A curious case of Ruchi Soya, if you seen in 2016-2018 P&L (I referred rediff money) “admin expenses” went up 3x where as operating income went down in same proportions. This should have been an easy red flag to spot.

2 Likes

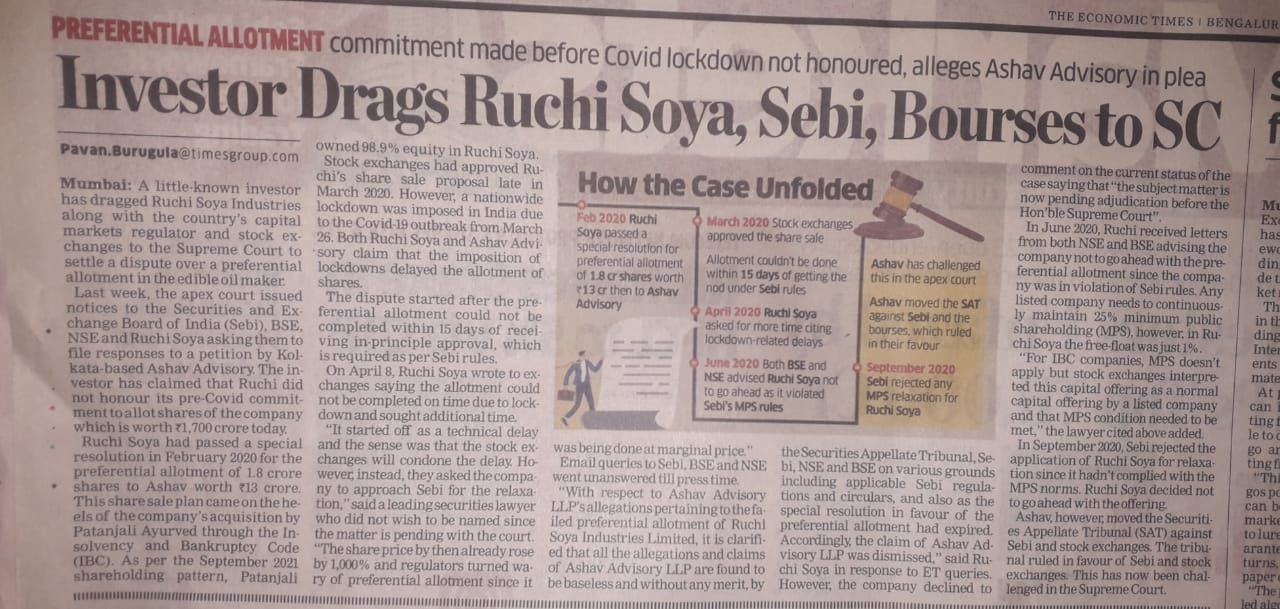

RUCHI soya FPO getting listed ON FRIDAY

Views invited . now a zero debt branded play with good distribution reach now backed by cash rich baba ji

I don’t see any scam in this. All businessmen do this. You take out loan from banks to acquire a company, you improve that company’s financials and then sale some stake (remember majority is still with Babaji) by FPO, to pare down the debt taken to buy that company…what’s wrong in this? Banks got their money back with interest, new investors are interested to subscribe to the FPO, then it seems all is well!

Having said that, only time will tell if those investors who applied for FPOs were taken for ride or not…

2 Likes

Fundamentals definitely seem to be improving. Revenues are increasing - any idea how much of that is because of Patanjali biscuit merger with Ruchi Soya?

Also how are new products of Nutrella faring and have fared during pandemic? like FMHG products?

Most importantly I am a bit wary of wild moves of this stock. Not sure if that is because of low float currently and this will stabilize like other FMCG firms …but when?

Also, strange things keep happening with Ruchi soya like withdrawal of FPO option etc. which I never heard before…

Disc: Applied in FPO in very small quantity to have a tracking position

1 Like

Patanjali biscuit contribution is negligible at Rs1000cr

1 Like

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

Do you mean 1000 cr for entire Fiscal year? Approx Dec 21 Q sales is 6280 cr so if this figure is for entire year then significant revenue increase looks organic…

If anyone has break up of revenue or even growth break up of subsegments in which Ruchi soya operates…would be good to know…Thanks

1 Like

You can check all necessary information in the AR 20-21

Dec 21 results

2 Likes

CEO’s interview on ET : Ruchi Soya | Patanjali: Ruchi Soya CEO on turning zero-debt co and rebranding as Patanjali Foods

1 Like

Sub. : Audio recording of the Investors and Analyst call

Pursuant to Regulation 30 and 46 (2) (oa) of the SEBI (Listing Obligations and Disclosure Requirements)

Regulations, 2015, as amended, we may inform you that the recording of audio call held on May 18, 2022

with the Investors and Analysts is available on the Company’s website i.e. www.ruchisoya.com.

The link to access the said audio recording is:

Chorus Call: Recording Downloader

Recording Id : ANT0420220518141380

this is the audio recording posted on youtube

If one listens then he will find Bharat shah of ASK discussing ( starts after 30 min ) the future growth with swami Ramdev and ramdev replying all the questions in his own energetic and emotional ways . I think the responses were perfect . there were amit jeswani of stallion and varinder bansal of omkara capital also asking a few things

3 Likes

Patanjali Foods Ltd - 5 Business Verticals

EDIBLE OIL - One of the largest edible oil refining company in India Brands across mass, value & premium segment Key Brands: Ruchi Gold, Mahakosh, Sunrich, Ruchi Star, Nutrela Vegetable Oil Crude Oil Refined Vegetable Oil Fats Vanaspati Bakery By-Products & Derivatives Crushing Refining

FOODS BUSINESS - Soya Flour & TSP(2) B. Noodles & Breakfast cereals, Biscuits, Cookies and Rusks C. Newy acquired food division of Patanjali Ayurveda Limited

NUTRACEUTICALS -Forayed into the Nutraceuticals and Wellness segment in the first quarter of FY2022. Co-branded under Patanjali and Nutrela brand names Key Segments: • Sports Nutrition • Medical Nutrition • General Nutrition

OIL PALM PLANTATION -Leading Indian player; MoUs with 11 state govt. • Allocated area of 6.02 lakh hectares, of which 59,239 hectares is under cultivation • Presence in 55 districts, engagement with 42,071 farm families

OTHERS

Oleochemicals: • value-based derivatives of castor, soya and palm • Domestic & export Wind Power: • Capacities across 11 locations with a total capacity of 84.6 MW, Located in Gandhidham (Gujarat) with close proximity to the Kandla and Mundra port

Manufacturing Prowess - Strategic Manufacturing facilities: 25processing plants (of which 19 are operational processing plants) across India, and access to 43 contract manufacturing units.

Revenue Split -

Edible Oil; largest category, accounting for 1/3rd of revenue has the potential to grow multifold on strong and well developed edible oil distribution base of Ruchi Soya Industries

• Top 2 products; Edible Oil and Ghee contribute to 64% of total sale

• Next 6 categories contribute to 36% revenue share; potential to grow multifold by leveraging Nutrela distribution base

• Consists of both high-margin, high-growth products along with high-volume, moderate growth products which shall have a positive impact on margin profile of the company

Future Business Growth may come from the Palm Oil Plantation business - Largest oil palm plantation company in India, with allocated area of 6.02 lakh hectares, of which 59,239 hectares is currently being utilized

• Backward integration strategy to create one of the largest palm oil plantation companies in India

• Public Private Partnership Business model, allows company to maintain an assetlight business model

• Completely digitized procurement and payment process • GEO tagging and other technological support

4 palm oil mills

Installed capacity - 900000

Produced – 467500

This is the Distribution Channel -

Big Basket, Walmart, MORE, Metro Cash & Carry, Spencers

4763 distributors

100 sale depots

524343 customer touchpoints

1,092 Chikitsalaya

3,260 Arogya Kendra operated by Patanjali Group

FY 2022 numbers -

Revenue – 24205

EBITDA – 1565 – EBITDA Margin 7.47%

PAT – 241.36 – PAT Margin 3.5%

YOY growth 48%

QOQ growth 37% June 2022

ROCE – 14.13%

ROE – 15.76%

Debt & Funding Metrics

External Debt paid 3072 cr

The Company has achieved Debt Free status post the FPO. Only Non-fund-based (LC Limits) of ~1,820 crores are being availed.

₹ 792 Cr being utilized for funding of Incremental Working capital

REvenue Split & EBITDA Margins -

88% of revenue comes from Oil & Vanaspati. This is a 3.96% EBITDA margin business

8.27% of revenue from Seed Extraction – This is a 6.37% EBITDA margin business

7.93% of revenue comes from Food Products - This is a 15.40 % EBITDA margin business

0.28% of revenue comes from Wind Turbine Power Generation. This is a 75.50 % EBITDA margin business

More about Palm Plantation & Government Support

Palm Oil Import

India imported around 133.52 lakh tonnes of edible oils costing around ₹ 80,000 crore. Out of all the imported edible oils, the share of palm oil is about 56%, followed by soybean oil at 27%. 74 lakh tonnes of palm oil imported. India Crude Palm Oil production 2.72 lakh tonnes as per 2021 stats

What is Palm Oil

Palm oil is derived from the fleshy mesocarp of the fruit, which contains about 45-55% of oil. Palm kernel oil, obtained from the kernel of oil palm, is the source of lauric oils. With quality planting material, irrigation and proper management, oil palm has the potential to produce 20-25 MT fresh fruit bunches (FFBs) per ha after attaining the age of 8- 9 years. In comparative terms the yield of palm oil is 5 times the yield of edible oil obtainable from traditional oilseeds

Government support to palm oil plantation

The government of India has continuously been making efforts to increase the area production of oil palm. For increased the availability of edible oils in the country and to reduce the import burden, various interventions since 1991-92 through schemes such as the Technology Mission on Oilseed & Pulses (TMOP), Integrated Scheme on Oilseeds, Pulses, Oil Palm and Maize (ISOPOM), Oil Palm Area Expansion (OPAE), National Mission on Oilseeds and Oil Palm (NMOOP) and the National Food Security Mission (NFSM)–Oilseeds & Oil Palm were under implementation in 13 States viz; Andhra Pradesh, Telangana, Chhattisgarh, Tamil Nadu, Kerala, Gujarat, Karnataka, Odisha, Mizoram, Nagaland, Assam, Arunachal Pradesh, Manipur with the funding pattern of 60:40 in case of general States and 90:10 in case of North-Eastern States and hill States.

IF they are able to execute the plantation business they wil go on to become the largest palm oil business in the country. They are targeting 7.5 lakh tonne of plam oil production in the next 30 years, lets extrapolate that to 2.5 lakh tone in next 10 years.

Indias current total Palm Oil production is 2.72 lakh tonne only. Promoter has 80% of shareholding and i think they will offload and bring it down to 75/70. they recently met with some of the big names from Indian mutual fund and pms industry.

Attaching the links to all the info i have shared here.

Investor meet & Business Overview - https://www.bseindia.com/xml-data/corpfiling/AttachLive/42025d11-091e-4b48-86bb-42017c3dbf51.pdf

Q4FY22 concall - https://www.bseindia.com/xml-data/corpfiling/AttachHis/4b162a7a-e46b-4339-8fc5-807a57e40f54.pdf

North East Palm Oil Plantation info - https://www.bseindia.com/xml-data/corpfiling/AttachLive/18fe299b-81db-48b4-baee-c552ea8d0c91.pdf

National Edible Oil Policy - https://www.pib.gov.in/PressReleasePage.aspx?PRID=1746942

Detailed Read on the National Mission on Edible Oil - https://nfsm.gov.in/Guidelines/NMEO-OPGUIEDELINES.pdf

I am invested and I will be slowly accumulating this stock. The liquidity in this stock is low and hence it may be volatile in price movement.

The biggest risk to the business is not being able to execute the plantation business. otherwise its a simple oil trading business (commodity play but essential commodity)

Growth drivers are the foods, and nutraceuticals business in the future, and that growth has not been factored into the price yet.

Waiting for the 2022 Annual Report to the get more detailed understanding on the company

4 Likes

Summarising my initial thoughts on Patanjali Foods. Q2FY23 results, will incorporate the acquired foods division from Patanjali (transferred wef July 1st, 2022). Please see attachment

In my limited understanding, the key to the stock performing will be the company’s ability to

a) grow its high margin, high premium food portfolio profitably and increase its revenue share (currently foods share is 20%, including the acquired food brands from Patanjali), by removing distribution bottlenecks - expanding the network, and leveraging ‘Patanjali’ brand. Company aims to increase share of food portfolio to 50% in the next few years

b) improve margins by enhanced operating efficiency and increasing palm plantation acreage and output

c) grow exports

d) Increase market share, profits and margins in nutraceuticals

Key Question, I am trying to figure: is the company a FMCG major in the making – by increasing share of foods and nutraceuticals in business. Can it improve ROCEs such that the stock can re-rate

Disclosure: Taken a tracking position

Patanjali Foods.docx (394.9 KB)

3 Likes

If you read the National Edible Oil Policy, The focus is primarily to reduce the dependency on Edible Oil Imports. Patanjali intends to become the largest Palm Oil plantation company in India and thereby the largest Palm Oil trader/seller. They have been allocated 6 lac hectares of land. They have started their new project in Arunachal Pradesh on roughly about 38000 hectares

(Patanjali Foods has committed itself to Government’s NMEO-OP program and plant to undertake large-scale cultivation of oil palm plantations on 5 lakh ha area in India; out of which 3.2 lakh hectare area will be in North East region. Patanjali’s NE Oil Palm Program will immensely benefit the state’s economy for over the next 30 years, key benefits include: avg annual production of around 7.5 lakh MT palm oil, saving of about Rs. 10,500 crores of forex outgo annually and employment generation for nearly 5.8 lakh persons)

They are targeting 7.5 lakh tone in 30 years, which translates to roughly 1.25 lakh tonnes in 5 years if everything goes as planned. The share of palm oil in the overall business will keep on increasing and hence i believe this will remain an essential commodity business with an FMCG tag name. THe other FMCG products will definitely bring value to the business however it remains to be seen how they scale the FMCG business and if it can become a big share in Patanjali Foods.

Even if they reach their target of 7.5 lakh tonnes in 30 years, they will only be able to fulfill 10% of the total current Palm OIl Imports. This opportunity is huge if they can scale it up and deliver.

4 Likes

Patanjali Foods to offload 6% stake as per SEBI rules, they have time till December.

1 Like