I still don’t get it. I think credit score can be fetched from cibil database. There are logistical challenges as well. Let’s say a merchant plan to stick to paytm. He still has to get a new QR. And if he has a PPB account linked, then he has to get a new bank account linked. Merchant may think that when I’m going through all this hassle, why not change the service provider as well in one go, especially in cases where a rival approaches the merchant and offers him some one time onboarding benefits like some cashback or fee waiver for certain period of time.

Let’s let time and the market prove either of us wrong. The credit score of the customer is not just CIBIL. It is also derived by paytm through proprietary algorithm such as what kind of bill payments is the customer doing or what phone the customer uses. Etc.

I am long Paytm.

With whatever little experience I have had in investing, sharing a few points:

- Fintech advantages of rapid experimentation, speed and agility starts eroding once the size becomes substantial as they have to start complying to regulatory norms of the nation

- Issues of lax culture in Paytm to regulatory norms and compliance was already known (check my post on this thread in June/July’23 for more details). Continued high attrition of those who joined from banking experience compounded the matter further. All along RBI had been warning Paytm on these issues to fix the course but they failed. PayTM founder is a product person, not a banker. Simple scuttle butt on company culture would have given these insights to anyone.

- Once a company loses fancy and trust of the market, Market takes its own sweet time to again trust and reward it. Hence we see the rush to get out and the lower circuits

- There will be bounce backs in between. However a seasoned investor would look for dust to settle, see some evidence of corrective actions and walking the talk by management before committing his/her money to the company. (Unless you are in it for trading or really know what you are doing)

- Those passionately discussing about PayTM advantage or PayTM going under, would request them to remember why we are in stock market for first place - Our goal should not be to be proven “right” or “wrong”, but to make money

As Rakesh ji use to say - Stock market investing is not an act of smartness but journey of wisdom.

May the divine grant all of us enough wisdom to protect and grow our investment capital.

Cheers!

But do they do underwriting using that data? I’m not sure. And if they don’t have a Payments Bank licence, then they are really a loan “aggregator” kind of thing. Because they can’t lend if they’re not Finance company or bank. They’re tech company only… Or they are like that already.

Eventually the other fintech company can also replicate this model.

IMO, finance business is great also if you have such data, which you mentioned. I would like PayTM more if they have their own banking services. Partnership with banks, any other fintech can do. And maybe PhonePe is already doing great.

SBI openly accepting that it is trying to capture paytm’s merchants. Other rivals. May also be active.

I think it is reasonable to believe that Paytm can reach their merchants faster than the competitors. Paytm also would know which merchants are top priority and next priority, etc.

It would be great to hear from any of our ValuePickr member who is a paytm merchant or an acquaintance of one such. It would be good to know how Paytm is migrating or communicating with them so that they don’t lose them to the false marketing by the competitors.

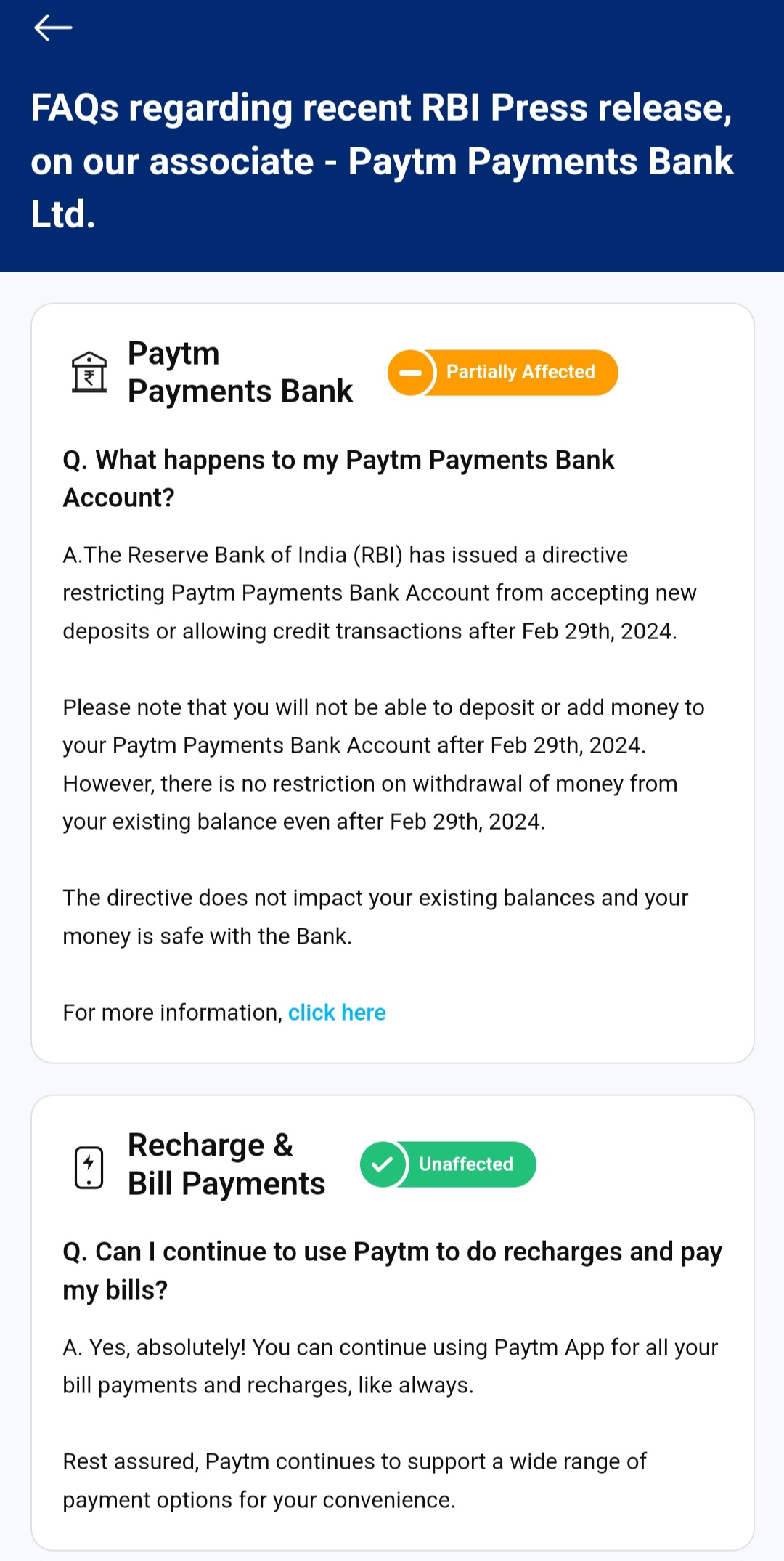

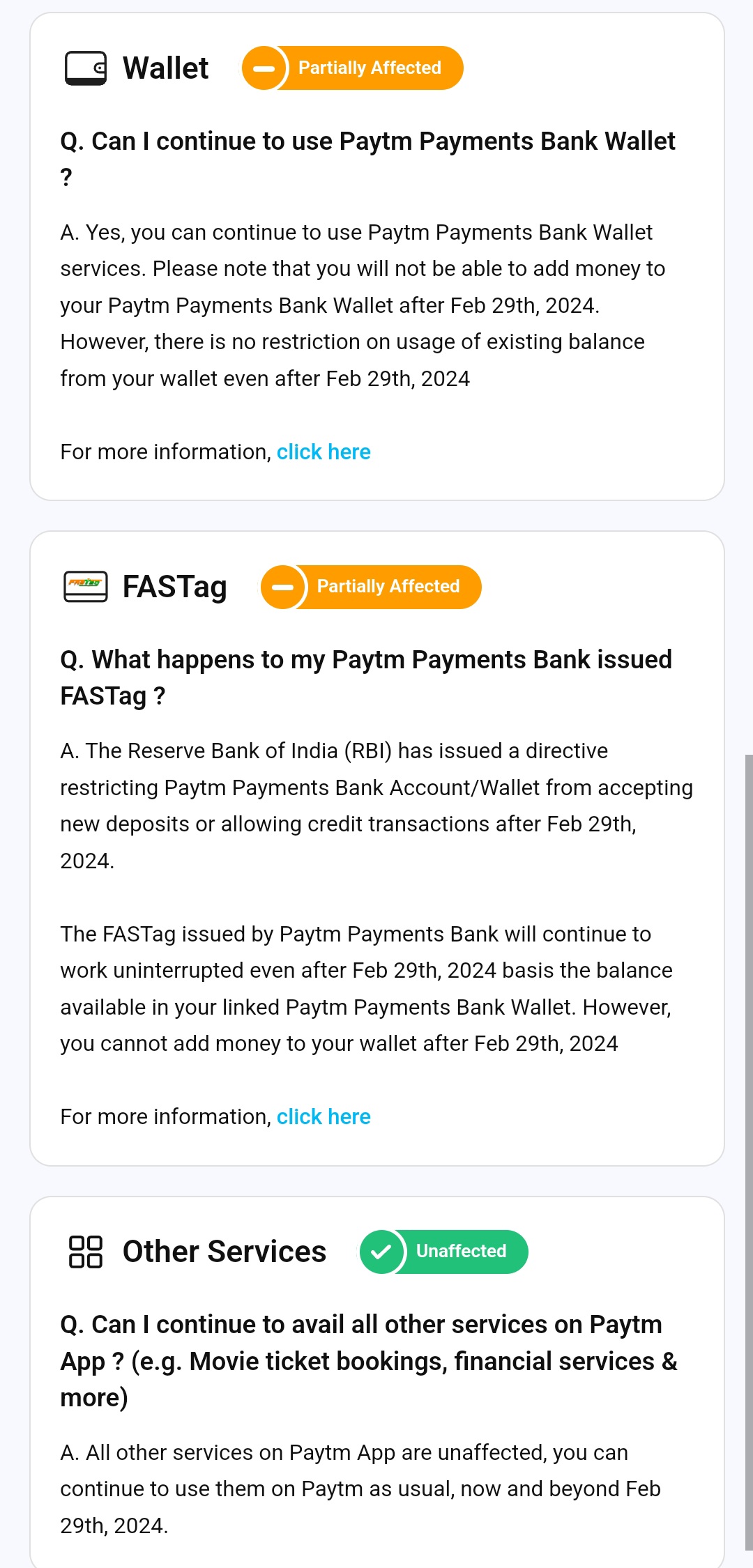

FASTag - partially affected?

That’s BS. I’m a user of Paytm FASTag and now in a limbo. Do they expect users to load a lot of money and keep it in the wallet before Feb end? And how long will it last? Once the wallet is empty what’s next?

I was/am waiting for the news that Paytm is working with RBI to reverse the ruling by becoming compliant. If that doesn’t happen soon, I’ll have to find a way to change my FASTag provider.

Disc:

Held Paytm in the past. But sold it out as it was a laggard. Still use Paytm only for UPI and FASTag user since 2020 - never had issues with its FASTag service.

I am not optimistic about the prospects of the PayTM superapp once it’s forced to change its plumbing away from PPBL to competing banks.

Disclosure: Never invested

Hi. Can you please explain what was the major competitive advantage of PPBL? And which will not be available to Paytm anymore?

Reserve Bank’s decision to freeze Paytm shows faulty understanding

– Andy Mukherjee / Bloomberg

https://www.business-standard.com/companies/news/reserve-bank-s-decision-to-freeze-paytm-shows-faulty-understanding-124020600093_1.html

Fellow startup founders coming out in support

A possible way forward is for RBI to identify corrective actions (something to similar to what USFDA does) and keep the doors open for reversal of ban rather than decisions which completely kill the business of PayTM, keeping in mind it is a public company with millions of shareholders. Assuming here that there is no fraud angle to the whole thing and it is more of compliance issues of operational nature, Government should also support in whatever way it can.

PPBL enabled PayTM super-app to window dress customer database and provide better optics to partners who provided products that would be cross-sold over the PayTM super-app… Now, without an inhouse payments bank, a true picture will emerge, thus negating any artificial opportunities to cross-sell third-party apps.

Hi

Please educate me with some numbers to back this claim. Last I read in the concall paytm app has 100 million monthly transacting users. Are you saying most of them come to the app because of PPBL? How to ascertain this?

Yes that is what I am trying to understand from you. How is PPBL helping Paytm today to be vastly different from competition? Which specific user experiences will not be possible now?

Kindly Refer to the monthly data released by RBI on payments data

Weren’t PayTM and ppbl different entities and supposed to conduct transactions at arms length already? Without PPBL, PayTM won’t be a Super App.