Recently I cashed in my holdings in Paushak due to personal reasons. Just wanted to make a disclosure.

I have no more holdings in Paushak Ltd.

Regards

Recently I cashed in my holdings in Paushak due to personal reasons. Just wanted to make a disclosure.

I have no more holdings in Paushak Ltd.

Regards

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/B719B7C4_47F9_4F77_B847_FCE252A8FC04_174415.pdf

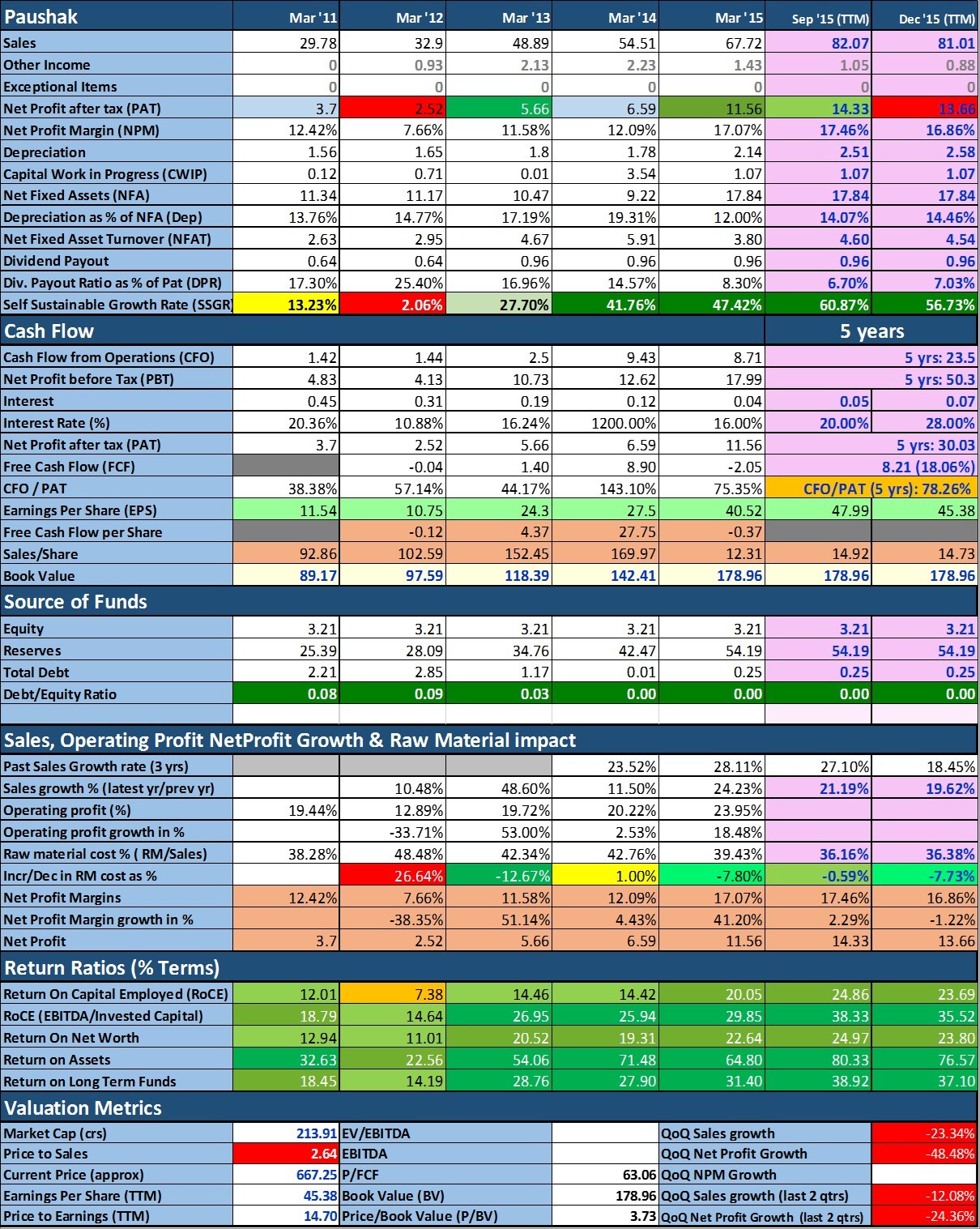

Q3 Results came out. Profit took a big dive. Stock may get bashed up

PS - invested

Anyone still holding/following? any comments/views?

well, Rallis India Ltd also reported -20% growth. As last year monsoon was not supporting for Agro Chemical company, So it’s expected to undergrowth.

The current valuation on Paushk is 15 p/e which is below than Nifty p/e of 19. So everything is already discounted in the stock price.

The company is not into agro chemical but into pharma intermediates. I think this is one of the weak quarter and their is no need to panic.

Management is optimistic is looking for new products and markets therefore it is long term bet.

The company has environment clearance for 400mt and current capacity is 200mt therefore it looks like a good long term bet.

I did not have the patience. took STCL today… lesson learnt…nothing on screen matters until it hits ur bank a/c…to imagine that I had 2x in this stock, on paper, it looks as if ages before but just months ago. Maybe, given the carnage in mid and small cap, this may be available at reasonable valuations in future

Is this just a one off bad qtr. ?

any idea who are the major clients like ?

Is this the only bad qtrs or start of series of bad qtrs? Whats the data point of such claims? Please put them here so we can all benefit. That said I am myself going to dig this in 1/2 weeks. Would appreciate if anybody could put some data point forward.

maven,

did you look at he nos.

[ Q315 WRT Q316 ]

top line : dropped approx. 1cr

Bottomline : dropped appr. 80 lakhs.

Any idea what is the reason for the unusual drop in sales ?

Not yet. There is no evidence that leads to any sort of conclusion. Is management commentary available post the results?

That said the company still has a good RoCE on TTM basis even after drop in sales and profit. In fact last 2 qtrs it has shown negative sales and profit growth on QoQ basis. For a stock commanding higher P/S and PE need to show growth and that too consistently. My scrutiny about the halting of growth and or stopping of growth is still in progress.

Hi Guys,

I am a new member and this is my first post.

Disclosure: Paushak forms around 5% of my holdings. Buy Price : 605.51

The Net profit for the period of Q1FY17 is the same as that for the Q1FY16 i.e 321 lacs. This seems very strange to me.

Also the profit for FY16 was marginally less that the profit for FY15. From the books I can only see that this is due to the increased Depreciation and expenses(Stores, Spares & Containers consumed and Manufacturing expenses).

Has Paushak hit a plateau and has the growth stalled?

Also I read about drug manufacturers in Europe and America moving away from the Phosgene related drugs. But since Phosgene can only be transported locally and assuming that that is what Paushak does, has there has been some adverse scenario in the Indian market?

There is noting in the annual reports except a mention of competition putting pressure on the prices.

Also if I disregard this years results, the Book Value and Earnings of Paushak sound quite attractive at the current level.

If anyone has any info on any of the above points, kindly do share.

Thank you so much in advance

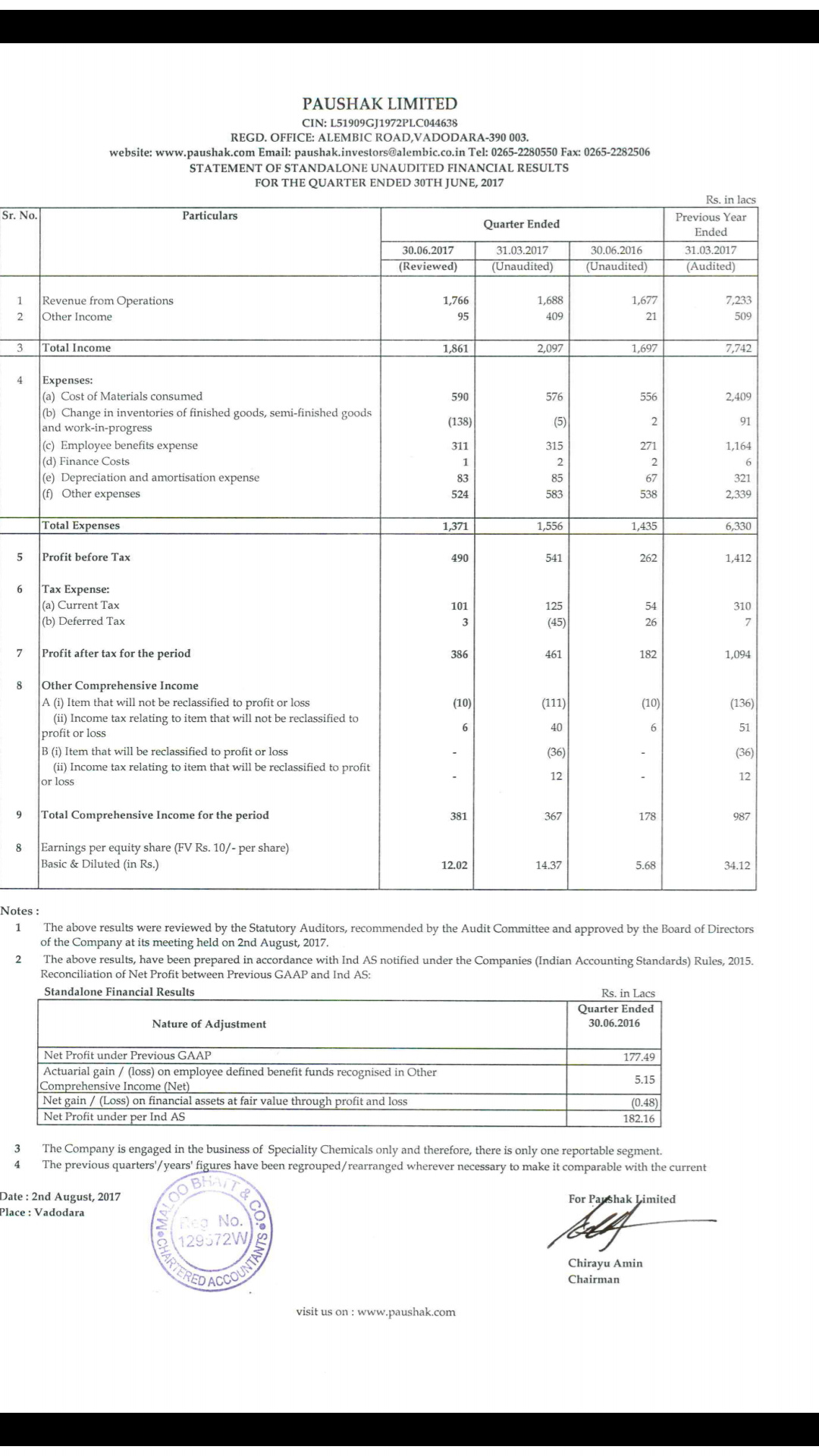

Paushak posted a great set of numbers for q1 2018.

Sales up 10%, PBT up 87%, PAT up 114% . Dividend of 3 per share.

After a lacklustre 2017, this year Seems to be good for paushak. Q2 results show sales up 8.2%, PBT up 140%, PAT up 170% Y-o-Y. The capital work in progress is again at 1.4cr which seems to have finished as in the last balance sheet.? Maintenance CapEx? The only negative seems to be 24 % jump in receivables which needs to be monitored.

0aa2ee05-0760-4aac-9ad8-d375a8e4a6fb.pdf (1020.8 KB)

But opportunity to make big money in this stock is behind us.

The real big money were made by people who bought when the stock was at PE of 2x in 2013 (PB of 0.5) and then the market rerated it to PE of 20x . Having said that I am still curious why was it available at such low valuations back then.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/44e81382-02cb-4654-afe0-3428861d4f63.pdf

Company to consider buy back along with financial results on 24th jan

http://www.bseindia.com/xml-data/corpfiling/AttachLive/9d182fa1-7d90-4dde-9f01-d1eb4754d968.pdf sales up 50%, profit nearly doubled. Buy back announced for 3.9% of total equity at a 15% premium to current price

FY 18 results and snippets from the AR

Positives:

Management commentary:

Risks;

chinese pressures on pricing

crude oil

foreign currency fluctuation

What would be the impact of rising crude oil on Q1 results?

Great show by paushak!

sales up 63%, PAT up 270% ( Y-o-Y). This was a bit unexpected. sales have more than taken care of raw material expense which have gone up from 33.4% to 45% of sales.

Sales and profit up 60%. Trade receivables down, good cash on hand. Good set of results