here is my analysis on paushak ltd (which is in my watchlist). comments are invited for better understanding the company. Paushak ltd - analysis.pdf (1.3 MB)

Disc: i have no financial background.

2 Likes

While at first look, your assessment appears correct, but knowing that the promoters of Paushak are not an obscure / unproven team, it made me look a little deeper in to this.

Sharing my findings and observations below

Nirayu Pvt Ltd is NOT a side adventure of the promoters. In fact, it is the HOLDING entity.

This is from Paushak AR FY19 (page 22)

Shreno Ltd

Shreno Ltd was a listed entity up till 2017-18

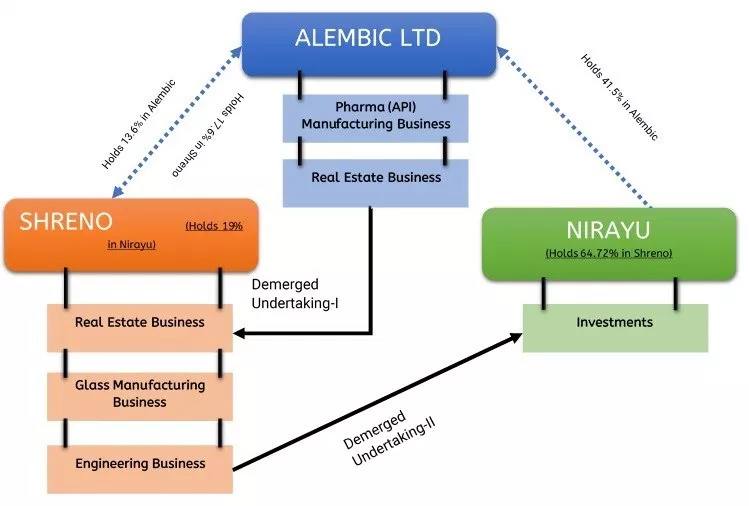

So whats the relation between all of these - Nirayu, Shreno, Paushak? They are part of the same group, headed by Amin Family, led by Chirayu Amin. Of course its a well known fact that Alembic Pharma and Alembic Ltd are also more famous entities of the group.

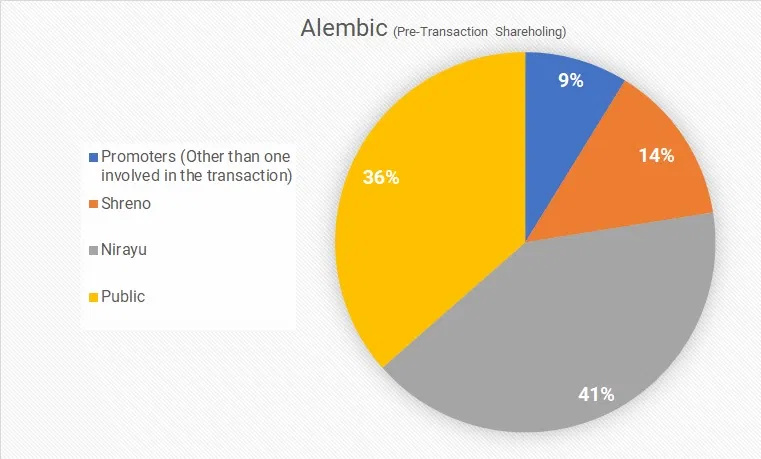

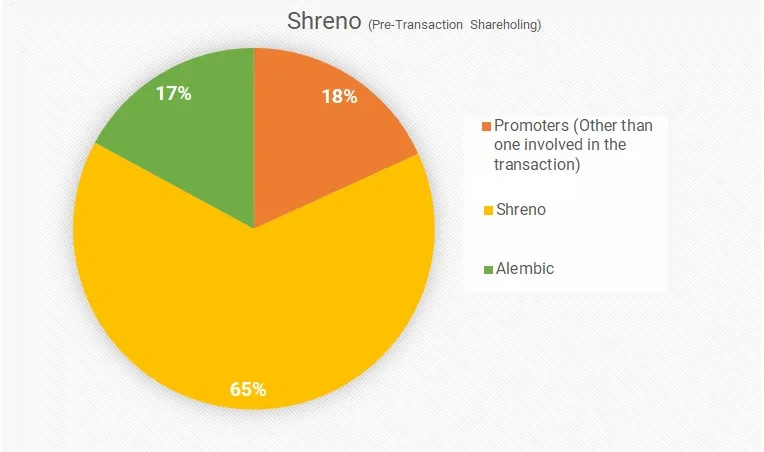

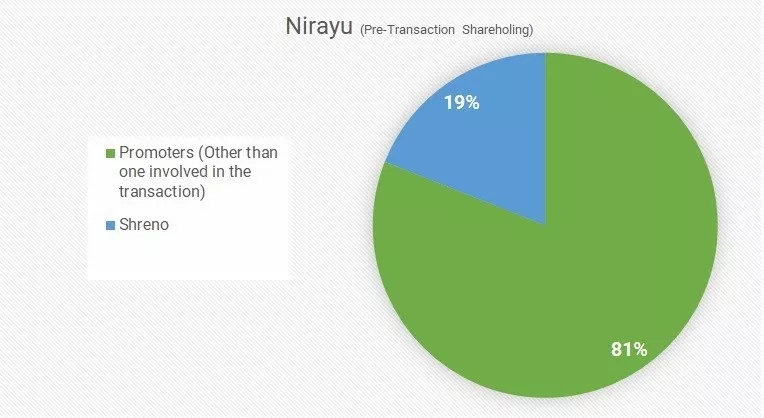

For some reason, all these companies had a spaghetti holding structure, with crazy amount of cross holdings. To get an idea, see the following graphs

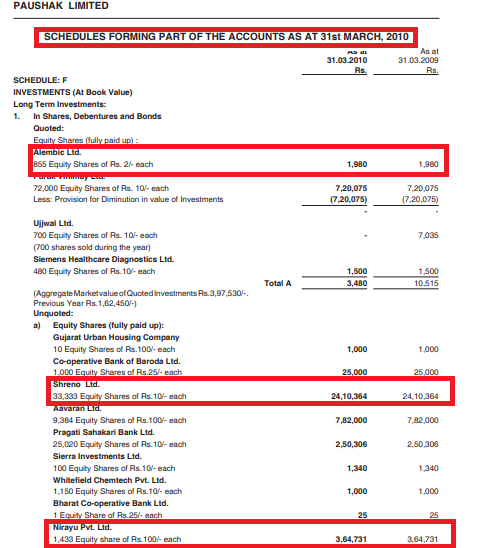

The criss-cross holdings are clear from above 3 graphs (credit: mergersindia.com). In fact, there is similar cross holding even between Paushak and Alembic for long now. Please see the snapshots below, taken from Paushak AR FY10, Page 61 ( Source: https://www.bseindia.com/bseplus/AnnualReport/532742/5327420310.pdf)

Please note the number of equity shares of Nirayu Pvt Ltd in image above - 1433, we will see this soon again.

Now, here is a snapshot from AR FY19 of Alembic

In fact, not just the shareholding, but there were cross-interest in terms of business segments across companies too. For example, both Alembic Ltd as well as Shreno were involved in Real-estate development.

In order to simplify this complex cross holding across companies, Alembic initiated an exercise of demerger to eliminate the cross holdings between Alembic, Shreno and Nirayu and to simplify the group structure as well as to consolidate and create efficiencies across business lines. Under this, there were 3 entities created

- Alembic Ltd : With investments in Alembic Pharma and Paushak

- Shreno : For Real-estate development and Project Management Consultancy

- Nirayu Pvt Ltd : As the holding company, with investments across group companies, and the engineering business

So the group structure pre and post demerger looks as follows

Pre-transaction structure

Post-transaction structure

For nauseating details of the scheme of demerger, please refer to the following document

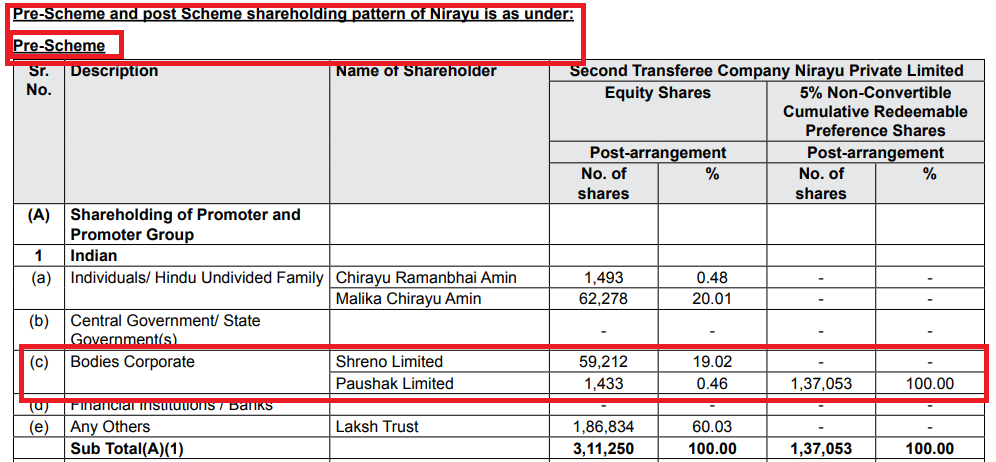

Sharing couple of snapshots from the above document (page 21 / 22)

Pre-scheme holdings

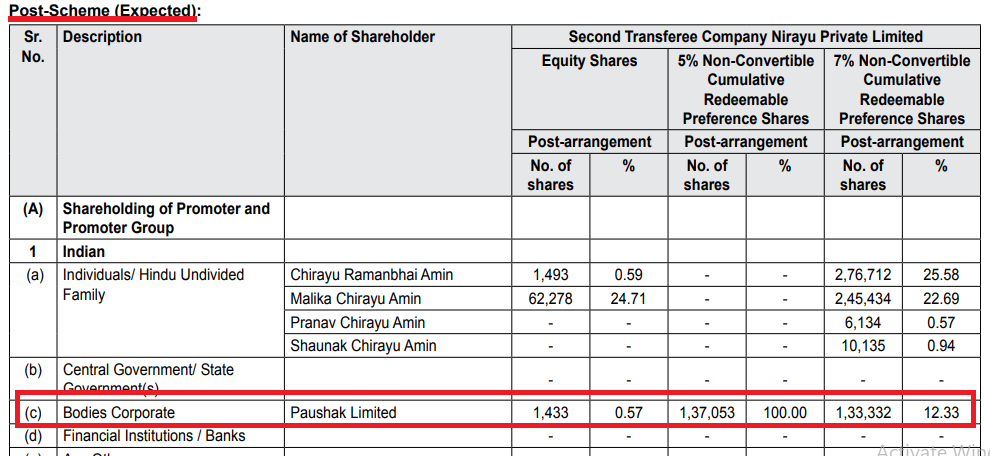

Post-scheme holdings… Note the cross holding of Shreno is now cleaned up, but that of Paushak continues… with exactly the same 1433 shares.

As for the massive change in investment value from Fy2018 to Fy2019, as pointed out by @lifetrix, I did not dig deeper to get to that, but I believe there would have a valid logical reason too, its just a matter of finding out. I am sure the reason is lying somewhere in the scheme of demerger document above.

But one thing is crystal clear from the data points above that there is no siphoning off of funds in any of this. Will be happy to learn more if I have made any mistakes in my dissection above.

Disc: Not invested, but interested

19 Likes

This year it will good opportunity to interact with many small cap managements through VC

This is inform you that the 47th Annual General Meeting (AGM) of your Company is scheduled to be held on Tuesday, 4th August, 2020 at 12:30 p.m. IST through Video Conferencing (“VC”) / Other Audio Visual Means (“OAVM”).

1 Like

Nice analysis. Has the stamp of Dr. Vijay Malik all over. Other than Ashish kacholia , Sanjay Ketkar and his brother and fly ( of Quick heal ) are major non promoter individual shareholders as per 2020 AR

Paushak has recently published their AR. The interesting stuff mentioned in MD&A is reproduced below :

Your Company is also actively exploring various opportunities, including contract manufacturing, with global customers and pleased to share that your Company has been able to initiate business with one of the global agro majors and expect to develop the relation further while increasing the product & service offerings. We believe that “Make in India”

presents a great opportunity for us along with “India alternative” to global customers.

Your Company has been putting substantial efforts to improve the technology while enhancing capabilities and capacities to achieve its vision of becoming “Technology driven Global Specialty Chemical Company”. Your Company has developed indigenous technology for its one of the key product portfolio last year and is in process of building a new plant, with full automation and as per global standards, which will not only result in majority of import

*substitution in India but will also help your Company to tap export markets. *

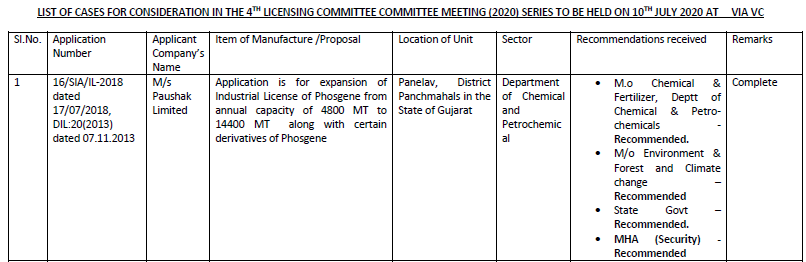

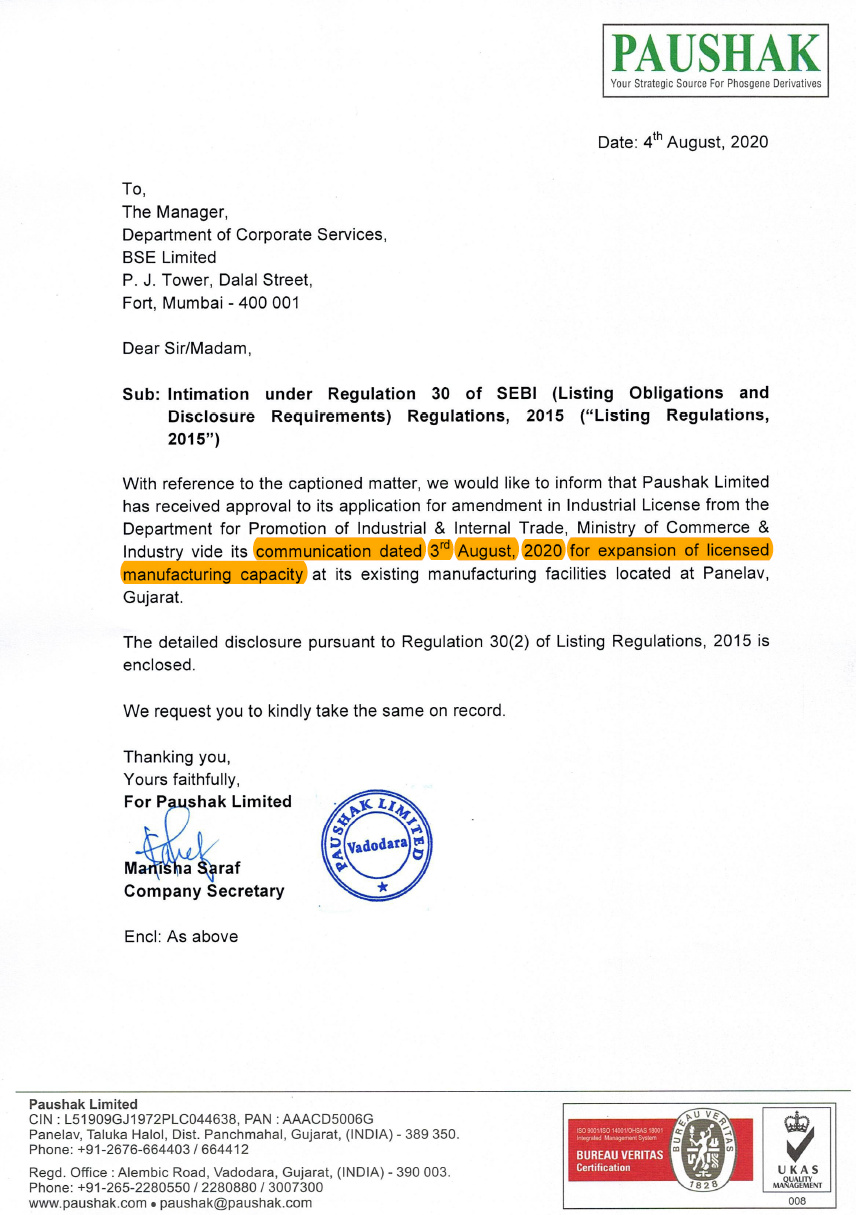

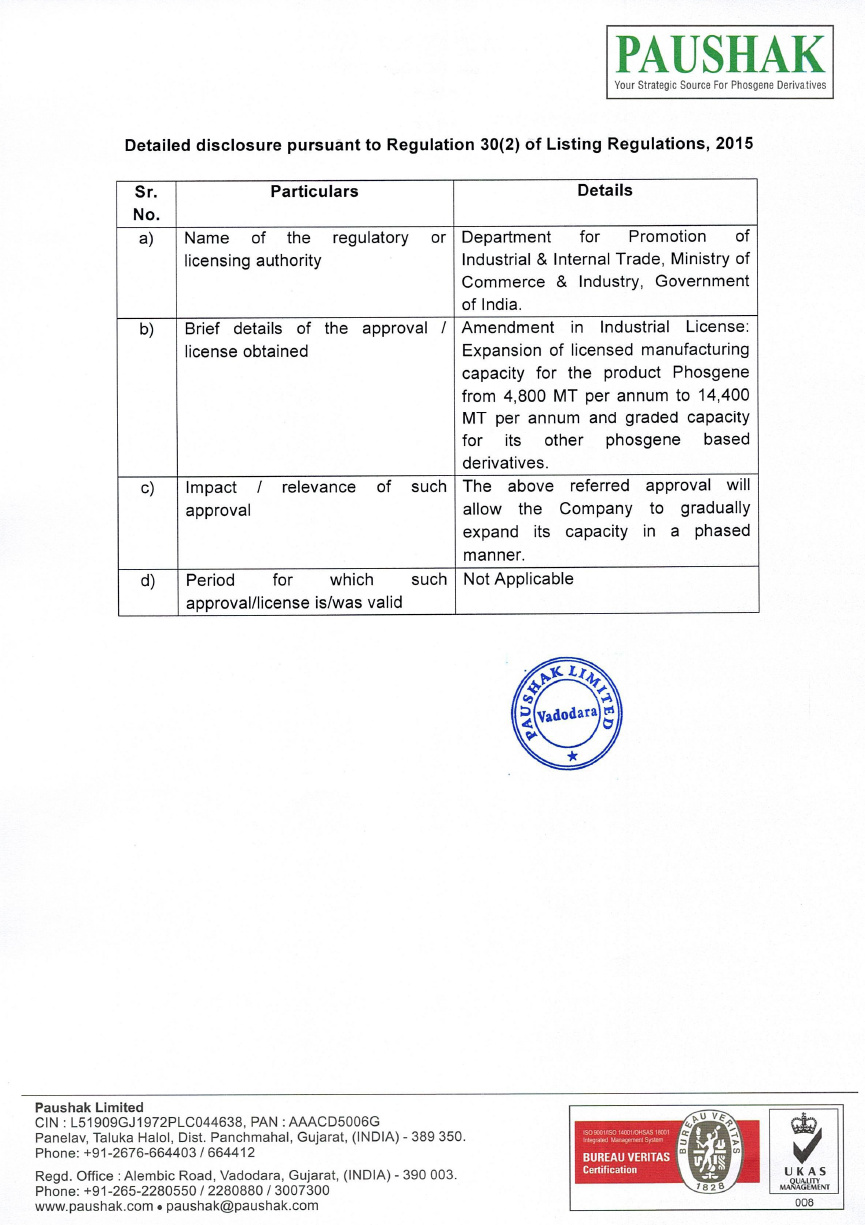

Your Company has also applied for expansion of its Phosgene capacity and is going through regulatory process & expect to have approval within FY 2020-21. This will help your Company to accelerate the growth in near future where opportunities have already been identified and we are working to scale up.

The tone of the management is extremely positive and bullish. If they are able to get even one customer for contract manufacturing it will be a great fillip to their reputation and financials.

11 Likes

The analysis summery highlights all the negative points.

5 Likes

In last 2-session it went up more than Rs 800…any positive news or development happening ?

Some people still choose to overlook management quality. This analysis by Dr. Vijay Malik should serve them as a good and painful reminder of their mistakes

3 Likes

Paushak Limited – Another PI in the making…Investing in Plant, people, process…

Written by Jeevan Patwa (04 Aug 2020)

Alembic group company, debt free balance sheet, 3x capacity expansion and entry into CSM with one global MNC tie up…Paushak is capitalizing on its Phosgenation strength. Paushak is Phosgene specialist with 40 years history of phosgene operations. Only other Indian player is Atul limited.

It announced receiving ministry approval for 3x expansion today on 4th August.

Average fixed assets for last 3 years is 38 crs and it is undergoing 120 crs capex …almost 1x sales and 3x profits…gives ample visibility for future…post completion it may generate 500 crs top line and similar level of PBT margins. Expansion will be funded through internal accruals with cash and investment value being 165 crs as on Mar-20. Company already started with modernization of old plant and complete expansion will happen in phases in next 2-3 years.

FY20 annual report mentions tie-up with global MNC…this marks Paushak entry into lucrative CSM space…Phosgene finds application in Pharma, agro chemicals and performance products…With new expansion, Paushak will be the partner of choice for any phosgene based applications for big pharma and Agro chem companies. This expansion will set the stage for Paushak for becoming niche CRAMS / CSM player in pharma and agro chemicals industry…it would be generating more than 100 crs free cash flow every year post that …

Look at last three years financials…Average gross margins 64%, PBT margins 30%, non-cash, non-investment RoE of 40%+…one of the best margin profile and return ratios in specialty chemicals…employee cost of 15%…highest among peers…this shows focus on R&D. It developed 7-8 products in last 2-3 years. As per management in 2019 AGM, focus is developing high margin products…

Paushak was one of the few companies to offer promotions and wage hike in Mar-20 during Covid-19 (check the twitter)…Paushak done massive recruitment pre-Covid for new plant operations…(can be seen from news paper advertisement)…Paushak is one of 63 companies in India to receive prestigious “Responsible Care” logo…this shows the commitment towards safety and environment…

Investment in plant, people, process going to reap great returns over long term…

8 Likes

Did any of the boarders attend the AGM? If yes, please do share an update on the thread, will be very helpful. I tried attending through electronic media via NSDL platform, but was disappointed to be unable to attend. Thanks in advance.

Attended the AGM . Was late though since I was trying for the first time to attend on online AGM (For that matter any AGM  ). Will try and post the points that I was able to capture.

). Will try and post the points that I was able to capture.

Attendees for the AGM from the Management side

Chirayu Amin : Chairman

Abhijit Joshi: MD

Ambareesh Dixit : COO (Hes the hands on guys who runs the business).

Kirti Shah: CFO

Top Management : Atul Patel, Vijay Gandhi, Amit Goradia

I missed the opening comments by Mr. Amin.

The key points from the Q&A which was addressed by Ambareesh Dixit and Kriti Shah.

-

The company recieved final clearance for expansion of the capacity from 400 MT to 1200 MT.

-

This 3x capex would take 2 to 3 years to be fully operational.

-

While they dont have major competition in India there is cut throat competition from Chinese, Japanese and European companies.

-

The company has introduced 6-7 new products in last 3-4 years .

-

Not able to share the top 10 customer details .

-

Company has a large basket of products . Not dependent on a single product.

-

Company is currently utilizing almost 100% of their down stream capacity.

-

Pharma is the largest segment they cater to followed by Agrochemical.

-

Somebody asked about CRAMS opportunity but they chose not to answer.

-

USP of Paushak as per the management : Experience, Focus on safety, Diversified portfolio, Not engaged in marketing end products thus customers dont feel threatened.

-

On China: There are huge capacities in China. China is a long term threat. Looking to build a technology and cost advantage to overcome chinese competition.

-

Most of the Assets are milked for 10 to 20 yrs.

-

Payback period of Capex is estimated to be 5 years.

-

Despite Covid plants have been running.

-

No plans for NSE listing soon.

-

Preferential shares will be held till redemption.

-

Want to become a global player.

In the closing comments Mr. Amin said that their vision is to revamp/modernize /build world class operations , focus on quality and technology. He seemed bullish on the future prospects of the company.

As usual management was not forthcoming with many details , but seemed bullish on the future. The capacity addition is the key. If they can manage it well with a 2x type Asset turn then the opportunity is huge.

13 Likes

Thanks @Midhunjoe for the notes from AGM, much appreciate it.

The long delayed final clearance for the expansion was certainly overdue, so that’s a big plus. Couple of days prior to the AGM, had found this

Not sure if there is a direct co-relation, but this approval seems to have been cleared on 10th July, and given that the official government documents on this decision would have taken (assuming) a week to come out by 17 July or so. And the stock seems to have been on a rocket booster mode from the very next day (20th July), vertically taking off from Rs 2678 to Rs 3970 on July 28. That’s a gain of about Rs 1292 or 48% in just 7 trading sessions, notching up a spectacular 12 points on P/E multiples! (from 24 to 36). All this in just few days after the decision was officially made, and just a few days prior to the news being made public at the AGM.

Interestingly, on 4th Aug 2020 at 12:07 PM, on the day the AGM, just about 20 minutes prior to start of AGM, company shared a disclosure with BSE, informing about receiving the approval of capacity expansion ![]()

Maybe this is just co-incidence and conjecture. But its quiet a strong co-incidence. Or maybe the information asymmetry still has a critical role to play, even in the age of internet and social media. ![]()

Disclosure: Have a very small tracking position, looking to add at lower levels.

7 Likes

My guess is , 3x revenue in 3 years and OPM remaining same (best case scenario) stock is available at forward PE of 10-12 PE which is long term average, looks like story has already priced in quite well.

1 Like

can someone please share the excat usage of posgane…

pharma and agr chemical is very open ended

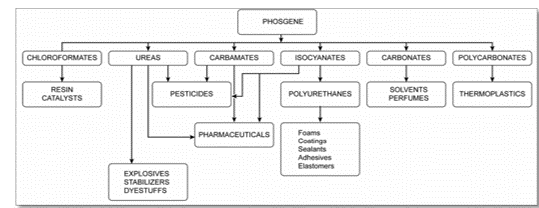

Applications of Phosgene

3 Likes

@kartik_bhat thanks a ton

This is fairly exchaustive…

Would you hv more info on pharma. What is it used for

Paushak is going great guns. Crossed 8k . Any further news on capacity / business etc.

1 Like

Hello! Here is my article that attempts to analyze and value Paushak Ltd!

Paushak: Has The Stock Gotten Way Too Ahead Of Itself?

Paushak is India’s largest phosgene-based specialty chemical manufacturer. It belongs to the storied Alembic Group of Companies which set up one of the first pharmaceutical plants in India. Paushak enjoys an unblemished track record of over 35 years and has established itself as a market leader across much of its product portfolio.

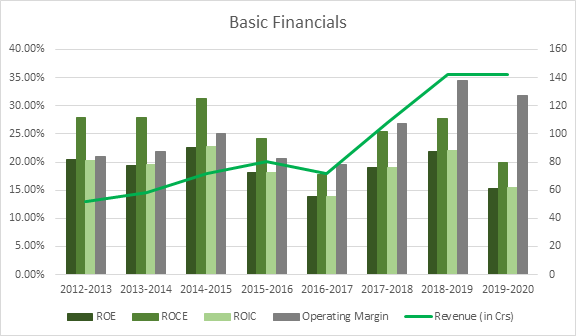

A 10-Year Revenue CAGR of 19% and 10 -Year Profit CAGR of 31% have led to handsome returns for investors, a 10-Year Stock Return CAGR of 60%!

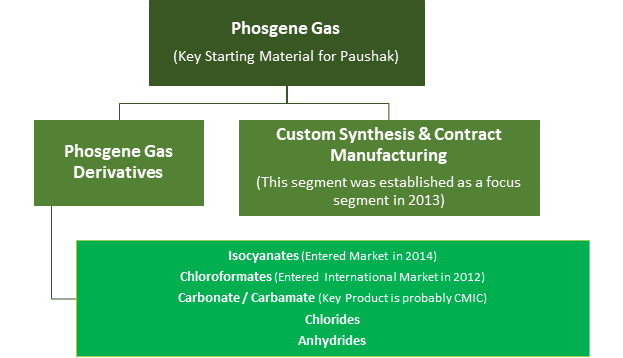

Paushak’s Business Model:

Paushak’s business model has been relatively resilient due to the hazardous nature of Phosgene Chemistry, and the subsequent government regulations that act as entry barriers. The company supplies phosgene-based derivatives (intermediates) to the Pharmaceutical, Agrochemical, and Performance Chemical industries.

Let us quickly understand what Phosgene is and why it enjoys strict regulation.

What is Phosgene?

- It is an organic chemical compound that exists in the form of a colorless gas, which is highly poisonous and is considered a viable chemical warfare agent. Phosgene can cause pulmonary edema and suffocation.

- It finds use in a vast multitude of areas – Organic synthesis, Dyes, Pharmaceuticals, Herbicides, Insecticides, Synthetic Foam (roughly 30% of entire Phosgene market), Resin, Polymers.

- All phosgene plants manufacturing over 30 tons of phosgene a year need to be declared to the OPCW (Organization for the Prohibition of Chemical Weapons). It is relatively easy to produce when compared to advanced chemical warfare weapons.

The toxicity as well as the relative ease with which it can be produced have led to a scarcity in the manufacturing permits that are issued. Hence, this stringent government regulation deters competition from entering this segment. Existing players too face an arduous process in procuring the required permits for expanding manufacturing facilities.

Paushak’s business strategy over the past few years can be summed up simply into three core areas:

- Vertical Integration

- Backward integration into Phosgene Gas.

- Forward Integration into newer complex Phosgene based derivatives. Paushak has been working on improving its ability to handle multi-tier complex reactions for high value products which are generally required by innovator companies.

- Low-Cost Producer

- Backward integration into Phosgene Gas has aided the company in controlling costs. However, it is still reliant on crude (thereby exposing it to some price volatility) for some of the raw materials.

- Over the years, the company has worked towards driving higher yields and improving efficiencies of the manufacturing processes it undertakes. In 2017, it commercialized a new solvent free manufacturing process which helped cut down on energy costs associated with solvent recovery in the older process.

- It has actively worked on lowering its Power & Fuel costs. A breakthrough came in 2016, when they were able to improve the thermal efficiency of their boilers from 62% to 74%. The company has set up a windmill for captive consumption and is looking towards harnessing solar energy in the future. Such improvements along with continuous efforts on running a tight ship have helped lower overall costs.

- The company recently got approval for tripling their Phosgene capacity from 4,800 MT to 14,400 MT (This approval process took about 3 years to get approved) at a total approximate cost of INR 120 Crores which is being funded entirely by internal accruals. The company hopes to attain economies of scale and become highly cost competitive on a global scale.

- Import Substitution

- Paushak has been working on developing and scaling indigenous technology for some of their products. This has helped them become highly competitive and has allowed them to plug some imports coming from China.

Paushak’s Business Segments:

The company has a vast plethora of products in their portfolio list; however, they are not forthcoming about which products constitute their core!

The Contract Manufacturing segment has only recently started seeing interest. The company is in talks with one global agrochemical major (there have been no updates on the progress yet).

End User Industries Served by Paushak:

- Pharmaceutical

- Legacy Business Segment.

- It supplies pharmaceutical intermediates to Generic Pharma companies in India.

- This segment has been prone to demand stagnation and pricing pressures in the past due to Generic Pharma companies’ woes in the US.

- Agrochemical

- New Business Segment launched in 2017.

- It supplies agrochemical intermediates and manufactures pesticides.

- This segment has been a growth driver since inception. Today, the company is looking to partner with global agrochemical majors (most likely for multi-tier complex reactions catering to innovators).

- Performance Chemicals

- Legacy Business Segment.

- It supplies intermediates to the dye and pigment industries (textiles, paint, coatings).

Competitive Advantages & Economic Moats Enjoyed by Paushak:

- Vertical Integration

- Low-Cost Producer (however, it is yet to establish itself as ‘the’ Lowest Cost Producer)

- Economies of Scale

- Barriers to Entry further heightened due to stringent government regulation and arduous process in getting licenses (for new entrants and for existing capacity expansions). On an average, any approval takes between 4-5 years.

- The key market of Paushak is the phosgene-based specialty derivatives catering to the Pharmaceutical and Agrochemical industries. These markets contribute to roughly 10% of the entire Phosgene market. Hence, the market may be too small and too specialized (due to high quality requirements) for the larger players to enter. This could be one of the reasons why Paushak has been facing competition from limited players (primarily from China).

Risks Faced by Paushak:

- Hazardous chemistry that necessitates the need for heightened levels of vigilance. Furthermore, any mishaps at the company’s facilities could spell long lasting trouble.

- A lot of the company’s raw materials are derivatives of crude, thereby exposing the company to crude oil price fluctuations.

- Foreign Currency Exchange Fluctuations.

- Despite being cost competitive, Chinese imports continue to provide stiff competition, leading to pricing power erosion. Key competitors are; Domestic – Atul & UPL, International – Covestro, Yantai Wanhua, BASF, DowDuPont.

- Slowdown in end-user industries will affect the company’s performance.

- Delays in capacity expansion execution.

- Current Proposed Expansion – 4,800 MT to 14,400 MT.

- Previous Largest Expansion (2014) – 1,440 MT to 4,800 MT.

- Massive difference in scale!

- The company changed its policy for recognition of receivables, payables, and working capital in 2018-2019. I dug deeper into the new policy, but found no change in the explanation (it was the same as that of the previous year). The company did adopt Ind AS 115 in 2018-2019 (maybe this caused some change in recognition policy, you may dig deeper through this link – https://mca.gov.in/Ministry/pdf/INDAS115.pdf). In some circumstances, changing recognition policies are a way of covering up certain business shortcomings.

- Related Party Transactions (RPT) galore! RPT’s are a natural occurrence when dealing with group companies. However, the group seems to use Paushak as a piggy bank at times.

Opportunities:

- Potential to grow revenues substantially following completion of proposed capex (full ramp up expected by 2022-2023).

- Generic Pharmaceutical companies have been faring favorably which is a positive boost to Paushak.

- The ‘China + 1’ strategy is something that Paushak hopes to leverage going forward.

- Agrochemical and Pharmaceutical demand generally tend to be fairly steady.

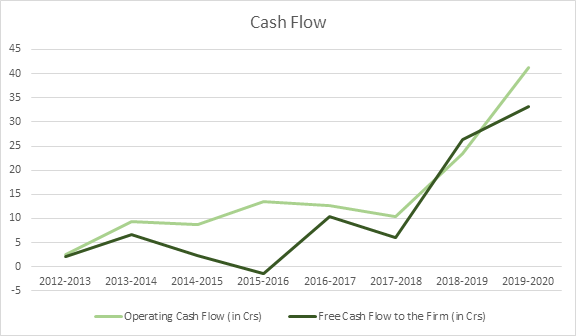

Financials:

Paushak is a debt-free company (has been near debt-free for the past 8 years) and expects to continue this trend.

Valuation:

The key valuation driver for Paushak is the new capacity coming online. Unfortunately, we do not have any data regarding the revenue potential. In my valuation, I decided to use a Fixed Asset Turnover of 3.5 which is slightly below the 8 year average of 3.94. This leads me towards a 10 Year Revenue CAGR of 16% (I feel that I am being quite optimistic in this scenario).

I believe that operating margins above 30% are not sustainable in the future. I have modeled margins to remain rangebound between 21% and 26%, with Terminal Year stable margins at 22%.

Cost of Capital (Terminal Year) stands at 8.81% with an ROIC of 10.81%.

My estimates lead to a valuation of INR 2176.95 to INR 2436.79 per share, well below the current market price of INR 7971.65

Conclusion:

Paushak has generated tremendous wealth for its shareholders over the past decade surging from a high of INR 122.7 in 2011 to a high of INR 9479 in 2021 (as of today).

Over the course of a year, the stock has skyrocketed from a low of INR 1301 to a high of INR 9479, triggered by the approval for tripling of capacity along with a relatively well-moated business.

My biggest concern surrounding my valuation would be the lack of data about: Revenue Potential from New Capacities, Timelines, and Key Products. The lack of information and the ensuing uncertainty is a key risk when investing in smaller companies, justifying an explicit application of Margin of Safety.

To recapitulate, Paushak does seem significantly overvalued, with the ‘overvalued’ nature being largely contingent on the capacity expansion coming to fruition!

14 Likes

Decent results. Jump in net profit. CWIP OF 60 Cr.

Plant closed from 28 april due to govt restrictions on use of oxygen ( shud be short term ).

Holding