Contribution to FY21 Topline | Sales CAGR FY18-FY21 | FY21 PBT Margins | Meets PBT benchmark? |

|---|---|---|---|---|

| Poeticgem International | 10.47% | 19.98% | 4.18% | Yes |

| Simple Approach | 9.71% | 5.52% | 3.35% | No |

| PDS Asia Star | 8.67% | 21.36% | 2.27% | No |

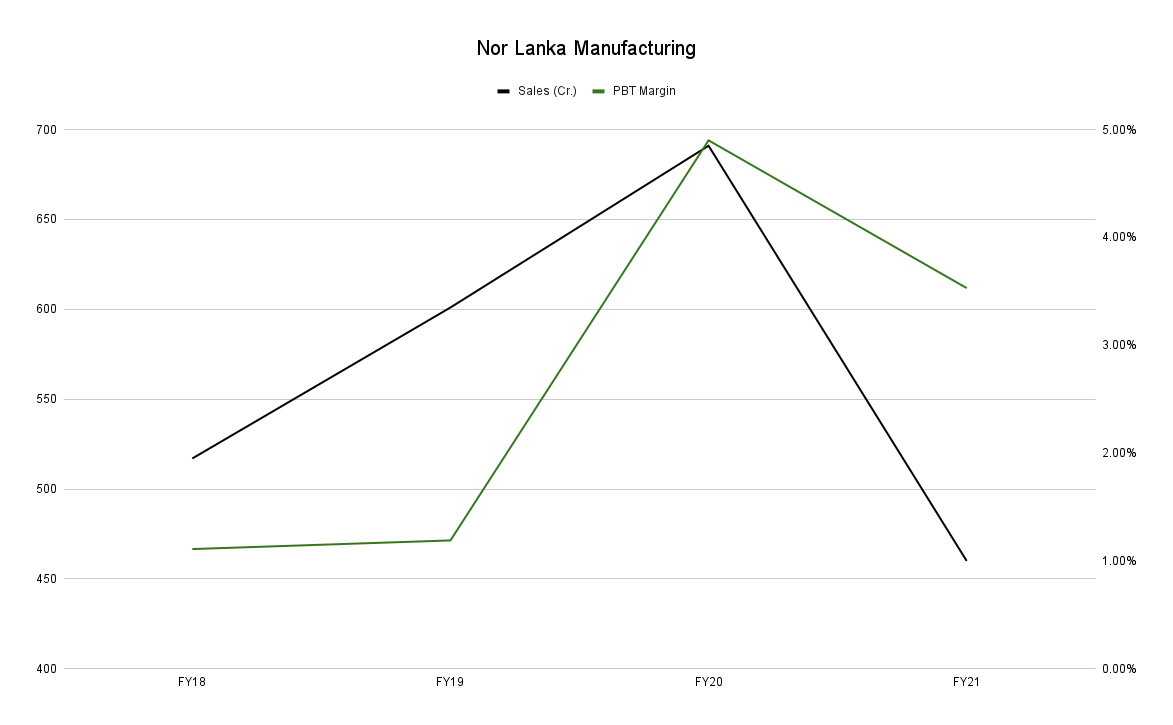

| Norlanka Manufacturing | 6.86% | -3.82% | 3.53% | No |

| Multinational Textile Group | 1.62% | 156.6% | 38.56% | Yes |

| Techno Designs HK | 5.39% | 164.33% | 5.39% | Yes |

| Krayons Sourcing | 4.08% | 48.54% | 6.80% | Yes |

| Clover Collections | 3.82% | 306.66% | 10.36% | Yes |

| Design Arc Asia | 5.5% | 37.04% | 3.64% | No |

| Norwest Industries | 4.16% | -27.7% | 53.41% | Yes |

Plan is to learn more about the jockeys, and why these 10 were successful before moving on to the next set of subsidiaries.

I will collate data here, and update whenever I work on this.

To test this claim, I looked at the verticals created after FY18. If they genuinely tried to improve, ventures onboarded after this meeting should perform better than pre 2017.

-

I found 25 subsidiaries formed after FY18. Out of these 25, 10 were formed in 2020 or 2021 and either do not have revenues, or have not yet commenced operations (as of AR21).

-

I looked at 15 of these that had meaningful revenues.

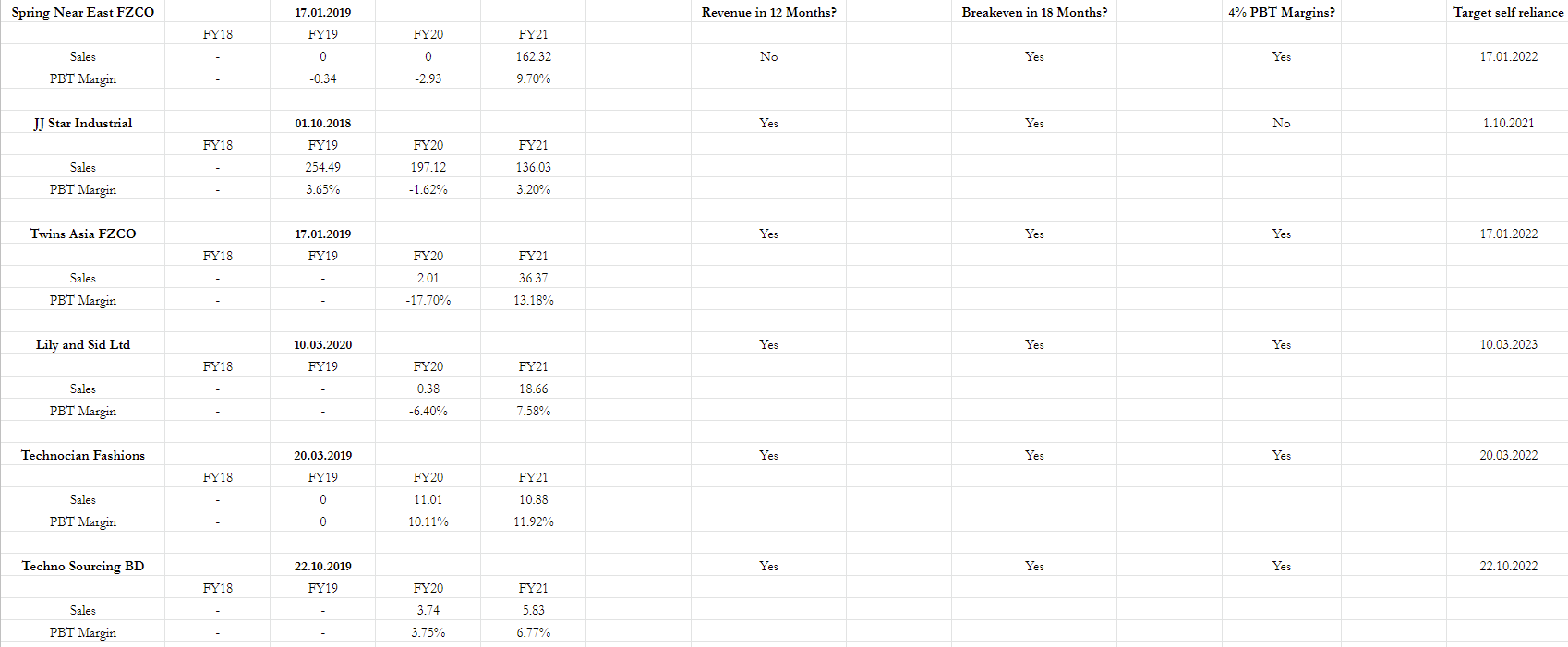

Benchmarks that PDS themselves have set:

- First six months go into ensuring team + infrastructure are set up.

- Expect the vertical to generate revenues within 12 months.

- Expect breakeven within 18 months.

- Expect self sufficiency within 36 months with 4% PBT margins.

This data is collected in the table below.

-

Out of these 15 subsidiaries, 10 successfully had revenues in the first year.

-

9/15 subsidiaries broke even in 18 months.

-

9/15 subsidiaries successfully hit the 4% PBT margin target.

-

Spring Near East and JJ Star are the largest amongst the new verticals, both have over 100 Cr. turnover in the span of 3 years.

-

Some companies have margins well above the 4% target, these can be seen in the table.

-

Casa Collective, Kindred Brands, Smart Notch Shanghai and Design Arc have not managed to generate revenues in 3 years. I wish we had information to understand why.

One can compare this data to slightly older verticals formed in 2015-16 (2014 was the demerger year) and see if growth / profitability between 2015-2017 is different to 2017-2021. I also plan to add the total amount of investments made in each vertical.

The way we should separate the subsidiaries then is by age. Brands like Simple Approach / Poetic Gem are decades old. Second bracket is those companies formed pre 2017, and the last bucket contains the 25 subsidiaries formed after.

@Chins my friend, you are doing an incredible job with the research on PDS, kudos to you!

I attended most of the concall too and had a few questions which I wanted to ask, but the institutions and large investors took away all of the time.

Slide 19 of the investor ppt speaks of the EY assessment and one of the recommendations is “Preparing ourselves for any disruptions in the business model”. I wanted to hear from the management what these potential disruptions may be. Honestly I still don’t perfectly understand the business model of PDS. I view them as a platform for several buying houses in different parts of the world, with a manufacturing facility for backward supply integration. But I am sure that this is not the most accurate way of describing them, and I was hoping my understanding would improve if I heard the management highlight potential risks/disruptions to the model.

Your last two posts have brought in a bit more clarity, but I think I’m still some distance form understanding the model perfectly well.

Disclosure: Have a small position (larger than a tracking position) and trying to understand the company better. The negative working capital cycle that they have managed to achieve and the 1000cr profit aspiration in 4 years makes me want to build even as my understanding develops. Will be a buyer on dips.

I often ignore bad analyst takes on a company, but on this instance I feel obliged to call them out.

Edelweiss released two recent reports on PDS. As someone who’s now spent nearly a year understanding the different moving parts, I looked to see what their take is on the business.

Now, we can have a difference of opinion on the business itself, but your numbers and projections lay out all assumptions. Let’s examine those. On the 6th of May, they released a report with the following estimates:

| (Cr.) | FY21A | FY22E | FY23E | FY24E |

|---|---|---|---|---|

| Income | 6,212 | 8,139 | 10,639 | 13,104 |

| EBITDA | 229.9 | 308.2 | 468.8 | 566.5 |

| PAT | 84.3 | 162.5 | 229.4 | 286.4 |

| RoE | 14% | 23% | 26.8% | 27.3% |

| EPS Growth | 41.5% | 92.7% | 41.2% | 24.9% |

At this point, 3 quarters of FY22 were known, and Q4’s results came out 10 days after this report.

On the 17th of May, Edelweiss wrote a follow up. Here are their new estimates:

| (Cr.) | FY21A | FY22A | FY23E | FY24E |

|---|---|---|---|---|

| Income | 6,212 | 8828 | 10,633 | 13,096 |

| EBITDA | 229.9 | 327.5 | 469.4 | 566.9 |

| PAT | 84.3 | 246.7 | 229.4 | 286.3 |

| RoE | 14% | 33.4% | 25.0% | 25.8% |

| EPS Growth | 41.5% | 192.6% | (7.0)% | 24.8% |

-

Three quarters of information were known for FY22. All they had to do was predict one quarter. They were off on their PAT esimates by 50%. It wasn’t as though PDS had a massive surprise in earnings. On the day they released the report estimating 162 Cr. of earnings, PDS had a TTM PAT of 232 Cr. and would need a loss in Q4 to meet Edelweiss’ esimates. Ultimately, PDS met their FY23 targets six days after the original report.

-

Despite this signalling that they should spend more than five minutes thinking about the company, they went ahead and kept all estimates for FY23 / FY24 unchanged. By their logic, PDS will now de-grow by 7% in FY23. However, note the almost robotic language they start their valuation segment with

We believe PDS will deliver strong growth in FY23 with improving profitability.

-

The analysts that decided to sign their names on the report aren’t new. They all have 8-10 years of experience covering companies.

-

In the first report, they assumed an increasing RoE, from 23% to 27% over two years. Within a week, PDS reported 33.4% RoE, their FY24 targets. What’s more, they now think the trend will decrease, almost immediately after their last report. RoCE and RoE predictions are important, as they affect what multiple one can expect a business to command.

-

By now, how much would one be willing to pay for this report? The reason that I chose to write this is because it isn’t something available on say Bloomberg Quint. Edelweiss charges you $70 per report (or 5300 rupees), to read this take.

I write this as part of a community that puts love and effort into their analyses. These reports, however, are the sole pieces of coverage available on PDS outside our forum (and a blog by one of those commenting). This is meant only as caution that often brokerages get things wrong, and one should do as much dilligence with brokerage reports as one would with their own investments.

Disclosure: invested and disappointed.

Referring to the earlier discussions here on what the moat is for PDS- sharing an excerpt from the essay “Globalization and all that” by Abhijit Banerjee

Full essay for anyone interested- https://www.srcc.edu/sites/default/files/globalisation%20and%20all%20that.pdf