HI,

Came across this link from another message board. It says that Paushak has got permission in Sep’18 from govt to expand capacity from 898 tons to 2500 tons per month.

DISCLOSURE : Have a small position in this stock.

HI,

Came across this link from another message board. It says that Paushak has got permission in Sep’18 from govt to expand capacity from 898 tons to 2500 tons per month.

DISCLOSURE : Have a small position in this stock.

Paushak Ltd is out of ASM list w.e.f. 7th Jan 2019.

Sorry for a stupid question, what happens when the company is on asm list ?

I am very surprised to see today’s date on that article. Jan 21st, 2019.

When was that happened?

Guess its automatically taking the date on which you open the article. I just tried it just now and it was showing todays date.

Yes, but then website is not bankable.

Disc: not Invested.

just rechecked, the original article is on 13 Sep, 2018. Maybe there is a software issue which is why the current date is showing up.

Good results by paushak on that back of a higher base last year. Sales up 29% , PAT up 45%.

any specific reason for this fall despite good results.Appreciate your inputs.

18_Jun_2018_150550510UQJ1B8Y0Annexure-AdditionalDocuments.pdf (744.3 KB)

Attaching a pdf document in which paushak is seeking expansion of capacity from 400MT per month to 1200 MT per month. There is also a response from the authorities.

Disclosure - Am invested

look at the margins. they hav fallen from 28% to 25%

Hi Hamir,

I got to know from the post that you are tracking the stock. I am interested in this stock and It will really help me if you can answer few question as you own the company

Hi, thanks for reaching out … will let you know as I understand this business.

Cyclicality - Dont think this business is cyclical, they produce highly niche products. Biggest plus point or moat is that there are very few in the world that can produce this chemical primarily due to inability to handle this product ( it is very hazardous) and requirements of high safety standards in mfg beside it being a niche category. Am specifically saying it because its a niche business. In India Atul Ltd is the only other company which can compete.

Buy Back - They had a buy back recently in which 1700 is the base price. In a buy back the promoters generally send out a message that the buy back value is the floor price and they would value it much higher.

Phosgene Approval - please go through the link, to my memory it says that approvals have been sought and provided.

I suggest that you also go through the MD&A in the annual report. Interesting thing mentioned in it is that they are now making import substitutes of products which were produced in China and else where. Probably the reason why the capex is underway. They had 120 MT per month capacity which was then increased to 400 MT and now I understand that its to be 1200 MT per month. With this kind of expansion and product profile I would like to assume that the share value would be higher.

Trust that this answers your queries. I have provided inputs as per my assessment and understanding. Happy to get views from others.

Excellent Q4 results but very low dividend payout

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=cbc0d113-fe51-4ebb-90e8-a83b11baed0e

Well they are growing and are building a large capital WIP

It has to be financed by retained earnings

Better to preserve cash

Good results again. 22% jump in revenues ( YoY), 36 % jump in profit before tax and exceptional items. Netprofit optically down, as they had a sale of land worth 10.15 crore as an exceptional item.

If company is so thinly traded on BSE what was the point in buyback? Also they have plan for capital expenditure in coming years, can someone explain about this?

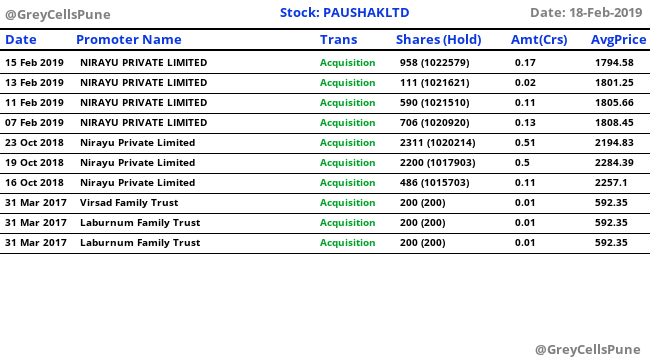

As per recent filing with BSE, ace investor Mr. Ashish Kacholia holds 1.19% in Paushak Ltd. Till last quarter, his name did not appear in shareholder list holding more than 1.00%