I have been studying Paytm of late and am mightily impressed. Much has been debated about it in the thread, nevertheless let me add my thoughts.

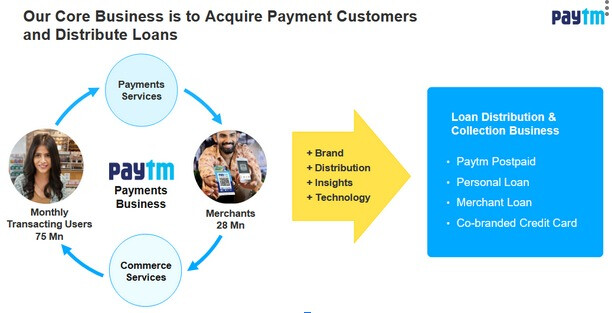

What does Paytm do? They onboard consumers and merchants through UPI payments and payment solutions, and then distribute loan to them.

Paytm business flywheel:

Consumers come for UPI/merchant payments > Merchants come for these consumers, add more and more use cases > more users > more merchants > Disburse loans to both these types of users.

They did a lot of iterations and figured out/crystalized their strategy to monetize and scale, a well thought out one. And have built a beautiful funnel/upsell workflow:

Consumers:

Come for UPI Payments > Paytm postpaid/credit card > Personal Loan > Repeat loan

Merchants:

Start with free Paper QR code payment > Soundbox > POS/EDC payment solution > Merchant loans > repeat loan

Soundbox, POS/payment solutions bring subscription revenue.

- 50% of personal loans come from postpaid customers

- 20% of personal loan customers repeat buy in 12-18 months

- Device merchants form 80% of merchant loan disbursal

- More than 50% of merchants loan by value come from repeat loans.

- Soundbox/EDC merchants retention rate 85%

Number of monthly transacting consumers - 9 Cr

Number of subscribed merchants - 68 L

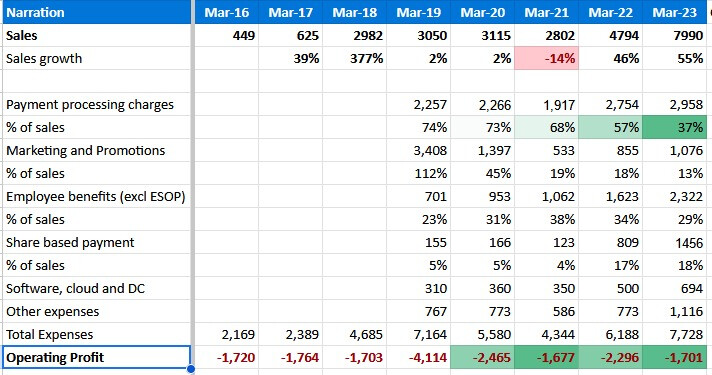

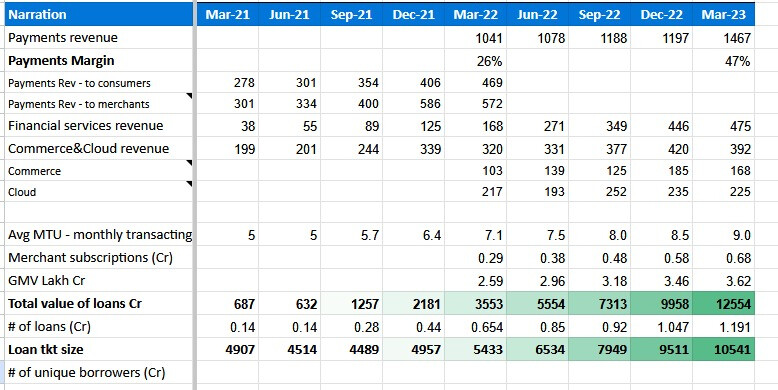

This shows up in their results:

-

Payments revenue is scaling up. Most importantly its margin is steadily improving - better bank rates, adoption/scale, account level rationalization. Margin means the profit after the expenditure on payments revenue.

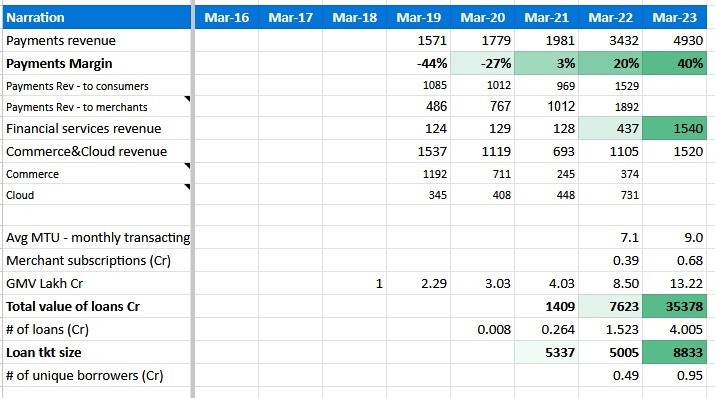

-

Financial services is growing fast and scaling high. Total value, loan tkt size and no. of borrowers are growing.

But an important point to note here is that they just scratched the surface in lending business. Lending penetration in their captive user base:

- Postpaid - ~5% of MTU

- Personal Loans - 1% of MTU

- Merchant loans - ~6% of device merchants

Now where do they stand vs Phonepe?

Digital payments market share:

Phonepe - 46%

Google Pay - 34%

Paytm - 15%

Phonepe has 10x customer base. with a lion’s share in UPI payments. Yet…

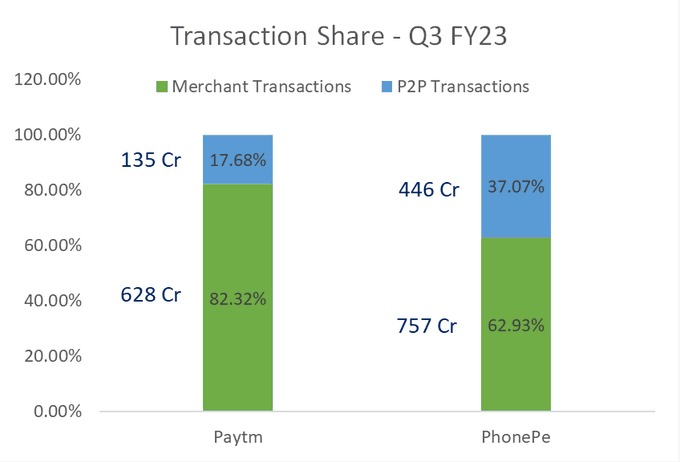

Phonepe revenue is only 1/4th of Paytm’s. This is because Paytm focuses on P2M transactions. Phonepe has more consumer UPI txns which doesnt have revenue.

Look at soundboxes deployed by these companies - that is, the merchant side:

Paytm - 30L as of Aug 2022

Bharatpe - 3L

Phonepe - 1L

This is a well planned strategy Paytm played to focus on merchants and give a whole ecosystem of solutions to them.

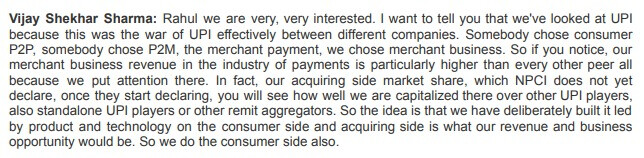

VSS comment about this in a recent conf call:

But what about the credit/collections risk? - They do not have credit risk as they dont carry the loans on their BL. However they have collection risk. Which they are executing the collection side also amazingly well. With very minimal loan loss. They even have lenders as customers only for collection side. They acquired CreditMate for this in 2017 and invested here really well. All collections are digital, no call center or manual effort.

Paytm’s near term target - 10Cr merchants and 50Cr payments customers

Vision - To bring Half-a-Billion Indians to the Mainstream Economy through Technology-led Financial Services

My conclusion:

Paytm’s distribution and tech are their strength, and of course the strong brand recall. They built an ecosystem around merchants. POS and payment solutions, cloud solutions for accounting, books, loyalty and so on. which other players dont have. This is Paytm’s moat. There could be many players who try to disrupt the UPI market further, but in my opinion this can only make acquisition costlier for Paytm, their distribution and the long headway for their lending and other services will still be their edge.

Digital lending is just 1% of TAM now. MSMEs are 30% of India’s GDP. 63mn in numbers. 20% of their credit needs satisfied by formal sector, 40% by informal, remaining 40% is a gap. Out of this 63mn, Paytm just reached 10%. In my thinking, Paytm is going to be a huge and significant player in the next growth leg of Indian economy. They are also going to build an inhouse general insurance arm, planning to spend 1000Cr in next 10 years. Other financial services like equity broking, mutual funds are being piloted.

Quite capable of pulling a 100x from here.

About the concerns discussed here:

- Buyback - They are sitting on a pile of 8000Cr cash. They are spending/investing aggressively in growing their business, and well on track to be cash flow positive next quarter. ESOPs expenditure will be done by 2026. Why keep excess cash then? Distribute it. I believe they did the right thing.

- Corporate governance - complex subsidiary structure - Berkshire Hathaway is an investor in Paytm, their only investment in India so far. This is my guarantee.

Their disclosures are top notch and as good as it gets. Monthly data published. Quarterly earnings release and PPT is so detailed and consistent, with all relevant KPIs explained.

I did not read up much about VSS before studying Paytm, for I might become a fanboy which could cloud my thought process. However reading through his intro remarks in the conf call scripts itself made me his fan. Clear, concise views about the business. I will add a few of his quotes in another post.

Disclosure: Invested, ~15% of India portfolio