The above shows the timeline of commercialisation of capex, mostly by sept2021. Also around 65 cr , for next fiscal years for downstream products. Paushak has sustained margins even though oil has been selling high. It will be interesting to note, year end results.

1 Like

One of the main concerns is their dependence on Industrial Oxygen supplies for the operations. I believe their plant is shut since end of April for the same reason. Not sure if there is any plans to have backward integration for industrial oxygen?

1 Like

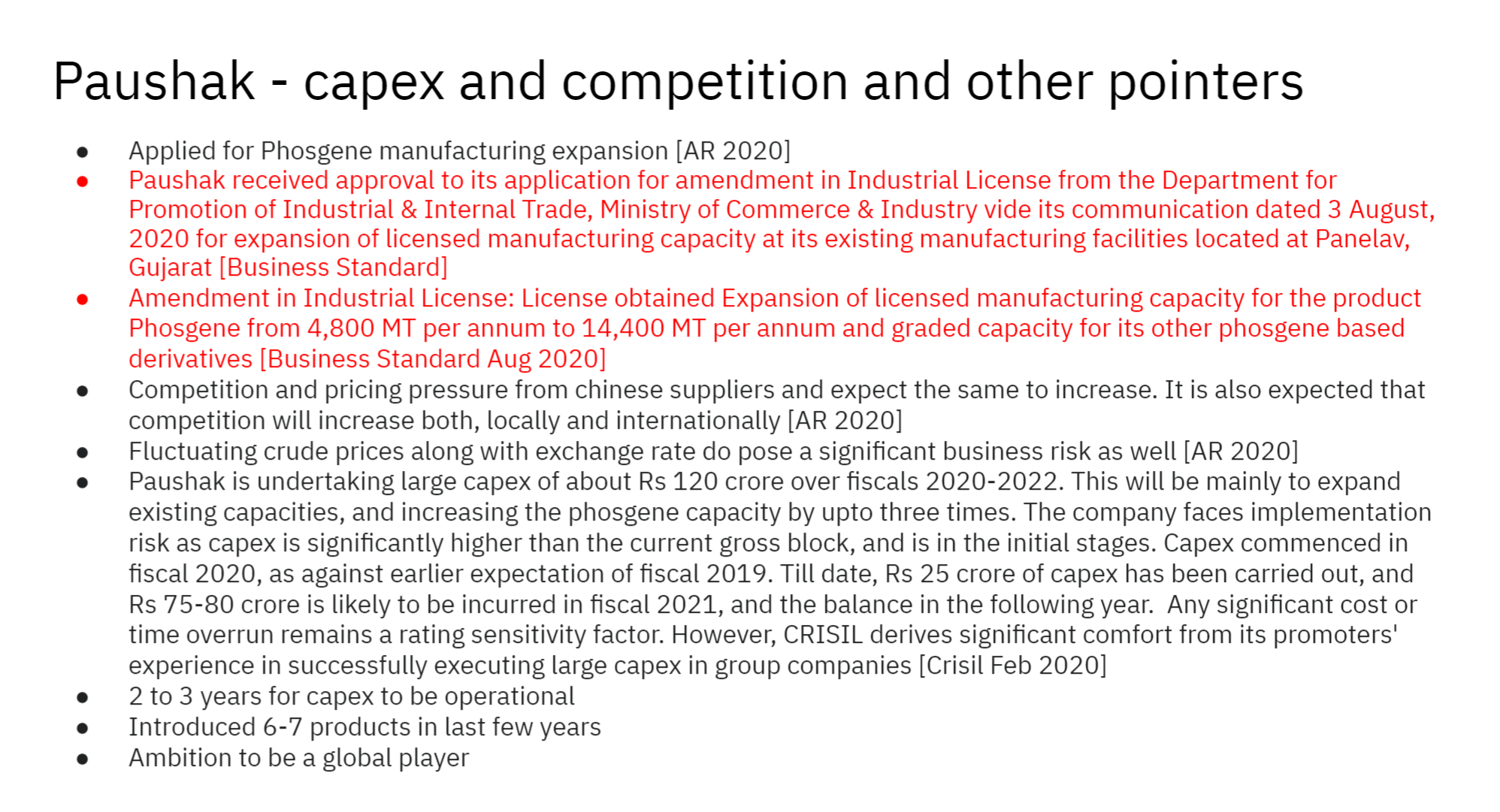

Your Company also received approval from the Government of India for expanding Phosgene capacity from 4800 MT/Year to 14400 MT/Year after all necessary legal compliances and approvals. Your Company had planned a capex programme of ₹120 Cr. to expand and accelerate the growth with identified opportunities. You would be pleased to know that your Company is the midst of project implementation for enhancing Phosgene Capacity and also one large derivatives plant

as downstream with associated infrastructure of utilities, etc. Your Company has also hired the services of one of the globally renowned design consultants to ensure that these plants are as per global standards of engineering, design & safety practices and would be state of the art facilities with full automation while benchmarking with global standards.

Above is the extract from the annual report …

1 Like

Hi @hamir_asher

This is something which they did in August 2020 I believe. The approval had come then. Some of my notes from last year.

Rgds

Deepak

Disc: Continue to be invested. No txns in last 30 days. Not a registered adviser/analyst.

4 Likes

Good results on all fronts. https://www.bseindia.com/xml-data/corpfiling/AttachLive/457ec934-e06b-41b6-ba82-130b7368c92f.pdf

"The new projects are largely in pre commissioning stage, the results of which will be seen in next half, and full impact next year. "

2 Likes

There are significant improvements happening in Paushak’s outlook and their aspirations.

- Capex is 2 times their current size. Management did not show inclination to invest till last so many years. Infact their topline was stable for the last 5 years - ~140 cr. Now this capex which triples their gross block is getting commissioned

- Company is looking to enter into some CMO opportunities/business also. They have been talking with some global companies for these opportunities and hopefully they may get some success. The below is the excerpt from their 2021AR. - “With change in geopolitical situation, the demand from domestic as well as global customers will also open new avenues for us. Paushak will continue to invest & expand its capabilities & capacities to accelerate the growth of business in domestic as well international market.”

- Not only this expansion but company is also suggesting that they will want to grow in future also through expansion - things which they did not did earlier.

- Post commissioning of the capex, they should be able to utilize the expanded capacity in 2 years (My guess, no inputs from Mgmt) which means that there revenues will triple from 140 cr to ~400 cr in 2-3 years with net profit of ~120 Cr (benefit of operating leverage should accrue).

The company after the recent correction was trading at ~2500 Cr marketcap which to me was attractive.

Regards

Nikhil

Disc: Invested.

9 Likes

Puashak q3 fy22 results:

https://www.equitybulls.com/category.php?id=306237

Result doesn’t seems to be good.

It seems there capacity expansion hasn’t commence in q3

Disc: Invested from very lower levels

1 Like

Uptrending numbers posted by the company for Q4 FY21-22. Dividend doubled from Rs. 6 in PY to Rs. 12.

2 Likes

Udit Amin Interview post the last results

5 Likes

Excerpt for Annual report, capacity is now 3x and has started contributing from 3rd qtr. A small para in the report but conveys a lot of things.

3 Likes

Paushak

(Few important points from Annual report 2022 and credit rating @july 2022)

1 …Backward integration

=Operating profitability remained strong at 36%, owing to a high degree of backward integration in the form of phosgene gas manufacturing capacity, even as the rest of the industry reeled from increasing input prices

=Backward integration of operations has led to robust operating margin (36% in fiscal 2022 and 35.8% in fiscal 2021). Return on capital employed was healthy at 15.7% in fiscal 2022. While most of the specialty chemicals industry depends heavily on imports for their raw material supplies, the company has a low import bill.

2…Revenue growth

=The full year benefit of enhanced capacity amidst steady product prices should lead to about 30% revenue growth in fiscal 2023, while operating profitability is expected to sustain at about 30% over the medium term.

3…The company is one of the few players licenced to manufacture phosgene gas, which is highly restricted by the government.

4…Capex

A…Phosgene Capacity expansion

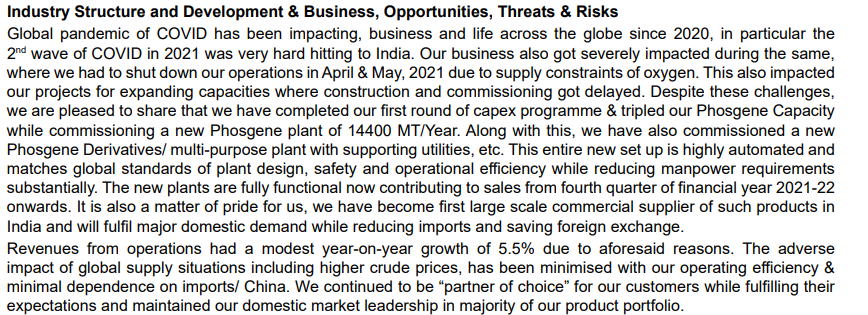

=We have completed our first round of capex programme & tripled our Phosgene Capacity while commissioning a new Phosgene plant of 14400 MT/Year (1200mt/month)

B…Multi-purpose plant

=Along with this, we have also commissioned a new

Phosgene Derivatives/ multi-purpose plant with supporting utilities, etc. This entire new set up is highly automated andmatches global standards of plant design, safety and operational efficiency while reducing manpower requirements substantially.

=The new plants are fully functional now contributing to sales from fourth quarter of financial year 2021-22

onwards.

=It is also a matter of pride for us, we have become first large scale commercial supplier of such products in India and will fulfil major domestic demand while reducing imports and saving foreign exchange

C…Future capex

=The company continues to have moderate capex plans averaging Rs 40-50 crore per annum over the medium term, which will be funded largely through internal accruals, thus building up its downstream capacities.

5…Diversification

=Revenue growth has picked up in the past four years, driven by diversification of customer base and product portfolio.

=Apart from pharmaceuticals, the company now caters to other sectors such as agro-chemicals and performance-based materials

6…Outlook:

=With the commissioning of the upstream and downstream capacities, we are focusing to expand domestically and globally while further expanding our operations.

= We are committed to invest more to create downstream capacities while developing newer technologies and product portfolios & improving our R&D capabilities.

= We have hired more technical resources with focus to grow capabilities. The new plants, just commissioned, will also catalyse our growth while demonstrating our technical capabilities, commitment and our vision to become a global technology leader in Phosgene and derivatives while creating niche for us & will help us to continue to be “Partner of Choice” for our customers.

Disc…invested

My latest portfolio

2 Likes

My Take On Paushak

- About Paushak

- MOAT

- Financials

- Valuation

- Suggestion

About Paushak

Incorporated in 1972, Paushak is managed by Mr. Chirayu Amin and his family members, promoters of Alembic Pharmaceuticals Ltd (rated ‘CRISIL AA+/Stable/CRISIL A1+’). Paushak manufactures phosgene-based specialty chemicals, used in the pharmaceuticals, agrochemicals, and performance-enhancement industries.

Phosgene’s market size is likely to be driven by its utilization in pharmaceutical, agrochemical, polycarbonates, and chemical industries. The demand for phosgene will be ever increasing and moreover, the demand will be fulfilled by existing players only as it is extremely difficult to set up plants for phosgene-based specialty chemical production

Paushak uses phosgene for 2 things - sell directly and use captively to create specialty chemicals. (According to the 2010 annual report)

MOAT: Phosgene is extremely poisonous and was used as a chemical weapon during World War I, where it was responsible for 85,000 deaths. It was a highly potent pulmonary irritant and quickly filled enemy trenches due to it being a heavy gas. Hence, the license to produce and handle phosgene is not given by the government to new entrants, making barriers to entry very high. License to increase capacity takes 4-5 years and Paushak has successfully increased its capacity from 1440 MT/Year to 4800 MT/year to 14400 MT/year in the last 15 years. The phosgene-based chemicals are essential and no other company can take the market share from Paushak due to extreme regulatory barriers, leading to an increase in demand met by Paushak only. Thus, making it a long-term value investment opportunity, at an appropriate valuation.

Financials

- Paushak has grown its sales from 30 Cr in 2011 to 150 Crores in 2022, leading to a 15.7% sales CAGR.

- The company has healthy margins with >30% EBITDA and ~25% PAT, >25% pre-tax ROCE

- 1 crore is needed to expand capacity by 80 MT/YEAR. The company completed a 120 Cr capex in 2022, thereby increasing the capacity from 4800 MT/year to 14400 MT/year. With the current capacity of 14400 MT/year, they have a maximum capacity to generate ~450 Crores of revenue, ~100 Crores of operating profit after tax, and ~85 Crores of net profit per year. The current increased capacity of 14400 MT/year may take ~7 years to reach this level of utilization.

Valuation

The current increased capacity of 14400 MT/year may take ~7 years to generate ~450 Crores of revenue, ~150 Crores of cash, and ~120 Crores of net profit per year. By this time I expect the company to get government approval for increasing their phosgene capacity even further, a trend which has been seen in the last 15 years when the company had 3 capacity expansions approved and successfully implemented (Paushak has successfully increased its capacity from 1440 MT/Year to 4800 MT/year to 14400 MT/year in the last 15 years)

Analyses suggest that ROIC is a major driver in the growth of valuation in the chemical sector across the globe (src: McKinsey)

The company has an ROIC of >40%, a very high ROIC vs an average ROIC of 15%. Generated a Net operating profit after tax of 36 Cr by employing ~40 crores of net working capital and ~40 crores of PPE

Having said all that the valuation seems very rich

- On the basis of EV/IC multiple: ~38x (last year’s numbers) vs the median multiple of ~2.5x for the companies in the Indian chemical sector.

- On basis of PE multiple: 85x vs the median multiple of ~20x for the companies in the Indian chemical sector.

- On the basis of a forward estimation: Even if we give the company a forward EV/IC of 19 (current median of top 10 valued chemical companies in India), after 7 years, the enterprise value will be ~4800 Cr (current EV is 3000 Cr), which is only a ~6.5% CAGR over 7 years.

Suggestion

Closely track the EV/IC multiple and price dip for Puashak. And start accumulating when EV/IC is below 12x.

13 Likes

Its damn overvalued. Even if they are able to do 120 Cr PAT by FY27 and market gives it 30x. It would be valued at 3600 Cr market cap (50% gain from current market cap). Non further calculation required.

It needs to fall more then 50% to be a buy (Depends on other opportunities as well).

1 Like

Corporate governance issues at Paushak?

— Tijori (@Tijori1) March 18, 2023

1. Paushak promoters took money in the form of loan from the company

2. They used this money to buy shares in Paushak and increase shareholding

3. Restructured the loan

talked about by @SmartSyncServ and added to knowledgebase! pic.twitter.com/8fn2m3aYg0

I think one should visit the link provided on the tijori link. It leads to a YouTube presentation on forensics where there is a 4 min portion mentioning paushak.

The discussion is a reference on promoters taking loan from company and using it to buyback its own shares, the fact is that from last 2 years the promoter holding is stable and has not changed much. The promoter buying is declared on exchanges and there is less than 10,000 shares traded most of which is internal transfer. There is a merger with another company which is alleged to favour promoters.

There is a mention of loans being rolled over and is made to look like a corporate governance issue. This is a normal thing and does not qualify in anyway as a corp gov issue.

There is a mention by a speaker that he knew someone who worked for Paushak and was there for 15 years and did not get promotion, once he ventured out he got double salary and a “3 level” higher designation, when he resigned Paushak management was willing to match the offer. This is highlihgted as an issue since as per the speaker the owners dont share stuff with employees. Just does not make sense , how is this governance issue.

As regards the money used to buy shares, no source or basis is provided excpet the fact that this is construed from the annual reports.

Somehow its seems just a wild allegation without substance specially when we hear the other reasons shown under corp gov.

Happy to be corrected if proven otherwise.

6 Likes

Any latest update on this company? I can hardly find any research reports, concalls and annual reports around it since last 12-18 months.

1 Like

Extracts from Annual Report -

- We are pleased to share that we have achieved rated capacities of the new plants while demonstrating

our technical expertise in developing indigenous technology platforms, launching new products and building state of

the art plants. These new automated plants have also been visited/audited by Global Customers/ Innovators from our

targeted segments resulting in more confidence and interest in our technical expertise and is expected to result in future

growth opportunities while establishing Paushak as serious global supplier for Phosgene derivatives. - Our major market like Pharmaceuticals and Agrochemicals are experiencing slow down along with price erosion and

intensified competition. This is expected to result in margin pressure in near future. However, the new plants have

catalysed our growth while demonstrating our technical capabilities, commitment and our vision to become a global

technology leader in Phosgene and its derivatives while creating niche for us. We are working on new technology

platforms while launching new products in near future while investing more to create downstream capacities. We remain

committed to be “Partner of Choice” for our customers while expanding R&D capabilities to support such launches with

addition of more technical resources.

10 Likes

Paushak ltd

( update from credit rating and annual report 2023)

PAUSHAK

1…Parental support

=Parental support from Nirayu Limited (Nirayu, rated ‘CRISIL AA+/Stable’), the holding company of the Alembic group. Nirayu overall holds a 53% stake in the company. This means a clearer intent by the parent to extend the requisite financial support in terms of letter of comfort, should it be required for future capital expenditure (capex) plans.

2…Capex

=Completion of 120cr capex in 2020-2022 for 3 times phosgene capacity.

=The company plans to undertake moderate capex plans of Rs 50-60 crore in the current fiscal, towards debottlenecking and corporate affairs.

3…FUTURE GROWTH

A…New plant

=The new plants have catalysed our growth while demonstrating our technical capabilities, commitment and our vision to become a global

technology leader in Phosgene and its derivatives while creating niche for us

B…Backward integration

=Backward integration of operations has led to robust operating margins (35% in fiscal 2023 and 36% in fiscal 2022). Return on capital employed was healthy at 19% in fiscal 2023.

=While most players in the specialty chemicals industry depend heavily on imports for their raw material supplies, the company has a low import bill.

C…New products

=We are working on new technology

platforms while launching new products in near future while investing more to create downstream capacities. We remain

committed to be “Partner of Choice” for our customers while expanding R&D capabilities to support such launches with addition of more technical resources.

D…Improving demand

=With the resurgence of Chinese manufacturers, pricing pressure and lower demand due to destocking being undertaken by customers, the first quarter of fiscal 2024 saw moderation in Paushak’s operating performance to Rs 49 crore of revenue and multi-quarter low margins of 25.4%

= However, with demand and pricing scenarios improving, operating performance is expected to recover, starting from the latter half of the fiscal, which would continue to be a key monitorable.

4…MOAT

A…Entry barrier

=The company is one of the few players licenced to manufacture phosgene gas, which is highly restricted by the government.

B…Backward integration

=Relatively stable margin despite headwinds of chemical industry.It is due to backward integration

=Paushak’s profitability, similar to other players in the specialty chemicals industry, remains susceptible to movement in the prices of key raw materials and end-user demand especially in the agrochemical and pharmaceutical industries.

=A dip in demand owing to destocking up the value chain, combined with some pricing corrections in the last 5-6 months owing to macroeconomic headwinds in 2023-2024 have led to margins moderating to 25% in the first quarter of fiscal 2024.

=However, a strong degree of backward integration and low fixed cost structure lends support.

Disc…invested

4 Likes

Paushak Ltd.'s stock price has corrected more than 50%. As per my openion this is could be due to a combination of factors, including delays in its capacity expansion plans and rising input costs.

The company’s capacity expansion plans have been delayed by two years. This is impacting the company’s ability to meet growing demand for its products. As a result, Paushak’s revenue declined by 3.36% year-over-year in the first quarter of fiscal 2023-24. This is the first time in over two years that the company’s revenue has declined.

Rising input costs are also putting pressure on Paushak’s margins. In the first quarter of fiscal 2023-24, the company’s net profit margin was 10.2%, down from 12.1% in the same quarter of the previous year.

The combination of delays in capacity expansion plans and rising input costs is likely to continue to weigh on Paushak’s financial performance in the coming quarters. Investors should carefully monitor the company’s financial performance to see if the recent decline in revenue and profit margin continues.

In addition to the number evidence provided in the previous paragraph, here are some other pieces of evidence that support the claim that Paushak Ltd.'s delayed capacity expansion plans and rising input costs are the major reasons for its decreasing performance and stock price correction:

- The company has announced that its capacity expansion project is now expected to be completed by the end of fiscal 2023-24, two years behind schedule.

- The company’s management has stated that rising input costs are putting pressure on its margins.

- Analysts have downgraded their earnings estimates for Paushak Ltd., citing the delays in capacity expansion plans and rising input costs as key concerns.

8 Likes