Any document which shows the lending business in stress? I think the indicative bounce rates and recovery rates disclosed by the company are top notch. On top of that the company continues to increase the number of lending partners. I have not see any evidence of defaults going up in any kind of lending the company does.

Why do you think there is no room for margins? They are upwards of 50% contribution margin and marketing as a percentage of revenue or GMV has been consistently coming down.

Operating leverage is now playing out in the company and the recent quarterly results are evidence of that. The company is making cash every quarter. Let me know what am I missing.

I am invested in the counter. Continue to be long Paytm.

any comments?

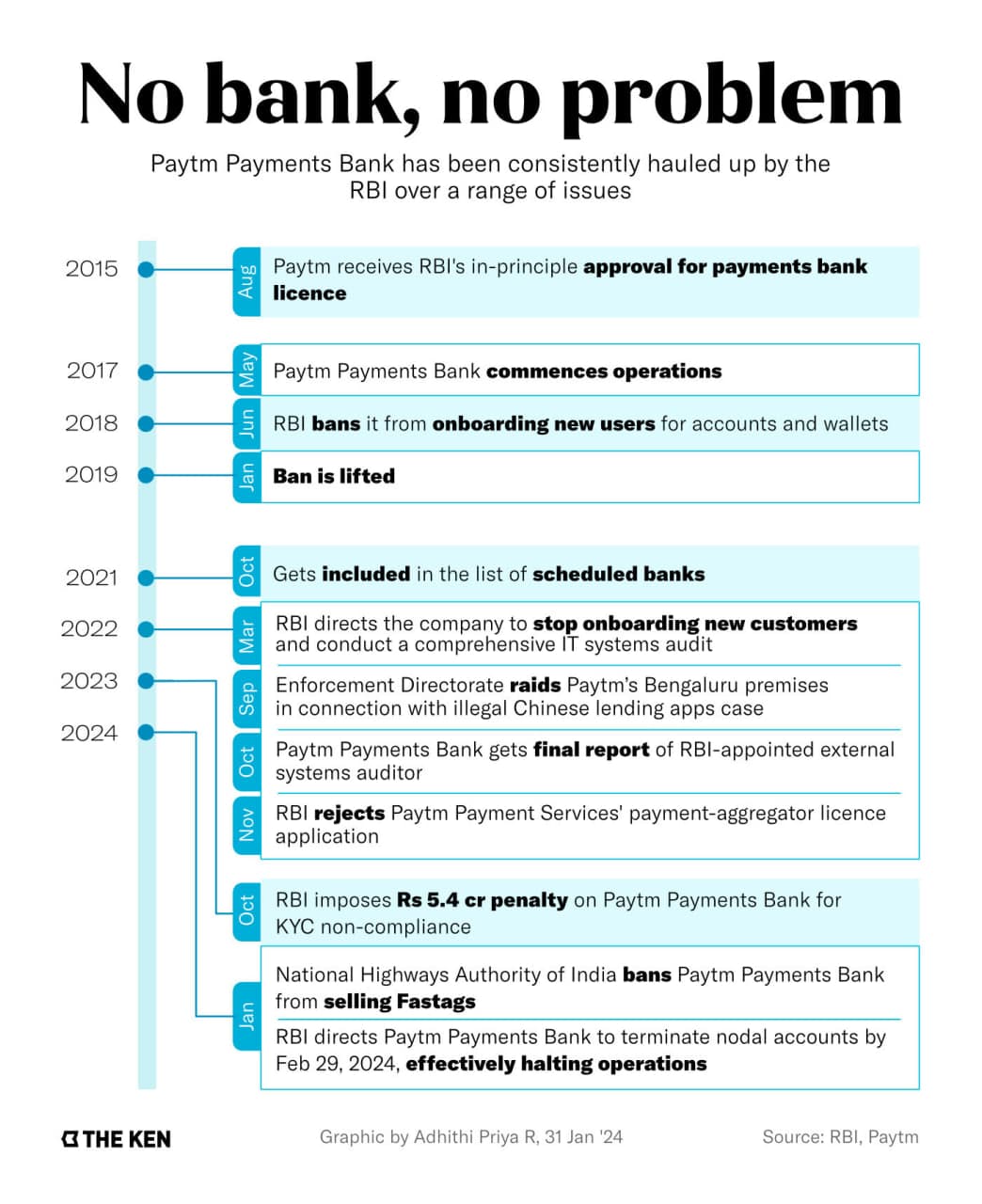

2 things is clearly gone, and that is wallet and fastag. Everything will be done with separate banking partners, like lending, PoS or QR. So, then what is the difference between PayTM and other fintechs like GPay and PhonePe. Especially PhonePe which provides almost similar suite of services like PayTM. The main difference was wallet, Fastag and Bank (ability to raise deposits, which can then be lent to customers). So, there might be issue of competitive pressure as well. This doesn’t look like an existential question as people are making it, but surely it will delay profitability in far future.

Just to put things in perspective,

If you compare it with phonepe valuation with 47%+ market share vs 14% for paytm in UPI** that should give around 3.6B USD (phonepe last valued at 12B USD) + lending business is much bigger than phonepe or anyone else in fintech + PayPay’s 5% stake (it is major player in Japan where you can get good money for payment business, as per google search (https://www.reuters.com/markets/deals/softbank-considering-us-listing-paypay-payments-business-sources-2023-07-12/) last time it was valued at 7B USD+) + PayTM money has decent scale + Decent marketing and distribution business/ event business + travel agent business + Offline dominance in soundbox - this is piece will get impacted in near term but nothing that will kill it.

**I do not think P2P UPI will ever chargeable (of course there can be charge after some limit) but main income is P2M where I think PayTM has more comparable share with Phonepe.

This is as of now. Thanks!

Disc. Holding significant position in portfolio so may be biased.

Paytm is posing as a payments player and pushing income from lending as their major revenue going forward. It is in lending yet it does not do the underwriting or is taking the responsibility of default. It is an originator rather than a lender and income is bound to be limited. They are definitely not the largest in Fintechs in personal loan (not even in top 5) and to clarify to a previous post they cannot use customer deposit to lend forward.

ECL of 5% is not top notch. Major part of the lending was Postpaid loans and that will vanish from next quarter. With not being in the good books of the regulators, will push away the lending partners. Anyway they will be pushed to a corner and find difficult to lend, but they have already stopped lending for two weeks and that will stretch further. Any discontinuity in lending is only going to push the NPAs even higher irrespective of what kind of customers they have lent to. It is quite surprising that the lender partners have not yet started feeling the impact of this massive tremor and some are even 10% up today.

Would point out the cryptocurrency situation back in 2017-18. When the regulator was not happy with the growth they killed it by directing banks to not partner with the crypto platforms and we all know what has happened after that. Here the regulator not approving the payments bank passes the signal to the lender partners of their view and that is going to deter any lender from associating. UPI services will be routed most probably with ICICI and that will continue. The services that have been stopped (deposit, fast tag, UPI etc) will in some way find a revival. However, the services that the regulator has not touched (lending) directly is going to suffer the most. Lets see if they are able to salvage through any partnerships.

As pointed out earlier it is going to hit lower circuit for few sessions. Revision of lower circuit may halt the slide for sometime, but market will definitely read between the lines. Salvaging the company is going to be a mammoth task and would require a lot of help from partners and regulator. The help from regulator is definitely not coming and they have given their opinion to the lenders through their notice to PPBL.

Turnaround stories still happen in the investing world but it requires a sincere, hard working and clean management. For now will just say falling knives are not supposed to be caught, it only cuts your hands. Rest, happy to be proven wrong solely for the sake of the huge workforce employed by Paytm.

By fintech, I meant only originator and not having balance sheet of its own. if you still think that it is not top 5, can you also give me few name which are in top5? just wanted it for my reference. Happy to be proven wrong!

Postpaid loans was not the major contributor to lending revenue. The major contributors are Merchant Lending and Personal Loans which Paytm continues to do.

Please confirm which 5 fintechs are bigger than Paytm when it comes to the quantum of loan origination per quarter.

Other than this the remaining post is full of opinion. I hold a counter opinion. But let’s wait for more data to decide.

In my opinion the major differentiator remains that Paytm already has its soundbox installed with 1.06 crore merchants. Also Paytm has a large salesforce of 25,000 which serves this merchant base. I have been trying to figure out why would a merchant stop using Paytm soundbox and move to PhonePe sound box. Please educate me what do you think could the reasons be for such a switch.

Competetors are active to capture paytm’s market by misguiding. Today I went to a local barber shop for haircut. He used to have paytm QR (no soundbox) at his shop but today had an airtel QR. He was telling that yesterday an airtel guy came to his shop and said paytm is banned from 1 March and everybody has to switch to some other app before that. That airtel guy requested him to join Airtel and he agreed.

This is interesting. Many people argued that paytm enjoys certain network effect. But if it’s that easy to switch to another service provider, then there really is no entry barrier in this business.

The merchant he spoke about was using a paper QR. In this case there is not much of a network effect.

But the merchant who is using a soundbox and is also borrowing from Paytm app is locked in. That is because Paytm has at least 6 months of his cash flow data and therefore has the underwriting capability. Another soundbox provider does not have that confidence to lend to this merchant.

So why can’t that merchant download his statement from paytm app and provide it to another app and that app sanction his loan on the basis of this data. Only the merchants who have already taken a loan from paytm will find themselves locked.

That isn’t enough information for taking an underwriting decision. There is also the additional information that Paytm has.

For example what is the credit score of the customer who has paid money to this merchant. Paytm also waits for 6 months to lend to the merchant because in addition to the cash flow Paytm’s algorithm is also monitoring the quality of the merchant’s customer base.

I am sure in addition to that there are more inputs that the algorithm takes. For example what is the ticket size of the transaction and at what time of the day, etc.

Maybe it is good that Paytm has to sever its ties from Paytm Payments Bank. Investors need not worry about conflict of interest in related party transactions. Right?

Paytm claimed that there were cost advantages. However, considering Payments Bank is a separate entity, and it had its own profit motivations, the cost advantage shouldn’t be significant. I think management is also saying the same.

")