Worth Noting!

1 Like

Significant decline in the procurement prices, especially in Maharashtra, would aid the gross margin for dairy companies based in these regions – Prabhat Dairy and Parag Milk Foods

2 Likes

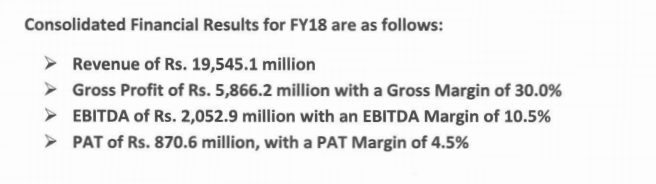

Performance for the whole year

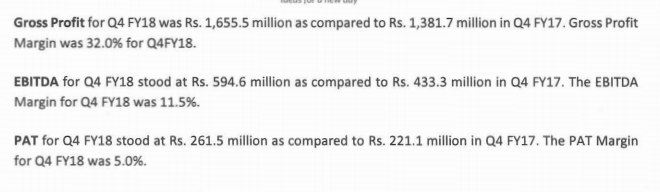

Performance for Q4

Looks pretty good. RoCE and RoE both should improve to 16% and 12%, going by my rough calculations.

At a EV/EBITDA of 26 and P/E of 28, this appears cheap, especially with Cheese market growing at 25% CAGR and with pure Milk plays (with better RoCE due to higher capital turns) trading at more than double valuations despite flat or shrinking bottomline.

4 Likes

This business got good potential, no second thoughts. But do you like the promoters here? How do you rate them on corporate governance? Promoter integrity? Shareholder friendliness? Do you see any red flags?

1 Like

As another member here pointed out - The remuneration for directors, KMP was 4.6 Cr in FY16 and is now 7.2 Cr in FY17 which is a sharp 56% increase - This doesn’t feel right at all. The contingent liabilities with the tax disputes, guarantees doesn’t reflect very well on governance. Is there anything else other than these? I guess these are reflected in the valuation as well.

Went to Analyst meet… Here are few updates from meet :

-

Management plans to achieve revenue of Rs.2.7-3bn by FY20, implying a CAGR of 18-24% with increase in EBIDTA margin to 11-12%.

-

Growth is expected to driven by value added product, scale up in health and nutrition segment and ramp up in overall distribution reach.

-

PMFL recently launched a sales pilot project in a select market where it distributed products more frequently with no minimum order size. It was focused on to providing fresh products to customer, increasing outlet reach, SKU range and driving sales value per day. This resulted into increase in reach by 200% and average daily sales also increased by 53%.

-

Given the pilot’s strong success, it now plans to extend the same to 60,000-100,000 retailers over next 6-8 months in order to improve sales productivity and overall efficiency of the distribution channel.

-

PMFL has tied up with “Alwa” to produce paneer with shelf life of 75 days. This process will be completely automated and untouched by humans.

-

It also extends its cheese portfolio with the launch of GO cheese targeting tier 2 and tier 3 cities.

-

In Ghee segment where it enjoys high brand value, it has plans to further premiumise the segment with the addition of Gowardhan Aurum super premium ghee at double the price of current product offering.

-

In health and nutrition portfolio, it is launching the nutritional product with the name “Go protein +” targeting pan India distribution.

-

PMFL planning to launch flavored curd “Mishti Doi” which is very popular product in East (west Bengal/ Orissa) and North.

-

To further increase reach in North, PMFL has acquired Danon facility for Rs.300mn. This will include setting up additional manufacturing units for pouch milk, flavoured milk, buttermilk and curd. The company is currently working on setting up a sourcing network. The acquisition allows it to leverage and strengthen its existing network and customer base in Northern market. The management expects revenue of Rs 1-1.2bn from this facility in FY19.

-

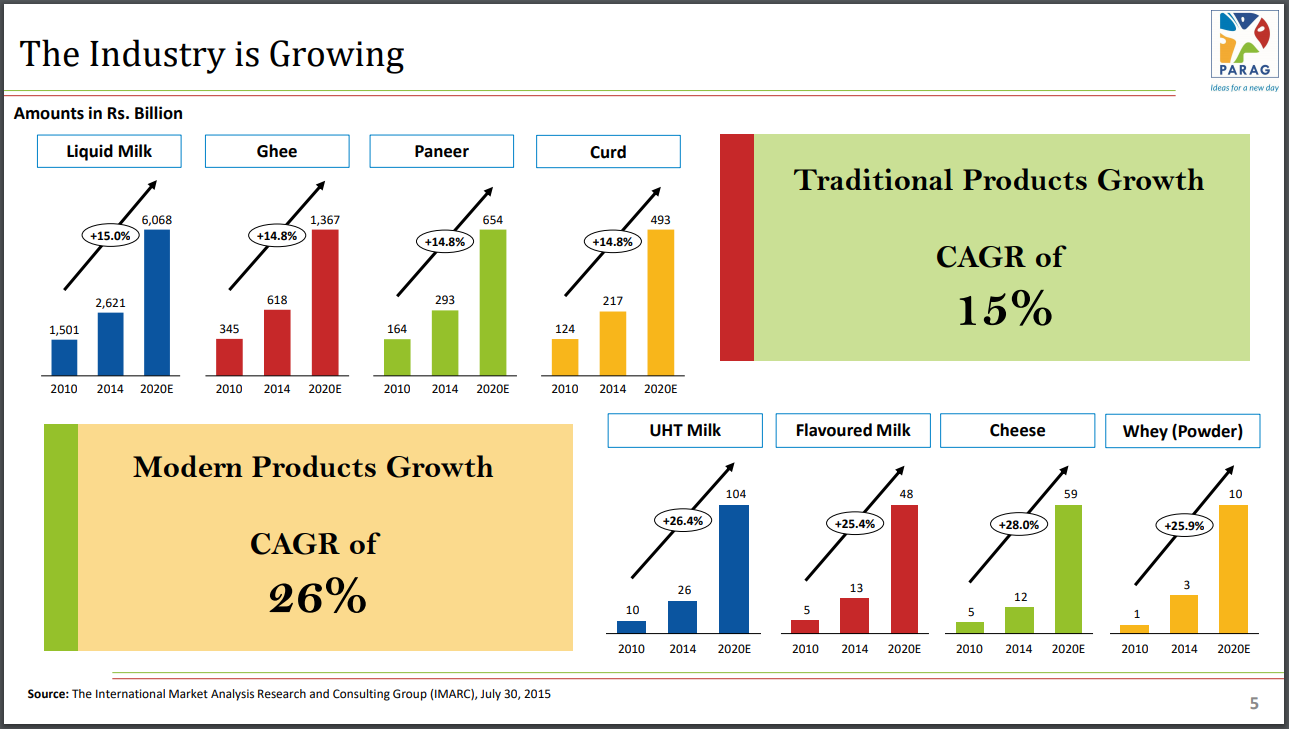

Traditional products like Milk, ghee, paneer and curd is expected to grow at 15% CAGR while other VADP (Value Added Dairy Products) like cheese, flavoured milk, etc. is expected to grow at 26% CAGR.

-

Market share of Parag milk in cheese market in India is 33% as of now, next to

Amul. -

Ghee is largest segment in the milk category

-

Intend to capture a major share of North India market in Paneer segment.

-

Company have started manufacturing cow dung base organic fertilizers with realization of INR 6/kg.

-

Company intends to focus on e-commerce with tie ups with portals like Amazon, big basket, grofers, others.

My view :

Rising innovation and technology driven process improvements, increase in portfolio with premium products like “Aurum super premium ghee”, addition of products in healthcare portfolio like “Go Protein +” & muscle gainer, acquisition of Denon facility to leverage their reach in North along with the professional management team in place, this provides me greater visibility to PMFs earning trajectory. Hence, I believe the 18-20% CAGR sales growth projection by management for two years is achievable and with the increase in VADP products and addition of premium products I expect PAT margins to sustain above current level of 4.50%. (Management has no major plans for CAPEX). Hence, I value business at 35x earning FY20 (sales 2700 and PAT margin of 4.50% conservative) for the target of 505.

Sensitivity analysis :

analysis:

I did the sensitivity analysis according to sales and margins projected by management and I came at valuation in different scenarios as below:

Best case | Mean | Worst case

Sales projected 2700 2850 3000

Best case 505.60 533.67 560.00

mean 385.20 406.60 428.00

worst case 280.90 300.00 312.00

Key variables considered in sensitivity analysis:

PE: Current: ~30.

- Best case: 35

- Mean: 30

- Worst case: 25

PAT margins: Current: ~4.50% - Best case: 4.50%

- Mean: 4.00%

- Worst case: 3.50%

1 Like

Recommend reading this report if you want to understand the dairy sector in depth. A key factor that is affecting Indian dairy sector, apart from the local factors, is international SMP price dynamics. SMP does get shipped easily and is a swing factor that affects prices worldwide. What seems to be a local demand supply driven product is affected by global dynamics at the margin.

14 Likes

Beautiful piece of research, thanks for sharing. A combination of globalisation, organised retail and capitalism has collectively skewed milk production and consumption. I don’t think this is restricted to just the milk business though and this disruption in the last 10 years has been at play in a lot of sectors.

A lot of capacity gets built in a growing market, growing market encourages consumption, as the scale gets bigger and bigger, more players jump in and try to grab a larger market share, then comes the painful consolidation where only the largest and toughest survive due to economies of scale while the small ones who unwittingly participated in the early stages get assimilated/crushed by the behemoths. Globalisation makes the whole world a market and capacities that get built in one place to serve the whole world can get adversely affected by policy changes in another country and consequently the whole sector in the country undergoes pain.

I think instead of SMP which gets converted back to milk by recombining with butter fat, slowly more and more milk will be converted to Cheese and the per-capita consumption of Cheese will go up because capitalism causes these consumption patterns. I doubt if much can happen in terms of structural changes recommended in the piece. Keeping the business local and maintaining social and ecological resilience will take a lot of effort from the govt. The govt. will take the easy way out and throw money at the problem with a minimum support price causing further distortions in the long run, as they have done in the Sugar sector. Won’t be surprised if call for MSP comes from Shrimp farmers next if our marine product exports decline and prices crash. This mess is not restricted to just Milk unfortunately.

Again, thanks for the report. Its the best thing I have read today.

6 Likes

You’re welcome.

The document has been authored by a farmer interest focused NGO so if you wish, you can adjust for some bias. Overall, I found it pretty useful in any case.

Some more data on Indian SMP exports which crashed after the EU move. See page 24/72. This explains the pressure on prices in India:

LOK SABHA

UNSTARRED QUESTION NO. 1190

TO BE ANSWERED ON 7TH DECEMBER, 2015

http://commerce.gov.in/writereaddata/UploadedFile/MOC_635975493407970101_LS20151207.pdf

There are distortions already, from a capitalist viewpoint, in the form of cooperatives. Amul, KMCF, and others are not “profit-maximizing” in a capitalist sense. KMCF, in the last year, in the run-up to the Karnataka elections has been doling out extra to farmers and ensuring extra supply and collections. Some believe Maharashtra procurement prices have dipped, and they have, because of this cause.

SMP can be utilized in VAP / reconstituted milk. Whether capacities are right-sized will determine whether you still have surplus. Surplus can deliver profits/losses because it is more of a commodity.

2 Likes

Hi

RBI has notified a few days ago that NRIs can invest via PIS in Parag Milk Foods up to 24% earlier it was 10%.

https://rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=43967

More on investment by NRIs/PIOs/FIIs here https://www.rbi.org.in/scripts/BS_FiiUSer.aspx#PAR180518

Rgds

Deepak

3 Likes

Launched the Misthi Doi product I mentioned in earlier comments…

Parag Milk Foods launches Gowardhan Mishti Doi.pdf (813.8 KB)

Kraft Heinz - Earlier cheese and now complan… Does this denote difficulty for foreign players to do Dairy related business in India?

Thank you for your notes on the Analyst meet. Are you sure that the company that parag milk is “Alwa”? Because they gave a disclosure on BSE that they are going to acquire patents of a swedish company. out of the names available, I found Arla Foods to be the company. Reason behind clarification is that Arla foods is a very big dairy company with annual turnovers of 10.3 Billion EUR (in 2017). It’ll be easier to quantify the benefits if it actually is Arla Foods. This is my first time commenting, do let me know if I get wrong.

Disclosure: Not personally invested, but working for a family office that has invested.

Interesting snippet on the strong growth ahead in Higher end products from FY18PPT

3 Likes

Nice article for Dairy companies…Milking it right…

2 Likes

Go colo power… one more VADP by PMFL… They utilize everything from cow… first, they produced milk, then cheese from milk with some waste, then utilize this waste to form whey, they utilize cowdung also and now colostrum… earlier colostrum was going waste and now it will be sold at Rs.750 per 200 gram…

2 Likes

Investors complaints r generally in the nature of 1. Annual report not received 2. Dividend not received 3 . Share transfer etc which companies generally resolve asap. Institutional investors are taking interest in this Co. & meeting with different institutionals has been taking place for last 4-5 months to update about the future plans etc (pl. go through the past notifications posted on BSE site). Company is in expansion mode and launching new products & tie up with multinational company etc

2 Likes

Stock has moved from 279 to 305 within an hour after the news. What is the real impact of this on earnings. PMFL has 3% of exports revenue out of total revenue.

Parag milk foods ltd commence the danone acquired facility in north. Commenced the production of curd only… but will refurbish the plant for other products soon…

Parag milk foods BSE notice.pdf (674.4 KB)