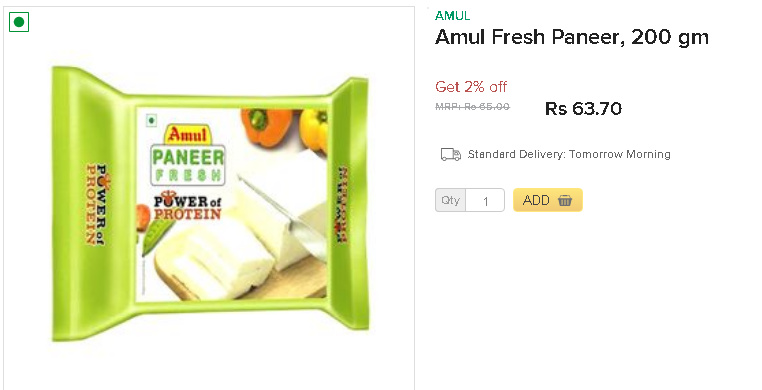

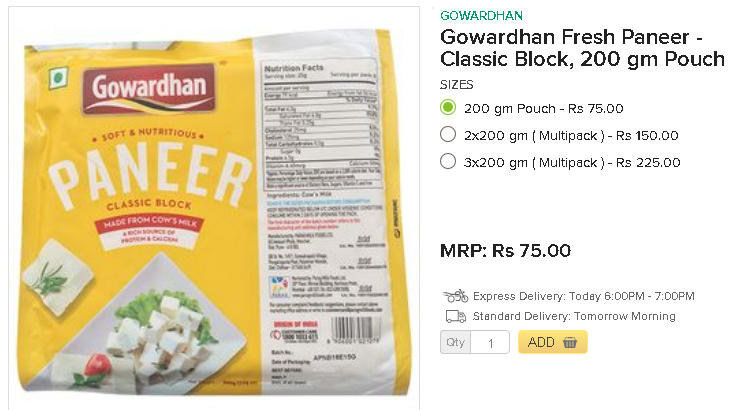

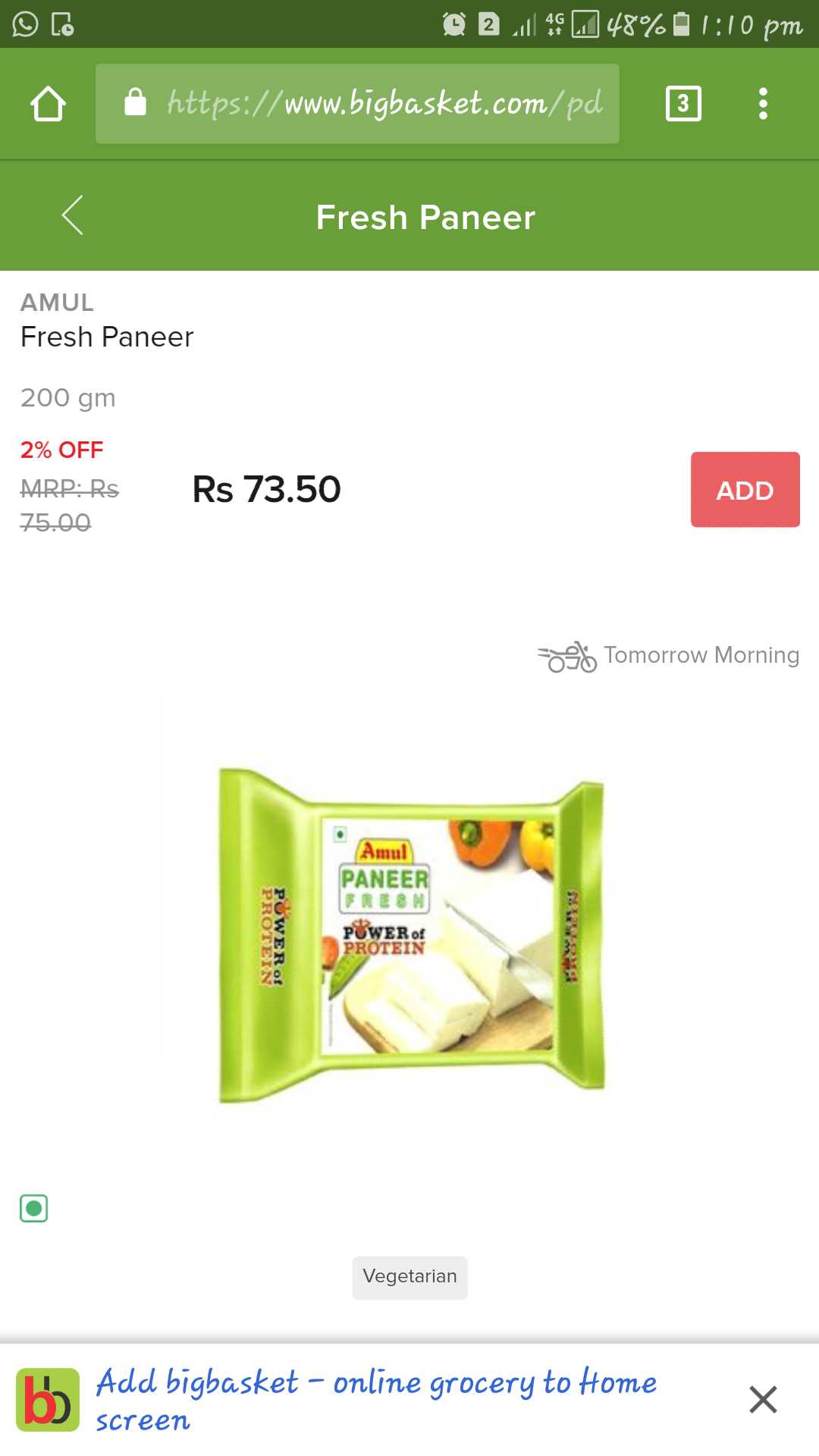

Amul paneer has shelf life of 6 months while gowardhan paneer has shelf life of 75 days. I can’t see why a shopkeeper (or anyone else) will prefer Gowardhan Paneer instead of Amul paneer when Amul paneer has higher shelf life and lower price. Even amul has strong network compare to gowardhan. What is the product differentiation for Gowardhan paneer. (In terms of nutritional value, Gowardhan paneer has 2 gm more protein per 100gm compare to Amul paneer but it has also higher cholesterol.)

Same goes with Avatar whey protein. It is even expensive than “ON” whey protein (premium one in whey protein segment) and “ON” has higher nutritional value and stronger distribution channel compare to “Avatar”. What is the product differentiation. And why anyone will prefer avatar compare to ON when ON has high brand value and lower price.

One differentiation is the pilot project they have started earlier in Borivali, Mumbai. This is good initiative but it has their own pros and cons… Pros are - This can boost sales to an extent as retaile shops will prefer to have a little stock with more churning as they will get to earn more with low investment. Cons are it will increase the cost as the frequency for distribution will increase. Also, it will be conducted in metro cities like mumbai only. So don’t know the real impact of this.

Now second possibility is, they might be providing higher margins to retail shopkeepers. This might be the reason why retail shops will promote PMFL products and thats why it might be priced higher. This is need to be checked if they are providing a higher margin to sellers.

Also, can anyone check through their networks if possible that at what rate Amul and PMFL provide cheese and paneer to other businesses like dominos, MacDonalds, and other hotel chains.

Reg. Vector’s help to better there distribution reach and product freshness, detailed information has been provided in q4 concall. You can also check vector website and go through presented case studies. It is being tried in Mumbai and will be scaled if found useful. Key is to incentivize distributors to go deeper but more frequently. Costs will increase but return on capital may improve due to lower inventory and stuff.

99% of whey protein (sports nutrition) is being imported currently. Parag claims to be the only facility in India making whey from fresh cow milk, which is sugar free, vegetarian product. Other imported whey products are usually made up of rennet (non-veg source).

Avvtar

ON

5.5 grams of naturally occurring BCAAs

4 grams of naturally occurring glutamine and glutamic acid

24 gr Protein

Overall, if you check customer reviews on Amazon or ask gym trainers (who determine what product gets recommended to their clients), Avvatar reviews have been extremely satisfactory. Few of my friends who have first hand experience with Whey said Avvtar tastes better and is more soluble than ON. Anyways, a lot can be subjective here, but the thing is that there are many differentiators here; at same price point, the product from Parag looks better in terms of BCAA and acids. In addition, appeal of being made from 100% vegetarian sources is big.

Nice @Mridul … You have got valid points and valuable information. Thank you for sharing.

I don’t know why it is showing different price for same product, but I would request you to check for both the products from same source… This different could be because of different prices in different locations… I was checking from mumbai… Check for the gowardhan paneer from same source too… or else, I will check from the store nearby too…

I think there is misunderstanding… I have read that too… but I was talking from the retail sellers point of view… If I would have been retail seller of paneer, I would have choose the stock which lasts long, has better brand value(No doubt Amul has upper hand in brand value) and will be cheaper…

PMFL said that customers will by fresh. So even Amul provides fresh, infact Amul will have high churning as it has higher sales. (For this try to visit any mall and check the manufacturing date) so it will be churned more frequently and will be more fresh as new stock comes. That may be applicable to Parag milk too but given the same price with same freshness and same quantity, I think customer will prefer the thing with good brand value (Where Amul has upper hand) and trust. I would request your view on this.

On the other things… on pilot project, we will need at least one or two more quarters to come to a conclusion, so I am not taking any view on this as of now. and from Avatar protein, I agree with you. This is 100% made from cow milk. That is differentiation.

Lets make it constructive. I would request your view on Cheese too and we can compare this with mother dairy too. This will boost our confidence on stock.

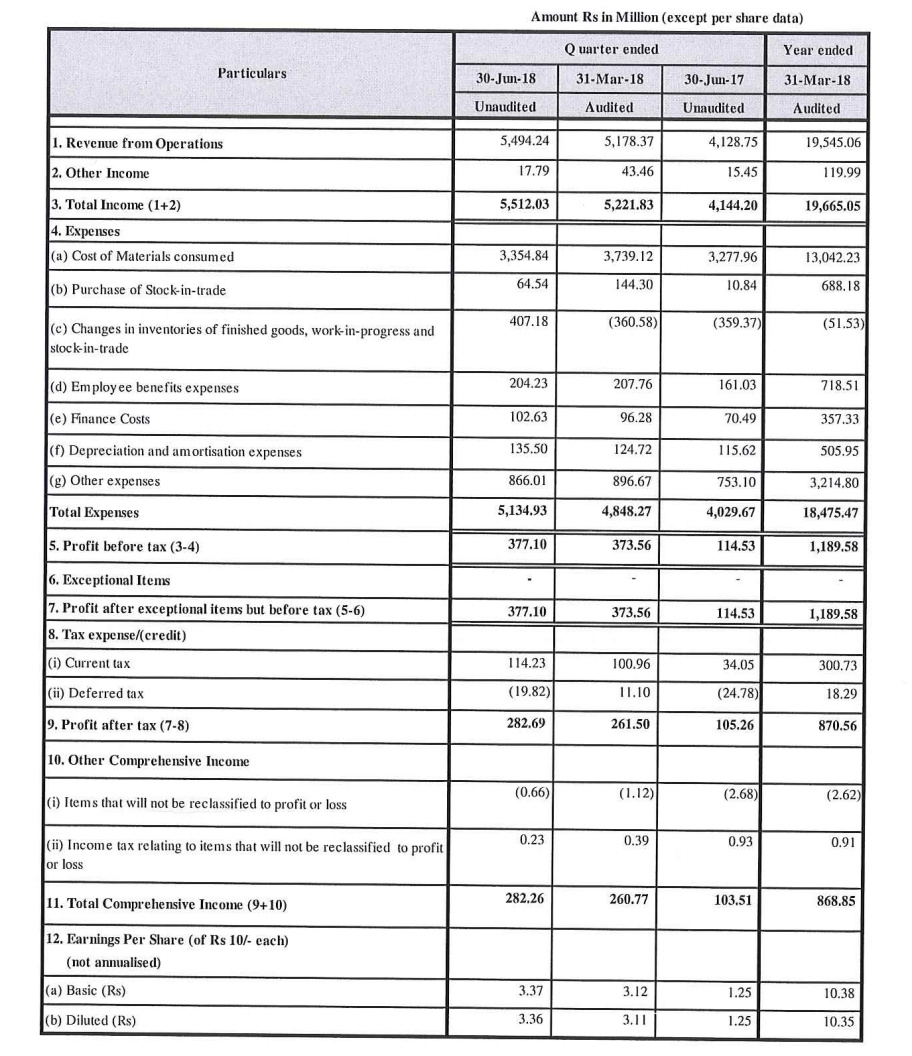

33% inc in revenues and 172% rise in PAT YoY. QoQ as well there is a steady 6% and 8% rise in revenues and profits. TTM P/E drops to 26 from 30. OPM up from 7.12% to 11.20% (YoY) and about 50 bps QoQ.

Parag has announced the launch of Gowardhan Mishti Doi, a premium product under the fresh product category.

Parag has also launched a new variant in whey protein called Advanced Muscle Gainer under the brand Avvatar.

Parag has also introduced Go Colo Power, the first 100% natural immunity booster in the health and nutrition segment. This product has made from Colostrum, which is the first milk of a cow when she gives birth to a calf and it is rich in immunity boosters. We have collaborated with ColoPlus AB a Swedish research organization to launch this product under their patented recipe. Colo Power will be available in e-commerce platforms and in all metro cities in a 200 grams pack

Strengthened our cheese category with the launch of Go Chocolate Cheese under Cheese Slices.

Commenced third manufacturing facility in North India post acquisition of the facility from Danone Manufacturing Foods and Beverages in Haryana in Sonipat. Completed all regulatory requirements and have commenced the supply of fresh curd to the nearby markets in Delhi NCR. Looking at expanding this facility further by adding a few more products lines.

Government of Maharashtra has fixed the procurement prices of milk at Rs.25 per liter, which is a win-win situation for both farmers and us. Government is taking positive steps towards the industry by offering Rs. 5 incentive to farmers through manufacturing companies like us for next 3 months.

Subsidy is not for the entire procurement. It is only for the value-added products, which are made in Maharashtra. So pure milk business there will not be any subsidy. But then those who are in pure milk business they will still have to pay Rs.25 but they will not get the Rs.5 benefit from the government.

The government has also announced that they will be providing a 10% subsidy on the export of milk and milk products. We believe that this move will boost dairy export from the India which has dried up in the past due to suppressed global prices. Parag is well placed to benefit from the same which will lead strong double-digit growth in exports. Parag exports are currently around 3%. They do not do bulk export and only export their value added products on B2C model.

No Capex in next one year and a half. Only investment which we are now making is one in Sonipat plant and a maintenance capex but no capacity enhancement outside of Sonipat plant. 60% of the 30 cr capex in Sonipat plant has been expended till now. So depreciation charge will remain at current levels.

We should be able to generate around Rs.60 – 70 Crores from curd segment from Danone facility.

For FY2019 tax rate will be in range of 26-28%.

The overall milk, which we would have handled and processed broadly on an average will be closer to 12.5-13 lakh liters a day and I think last year we were about closer to 10- 10.5 lakhs.

Sales from health and nutrition will be 7% of sales by FY21 and margins in Whey are better than what we are doing now. Currently it’s around 2.5% of sales.

Basically we have improved our distribution across India, 30 - 35% of the total growth has come from the distribution expansion, 65-70% is because of the improved demand from the market as we have our brands already established in the market. We have just started our distribution expansion, so I think in coming two quarters the result will be more because of the distribution.

Advertisement and Marketing would be around 8-8.5% of Sales where ~6% is used at the trade level and 2.5% is used for the direct A&P spends. Avvatar is a niche category and we spend a lot on influencers and social media and the amount is small. The target audience can be easily captured through Gyms and selective websites. When it comes to slurp, we wanted to keep the brand completely different from milk. The perception of a Mango drink is supposed to be refreshing. We have created premium brands for the milk category and by combining different products in one brand we don’t want to have a rub off effect on our products. For Slurp we do a lot of outdoor and trade related stuff and it is helping us in distribution of our other milk-based beverages like ToppUp, buttermilk and lassi.

Debt at the end of quarter was Rs. 264 cr.

We as of now are covering approximately 2.6-2.7 Lakh retail outlets and our target is to add about 9,000 to 10,000 outlets a month on distribution front.

In terms of our product categories, our milk Products category overall would be between 28% and 40% gross margin, skimmed milk power would be anywhere between 5% to 7% and liquid milk is anywhere between 10% to 12%.

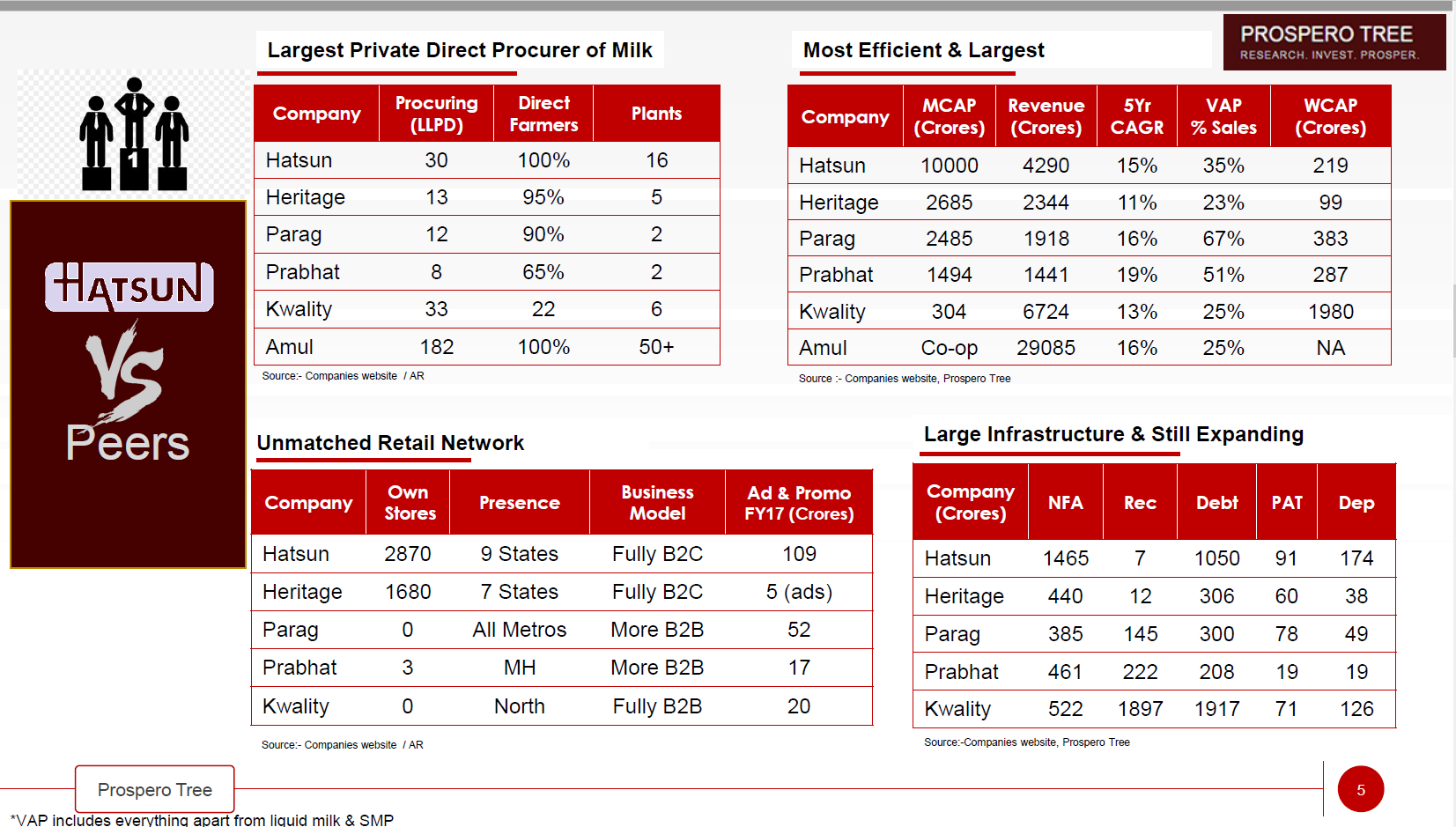

Excellent presentation on the dairy sector opportunity from Dhruvesh Sanghvi with focus on Hatsun, presentation here

I specially liked the Peer Comparison - Parag is very well placed on VAP but the high receivables and high WCAP will be a dampner as discussed earlier too in the thread

Just one correction/addition to what has been presented in this report - Parag has been spending 8-8.5% on advertisements and marketing (6% is used at the trade level and remaining is used for direct A&P spends). Though, other companies might be doing this in some way, which i am not aware of.

Parag Milk Foods Ltd FY18 AR Notes

Management is quite positive for the next two years. Management’s focus is on increasing share of consumer products in the portfolio, through distribution expansion and launch of innovative value added products. They want to place the company as a FMCG player instead of a commodity player (Not fully convinced by this as company was unable to pass on the sudden increase in Milk prices to end customers in FY17). Shift from unorganised to organised, changing preferences towards health consciousness and value added products, greater per capita income and Urbanisation are all good signs for the dairy industry in medium to long term. Company has been constantly launching new products and managing it’s inventory quite well, inventory days reduced from 91 days to 81 days. On debtors front we need more clarity from the management as debtor days increased from 36 days to 46 days and also provisioning for doubtful debts is quite high. Following are the highlights from the AR.

3 manufacturing plants. 9 milk processing and packaging units. 1 State of the Art dairy farm. 2.9 mn litres per day milk processing capacity. 7 brands. Currently we have 250000+ retail touch points, 3000+ distributors, 140+ super stockists and 17 depots.

Capacities

Milk: 2.9 mn litres per day.

Cheese: 60 MT per day

Paneer: 20 MT per day.

Ghee: 110 MT per day.

Whey: 6 lakh litre per day.

Company recorded a Consolidated Revenue of Rs. 19,545.1 million for FY18 as compared to Rs. 1,7307.4 million in FY17, representing a growth of 12.9%. Growth in revenue was driven by a growth in the consumer products category, mainly in value added products like cheese, paneer, and ghee.

EBITDA witnessed a growth of 594 bps from 683.2 million in FY17 to 1,932.9 million in FY18. The EBITDA Margin stood at 9.9% for FY18 driven by operating efficiencies.

Profit after tax on consolidated basis was 870.56 in comparison to 47.56 million in the previous year on account of gross margin expansion and operational efficiency.

BDFPL’s (Bhagyalaxmi Farm) total revenue Stood at Rs. 832.45 Mn in FY 17-18 in comparison to Rs. 517.98 Mn in FY 16-17. BDFPL made Profit Aft er Tax of Rs. 85.78 Mn for FY 17-18 in comparison to Rs. 65.19 Mn in FY 16-17.

The consumer products category, which is the largest revenue generator for the company, witnessed a 15.7% growth YoY, rising from Rs. 11,079 million in FY17 to ` 12,818 million in FY18. Share of consumer products increasing from 64.0% in FY17 to 65.6% in FY18.

The share of Fresh Milk, Skimmed Milk Powder and other revenue (category which includes the conversion income from the job-work done for others) was 19.9%, 12.9% and 1.6% of total revenues for FY18.

Exports consisted of 3.1% of the revenue mix.

The Company has a strong presence in the urban parts of West and South India and is currently the largest private player in Mumbai, the second largest private player in Pune and amongst the top players in newer markets like Bangalore, Hyderabad, Chennai and Nagpur, among others.

To strengthen the presence in north we have acquired the manufacturing unit of Danone Foods and Beverages India Pvt Ltd., the local entity of French dairy firm Danone SA. The plant is spread across 5,500 square meters on the outskirts of Delhi NCR. Its current milk processing capacity is 0.75 LLPD (lakh litre per day) along with curd processing capacity of 15 tonne. Initially we have associated with over 2,000 farmers (to procure cows milk) and we will keep on adding to these numbers going forward.

We made investments to increase our capacity in cheese from 40MT to 60MT per day. Also expanded our Paneer capacity by five times to 20MT per day by installing a fully automated paneer unit.

Company also appointed a consulting group to optimise its distribution model through the concept of ‘Theory of Constraints’. It allowed the Company to improve the distribution reach with lower stock outs, reducing non-moving inventory and better rationalisation of inventory at dealers, retailers and the company level. The roll out of SFA (sales force automation) and DMS (distribution management system) will further strengthen the distribution network.

Vision 2020 - Annual revenue of Rs. 2700-3000 cr, EBITDA and ROCE of 11-12% and 18-20%. With the support of the new senior leadership team, we are aiming at a double digit growth this fiscal.

Advertisement and Sales promotion expenses remained almost same at Rs. 52.6 cr at 2.74% of sales.

Provision for Doubtful debts of Rs. 16 cr in FY18 and Rs. 28.8 cr in FY17.

Loans increased from Rs. 262 cr to Rs. 290 cr.

Promoter holding increased slightly from 47.48% to 48.71% during the year.

New Launches

To strengthen the company’s presence in north region, we have introduced fresh dahi. With this launch, we have expanded our geographical reach and have entered into ` 1,500 cr curd market of Delhi. The Northern region contributes ~33% of curd consumption in India.

addition of Mishti Doi to our product portfolio will further build up the Gowardhan Dahi category.

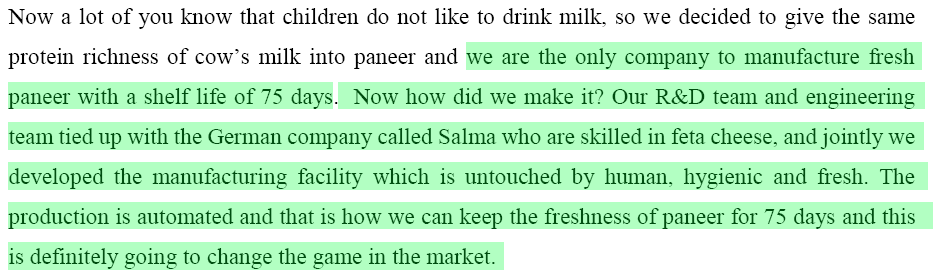

Launched Gowardhan Paneer as a fresh paneer category with a shelf life of 75 days and is made from 100 % cows’ milk. Being the 1st mover, we intend to create Branded category of fresh Paneer and rule the market as category leader. It is unadulterated and despite of 75 days of shelf life, it is free from preservatives and additives. This is the only product which has used ESL technology.

Launched G0 Cheese Cubes and Go Chocolate Cheese this year.

Under Avvatar brand launched Advanced Muscle Gainer which is the 1st Gainer in India to get Informed-Sports certification from WADA approved lab in UK confirming that it is banned substance free making it a perfect product for consumers and athletes.

With the launch of its first 100% natural immunity booster called ‘GO Colo Power’ in July 2018, the Company has further strengthened its offerings in the health & nutrition segment. Colo Power is made from the fi rst milk of cows just aft er calving and is enriched with immunoglobulins and probiotics and has the same goodness equivalent to that of a mother’s fi rst milk. The colostrum helps to build long-term immunity and improves and strengthens the digestive system.

Industry Data

The total industry size stands at approximately Rs. 7.1 trillion in 2018 (as per market realisations) and is projected to reach a value of Rs. 9.4 trillion by 2020.

In 2017 India’s milk production stood at 169 MMT, contributing to around 20.5% of the total global production. 77% of this production is retained by the producers for household consumption and the rest is available for commercial use. The milk production grew by 4.5% volume CAGR between FY10-16. In terms of value, the Indian Dairy Industry recorded an impressive 16.9% CAGR during the same time period with strong growth in organised sector.

The organized fresh milk market is growing faster than the unorganised market and is estimated to account for 26% of the total liquid milk market by 2020.

The organised Ghee market is very low at around 18-20% of total but is witnessing a CAGR of 17%.

The organized curd market is currently very low at ~6% of total market. However, it is witnessing a rapid CAGR of over 20%, with even higher growth in the metro markets. Current Curd volumes are estimated at around 3.2 million MTs and expected to reach 4 million MTs by 2020, translating to a market size of ` 50,000 crores. The Company also has a significant presence in major metros like Mumbai, Pune, Nagpur, Hyderabad, Bangalore & Chennai and is now expanding into Delhi NCR and nearby markets of North and East India.

Whey Proteins market is estimated at 35,000 MTs, translating into a market size of Rs. 3,000 crores, growing at more than 25% every year. The market today is evenly divided between sports nutrition and nutrition foods at Rs. 1,500 crores each.

Government Initiatives for dairy industry.

It plans to register 40 million milch animals with UID and issuance of health card, which will lead to 20% increase in milk production by 2020.

Government has also planned to allocate ` 200 crores in FY19 for the establishment of 20,000 plus self-employed dairy units, provide training to 4,000 multipurpose artificial insemination technicians and to introduce sex sorted semen technology of 1.5 million doses to increase the availability of high genetic merit heifers to increase milk production and profitability in dairy farming. The outcome of these factors and of these efforts of the Government would increase the value of output of milk by Rs. 15,000 crores along with additional employment to 1 lakh people and increase in artificial insemination by 15% over the medium term.

Further, in Union Budget 2018-19, Rs. 10,000 crore fund was allocated by the Government of India in for the upgradation and modernising of milk procurement, processing and marketing operations.

As you are expecting actual product feedback, here is mine… As a batchelor residing at Pune, am a frequent user of their milk and curd and we (me and flatmates) really likes it over other products available here including Amul… I havent used other products, bt the Dmart shelf is rich with Parag products.

I used to subscribe dailly their ‘Pride of cows’ milk (Rs 90 /litter) for more than 2 years. It’s A1 cow milk, delivered at door step (you can’t find it any retail stores as low self life). It’s really good product, but now we subscribed to A2 cow milk from another dairy. I called their centre to stop my subscription. They did it promptly but never anyone called me to try to retain me. That was a put off for me as an investor. I was buying 32k a year for their milk. Also they never tried to up-sell other products, given they had access to my doorstep. We regularly buy their ghee (Go brand) and Paneer.

Disclosure : Had a tracking quantity. Not holding.

Yes… This is not the way they should work… but given the share of pride of cows in sales… It is possible that they don’t want to focus much on that front… even the competition is not that steep in that segments… So I feel it should not necessarily raise the red flag…

Its really good that in north they are making their presence feel… I think in north they don’t have much exposure… but they are expecting it to icrease… waiting for Sonipath plant to be functional fully…