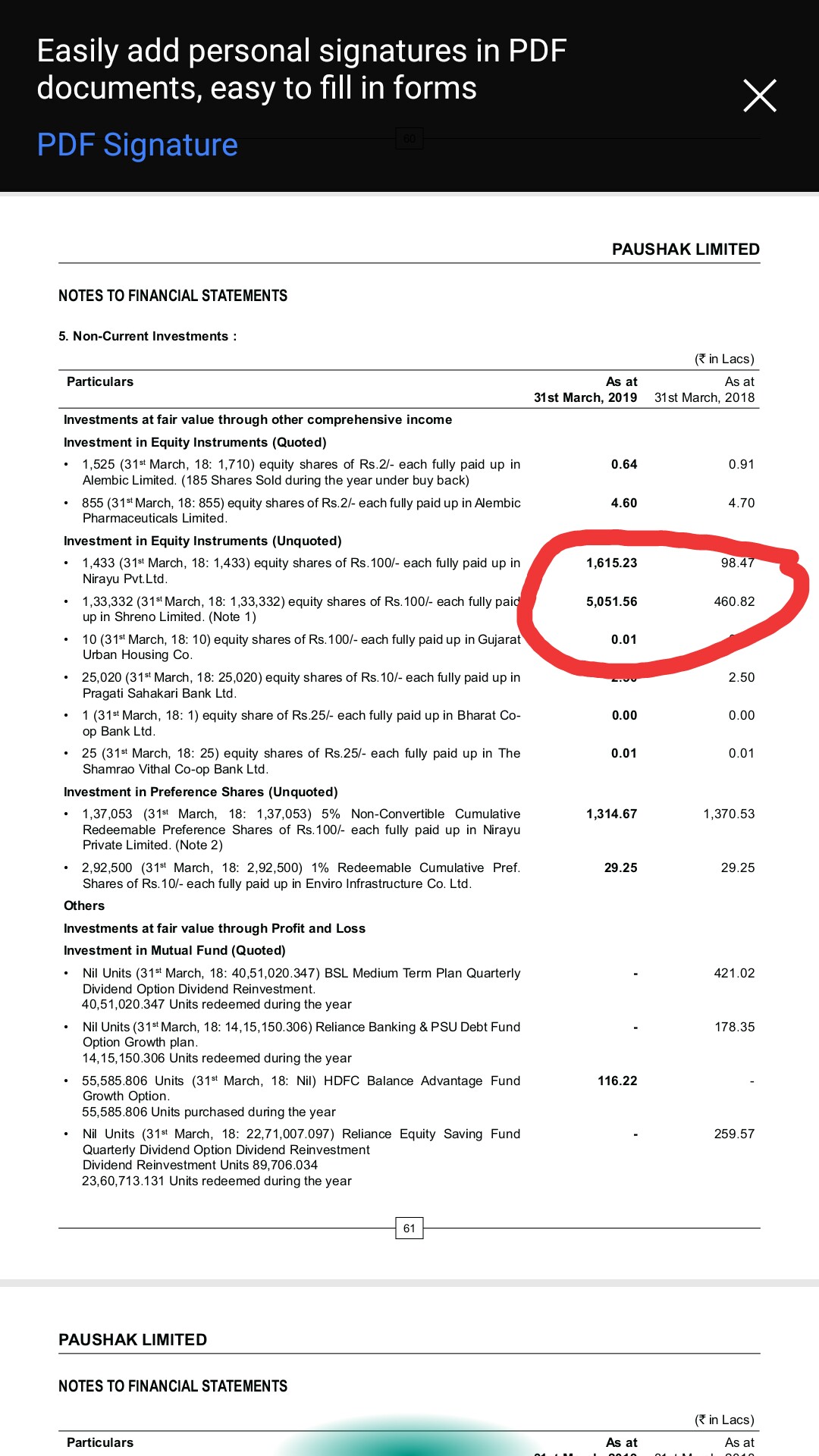

So,value of nirayu increases from 98.47 lkhs (2018) to 1615.23lkhs(2019)

Value of Shreno ltd increases from 460.82 lkhs(2018) to 5052.56lkhs(2019)

Is it normal or we are missing something

Nirayu ltd has 59.80% share holding in alembic pharma

So,value of nirayu increases from 98.47 lkhs (2018) to 1615.23lkhs(2019)

Value of Shreno ltd increases from 460.82 lkhs(2018) to 5052.56lkhs(2019)

Is it normal or we are missing something

Nirayu ltd has 59.80% share holding in alembic pharma

Sir, i meant that promoters are not taking money out from Paushak so in that sense you were absolutely right. however, this increase in value of investment is looking very much inflated which i wanted to highlight. an investment of 4.6 cr turning into 50.5 cr in just 1 year?

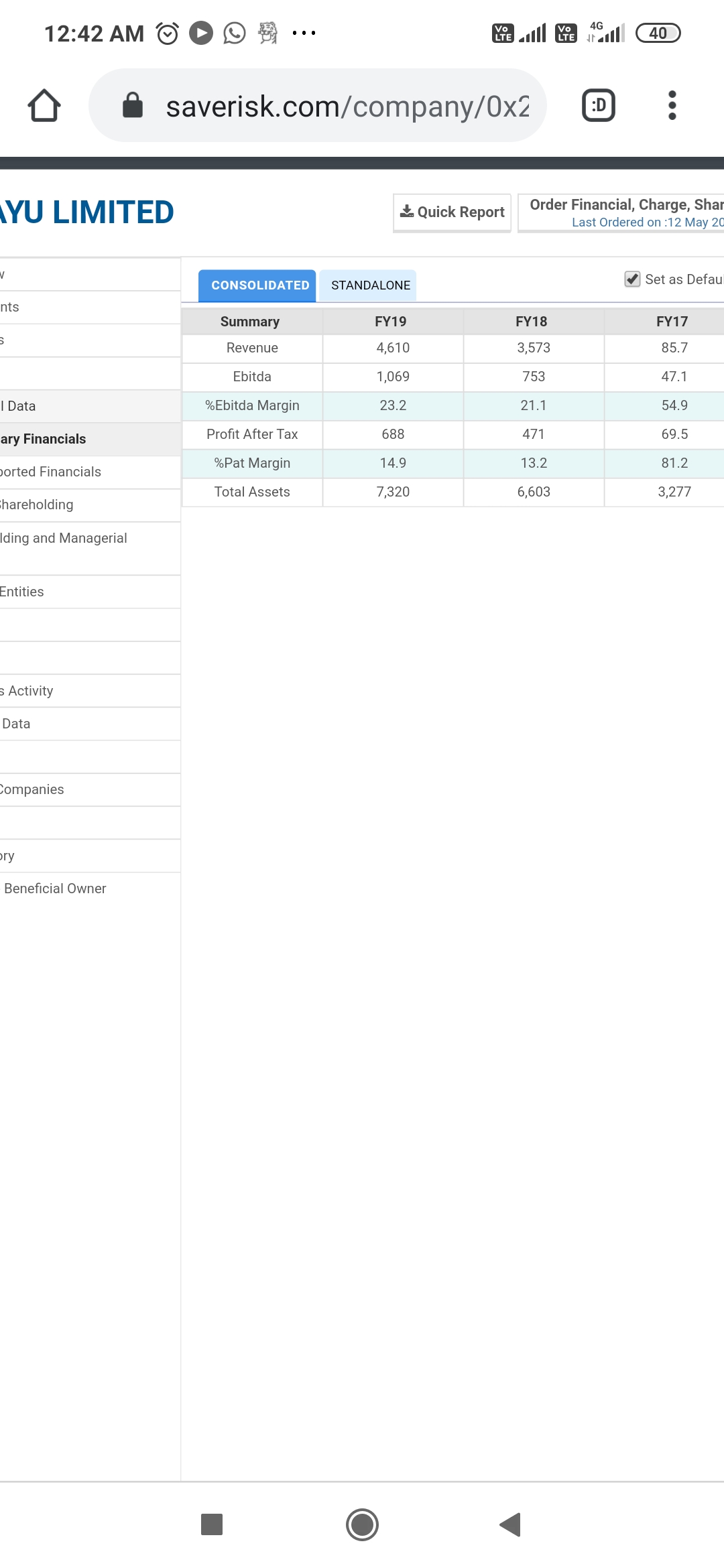

PnL statement of Nirayu Ltd.

Have a look at the growth of FY18 over FY17, and continued growth post that.

Profit after taxes have grown 1000pc

What do they do?

I Know but I find it difficult to see your point. They can show 500cr if they want, how has it affected paushak financials or valuations. A shareholder ignores these values, they don’t form part of p&l. They are in balance sheet but equity is a sum of future profits. For a sum of future profits, you take present profit and add growth.

The inflated value did not come into income statement. It probably adversely affects roe As the profit directly goes to retained earnings which is capital for roe calculation, so in their interest it is better to show a lower value not higher.

Do you know what equity method of accounting and cost method of accounting for subsidiaries is ?

Sorry I am not trying to be condescending but I fail to see your point honestly

This kind of adjustments is not consistent with good management behavior. I like to take management quality into account before investing in a stock. The stock may have sound financials but if the management is not honest then it’s a red flag because what they can do in future is uncertain.

It’s the adjustment not solely decided by the management And many times it’s stipulated In gaap, I don’t see anything wrong with it but that’s not the reason I haven’t invested here

IF someone who knows what the level of phosgene supply demand is in India I would be more inclined to invest

If management is dishonest they should reduce the value of investment to zero not increase it

Increasing value has now made equity higher, profit same as before, so return on equity is now lower and the stock appears worse than before the increase

If they would have decreased the investment, return on equity would have been higher

Increase in investment value has not been shown into p&l

That’s why I am confused by your statements

No business becomes 14 times or 16 times profitable in one year. If this management thinks that their investments have become so profitable then they are fooling everyone. And if their investment value is real they should just book the profits for it is a windfall gain and use it for capacity expansion or just distribute it.

If management reduce the value of investment ,then asset will also decrease and which lead to higher debt equity ratio.

So increasing valuation of investment also inflate asset

Incresing investment value will decrease roe but also decrease d/e ratio which is always favoured by management .So dishonest management try to inflate asset.

So ,management want to show higher valuation of investment in their favour.

Isn’t it

Pardon me if i m wrong

I told you million times already that this profit is NOT shown in profit and loss account

For this company debt is already near zero, they don’t have to worry about this ratio. If dishonest there was room to increase debt equity ratio

Ok sir

Got it

I understood that this increase value of investment has no effect on P&L account

But this will not inflate asset and thereby book value of company?

Thanks .

Only one querry

Yes it will Pragnesh

What is book value, assets - liabilities, right?

What goes in a formula for return on equity

Profit / equity

But equity is assets - liabilities

So they increased equity and made their life a bit difficult as they have to beat the present roe without benefit of profit that comes from that investment

Thank u very much sirji

As per your experience is it red flag or not much problematic for investor

Thanks

It’s not a red flag

Under gaap rules, a subsidiary has to be shown using net asset method.

If they are showing 50cr, it means their percentage of the business had 50cr in net assets. Unlisted companies cannot be valued at pe multiple during consolidation

If you can find out what the subsidiary company is doing, you might have an idea of why valuation changed so much. Maybe they had land and they sold which added to the subsidiaries net asset

No problem, hope it helps you in your investment journey. Usually I dig deeper into annual reports if it fails any of the below tests:

Do not forget that it is a small cap company with a market cap of 600+ crore. Definitely the level of information available will be less and management will be less transparent and there is no harm in that.

Why so bad result by Paushak - Only 15 days of previous quarter we had lockdown.

Revenue down 24% and Profit down 35%. Is it the beginning of end of Chemical Story in India ?

Risk is that China has opened up manufacturing facilities almost fully. New facilities are also coming up in China. Export subsidy has also been increased significantly in China.