Revenue of Rs 109 crore was reported for the first nine months of fiscal 2020, a year-on-year growth of 8%. Growth is likely to be in the range of 7-8%, over the medium term, led by improved realisations as the current capacity is almost fully utilised.

*** Exposure to risks related to the large capex:** Paushak is undertaking large capex of about Rs 120 crore over fiscals 2020-2022. This will be mainly to expand existing capacities, and increasing the phosgene capacity by upto three times. The company faces implementation risk as capex is significantly higher than the current gross block, and is in the initial stages. Capex commenced in fiscal 2020, as against earlier expectation of fiscal 2019. Till date, Rs 25 crore of capex has been carried out, and Rs 75-80 crore is likely to be incurred in fiscal 2021, and the balance in the following year. Any significant cost or time overrun remains a rating sensitivity factor. However, CRISIL derives significant comfort from its promoters’ experience in successfully executing large capex in group companies.

With some part of the production capacities likely to be commercialised by September ’ December 2020, ramp up in scale is expected from fiscal 2022 onwards.

Rating Sensitivity factors Upward factors

Improvement in product mix

Higher-than-expected revenue growth of 12% over the medium term, and sustenance of healthy operating profitability

Sustenance of healthy financial risk profile

Downward factors

Decline in operating margin to below 20%

Time or cost overruns in capex, or debt-funded acquisition, weakening key credit metrics

Hi, Ive been trying to build my understanding of this business and here are a few questions I have on the same -

Just like Chlorine, Phosgene is a hazardous gas and hence transportation is difficult. The point here is that given the entire noise around pollution/use of hazardous chemicals, wont technology be able to adapt to better quality substitutes in place of Phosgene?

2)From the EC Report, what one understands is that Phosgene is the upstream gas and the company is basically expanding capacity for the downstream derivates - some of the notables being Esters, Isocyanates, Urea and Chloroformates. My question is that do all of these materials need Phosgene as a starting RM?

3)Who are the main manufacturers of these downstream derivatives mentioned in (2) Above?

There might be other chemical substitutes of Phosgene to manufacture those downstream products, but in all certainty those are not standardized procedures or involve much greater cost or wastage. So, it is much more plausible to upgrade technology & practices that ensures less leakage of those chemicals to the environments, than finding other substitutes & standardizing those processes.

Regardless, it is because of the hazardous nature of Phosgene that only a handful number of companies are granted license to deal with such chemicals, which acts as barriers to entry & protection of margins.

First of all great thankyou to everyone who has contributed in this thread. It was great to get an insight into last 5 years of paushak history. Saying that with the 3x expansion that they have planned? Have they been planning this since the past few years without any success? Secondly, since it is expected (as of now) that pharma might do well and chemicals story is already playing out. Do you think that the companies still has a long path to providing a good 12% growth in revenues? Considering that it also has a moat in some aspects.

I read on the thread that a few guys exited the stock in 2017 saying that it either seems over valued to them or the growth has played out. But since then it was multiplied 4 times.

On checking the company from my end. The fundamentals look very good. A smooth growth of sales & EPS over the years.

1…Why paushak’s cummulative cfo (10 years)is not matching with cummulative pat(10 years)

Cummulative pat=126 cr

Cummulative cfo=90cr

2…Receivable% is incresing in last few years

(In 2019 annual report

During the year, the Company has made changes in its Policy for receivables, payables and working

capital which resulted in lower Receivable days and higher current ratio.)

It’s not a correct way to measure

Let’s say you start a business with rs 1000

You buy goods for 1000

You make profit of 100

You will have receivables of 1100

You take credit and buy now 1100 worth of goods

You make 110 next time

Now you have receivables of 1210

Let’s say you can no longer go over 1100 stock so you again buy 1100, receivables will be 1210, and cash in hand will be 210

So profit has been 320 over 3 transactions however you Will have cash of only 210 as the last profits are stuck in receivables

You have to look at change in working capital. Operating cash flow shows all changes in working capital

If you have to pay advance for your goods or credit terms are not same like the terms you give on your sales, you will need to take short or long term loan

I had read one article of Dr vijay malik

As per his explanation cfo and pat of last 10 years should match.

If cummulative pat> cummul cfo,then we have to find out cause because pat after all working capital changes(receivables,payables,inventory) should match at end of ,say 10 years.

Promoters have taken profits out and diverted funds to other group companies. They have in LATEST AR bot shares of nirayu Pvt ltd worth 16 crore and shreno Pvt ltd to the tune of 50 crores. This is a big diversion of funds at the expense of minority shareholders. While this excess fund should have been used either in capital expansion or prudent financial instruments. The promoters have simply diverted the funds to their companies in the name of investment. If those cos fail then the investment would be written off as loss on investment. And minority shareholders will suffer. This is a very serious and cautionary signal to retail investors about the integrity of management.

It is from their balance sheet only. if you notice the investment section it has increased from 56 Cr to 113 Cr in 2018-19. Further 19-20 balance sheet is not out but half yearly data reveals it has increased to 130 Cr. This increase I am suspecting would be later revealed to be further investments in group companies

Why do you guys do it in a round about way to find if promoters are siphoning money

In the cash flow, under investments you’d have 10 years money spent on investments

Over 10 years there is not much

On net asset value however it’s good to know that one investment has done well and by itself is around 80cr !

Ps: not invested however tracking and waiting for more news on their 70cr posgene expansion. I don’t know what the supply of posgene is in market but if there is constraint at the moment than it might be a good investment nearing completion or when we know a bit more about how they will allocate capital and proceed with the expansion

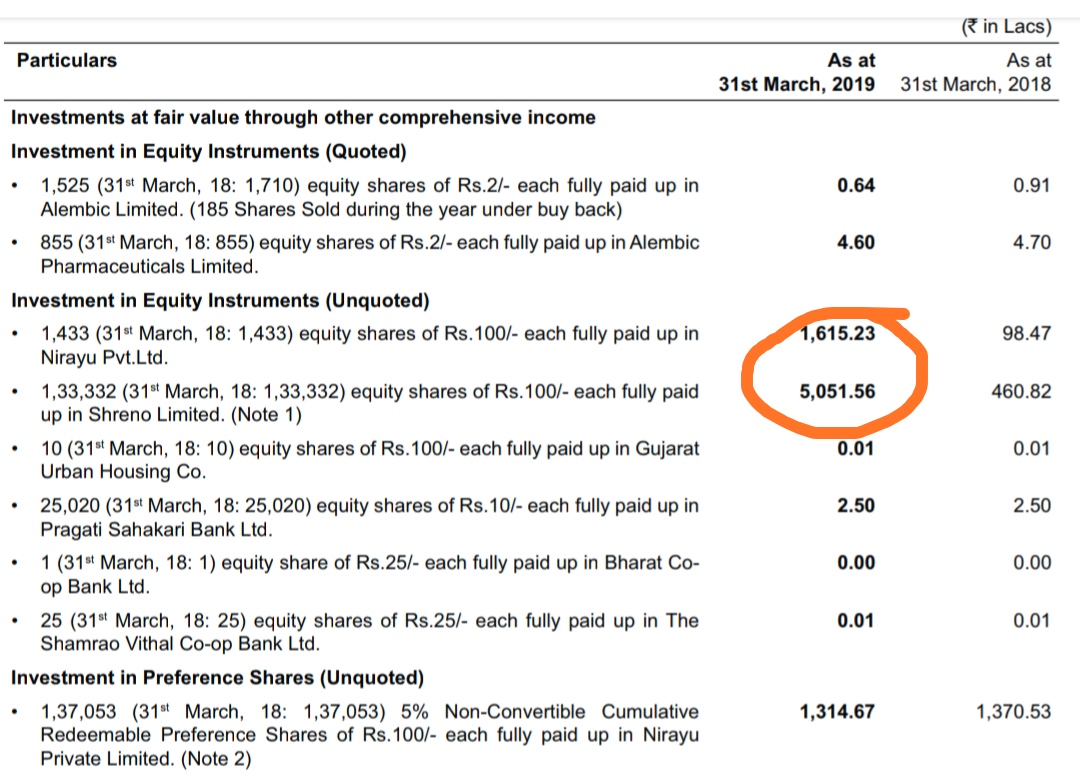

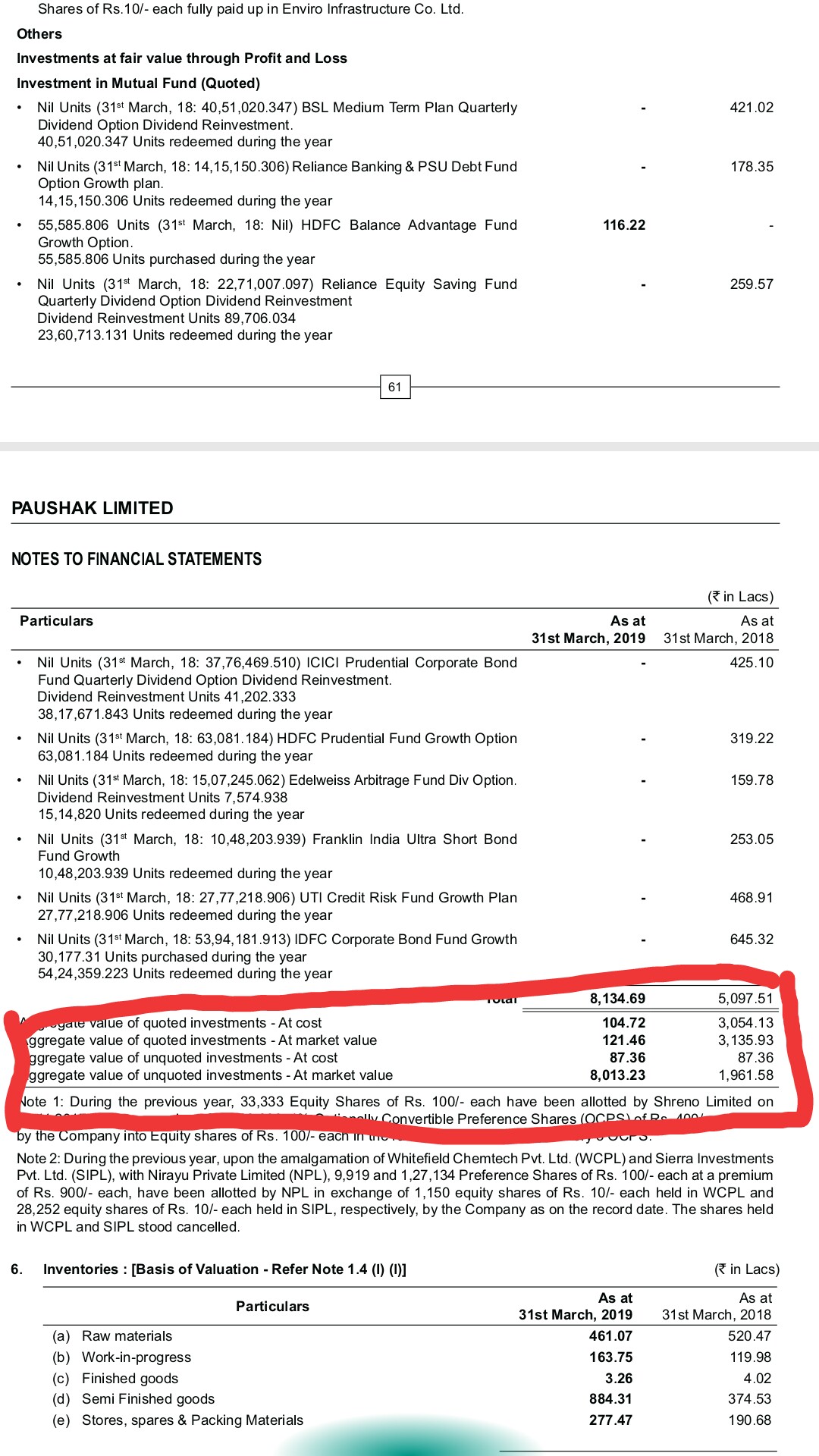

You are right.However, this is even more worrisome. These shares in question were converted from preference shares to equity. " During the year, 33,333 Equity Shares of Rs. 100/- each have been allotted by Shreno Limited on 16.11.2017 upon conversion of the 99,999; 1% Optionally Convertible Preference Shares (OCPS) of Rs. 400/- each held by the Companyinto Equity shares of Rs. 100/- each in the ratio of 1 Equity Share for every 3 OCPS."

so the promoters held 99999 shares @400 or worth 4 cr and got it converted into equity at 1.3 cr (1,33,332 shares worth rs 100 each). the market value of this investment was 4.6 cr as of 2018 ( 3.5 times return) and 50 cr as of 2019 (38 times return). this is not all.

the investments in Nirayu pvt. ltd. were worth 51 lacs, 52 lacs, 98 lacs and then suddenly 16 crores from 2016 to 2019. what is this business that nirayu and shreno are into which gives 38 times or 16 times returns in just one year???

the promoters should just sell these investments and book profits and use it for expansion. don’t you think something is massively wrong with management.

sir please see how the value of these investments increased. from combined value of 5.58 cr to 80 crores in just 1 year. this is not a normal scenario. infact data from screener.in shows that the value of investments have now increased to 130 crores. the total cumulative profits from 2008 to 2019 are 173 crores. infact, instead of the 70 cr phosgene expansion, the company should use those 70 crores to invest in these businesses which are making 16 times returns. i just expressed my doubts here. rest is individual choice.

Lifetrix, I am not invested, I thought I’ll put a disclosure before adding

However this is good excercise in diligence

So I assume you took the above from 2018 annual report

Looking at Shreno:

In 2017 annual report they say, under “investments in associates”

99,999 shares of 100 each valued at 24.10

Further down under unquoted preference shares

99,999 shares valued at 20.0

In 2018 they say these 99,999 preference shares were converted to equity instead of preference shares.

These are not shares of paushak but shares of shreeno that paushak is holding as investments

These are then shown at market value resulting in a profit. However this profit is not shown usually in the income statement. It is shown as an adjustment to oci.

If you search the amount of 1,296.06 in 2018 annual report you will get an idea of how its treated.

Maybe its too high as you claim, maybe its not but how has it affected the normal running of the business and the presentaiton of it via income statement, cash flow and balance sheet.

I am failing to understand where you are coming from